24-1 general nature of homeowners program section i:property (this chapter) liability (covered...

Post on 20-Dec-2015

213 views

TRANSCRIPT

24-1

General Nature of Homeowners Program

Section I: Property (this chapter)

Liability (covered earlier)

24-2

Homeowners Forms

Five standard forms in most jurisdictions

HO 00 02 Broad

HO 00 03 Special Form

HO 00 04 Tenants Broad Form

HO 00 06 Condominium Unit Owners Form

HO 00 08 Modified Coverage Form

24-3

Homeowners Section I Coverages

Coverage A Dwelling

Coverage B Other structures

Coverage C Personal property

Coverage D Loss of use

24-4

Table 23.1Homeowners Forms

A: Dwelling $15,000 min. $20,000 min. Not covered $1,000 $15,000 min.B: Other Structures 10% of A 10% of A Not covered Part of A 10% of AC: Personal Property 50% of A 50% of A $6,000 min. $6,000 min. 50% of AD: Indirect Loss 20% of A 20% of A 20% of C 40% of C 10% of A

Fire Open Peril Same perils Same perils FireLightning coverage as Form 2 as Form 2 LightningWindstorm on Dwelling WindstormHail HailExplosion ExplosionRiot, Civil Same Perils Riot, Civil Commotion as Form 2 CommotionAircraft on personal AircraftVehicles property VehiclesSmoke SmokeVandalism VandalismTheft TheftGlass Breakage VolcanicFalling Objects eruptionWeight of Ice, snow or sleetDischarge or overflow of water or steamTearing apart, cracking, burning, or bulgingFreezing of plumbing, heating, etc. systemsDamage from artificial electric currentVolcanic eruption

Coverage HO 00 02 HO 00 03 HO 00 04 HO 00 06 HO 00 08

24-5

Homeowners - Perils Insured

HO-2, 4, 6 HO-3

Dwelling Named Perils Open Peril

Other Structures Named Perils Open Peril

Personal Property Named Perils Named Perils

Loss of Use Named Perils Named Perils

24-6

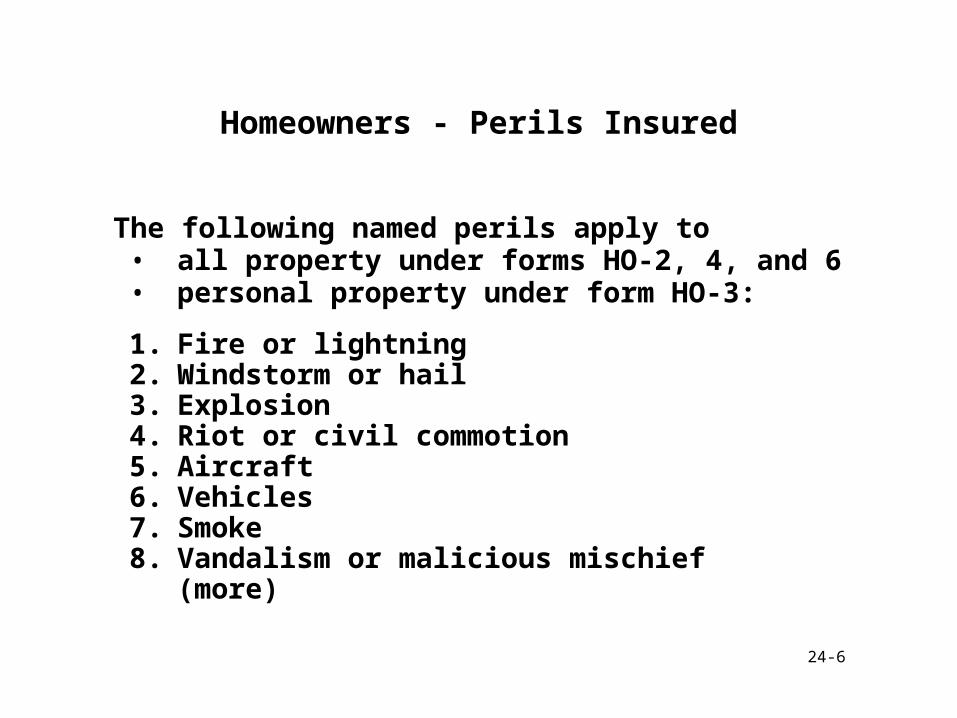

Homeowners - Perils Insured

The following named perils apply to • all property under forms HO-2, 4, and 6• personal property under form HO-3:

1. Fire or lightning2. Windstorm or hail3. Explosion4. Riot or civil commotion5. Aircraft6. Vehicles7. Smoke8. Vandalism or malicious mischief

(more)

24-7

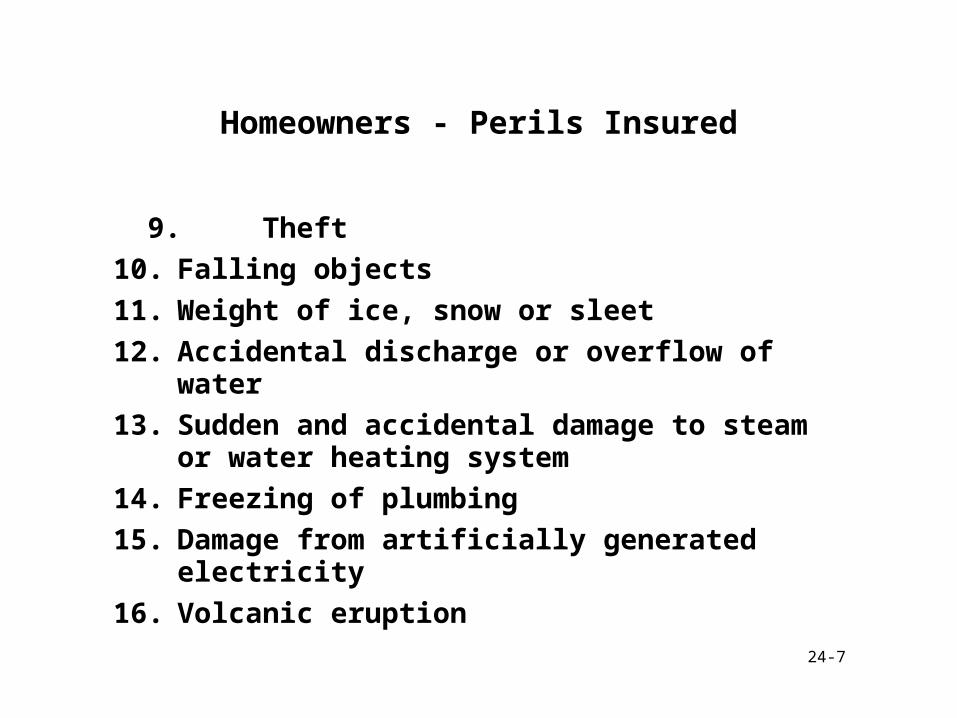

Homeowners - Perils Insured

9. Theft

10. Falling objects

11. Weight of ice, snow or sleet

12. Accidental discharge or overflow of water

13. Sudden and accidental damage to steam or water heating system

14. Freezing of plumbing

15. Damage from artificially generated electricity

16. Volcanic eruption

24-8

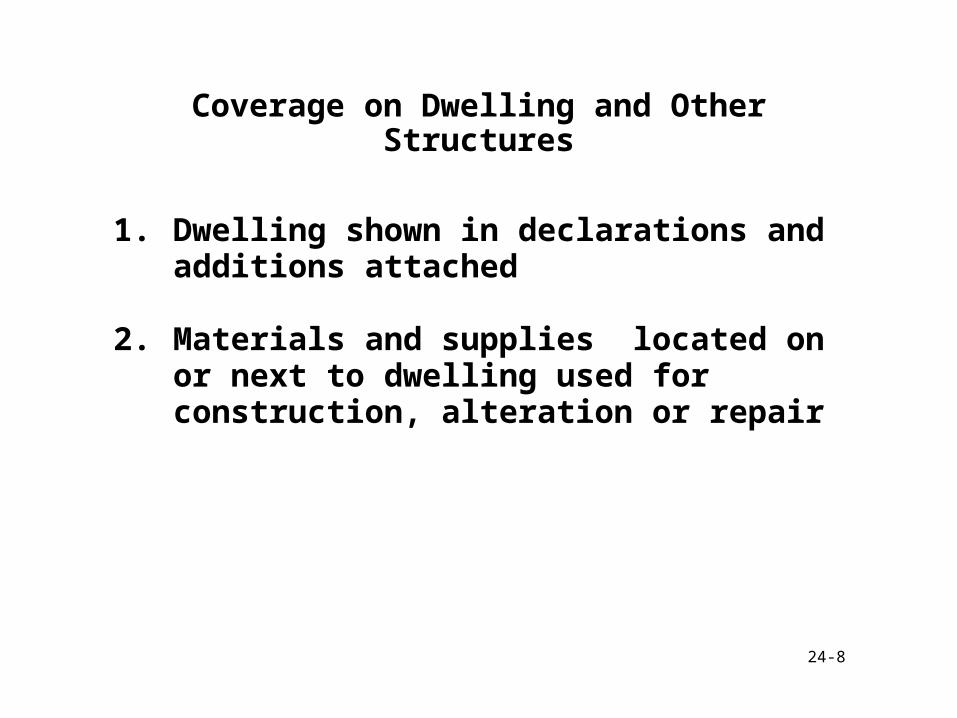

Coverage on Dwelling and Other Structures

1. Dwelling shown in declarations and additions attached

2. Materials and supplies located on or next to dwelling used for construction, alteration or repair

24-9

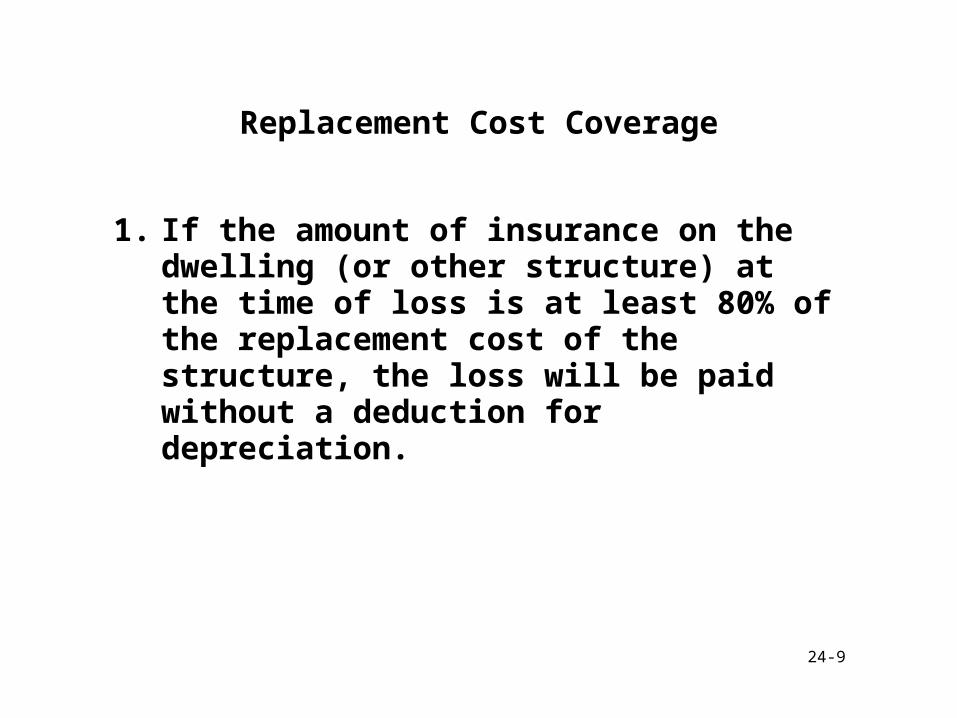

Replacement Cost Coverage

1. If the amount of insurance on the dwelling (or other structure) at the time of loss is at least 80% of the replacement cost of the structure, the loss will be paid without a deduction for depreciation.

24-10

Replacement Cost Coverage

2. If the amount of insurance is less than 80% of replacement cost, payment will be made for the larger of two amounts:

• the actual cash value of the loss

• the portion of the replacement cost of the loss that the amount of insurance bears to 80% of the replacement cost value of the structure

Payment will be made according to the following formula:

24-11

Replacement Cost Coverage

Insurance Carried on Building

Replacement Cost of Building X .80X Loss

24-12

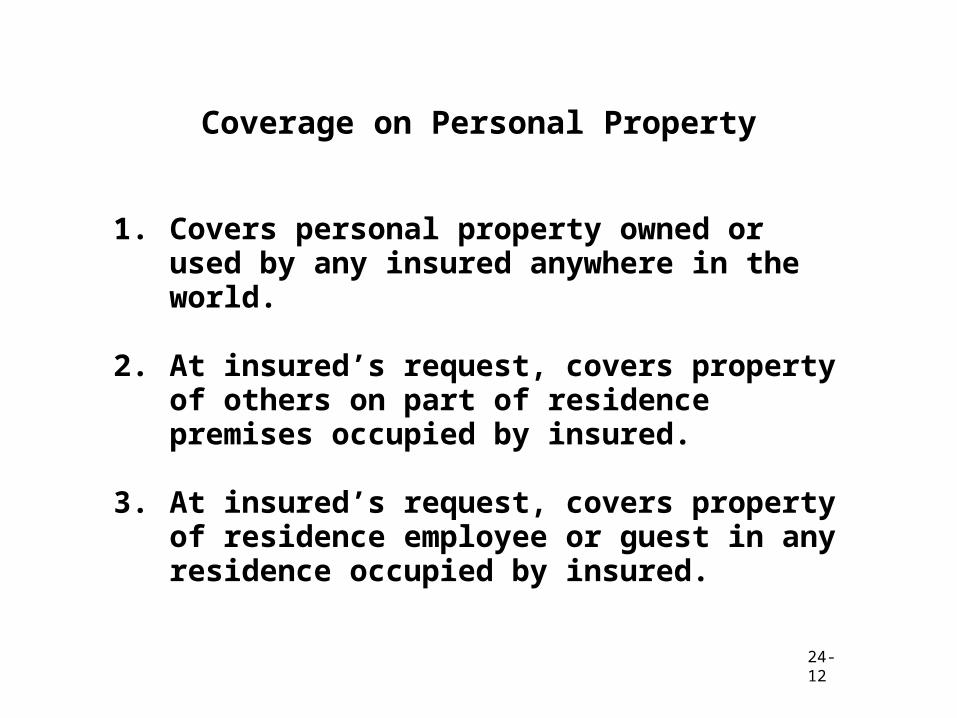

Coverage on Personal Property

1. Covers personal property owned or used by any insured anywhere in the world.

2. At insured’s request, covers property of others on part of residence premises occupied by insured.

3. At insured’s request, covers property of residence employee or guest in any residence occupied by insured.

24-13

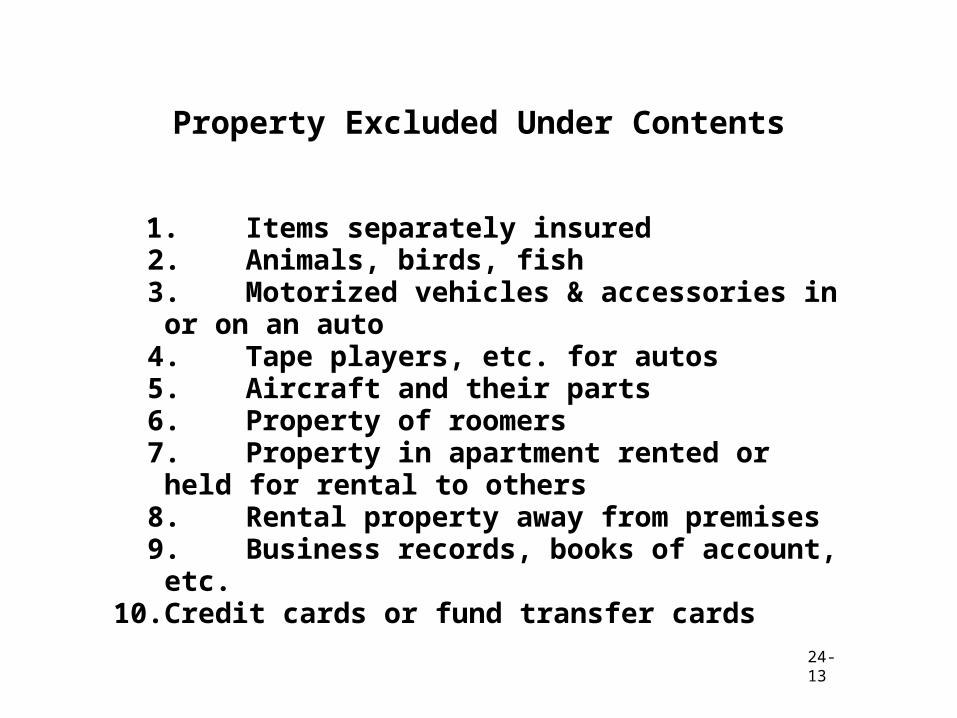

Property Excluded Under Contents

1. Items separately insured 2. Animals, birds, fish 3. Motorized vehicles & accessories in or on an auto 4. Tape players, etc. for autos 5. Aircraft and their parts 6. Property of roomers 7. Property in apartment rented or held for rental to

others 8. Rental property away from premises 9. Business records, books of account, etc.10. Credit cards or fund transfer cards

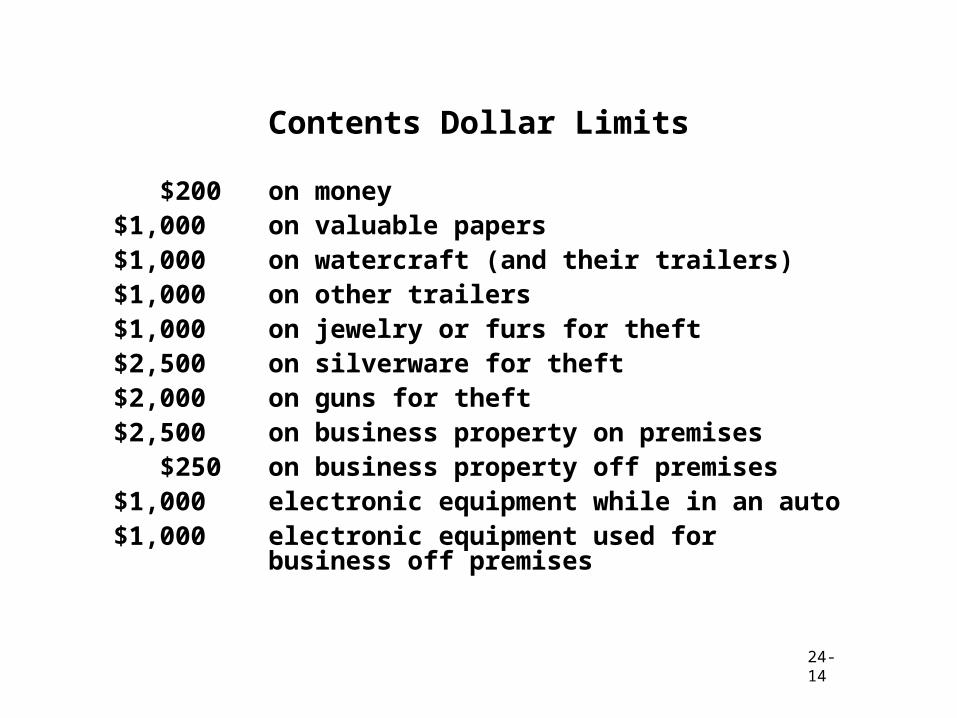

24-14

Contents Dollar Limits

$200 on money$1,000 on valuable papers$1,000 on watercraft (and their trailers)$1,000 on other trailers$1,000 on jewelry or furs for theft$2,500 on silverware for theft$2,000 on guns for theft$2,500 on business property on premises $250 on business property off premises$1,000 electronic equipment while in an auto$1,000 electronic equipment used for business

off premises

24-15

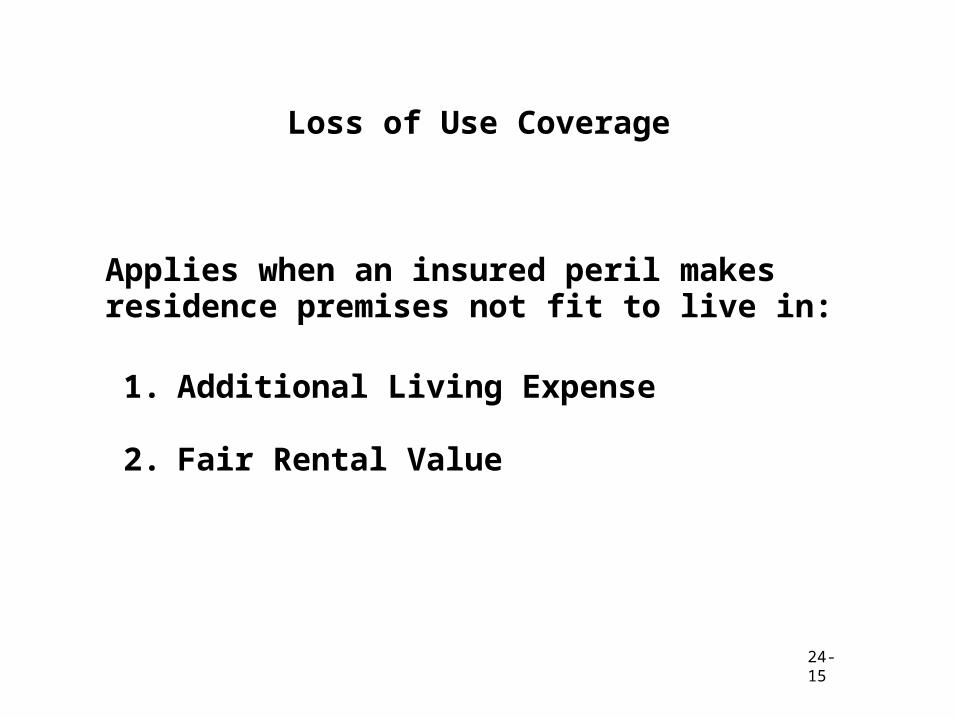

Loss of Use Coverage

Applies when an insured peril makes residence premises not fit to live in:

1. Additional Living Expense

2. Fair Rental Value

24-16

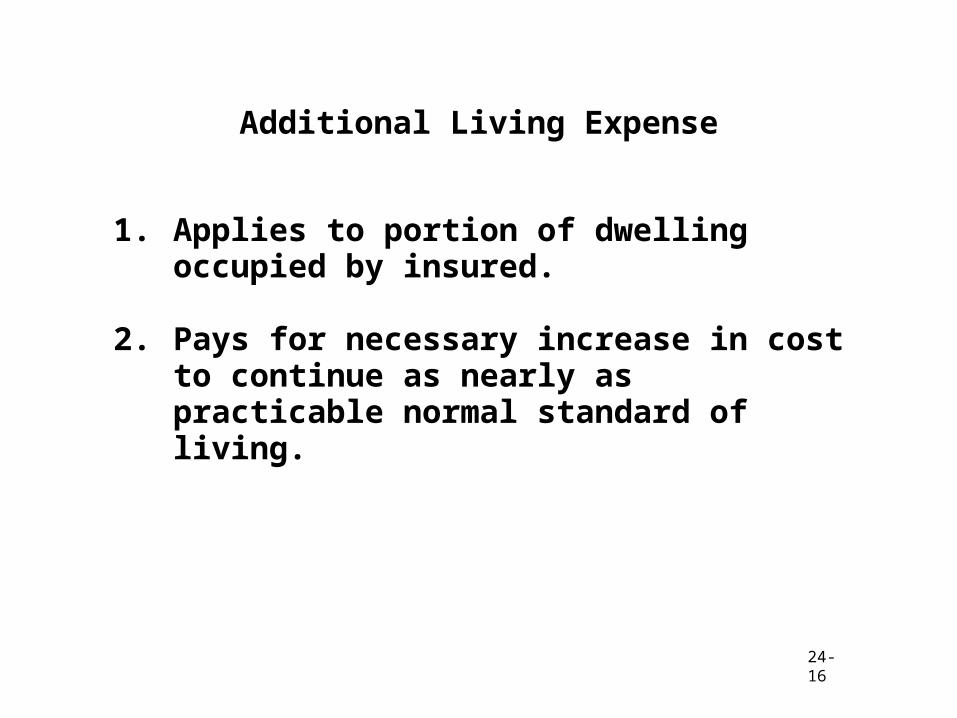

Additional Living Expense

1. Applies to portion of dwelling occupied by insured.

2. Pays for necessary increase in cost to continue as nearly as practicable normal standard of living.

24-17

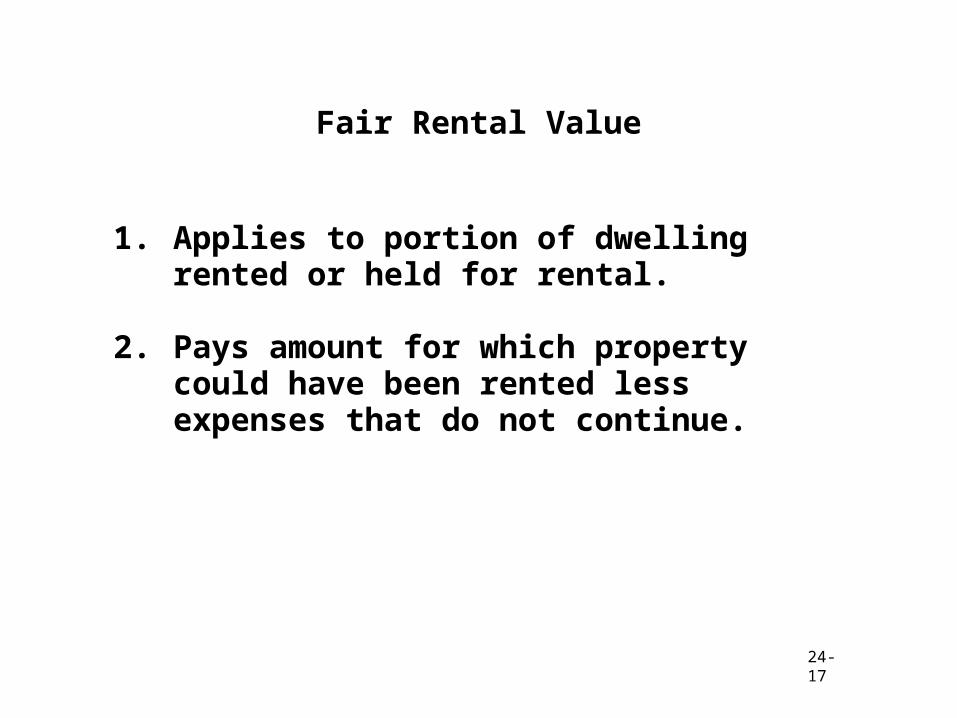

Fair Rental Value

1. Applies to portion of dwelling rented or held for rental.

2. Pays amount for which property could have been rented less expenses that do not continue.

24-18

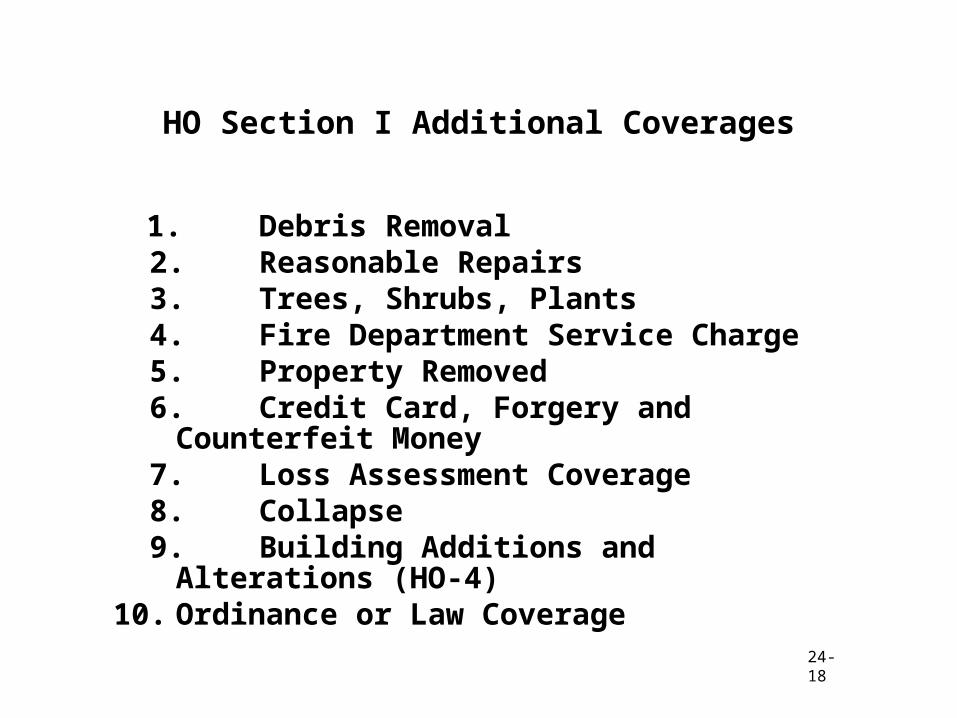

HO Section I Additional Coverages

1. Debris Removal 2. Reasonable Repairs 3. Trees, Shrubs, Plants 4. Fire Department Service Charge 5. Property Removed 6. Credit Card, Forgery and Counterfeit Money 7. Loss Assessment Coverage 8. Collapse 9. Building Additions and Alterations (HO-4)10. Ordinance or Law Coverage

24-19

Collapse

a. perils insured against in Coverage C

b. hidden decay

c. hidden insect or vermin damage

d. weight of contents, equipment, animals, or people

e. weight of rain on a roof

f. defects in material or methods used in construction, remodeling or renovation if the collapse occurs during the course of construction, remodeling or renovation.

24-20

Section I General Provisions

1. Insurable interest and limit of liability

insurer will not be liable for more than the interest of the insured

or

the limit of liability.

24-21

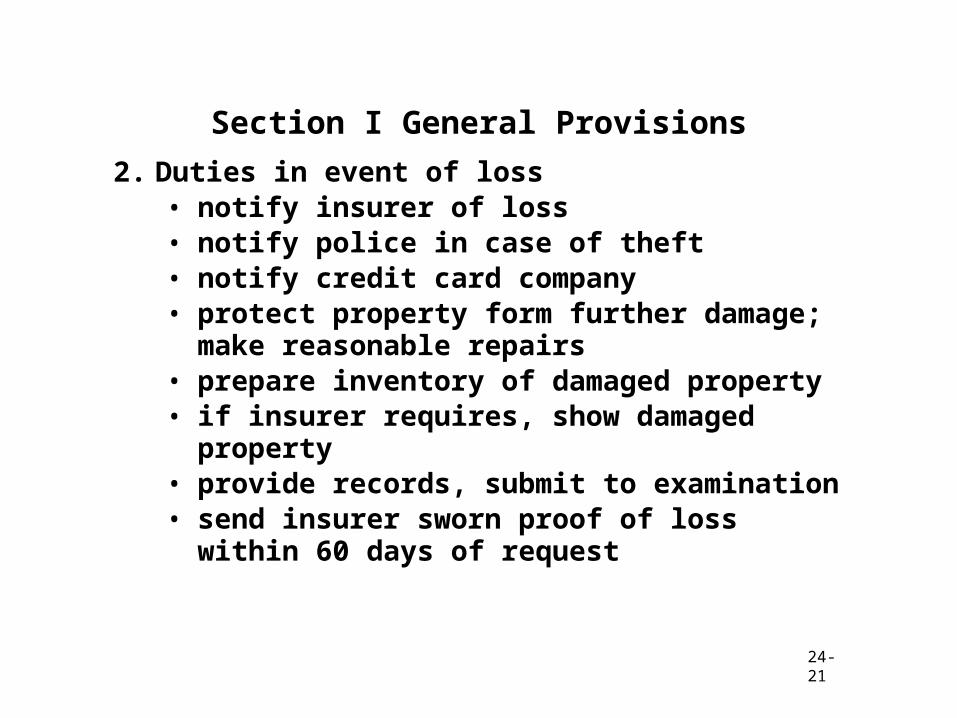

Section I General Provisions

2. Duties in event of loss• notify insurer of loss• notify police in case of theft• notify credit card company• protect property form further damage;

make reasonable repairs• prepare inventory of damaged property• if insurer requires, show damaged property• provide records, submit to examination• send insurer sworn proof of loss within 60

days of request

24-22

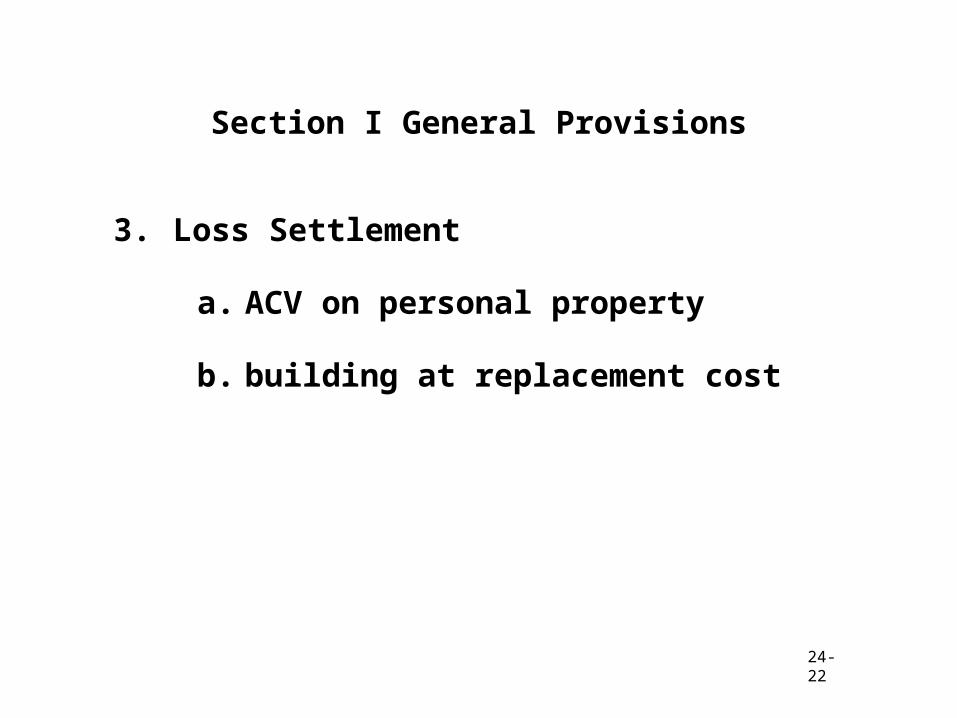

Section I General Provisions

3. Loss Settlement

a. ACV on personal property

b. building at replacement cost