2016 lea indirect cost application aasbo tuscaloosa, alabama february 11, 2015

TRANSCRIPT

2016 LEA INDIRECT COST APPLICATION

AASBO Tuscaloosa, AlabamaFebruary 11, 2015

Authorization

• The Alabama State Department of Education has been delegated the authority to establish Indirect Cost Rates for the LEA’s in Alabama by the U S Department of Education.

• The methodology currently being used was reviewed and approved by the USDE, Indirect Cost Group in 2014.

• Current agreement goes through September 30, 2019.

The Indirect Cost process is a method used to distribute allowable administrative costs that are paid from state and local funds to Federal Grants. This is a reimbursement process, not a revenue source.

Indirect Costs are costs that have been incurred for common or joint purposes. Indirect costs benefit more than one cost objective and cannot be readily identified with a particular final cost objective. Examples would be purchasing, accounting, and human resources.

Indirect Cost Rates are devices used for determining, in a reasonable manner, the proportion of indirect costs each program should bear. The indirect costs are included in the pool (numerator) and the direct costs are included in the base (denominator). The result is expressed as a percentage (rate) of the indirect costs to direct costs. Types of indirect cost rates are Provisional, Final, Fixed, and Predetermined.

Getting Started• Is your 2014 Financial Statement approved? The 2016 Indirect Cost

Application cannot be completed and submitted until final 2014 expenditures have been approved.

• Pull out your approved 2014 Indirect Cost Application (completed in the spring of 2013). Amounts from the 2014 application will be used on the fixed with carry-forward calculation page to compare the 2014 estimated indirect cost pool to the actual indirect costs incurred. If you cannot locate a copy, ask your system accountant to email you one.

Retrieve IDC Proposal Form From LEA Accounting Website

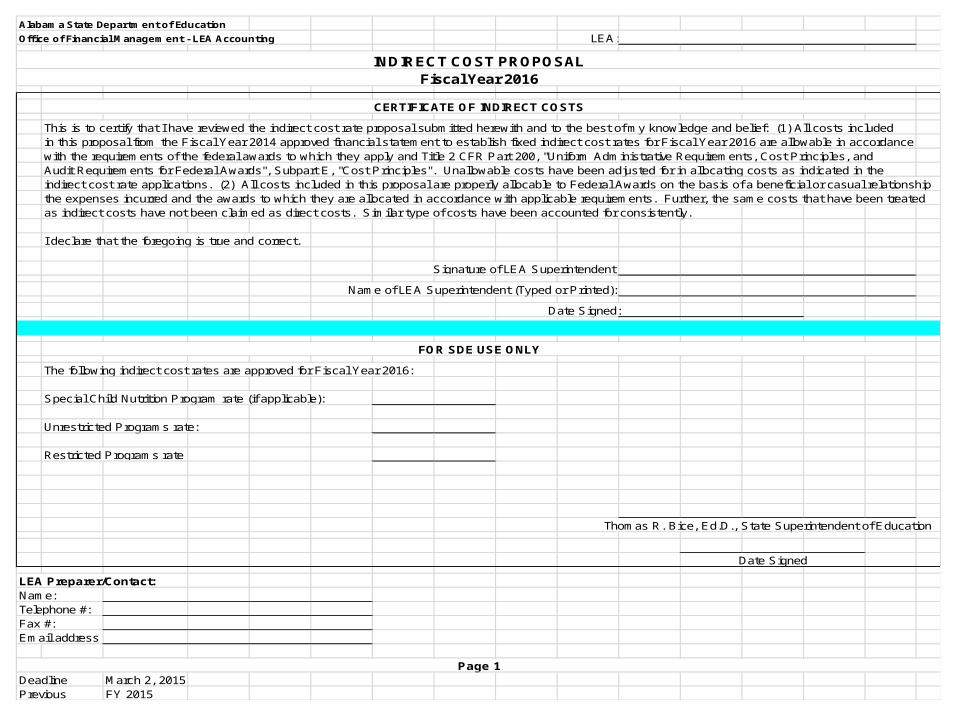

Alabama State Department of Education

Office of Financial Management - LEA Accounting LEA:

INDIRECT COST PROPOSALFiscal Year 2016

CERTIFICATE OF INDIRECT COSTS

This is to certify that I have reviewed the indirect cost rate proposal submitted herewith and to the best of my knowledge and belief: (1) All costs includedin this proposal from the Fiscal Year 2014 approved financial statement to establish fixed indirect cost rates for Fiscal Year 2016 are allowable in accordancewith the requirements of the federal awards to which they apply and Title 2 CFR Part 200, "Uniform Administrative Requirements, Cost Principles, andAudit Requirements for Federal Awards", Subpart E, "Cost Principles". Unallowable costs have been adjusted for in allocating costs as indicated in theindirect cost rate applications. (2) All costs included in this proposal are properly allocable to Federal Awards on the basis of a beneficial or casual relationshipthe expenses incurred and the awards to which they are allocated in accordance with applicable requirements. Further, the same costs that have been treatedas indirect costs have not been claimed as direct costs. Similar type of costs have been accounted for consistently.

I declare that the foregoing is true and correct.

Signature of LEA Superintendent:

Name of LEA Superintendent (Typed or Printed):

Date Signed:

FOR SDE USE ONLY

The following indirect cost rates are approved for Fiscal Year 2016:

Special Child Nutrition Program rate (if applicable):

Unrestricted Programs rate:

Restricted Programs rate:

Thomas R. Bice, Ed.D., State Superintendent of Education

Date Signed

LEA Preparer/Contact:Name:Telephone #:Fax #:Email address:

Page 1Deadline March 2, 2015Previous FY 2015

Alabama State Department of Education

Office of Financial Management - LEA Accounting LEA: Marshall County (048)

INDIRECT COST PROPOSALFiscal Year 2016

ORGANIZATION CHART FOR FISCAL YEAR 2014****

****Organization Chart must relate to expenditures incurred between October 1, 2013 through September 30, 2014.

If there are no changes from previous proposal, a photocopy of that organization chart may be included.

Page 2

Reports to Print from http://www.alsde.edu/leareports/

Under Optional Reports

•Unrestricted Indirect Cost Rate Data – Unadjusted – Fiscal Year 2014 Period 12

•Restricted Indirect Cost Rate Data – Unadjusted – Fiscal Year 2014 Period 12

(A) (B) (C) (D) (E)

Expenditures Expenditures Expenditures Expenditures Total All Fund

Excluded Not Allowed Indirect Direct Expenditures

$1,197,549.54 $25,229,108.81 $26,426,658.35

$154,077.68 $4,757,529.28 $4,911,606.96

$150,179.79 $3,531,149.11 $3,681,328.90

$370,300.99 $4,348,067.34 $932,291.28 $5,650,659.61

$2,262,820.70 $5,771,214.86 $8,034,035.56

$0.00 $64,862.42 $64,862.42

$14,900.00 $1,170,921.30 $253,646.83 $1,439,468.13

$10,128.00 $458,730.16 $0.00 $468,858.16

$0.00 $223,112.08 $0.00 $223,112.08

$0.00 $0.00 $0.00 $0.00

$0.00 $0.00 $0.00 $0.00

$0.00 $11,378.45 $0.00 $11,378.45

$0.00 $6,707.92 $0.00 $6,707.92

$0.00 $0.00 $0.00 $0.00

$0.00 $25,255.74 $0.00 $25,255.74

$340,047.04 $0.00 $340,047.04

$1,728,202.14 $0.00 $1,728,202.14

$554,678.00 $1,693,503.16 $2,248,181.16

$6,782,883.88 $6,244,172.99 $42,233,305.75 $55,260,362.62

$1,965,598.20 $1,965,598.20

$8,748,482.08 $6,244,172.99 $42,233,305.75 $57,225,960.82

(enter on B10) (enter on D10) (enter on E10) (enter on F10)

$1,780,443.17

$154,402.23

14.78%

Total Expenditures and Other Fund Uses:

Utilities (Object Code 370-379) Shown as Indirect:

Child Nutrition Utilities Paid Directly (Fund Source 5100-5199, Object Code 370-379):

Indirect Cost Rate = Total Indirect Cost (column C) divided by Total Direct (B) + Total (D)unadjusted rate - the rate based on the direct and indirect cost pools before expenditure adjustments

Capital Outlay (7000 - 7999)

Debt Service - Long Term (8000 - 8999)

Other Expenditures (9000 - 9899)

Total Expenditures:

Other Fund Uses (9900 - 9999)

Staff Services (6430)

Printing, Publishing, & Duplicating Services (6450)

Other Central Support Services (6490)

Central Office Services (6500 - 6599)

Other General & Central Support Services (6900 - 6999)

Board of Education Services (6100 - 6199)

Executive Administrative Services (6200 - 6299)

Business Support Services (6300 - 6399)

Information Services (6410)

Data Processing Services (6420)

Total Instructional Services (1000 - 1999)

Total Other Instructional Support Services (2000 - 2299)

Total School Administration (2300 - 2399)

Operation & Maintenance Services (3000 - 3999)

Auxiliary Services (4000 - 4999)

STATE OF ALABAMADEPARTMENT OF EDUCATION

LEA Financial SystemUnrestricted Indirect Cost Rate Data - Unadjusted

Actual Costs for Fiscal Year Ended September 30, 2014048 - Marshall County Schools

Function of Expenditure Account Codes

Expenditures Not Allowed column remains blank on the unrestricted report. The unrestricted rate are for those federal fund sources not subject to supplement/ supplant restriction

research any expenditure showing in the gray area. Account code 62xx normally contains allowable indirect expenditures.Research shows these expenditures are coded to federal fund sources which are never pulled to the indirect column. This expenditure is correctly placed in the direct column.

Expenditures coded to federal fund sources should never show in the indirect cost column.

enter on D36

enter on D39

Notes

(A) - Expenditures Excluded:

Local School Funds (Public and Non-Public) Fund Sources 7000-7999

Capital Outlay - Real Property Account Codes 7000-7999

Debt Service - Long Term Account Codes 8000-8999

Other Fund Uses Account Codes 9900-9999

Purchased Food Object Code 461

USDA Commodities Object Code 462

Food Processing Supplies Object Code 464

Equipment Object Codes 500-599

Other Objects Object Codes 600-619, 627, 690-899

Other Fund Uses Object Codes 900-997

(B) - Expenditures Not Allowed:

N/A for Unrestricted

(C) - Expenditures Indirect:

Operation and Maintenance Services Fund Type 11, Account Codes 3000-3999, Excluding Fund Sources 3000-5999 and 8000-9999

Operation and Maintenance Services Fund Type 12, Account Codes 3000-3999, Fund Sources 6000-6999

Executive Administrative Services Fund Type 11, Account Codes 6200-6299, Excluding Fund Sources 3000-5999 and 8000-9999

Executive Administrative Services Fund Type 12, Account Codes 6200-6299, Fund Sources 6000-6999

Business Support Services Fund Type 11, Account Codes 6300-6399, Excluding Fund Sources 3000-5999 and 8000-9999

Business Support Services Fund Type 12, Account Codes 6300-6399, Fund Sources 6000-6999

System-Wide Support Services Fund Type 11, Account Codes 6400-6499, Excluding Fund Sources 3000-5999 and 8000-9999

System-Wide Support Services Fund Type 12, Account Codes 6400-6499, Fund Sources 6000-6999

Central Office Services Fund Type 11, Account Codes 6500-6599, Excluding Fund Sources 3000-5999 and 8000-9999

Central Office Services Fund Type 12, Account Codes 6500-6599, Fund Sources 6000-6999

Other General & Central Support Services Fund Type 11, Account Codes 6900-6999, Excluding Fund Sources 3000-5999 and 8000-9999

Other General & Central Support Services Fund Type 12, Account Codes 6900-6999, Fund Sources 6000-6999

(D) - Expenditures Direct:

(E) - (A) - (B) - (C)

(E) - Total All Fund Expenditures:

Exhibit F-II-A Expenditure Totals

For Unrestricted and Special Child Nutrition Program Indirect Cost Rates, Total Expenditures

are divided into three cost pools: Excluded, Indirect, and Direct.

Special Child Nutrition Program Rate

• Special Child Nutrition Program rates apply to LEAs that pay their utilities directly from the USDA – Food and Nutrition Fund Source 5101. These LEAs either have separate utility meters in their lunch rooms or have usage studies performed by a utility company. Expenditures for system-wide utilities are subtracted from the indirect cost pool in calculating this special rate.

Alabama State Department of Education

Office of Financial Management - LEA Accounting IDC Proposal for: Marshall County (048)LEA Name

INDIRECT COST - UNRESTRICTED / CNP RATE APPLICATIONFiscal Year 2016

Excluded Disallowed Indirect Direct Total

Costs Costs Costs Costs ExpendituresProposed Pool and Base Amounts

from LEA Financial System Unrestricted Indirect Cost Data Report

as of 09/30/2014 8,748,482.08$

This column is for restricted rate. Identifies those 6,244,172.99$ 42,233,305.75$ 57,225,960.82$

Adjustments (with Explanation including account code, object, and fund source) to Pools and Base:

expenditures allowable on unrestricted that

The indirect cost column should never contain -$

are not allowable any expenditure -$ Potential Adjustments: on restricted due to coded to a federal -$ Fund Source 2120 flex amounts not the supplement/ fund source -$

in fund 11-adjustment is only made for supplant restriction (3xxx - 5xxx) -$

those account codes that are normally -$

allowable indirect costs. -$ Fund Source 1320 flex amounts not -$ in fund 11-adjustment is only made for -$ those account codes that are normally -$ allowable indirect costs. -$

Advertising Expenditures-object 363 -$ if account code 61xx is used -$ Legal Expenditures-object 325 -$ if expenditures meet criteria -$

Flow Through -$

-$

-$

-$

-$

- - - - -$ Adjusted Pool and Base Amounts 8,748,482.08$ should be 0 6,244,172.99$ 42,233,305.75$ 57,225,960.82$

Total indirect costs: 6,244,172.99$ formula - pulls the indirect cost total from cell D32

4,734.67$ If applying for CNP Rate, identify utilities shown as indirect: 1,780,443.17$ (1,785,177.84)$

4,458,995.15$

Child Nutrition utilities paid direct: 154,402.23$

Page 5

Indirect costs applicable to Child Nutrition (Total indirect cost less utilities flex adjustment less indirect utilities identified above):

Adjustments for flexed utilities not coded to fund type 11:

EXAMPLE

To calculate the CNP rate for systems who pay CNP utilities directly from fund source 5101, the system wide utilities must be deducted from the indirect cost total (they are originally included because they are allowable when calculating the unrestricted rate).

Cell F10 is a formula and should match the total on the Unrestricted Indirect Cost Data Report

enter the amount of any utilities not coded to fund type 11. Account code should be an acceptable indirect as well as fund source. In this case, the system had utilities (370-379) coded to fund type 14, fund source 2120 in the amount of $4,734.67. Since 2120 can be flexed and and adjustment for the flex item would have been made in the adjustment section, we have to back this number out of the indirect cost pool for CNP purposes.The system also had utilities coded to fund type 12, account code 4210, fund source 5101. These would not included because they are federal funds and are pulled to the direct cost column.

cell F32 is a formula and should match the total on the Unrestricted Indirect Cost Data Report even after adjustments.

Approved MethodologyFixed Rate with Carry-Forward

Adjustments

• Fixed rates with adjustment for the difference in estimated (2012 adjusted General Purpose Financial Statements) and actual recovery (2014 adjusted GPFS) are established on an annual basis. The 2016 rate calculations reflect carry-forward adjustments.

Indirect Cost Calculation

• For the 2016 rate calculation pages, we are asking for input from Fiscal Year 2012 and 2014. This information can be found on the LEA’s approved 2014 Indirect Cost Application. The prior years’ information is used to calculate the actual under or over recovery of indirect costs versus the estimated recovery that the rate was based on at the time it was negotiated. Input items have a reference number (1-7) as well as a footnote of where the data can be found.

• For positive negotiated indirect cost rates, the full amount of the 2012 recovery carry forward (both positive and negative) should be entered 2014 item (7).

• For indirect cost rates that were negative and negotiated at zero percent, the amount of the entry in 2012 item (7) should be equal to the indirect cost amount in the line above, returning a zero percentage at the top of the column.

Alabama State Department of Education

Office of Financial Management - LEA Accounting IDC Proposal for:

FIXED RATE AS NEGOTIATED : (B/A) - Computed as follows: 14.12% 10.90% 16.91%

Direct Costs: (A) 44,072,093.10 (1) 42,563,449.55 42,233,305.75 formula. Pulls the

Indirect Cost Pool: total adjusted direct

Indirect Costs 6,342,632.80 (2) 5,383,347.56 6,244,172.99 costs from page 5.

Fixed-Carry Forward (118,336.05) (3) (744,947.57) (7) 895,795.09Total Pool: (B) 6,224,296.75 4,638,399.99 7,139,968.08

ACTUAL COSTS NEGOTIATED:Actual Direct Costs: 42,563,449.55 (4) 42,233,305.75 (6)

Actual Indirect Costs 5,383,347.56 (5) 6,244,172.99 (6)

Fixed-Carry Forward (118,336.05) (744,947.57)

Total Pool 5,265,011.51 5,499,225.42

CARRY-FORWARD COMPUTATION: (Indirect Eligible for Recovery)

Actual Direct Costs: 42,563,449.55 42,233,305.75

Fixed Rate x Actual Direct: 14.12% 10.90%

Equals Indirect Costs Applied (6,009,959.08) (4,603,430.33)

UNDER/(OVER) RECOVERY-CARRY FORWARD TO SUBSEQUENT YEAR: (Actual Indirect Cost less Indirect Costs Applied) (744,947.57) 895,795.09

NOTE (1): ENTER DATA FROM FY2014 IDC APPLICATION, PAGE 6, FY2012 COLUMN, "DIRECT COSTS"

NOTE (2): ENTER DATA FROM FY2014 IDC APPLICATION, PAGE 6, FY2012 COLUMN, INDIRECT COST POOL, "INDIRECT COSTS"

NOTE (3): ENTER DATA FROM FY2014 IDC APPLICATION, PAGE 6, FY2012 COLUMN, INDIRECT COST POOL, "FIXED-CARRY FORWARD"

NOTE (4): ENTER DATA FROM FY2014 IDC APPLICATION, PAGE 6, FY2012 COLUMN, "ACTUAL DIRECT COSTS"

NOTE (5): ENTER DATA FROM FY2014 IDC APPLICATION, PAGE 6, FY2012 COLUMN, "ACTUAL INDIRECT COSTS" NOTE (6): CALCULATIONS PULLED FROM UNRESTRICTED ADJUSTMENT PAGE 5 NOTE (7):

CELL C31 NOT TO EXCEED THE INDIRECT COST AMOUNT IN CELL E15

IF THE SYSTEM'S NEGOTIATED RATE FOR FY14 WAS POSITIVE, ENTER THE FULL AMOUNT FROM CELL C31

Marshall County (048)LEA Name

INDIRECT COST CALCULATIONUNRESTRICTED RATE - FIXED RATE WITH CARRY FORWARD

Fiscal Year 2016

EXAMPLE

Page 6

Fiscal Year 2012: Fiscal Year 2014: Fiscal Year 2016:

IF THE PERCENTAGE SHOWN ON THE FY2014 IDC APPLICATION WAS NEGATIVE, ENTER AMOUNT FROM

this column should match the data reported on the FY2014 IDC Proposal

formula. The rate negotiated for FY12 based on FY10 adjusted expenditures was to high. The actual FY12 indirect cost were lower

enter the amount from cell C31. If negative, do not exceed E15

formula. The rate negotiated for FY13 based on FY12 adjusted expenditures was to low. The actual FY14 indirect cost were higher

The FY16 rate is based on FY14 adjusted expenditures from the approved financial statement

formula. Pulls the total adjusted indirect costs from page 5.

formula. Pulls the over/ under recovery from cell F31.

Alabama State Department of Education

Office of Financial Management - LEA Accounting IDC Proposal for:

FIXED RATE AS NEGOTIATED : (B/A) - Computed as follows: 10.45% 6.98% 12.18%

Direct Costs: (A) 44,072,093.10 (1) 42,563,449.55 42,233,305.75 formula. Pulls the

Indirect Cost Pool: total adjusted direct

Indirect Costs 4,782,898.69 (2) 3,797,772.58 4,458,995.15 costs from page 5.

Fixed-Carry Forward (175,211.78) (3) (825,319.68) (7) 685,790.73Total Pool: (B) 4,607,686.91 2,972,452.90 5,144,785.88

ACTUAL COSTS NEGOTIATED:Actual Direct Costs: 42,563,449.55 (4) 42,233,305.75 (6)

Actual Indirect Costs 3,797,772.58 (5) 4,458,995.15 (6)

Fixed-Carry Forward (175,211.78) (825,319.68)

Total Pool 3,622,560.80 3,633,675.47

CARRY-FORWARD COMPUTATION: (Indirect Eligible for Recovery)

Actual Direct Costs: 42,563,449.55 42,233,305.75

Fixed Rate x Actual Direct: 10.45% 6.98%

Equals Indirect Costs Applied (4,447,880.48) (2,947,884.74)

UNDER/(OVER) RECOVERY-CARRY FORWARD TO SUBSEQUENT YEAR: (Actual Indirect Cost less Indirect Costs Applied) (825,319.68) 685,790.73

NOTE (1): ENTER DATA FROM FY2014 IDC APPLICATION, PAGE 6A, FY2012 COLUMN, "DIRECT COSTS" NOTE (2): ENTER DATA FROM FY2014 IDC APPLICATION, PAGE 6A, FY2012 COLUMN, INDIRECT COST POOL, "INDIRECT COSTS" NOTE (3): ENTER DATA FROM FY2014 IDC APPLICATION, PAGE 6A, FY2012 COLUMN, INDIRECT COST POOL, "FIXED-CARRY FORWARD" NOTE (4): ENTER DATA FROM FY2014 IDC APPLICATION, PAGE 6A, FY2012 COLUMN, "ACTUAL DIRECT COSTS"

NOTE (5): ENTER DATA FROM FY2014 IDC APPLICATION, PAGE 6A, FY2012 COLUMN, "ACTUAL INDIRECT COSTS"

NOTE (6): CALCULATIONS PULLED FROM UNRESTRICTED ADJUSTMENT PAGE 5 NOTE (7):

CELL C31 NOT TO EXCEED THE INDIRECT COST AMOUNT IN CELL E15IF THE SYSTEM'S NEGOTIATED RATE FOR FY14 WAS POSITIVE, ENTER THE FULL AMOUNT FROM CELL C31

Fiscal Year 2012: Fiscal Year 2014: Fiscal Year 2016:

Page 6A

Marshall County (048)LEA Name

INDIRECT COST CALCULATIONCNP RATE - FIXED RATE WITH CARRY FORWARD

Fiscal Year 2016

IF THE PERCENTAGE SHOWN ON THE FY2014 IDC APPLICATION WAS NEGATIVE, ENTER AMOUNT FROM

EXAMPLE

this column should match the data reported on the FY2014 IDC Proposal

formula. The rate negotiated for FY12 based on FY10 adjusted expenditures was to high. The actual FY12 indirect cost were lower

enter the amount from cell C31. If negative, do not exceed E15

formula. The rate negotiated for FY13 based on FY12 adjusted expenditures was to low. The actual FY14 indirect cost were higher

The FY16 rate is based on FY14 adjusted expenditures from the approved financial statement

formula. Pulls the CNP Indirect Cost from page 5, bottom section, "Indirect costs applicable to Child Nutrition"

formula. Pulls the over/ under recovery from cell F31.

(A) (B) (C) (D) (E)

Expenditures Expenditures Expenditures Expenditures Total All Fund

Excluded Not Allowed Indirect Direct Expenditures

$1,197,549.54 $0.00 $25,229,108.81 $26,426,658.35

$154,077.68 $0.00 $4,757,529.28 $4,911,606.96

$150,179.79 $0.00 $3,531,149.11 $3,681,328.90

$370,300.99 $4,348,067.34 $932,291.28 $5,650,659.61

$2,262,820.70 $5,771,214.86 $8,034,035.56

$0.00 $64,862.42 $64,862.42

$14,900.00 $1,170,921.30 $253,646.83 $1,439,468.13

$10,128.00 $95,319.36 $363,410.80 $0.00 $468,858.16

$0.00 $27,146.00 $195,966.08 $0.00 $223,112.08

$0.00 $0.00 $0.00 $0.00 $0.00

$0.00 $0.00 $0.00 $0.00 $0.00

$0.00 $0.00 $11,378.45 $0.00 $11,378.45

$0.00 $0.00 $6,707.92 $0.00 $6,707.92

$0.00 $0.00 $0.00 $0.00 $0.00

$0.00 $25,255.74 $0.00 $25,255.74

$340,047.04 $0.00 $340,047.04

$1,728,202.14 $0.00 $1,728,202.14

$554,678.00 $1,693,503.16 $2,248,181.16

$6,782,883.88 $5,641,454.00 $602,718.99 $42,233,305.75 $55,260,362.62

$1,965,598.20 $1,965,598.20

$8,748,482.08 $5,641,454.00 $602,718.99 $42,233,305.75 $57,225,960.82

(enter on B10) (enter on C10) (enter on D10) (enter on E10) (should match F10)

1.26%

Total Expenditures and Other Fund Uses:

Indirect Cost Rate = Total (C) divided by Total (B) + Total (D) rate based on unadjusted expenditures

Capital Outlay (7000 - 7999)

Debt Service - Long Term (8000 - 8999)

Other Expenditures (9000 - 9899)

Total Expenditures:

Other Fund Uses (9900 - 9999)

Staff Services (6430)

Printing, Publishing, & Duplicating Services (6450)

Other Central Support Services (6490)

Central Office Services (6500 - 6599)

Other General & Central Support Services (6900 - 6999)

Board of Education Services (6100 - 6199)

Executive Administrative Services (6200 - 6299)

Business Support Services (6300 - 6399)

Information Services (6410)

Data Processing Services (6420)

Total Instructional Services (1000 - 1999)

Total Other Instructional Support Services (2000 - 2299)

Total School Administration (2300 - 2399)

Operation & Maintenance Services (3000 - 3999)

Auxiliary Services (4000 - 4999)

STATE OF ALABAMADEPARTMENT OF EDUCATION

LEA Financial SystemRestricted Indirect Cost Rate Data - Unadjusted

Actual Costs for Fiscal Year Ended September 30, 2014048 - Marshall County Schools

Function of Expenditure Account Codes

expenditures coded to federal fund sources are never included in the indirect cost pool

identifies allowable indirect cost expenditures on unrestricted that are not allowable indirect cost expenditures for the restricted rate

verify any expenditure shown in the gray areas are pulled to the correct column

Notes

(A) - Expenditures Excluded:

Local School Funds (Public and Non-Public) Fund Sources 7000-7999

Capital Outlay - Real Property Account Codes 7000-7999

Debt Service - Long Term Account Codes 8000-8999

Other Fund Uses Account Codes 9900-9999

Purchased Food Object Code 461

USDA Commodities Object Code 462

Food Processing Supplies Object Code 464

Equipment Object Codes 500-599

Other Objects Object Codes 600-619, 627, 690-899

Other Fund Uses Object Codes 900-997

Technology Coordinator Fund Source 1221

Operation and Maintenance Services Fund Type 11, Account Codes 3000-3999, Excluding Fund Sources 3000-5999 and 8000-9999

Operation and Maintenance Services Fund Type 12, Account Codes 3000-3999, Fund Sources 6000-6999

Executive Administrative Services Fund Type 11, Account Codes 6200-6299, Excluding Fund Sources 3000-5999 and 8000-9999

Executive Administrative Services Fund Type 12, Account Codes 6200-6299, Fund Sources 6000-6999

Chief School Financial Officer Object Code 116, Fund Type 11, Account Codes 6200-6299, Excluding Fund Sources 3000-5999 and 8000-9999

Chief School Financial Officer Object Code 116, Fund Type 11, Account Codes 6300-6399, Excluding Fund Sources 3000-5999 and 8000-9999

Chief School Financial Officer Object Code 116, Fund Type 11, Account Codes 6400-6499, Excluding Fund Sources 3000-5999 and 8000-9999

(C) - Expenditures Indirect:

Business Support Services Fund Type 11, Account Codes 6300-6399, Excluding Fund Sources 3000-5999 and 8000-9999

Business Support Services Fund Type 12, Account Codes 6300-6399, Fund Sources 6000-6999

System-Wide Support Services Fund Type 11, Account Codes 6400-6499, Excluding Fund Sources 3000-5999 and 8000-9999

System-Wide Support Services Fund Type 12, Account Codes 6400-6499, Fund Sources 6000-6999

Central Office Services Fund Type 11, Account Codes 6500-6599, Excluding Fund Sources 3000-5999 and 8000-9999

Central Office Services Fund Type 12, Account Codes 6500-6599, Fund Sources 6000-6999

Other General & Central Support Services Fund Type 11, Account Codes 6900-6999, Excluding Fund Sources 3000-5999 and 8000-9999

Other General & Central Support Services Fund Type 12, Account Codes 6900-6999, Fund Sources 6000-6999

(D) - Expenditures Direct:

(E) - (A) - (B) - (C)

(E) - Total All Fund Expenditures:

Exhibit F-II-A Expenditure Totals

(B) - Expenditures Not Allowed (costs which would constitute supplanting):

Alabama State Department of Education

Office of Financial Management - LEA Accounting IDC Proposal for: Marshall County (048)LEA Name

INDIRECT COST - RESTRICTED RATE APPLICATIONFiscal Year 2016

Excluded Disallowed Indirect Direct Total

Costs Costs Costs Costs ExpendituresProposed Pool and Base Amounts

from LEA Financial System Restricted Indirect Cost Data Report as of

09/30/2014 8,748,482.08$ 5,641,454.00$ 602,718.99$ 42,233,305.75$ 57,225,960.82$ Adjustments (with Explanation including account code, object and fund source) to Pools and Base:

the indirect cost column should never contain any -$

reflects those expenditure coded -$ Potential Adjustments: expenditures that to a federal fund -$ CSFO Salary and Benefits are allowed indirect source -$

Fund Source 2120 flex amounts not cost on unrestricted -$

coded to fund 11 (only if the item is but not allowed on -$

an allowable indirect account code) restricted due to -$ Fund Source 1320 flex amounts not supplement/supplant -$ coded to fund 11 (only if the item is restriction -$ an allowable indirect account code) -$ Auditing Expenditures - object 323 -$ adjustment needed if expenditures -$ are coded to account 61xx and 62xx -$ Legal Expenditures - object 325 -$ only if expenditures are allowable -$ Flow Through -$

-$ -$ -$

-$

-$

-$

-$

-$

- - - - -$ Adjusted Pool and Base Amounts 8,748,482.08$ 5,641,454.00$ 602,718.99$ 42,233,305.75$ 57,225,960.82$

Page 9

EXAMPLE

Alabama State Department of Education

Office of Financial Management - LEA Accounting IDC Proposal for:

FIXED RATE AS NEGOTIATED : (B/A) - Computed as follows: 0.87% 1.14% 1.46%

Direct Costs (direct plus disallowed) : (A) 49,935,843.77 (1) 47,447,077.77 47,874,759.75

Indirect Cost Pool:

Indirect Costs 478,882.13 (2) 499,719.34 602,718.99

Fixed-Carry Forward (45,444.23) (3) 41,485.33 (7) 98,432.06Total Pool: (B) 433,437.90 541,204.67 701,151.05

ACTUAL COSTS NEGOTIATED:Actual Direct Costs (direct plus disallowed) : 47,447,077.77 (4) 47,874,759.75 (6)

Actual Indirect Costs 499,719.34 (5) 602,718.99 (6)

Fixed-Carry Forward (45,444.23) 41,485.33

Total Pool 454,275.11 644,204.32

CARRY-FORWARD COMPUTATION: (Indirect Eligible for Recovery)

Actual Direct Costs: 47,447,077.77 47,874,759.75

Fixed Rate x Actual Direct: 0.87% 1.14%

Equals Indirect Costs Applied (412,789.58) (545,772.26)

UNDER/(OVER) RECOVERY-CARRY FORWARD TO SUBSEQUENT YEAR: (Actual Indirect Cost less Indirect Costs Applied) 41,485.53 98,432.06

NOTE (1): ENTER DATA FROM FY2014 IDC APPLICATION, PAGE 10, FY2012 COLUMN, "TOTAL DIRECT COSTS" NOTE (2): ENTER DATA FROM FY2014 IDC APPLICATION, PAGE 10, FY2012 COLUMN, INDIRECT COST POOL, "TOTAL INDIRECT COSTS" NOTE (3): ENTER DATA FROM FY2014 IDC APPLICATION, PAGE 10, FY2012 COLUMN, INDIRECT COST POOL, "FIXED-CARRY FORWARD" NOTE (4): ENTER DATA FROM FY2014 IDC APPLICATION, PAGE 10, FY2012 COLUMN, "ACTUAL DIRECT COSTS" NOTE (5): ENTER DATA FROM FY2014 IDC APPLICATION, PAGE 10, FY2012 COLUMN, "ACTUAL INDIRECT COSTS" NOTE (6): CALCULATIONS PULLED FROM RESTRICTED ADJUSTMENT PAGE 9

NOTE (7):

CELL C31 NOT TO EXCEED THE INDIRECT COST AMOUNT IN CELL E15

IF THE SYSTEM'S NEGOTIATED RATE FOR FY14 WAS POSITIVE, ENTER THE FULL AMOUNT FROM CELLC 31

Fiscal Year 2012: Fiscal Year 2014: Fiscal Year 2016:

Page 10

Marshall County (048)LEA Name

INDIRECT COST CALCULATIONRESTRICTED RATE - FIXED RATE WITH CARRY FORWARD

Fiscal Year 2016

IF THE PERCENTAGE SHOWN ON THE FY2014 IDC APPLICATION WAS NEGATIVE, ENTER AMOUNT FROM

EXAMPLE

this column should match the data reported on the FY2014 IDC Proposal

formula. The rate negotiated for FY12 based on FY10 adjusted expenditures was to low. The actual FY12 indirect cost were higher

enter the amount from cell C31. If negative, do not exceed E15

formula. The rate negotiated for FY12 based on FY10 adjusted expenditures was to low. The actual FY12 indirect cost were higher

formula. Pulls the total adjusted direct cost plus the total adjusted disallowed cost from page 9.

formula. Pulls the total adjusted indirect cost from page 9.

formula. Pulls the over/ under recovery from cell F31.

Excluded Cost Pool: Extraordinary or Distorting Items

• Extraordinary or distorting items are excluded when calculating the rate and the indirect cost reimbursement because the activities require minimal administrative support. Expenditures of food are generally referred to as “distorting items” since they do not generate administrative overhead or benefit from it, to the same degree as most other direct cost objects (such as salaries and wages). Excluded expenditures are the same for unrestricted, CNP, and restricted rate calculations.

Expenditures Excluded on the Data Reports (Column A)

• Fund Sources – 7XXX - Local School Funds – Public and Non-Public• Account Codes 7XXX - Capital Outlay – Real Property• Account Codes 8XXX - Debt Service – Long Term• Account Codes 9XXX – Other Fund Uses• Object Code 461 - Purchased Food• Object Code 462 - USDA Commodities• Object Code 464 - Food Processing Supplies• Object Codes 5XX – Equipment• Other Object Codes 600-619, 627, 690-899, 900-997

Expenditures Excluded on the Data Reports (Column A) cont’d

• Short Term Debt• Doubtful Accounts Expense• Depreciation Expense• Building and Land Improvements less than $50,000• Indirect Costs Recovered• Operating Transfers • Refunds• Fines and Penalties• Judgments• Other Claims

Expenditures to Exclude That Require Adjustments

• Advertising, legal, and other expenses associated with construction projects that are not coded to capital outlay

• Settlements and judgments against the LEA that are not coded to be automatically excluded. . .for example, coded to object code 325 - Legal Fees.

• Flow through transactions where the LEA only serves as fiscal agent and does not provide administrative services. An example would be State Supported Special Education Facilities funded through the Foundation Program where the LEA only forwards the funds and does not issue purchase orders or pay salaries directly. Other examples could include HIPPY and At-Risk Special Use 0054 organizations.

Indirect Cost Expenditures on the Unrestricted Data Report

(Column C)

• Account Codes 3XXX - Operation & Maintenance Services• Account Codes 62XX - Executive Administrative Services• Account Codes 63XX - Business Support Services• Account Code 64XX - Information Services, Data Processing Services,

Staff Services, Printing, Publishing, Duplicating Services, and Central Support Services

• Account Codes 65XX & 69XX- Central Office Services

Possible Adjustments in Calculating the Unrestricted, CNP, and Restricted Rate

• Auditing – Object Code 323 – charged to Account Code 61XX should be adjusted out of Column D into Column C

RecordTypeFiscalYearFiscalPeriodSystemFundTypeAccountTypeAccountCodeObjectOfExpenditureCostCenterFundSourceAppropriationYearProgramCodeSpecialUseTypeAcct BalF 2012 12 006 11 5 6190 323 8620 6001 0 8610 0000 D 9,383.00 F 2012 12 007 11 5 6190 323 8610 6001 0 8610 0000 D 18,492.00 F 2012 12 015 11 5 6110 323 8600 6001 0 8600 0000 D 15,388.75 F 2012 12 016 11 5 6190 323 8620 6001 0 8610 0000 D 540.00 F 2012 12 028 11 5 6190 323 8610 6001 0 8610 0000 D 7,176.00 F 2012 12 031 11 5 6190 323 8640 1110 0 8640 0000 D 11,040.00 F 2012 12 032 11 5 6190 323 8610 6001 0 8610 0000 D 10,971.00 F 2012 12 044 11 5 6110 323 8620 6001 0 8610 0000 D 11,040.00 F 2012 12 046 11 5 6190 323 8620 1110 0 8610 0000 D 3,864.00 F 2012 12 046 11 5 6190 323 8620 6001 0 8610 0000 D 7,176.00 F 2012 12 063 11 5 6190 323 8610 6001 0 8610 5300 D 11,040.00 F 2012 12 065 11 5 6110 323 8600 6001 0 8610 0000 D 11,040.00 F 2012 12 106 11 5 6110 323 8620 6001 0 8620 0000 D 13,000.00 F 2012 12 125 11 5 6110 323 8610 6001 0 8610 0000 D 48,035.00 F 2012 12 128 11 5 6190 323 8620 6280 0 8620 0000 D 30,600.00 F 2012 12 130 11 5 6190 323 8632 6001 0 8610 6998 D 71,330.88 F 2012 12 132 11 5 6190 323 8620 6001 0 8620 0000 D 29,000.00 F 2012 12 144 11 5 6190 323 8600 6001 0 8610 0000 D 37,850.00 F 2012 12 146 11 5 6190 323 8620 6001 0 8620 0000 D 20,300.00

Possible Adjustments in Calculating the Unrestricted, CNP, and Restricted Rates

• McAleer and INOW maintenance agreements that are coded to Fund Type 14, Account Code 6XXX would not be included in the indirect cost pool but should be moved there if paid from state or local funds.

RecordTypeFiscalYearFiscalPeriodSystemFundTypeAccountTypeAccountCodeObjectOfExpenditureCostCenterFundSourceAppropriationYearProgramCodeSpecialUseTypeAcct BalF 2012 12 015 14 5 6310 333 8600 2120 0 8600 0000 D 23,200.00 F 2012 12 107 14 5 6540 333 8640 2120 0 8640 0000 D 15,431.50 F 2012 12 114 14 5 6410 333 8690 2120 0 8640 0000 D 25,299.00 F 2012 12 137 14 5 6310 333 8630 2120 0 8630 0000 D 1,259.00 F 2012 12 141 14 5 6310 333 8600 2120 0 8600 0000 D 26,700.00 F 2012 12 159 14 5 6420 333 0001 2120 0 2900 0101 D 1,091.97 F 2012 12 159 14 5 6420 333 0001 2120 0 8640 0101 D 16,258.03 F 2012 12 200 14 5 6430 333 8620 2120 0 8620 0609 D 12,174.00 F 2012 12 200 14 5 6450 333 8620 2120 0 8620 0609 D 2,377.00 F 2012 12 201 14 5 6420 333 0010 2120 0 8620 8601 D 744.50 F 2012 12 201 14 5 6420 333 0020 2120 0 8620 8601 D 744.50 F 2012 12 201 14 5 6420 333 0030 2120 0 8620 8601 D 744.50 F 2012 12 201 14 5 6420 333 0040 2120 0 8620 8601 D 744.50 F 2012 12 201 14 5 6420 333 8600 2120 0 8620 0000 D 16,900.00 F 2012 12 201 14 5 6420 333 8600 2120 0 8620 8601 D 2,450.00 F 2012 12 201 14 5 6420 333 8600 6520 0 8601 0000 D 46,246.60

Possible Adjustments in Calculating the Unrestricted, CNP, and Restricted Rate• Legal – Object Code 325 – Coded to Account Code 61XX will all be in

direct costs. If any of the fees are eligible for indirect (retainer fees, etc.), moved out of Column D into Column C.

RecordTypeFiscalYearFiscalPeriodSystemFundTypeAccountTypeAccountCodeObjectOfExpenditureCostCenterFundSourceAppropriationYearProgramCodeSpecialUseTypeAcct BalF 2012 12 003 11 5 6110 325 8620 6001 0 8610 0000 D 99,336.32 F 2012 12 004 11 5 6190 325 8630 1110 0 8600 0000 D 1,524.23 F 2012 12 004 11 5 6190 325 8630 1240 1 8600 0000 D 10,013.41 F 2012 12 004 11 5 6190 325 8630 1242 1 8600 0000 D 25,602.70 F 2012 12 005 11 5 6110 325 8630 6001 0 8610 0000 D 7,476.51 F 2012 12 005 11 5 6110 325 8630 6001 0 2900 0000 D 7,600.00 F 2012 12 005 11 5 6110 325 8630 1110 0 8610 0000 D 32,740.41 F 2012 12 006 11 5 6110 325 8620 6001 0 8610 0000 D 38,097.18 F 2012 12 007 11 5 6190 325 8620 6001 0 8610 0000 D 1,245.00 F 2012 12 007 11 5 6190 325 8620 6001 0 2900 0000 D 4,937.50 F 2012 12 007 11 5 6190 325 8610 6001 0 8610 0000 D 11,566.47 F 2012 12 009 11 5 6190 325 8600 6001 0 8600 0000 D 11,695.35 F 2012 12 010 11 5 6190 325 8600 6001 0 8610 0000 D 27,631.22 F 2012 12 010 11 5 6190 325 8600 6001 0 8610 5010 D 100,066.58 F 2012 12 011 11 5 6110 325 8620 6110 0 8610 0000 D 7,100.00 F 2012 12 012 11 5 6110 325 8610 2901 0 8610 0000 D 901.96 F 2012 12 012 11 5 6110 325 8610 6001 0 8610 0000 D 23,556.43

Possible Adjustments in Calculating the Unrestricted, CNP, and

Restricted Rate• Flexibility used in Fund Source 1320 or 2120 to pay for allowable

indirect costs but coded to Fund Type 14 instead of 11. Utilities for Unrestricted/CNP would be moved out of Column D into Column C

RecordTypeFiscalYearFiscalPeriodSystemFundTypeAccountTypeAccountCodeObjectOfExpenditureCostCenterFundSourceAppropriationYearProgramCodeSpecialUseTypeAcct BalanceF 2012 12 101 14 5 3200 371 0020 2120 0 8300 0000 D 309,035.16 F 2012 12 049 14 5 3200 373 0595 2120 0 8320 0000 D 145,115.18 F 2012 12 163 14 5 3200 371 0040 2120 0 8390 0000 D 141,488.35 F 2012 12 049 14 5 3200 373 0120 2120 0 8320 0000 D 132,216.89 F 2012 12 050 14 5 3200 371 0070 2120 0 8320 0000 D 123,684.90 F 2012 12 155 14 5 3200 371 0030 2120 0 8320 0000 D 119,191.17 F 2012 12 050 14 5 3200 371 0020 2120 0 8320 0000 D 108,212.91 F 2012 12 024 14 5 3200 371 0080 2120 0 8320 9999 D 106,086.61 F 2012 12 106 14 5 3200 371 0030 2120 0 8320 0000 D 104,175.99 F 2012 12 106 14 5 3200 371 0020 2120 0 8320 0000 D 102,908.80 F 2012 12 049 14 5 3200 373 8662 2120 0 8320 0000 D 100,655.50 F 2012 12 155 14 5 3200 371 0035 2120 0 8320 0000 D 98,274.62 F 2012 12 024 14 5 3200 371 0020 2120 0 8320 9999 D 98,000.89 F 2012 12 049 14 5 3200 373 0070 2120 0 8320 0000 D 92,223.36 F 2012 12 024 14 5 3200 371 0120 2120 0 8320 9999 D 91,496.34 F 2012 12 049 14 5 3200 373 0112 2120 0 8320 0000 D 90,421.77

Adjustments Required in Calculating the Restricted Rate

• Ensure that the CSFO salary, benefits, and expenses are not included in the indirect cost pool. Expenditures to Object Code 116 from a state or local fund are automatically shown in not allowed.

• Account Code 62XX expenditures are categorized as not allowed on the data report. Any allowable indirect costs that are coded there will need to be moved out of Column B into Column C.

• Compensation for Unused Leave (object 195) plus associated fringe benefits should be removed from the indirect cost pool and added to the direct cost pool (base).

Indirect Cost Expenditures that would constitute supplanting are Moved in the Restricted Rate Data Report from Column C to Column B – Not Allowed

• Account Codes 3XX – Operations and Maintenance• Account Codes 62XX - Executive Administration• Object Code 116 - CSFO Salary • Fund Source 1221 - Technology Director

Adjustments Required in Calculating the Restricted Rate

• Auditing Coded to Account Code 62XX will need to be moved out of Column B into Column C

F 2012 12 014 11 5 6210 323 8620 6001 0 8620 0000 D 3,176.00 F 2012 12 113 11 5 6210 323 8620 6001 0 8620 0000 D 39,050.00 F 2012 12 188 11 5 6210 323 8600 6001 0 8620 0000 D 22,450.00 F 2012 12 200 11 5 6210 323 8620 6001 0 8620 0000 D 11,040.00 F 2012 12 019 11 5 6220 323 8600 1110 0 8600 0000 D 3,864.00 F 2012 12 133 11 5 6220 323 8600 6001 0 8600 0156 D 250.00 F 2012 12 159 11 5 6220 323 8102 6001 0 2900 0000 D 1,925.00 F 2012 12 189 11 5 6290 323 0010 6001 0 8620 0000 D 1,400.00 F 2012 12 189 11 5 6290 323 0020 6001 0 8620 0000 D 1,400.00 F 2012 12 189 11 5 6290 323 0040 6001 0 8620 0000 D 1,400.00 F 2012 12 189 11 5 6290 323 0030 6001 0 8620 0000 D 2,715.72 F 2012 12 189 11 5 6290 323 8620 6001 0 8620 0000 D 16,000.00

Adjustments Required in Calculating the Restricted Rate

• Eligible Legal costs coded to 62XX will need to be moved out of Column B into Column C

F 2012 12 001 11 5 6210 325 8620 2901 0 8620 0000 D 10,828.66 F 2012 12 001 11 5 6210 325 8620 1110 0 2900 0000 D 11,336.11 F 2012 12 009 12 5 6210 325 8600 6960 0 8600 0000 D 2,816.00 F 2012 12 014 11 5 6210 325 8620 6001 0 8620 0000 D 6,704.57 F 2012 12 018 11 5 6210 325 8621 6001 0 8621 0000 D 60,134.02 F 2012 12 019 11 5 6210 325 8600 1110 0 8600 0000 D 33,790.23 F 2012 12 020 11 5 6220 325 8620 6001 0 8620 0000 D 120.00 F 2012 12 025 11 5 6290 325 8620 1110 0 8620 0000 D 123,078.66 F 2012 12 028 11 5 6210 325 8620 6001 0 8620 0000 D 9,500.00 F 2012 12 028 11 5 6290 325 8610 6001 0 8620 0000 D 19,946.00 F 2012 12 036 11 5 6210 325 8600 6001 0 8620 0000 D 3,380.48 F 2012 12 037 11 5 6220 325 8620 2130 0 8600 0000 D 25,915.00 F 2012 12 037 11 5 6220 325 8201 6001 0 2900 0000 D 190,203.60 F 2012 12 037 11 5 6290 325 8620 2901 0 8600 0000 D 12,172.99 F 2012 12 037 11 5 6290 325 8620 6001 0 8600 0000 D 559,188.63 F 2012 12 038 11 5 6210 325 8620 1110 0 8620 0000 D 7,708.75 F 2012 12 047 11 5 6220 325 0080 6965 0 2900 0000 D 3,000.00 F 2012 12 047 11 5 6220 325 0090 6965 0 2900 0000 D 8,675.20 F 2012 12 049 11 5 6210 325 8623 6001 0 8620 0000 D 679,005.28

Budgeting Indirect Cost

• Example of budgeting for indirect costs: Assume an LEA’s approved indirect cost rate is 8.00 percent and the grant amount is $10,000. The LEA plans to spend the entire $10,000 in the same fiscal year and does not expect to spend any of the $10,000 on excluded costs. Since the grant amount is for $10,000, and indirect costs are part of the grant amount rather than in addition to it, you must back into a budgeted indirect cost amount that keeps the grant from exceeding $10,000. To do this, divide $10,000 by 1.08, which equals $9,259.26. Then subtract $9,259.26 from $10,000, which equals $740.74. The $740.74 is the maximum amount the LEA could budget for indirect costs. (To test this, $9,259.26 times 8.00 percent equals $740.74, and $9,259.26 plus $740.74 equals $10,000.)

3310-0 Allocation 906,732.00

Less:461 - Purchased Food464 - Food Supplies5XX - Capital Outlay 27,000.00 61X - Debt Service627 - Doubtful Accounts69X - Other Objects7XX - Improvements9XX - Other Fund Uses -

27,000.00

879,732.00 Divided by 1.0401

Indirect Cost Base 845,814.83 Maximum Indirect Cost 4.010% 33,917.17 Equipment 27,000.00

Allocation 906,732.00

Budgeting Indirect Cost (cont’d)

After a budget file has been uploaded, verify that the indirect costs budgeted by fund source are correct. http://www.alsde.edu/leareports/From the above link, under optional reports, pull the Indirect Cost Earned vs. Budgeted report and check for any negative variances. Some negative variances can be explained and are acceptable. Direct federal grants are allowed to charge the unrestricted rate. Administrative fees earned are coded to Object Code 910 and are allowed by the signed agreement.

Applying the Approved Indirect Cost Rate

Multiply total expenditures less exclusions by the appropriate rate.After uploading financial statement data, verify the indirect costs amounts charged by going to:http://www.alsde.edu/leareports/Under optional reports pull:Indirect Cost Earned vs. CollectedIndirect Cost Earned vs. Collected – CNP Funds by Cost Center

Applying the Approved Indirect Cost Rate (cont’d)

• LEA Accounting system accountants use these reports to verify that excess indirect costs have not been charged to Federal Programs or CNP during their annual financial statement review.

• Fund sources that have an administrative expense limit that is lower than the LEA’s approved indirect cost rate, the lower is used for the calculation. On the Mobile example, their approved rate is 4.01% but Neglected & Delinquent (4116) does not allow administrative charges and the ELA (4150) administrative limit is 2%.

Links

• Cost Principals for State and Local Governments - 2 CFR Part 200 - http://www.ecfr.gov/cgi-bin/text-idx?tpl=/ecfrbrowse/Title02/2tab_02.tpl

• Cost Allocation Guide for State and Local Governments, USDE, Indirect Cost Group, Office of Chief Financial Officer, September, 2009 http://www2.ed.gov/about/offices/list/ocfo/fipao/guideigcwebsite.pdf

• USDA Indirect Cost Guidance - http://www.fns.usda.gov/cnd/Governance/Policy-Memos/2011/SP41-2011_os.pdf

2015 LEA Indirect Cost Application

Direct any questions to your assigned accountant or

1-800-831-8823