2014 media landscape broadmoor

DESCRIPTION

We kicked off a new programming season with a Luncheon Thursday, September 19th at Fogo de Chao, downtown. The room was filled with 40+ marketers all eager to learn how Vladimir Jones and The Broadmoor use new media to put heads in beds. The presentation was packed with useful facts and real life examples. Check it out!TRANSCRIPT

2014 Media LandscapeThe Broadmoor Resort - Vladimir Jones

September 2013

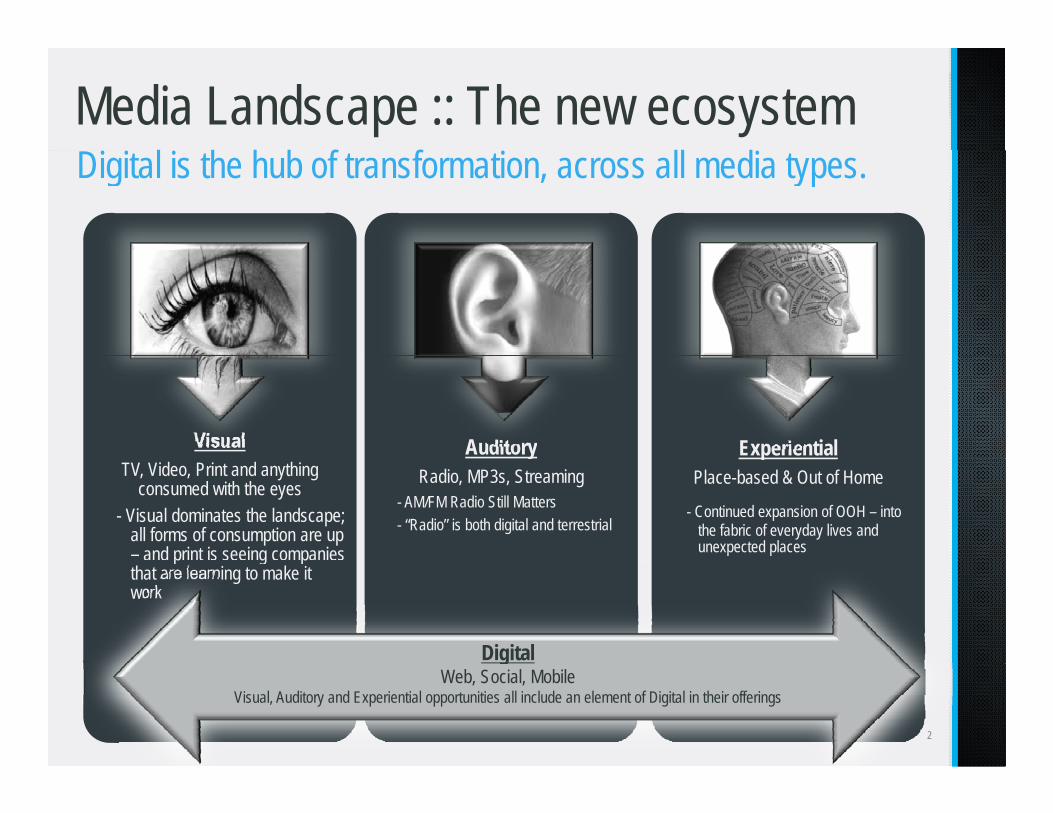

Media Landscape :: The new ecosystemDigital is the hub of transformation, across all media types.

Visual Auditory ExperientialTV, Video, Print and anything

consumed with the eyes- Visual dominates the landscape;

all forms of consumption are up – and print is seeing companies

yRadio, MP3s, Streaming

- AM/FM Radio Still Matters- “Radio” is both digital and terrestrial

pPlace-based & Out of Home

- Continued expansion of OOH – into the fabric of everyday lives and unexpected places

Visual, Auditory and Experiential opportunities all include an

p g pthat are learning to make it work

Digital

2

opportunities all include an element of Digital in their offerings

gWeb, Social, Mobile

Visual, Auditory and Experiential opportunities all include an element of Digital in their offerings

2013 highlights :: An alternate video universeVideo consumption will remain strong… but continue to evolve. Messages live across platforms, but come to life for consumers differently g p , yin each space.

• Use of the 15-second video ad has decreased steadily; the 30-second ad gained share

• Video completion rates are at an all-time high across content lengths- 93% for long-form content (20+

minutes)- 81% for mid-form content (5-20

• Video-viewing smart phones, tablets, game consoles, etc., continues to rise

- 12% of total video viewing

• Video ad volume spiked 47%- Pre-roll volume rose 45%- Mid-roll rose 60%

minutes)- 68% for short-form content (<5

minutes) • Premium content being consumed online continues to rise, 23% YOY

3Source: Free Wheel Video Monetization Report

2013 highlights :: Audio reconstructionA blending of traditional and non-traditional audio platforms.Digital and terrestrial radio schedules being evaluated, bundled and

h d t thpurchased together.

• Pandora has integrated audience data into media-buying platforms

C di ti id b id ith t t i l di t ti- Compare audience ratings side by side with terrestrial radio stations

• Provides context to the online listening audience

- Adds digital targeting abilitiesAdds digital targeting abilities- Adds size and scope of online listening

universe

• Simplifies the evaluation and purchasing of online audio

- There are currently around 500 licensed digital music services

4

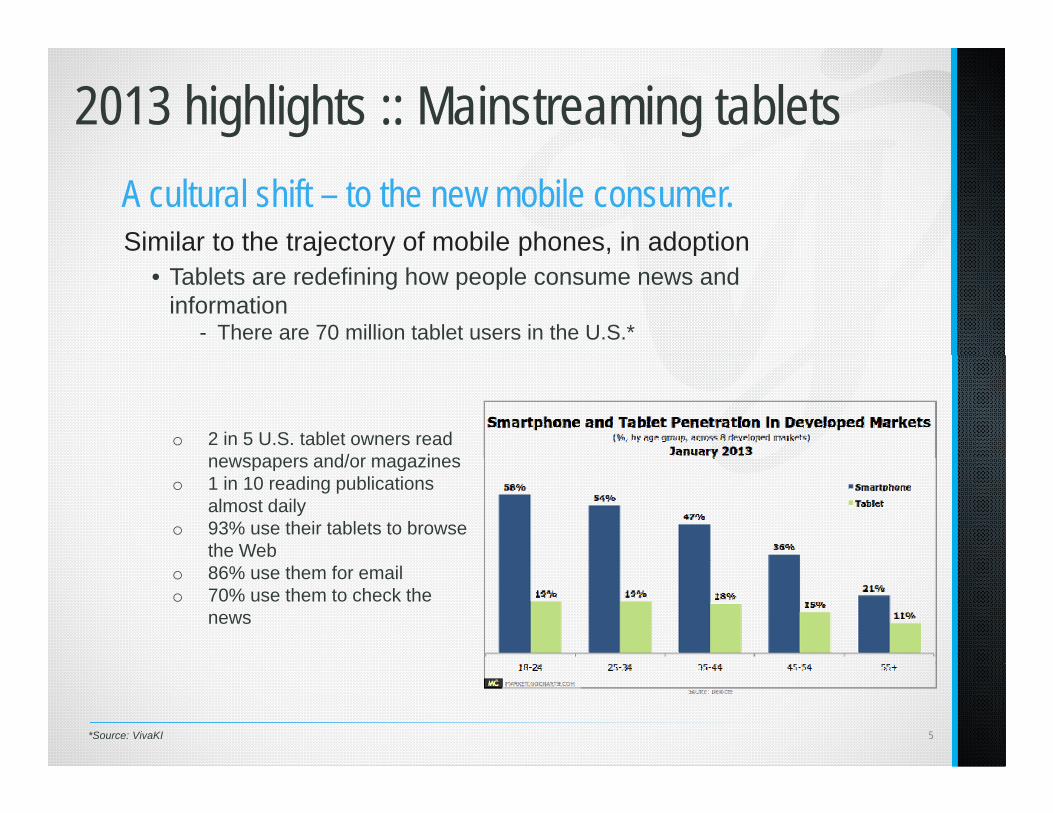

2013 highlights :: Mainstreaming tabletsA cultural shift – to the new mobile consumer.Similar to the trajectory of mobile phones, in adoptionj y p , p

• Tablets are redefining how people consume news and information

- There are 70 million tablet users in the U.S.*

o 2 in 5 U.S. tablet owners read newspapers and/or magazinesnewspapers and/or magazines

o 1 in 10 reading publications almost daily

o 93% use their tablets to browse the Web

o 86% use them for emailo 70% use them to check the

news

5*Source: VivaKI

2013 highlights :: The Fab FourTh t t h The great tech war.Amazon, Apple, Facebook and Google continue to collide in markets for mobile phones and tablets, mobile apps, social networking, and more.

The Post-PC World• Each company embraced what Steve Jobs

branded the “post-PC world”

p , pp , g,

• A vision of daily life that is enabled by, and comes to depend on, smartphones, tablets, and other small, mobile, easy-to-use computers.

Facilitation of ConsumptionData Collection

The Battle Field

p• Used post-PC devices to encourage and

facilitate consumption• Amazon, Apple, Facebook and Google don’t recognize

any borders; they march beyond the walls of tech into retailing advertising publishing movies TV

• Leveraged activity on devices to produce a wealth of data

• Data fuels new and better advertising systems (which Google and Facebook depend on)

• Data fuels better insights into purchasing habits (which

6

retailing, advertising, publishing, movies, TV, communications, and even finance

• Data fuels better insights into purchasing habits (which Amazon and Apple want to know)

• Data also powers new inventions

2013 highlights :: Broadcast Reprioritization of media and marketing strategies.The 2012–2013 Upfront season was weak – Conversely, cable had a stellar year, with big hits such as The Walking Dead and Duck Dynasty

TV NetworksTotal commitments down for broadcast networksDifficult to pursue CPM increases at historical ratesA di t d ith ti d Audience guarantees down with ratings down in current season

C bl N t kCable NetworksUp from previous yearBenefiting from original programming hits at or higher ratings than network

7

2014 Media Landscape

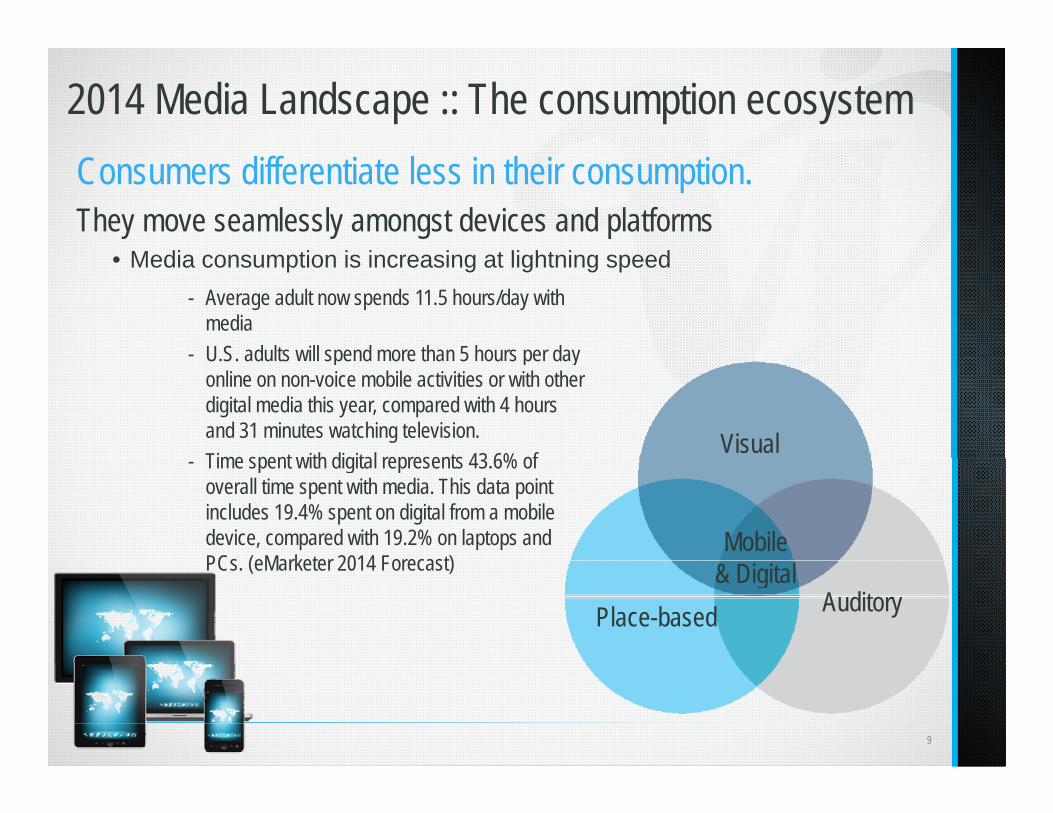

2014 Media Landscape :: The consumption ecosystemConsumers differentiate less in their consumption.They move seamlessly amongst devices and platforms

M di ti i i i t li ht i d• Media consumption is increasing at lightning speed- Average adult now spends 11.5 hours/day with

media- U S adults will spend more than 5 hours per day - U.S. adults will spend more than 5 hours per day

online on non-voice mobile activities or with other digital media this year, compared with 4 hours and 31 minutes watching television.Time spent with digital represents 43 6% of

Visual- Time spent with digital represents 43.6% of

overall time spent with media. This data point includes 19.4% spent on digital from a mobile device, compared with 19.2% on laptops and PCs (eMarketer 2014 Forecast)

Mobile PCs. (eMarketer 2014 Forecast) & Digital

AuditoryPlace-based

9

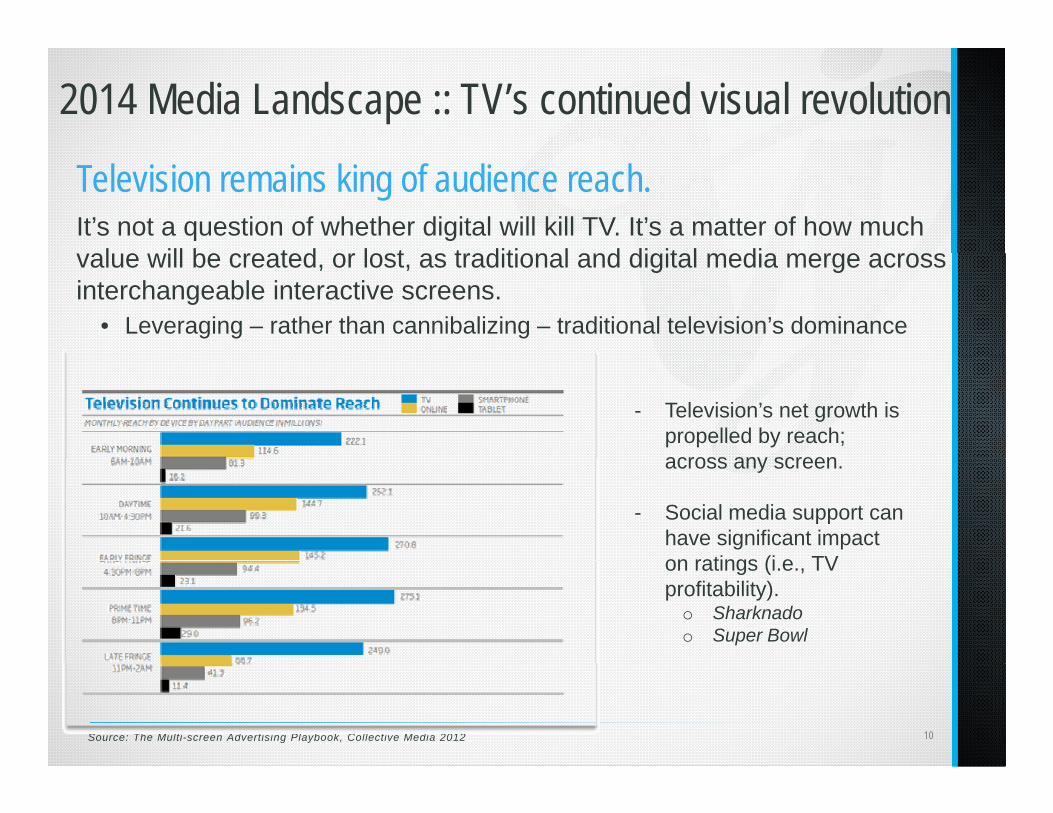

2014 Media Landscape :: TV’s continued visual revolution

Television remains king of audience reach.It’s not a question of whether digital will kill TV. It’s a matter of how much

l ill b t d l t t diti l d di it l divalue will be created, or lost, as traditional and digital media merge across interchangeable interactive screens.

• Leveraging – rather than cannibalizing – traditional television’s dominance

- Television’s net growth is propelled by reach; across any screenacross any screen.

- Social media support can have significant impact on ratings (i e TVon ratings (i.e., TV profitability).

o Sharknadoo Super Bowl

10Source: The Multi-screen Advertising Playbook, Collective Media 2012

The Broadmoor:: Using data onlineClosing in on the funnel – remarketing toward conversion

Through data aggregation, The Broadmoor deploys re-messaging and re-targeting

• Qualify audience that engages• Consider sequential messaging with each Co s de seque t a essag g t eac

data point learned• Based on the user’s first

engagement, a message choice is made for the next ad served

11

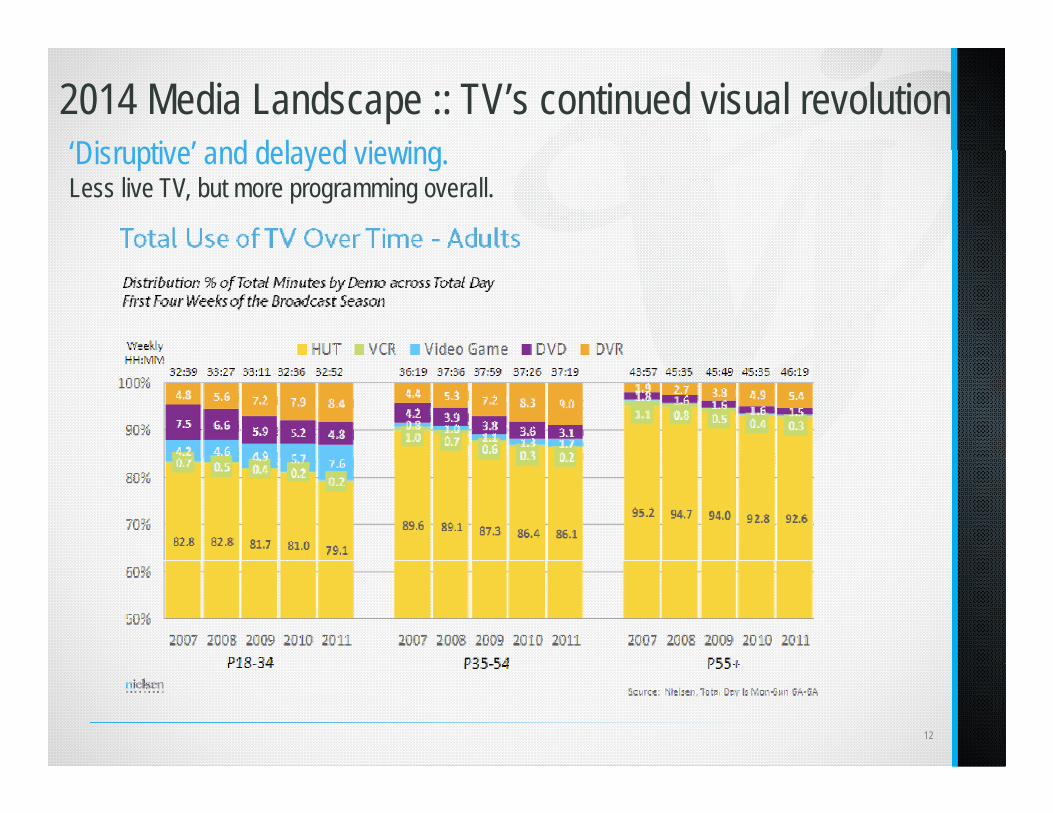

2014 Media Landscape :: TV’s continued visual revolution‘Disruptive’ and delayed viewingDisruptive and delayed viewing.Less live TV, but more programming overall.

12

The Broadmoor:: Maximizing Visual AssetsUsing Cinemagraphs – Online, OOH and VideoThis technique was used to extend the print campaign into digital OOH,

li d TV t d l tonline and TV spot development

13

The Broadmoor:: Maximizing Visual AssetsMulti-use creative – Website & AdvertisingBy using the same TV video asset, The Broadmoor deploys online video

it ith ti CTA h i t d iunits with creative CTA mechanisms toward conversion

14

2014 Media Landscape :: Print’s visual digitizationLong live Print? The printed media holds ground – digital evolution progresses

• Users are spending more time accessing news content via Tablet andUsers are spending more time accessing news content via Tablet and Smartphone than conventional computers

- Also visiting more pages in one setting and returning more frequently than on the PC

• 11.5% of tablet owners reading newspaper apps almost every day• Newspaper brands need to follow Mags to capitalize and monetize• Investor interest aids evolution

- Magazines/periodicals showed even higher readership rates than newspapers with 39.6% of tablet

di i th iowners reading magazines on their device during the month

- Big opportunity in the social and mobile realms

15

2014 Media Landscape :: Print’s visual digitization

What is Newspaper’s new normal? Circulation and ad revenue drops appear to have stabilized; but the business model standard has not been establishedbusiness model standard has not been established.

• More than 400 of 1,300 U.S. newspapers now use a paywall

• Some are abandoning their paywall and moving to a premium modelSome are abandoning their paywall and moving to a premium model (San Francisco Chronicle, Dallas Morning Star)

• Others are reinventing their model, trimming home delivery to 4 days/week with digital PDF versions replacing paper versions on non-delivery days (Cleveland Plain Dealer)(Cleveland Plain Dealer)

• Yet others are trimming the sizes of their papers to save on paper costs (The Denver Post and St. Paul Pioneer Press)

16

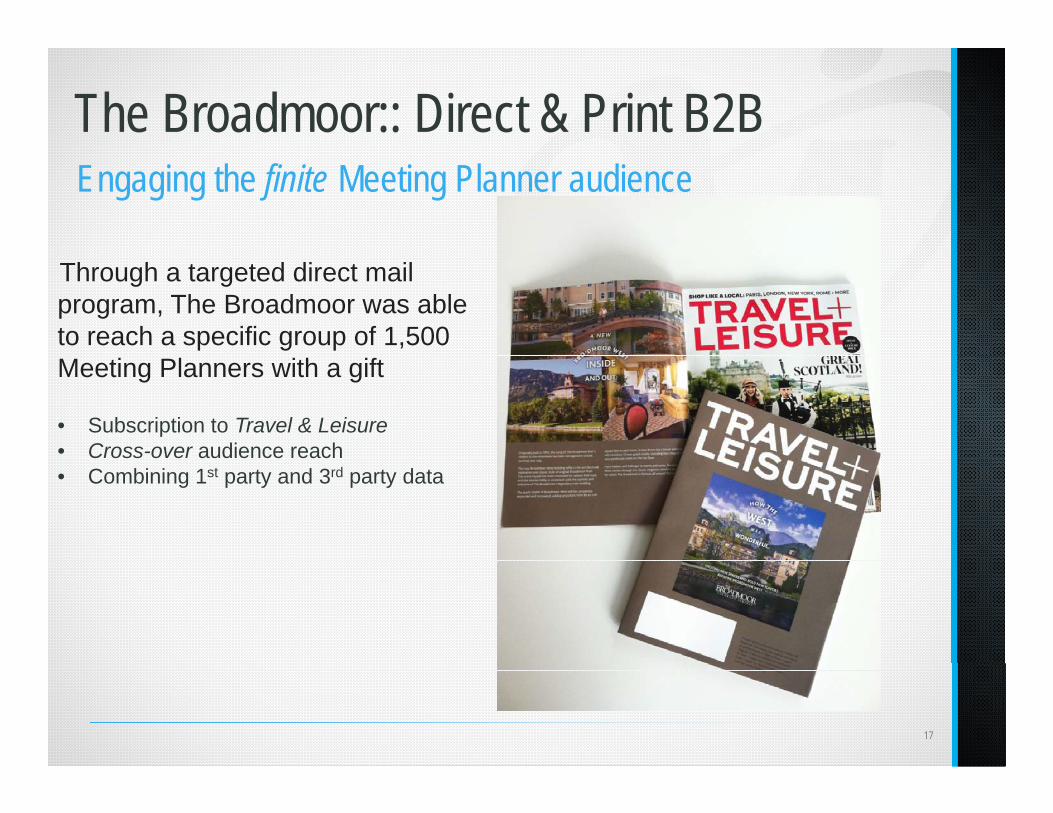

The Broadmoor:: Direct & Print B2BEngaging the finite Meeting Planner audience

Through a targeted direct mail program, The Broadmoor was able to reach a specific group of 1,500

• Subscription to Travel & Leisure• Cross-over audience reach

Meeting Planners with a gift

C oss o e aud e ce eac• Combining 1st party and 3rd party data

17

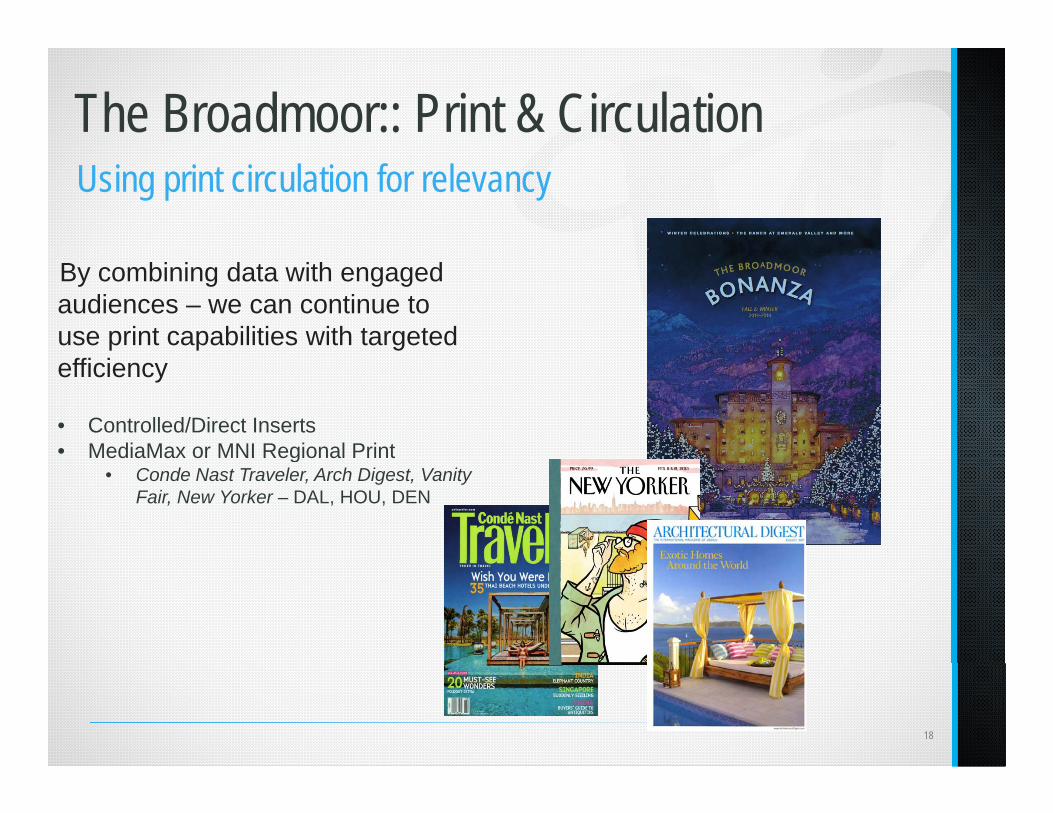

The Broadmoor:: Print & CirculationUsing print circulation for relevancy

By combining data with engaged audiences – we can continue to use print capabilities with targeted

• Controlled/Direct Inserts• MediaMax or MNI Regional Print

efficiency

ed a a o eg o a t• Conde Nast Traveler, Arch Digest, Vanity

Fair, New Yorker – DAL, HOU, DEN

18

2014 Media Landscape :: Radio & audible growth

An emerging market of niches.Both terrestrial and Internet radio are increasingly “going mobile”

• Terrestrial radio increasingly taking place in carsTerrestrial radio increasingly taking place in cars• Internet radio increasingly taking place in the home on smartphones

and tablets… and cars

Terrestrial radioFocus predominantly on prime dayparts (AM Drive, Mid-day and PM Drive).Leverage the human element of DJs through g glive reads or other interactive opportunities.

Online radio stationsCompletely different approach – streaming can be passive, break through the clutter to overcome a visual platform in an audio realm.

19

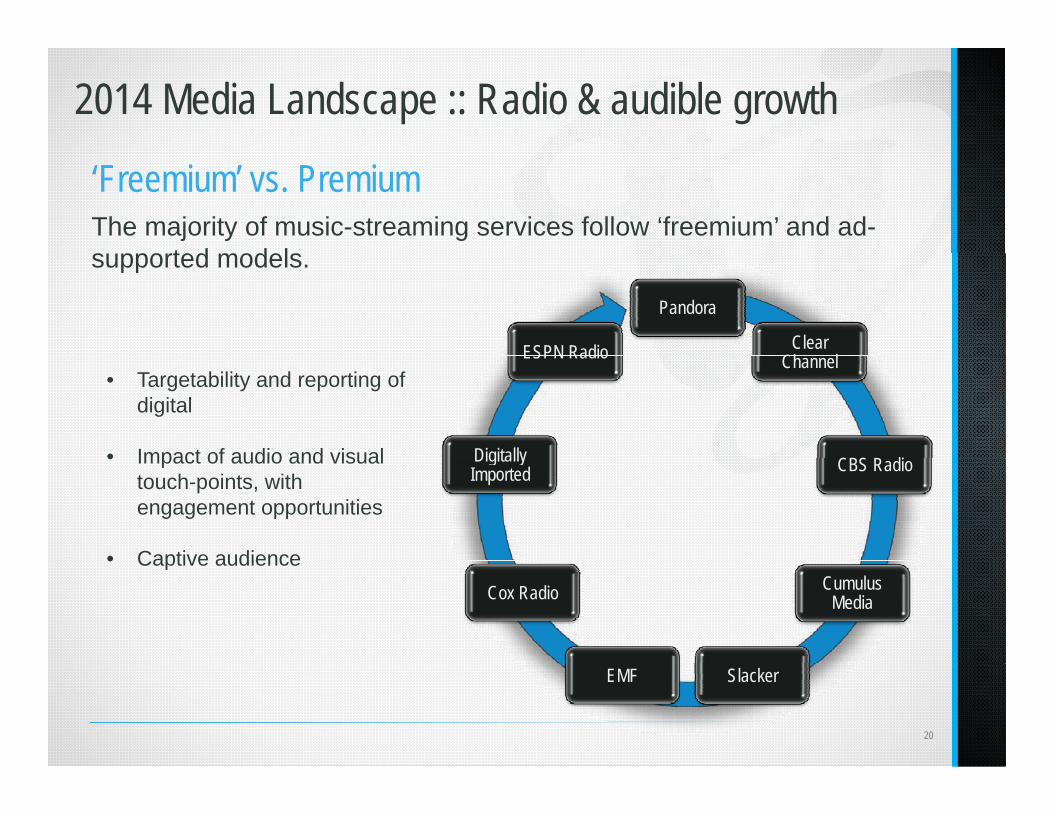

2014 Media Landscape :: Radio & audible growth

‘Freemium’ vs. PremiumThe majority of music-streaming services follow ‘freemium’ and ad-

t d d lsupported models.

Pandora

Clear Ch lESPN Radio Channel

CBS R diDigitally

ESPN Radio• Targetability and reporting of

digital

• Impact of audio and visual CBS RadioDigitally Imported

• Impact of audio and visual touch-points, with engagement opportunities

• Captive audienceCumulus

MediaCox Radio

• Captive audience

20

SlackerEMF

2014 Media Landscape :: OOH’s experimental outreachNo boundariesNo boundaries.The lines have blurred between traditional and non-traditional Out of Home; innovative thinking

iwins.• Digital place-based targeting:

- Customization with different forms of digital outdoor advertising will allow more clients tooutdoor advertising will allow more clients to directly target specific audiences with:

o Providing an engaging mediumo Interactive displayso LED technology o Social Media crossover appealo Government or Private sub-contracting

21

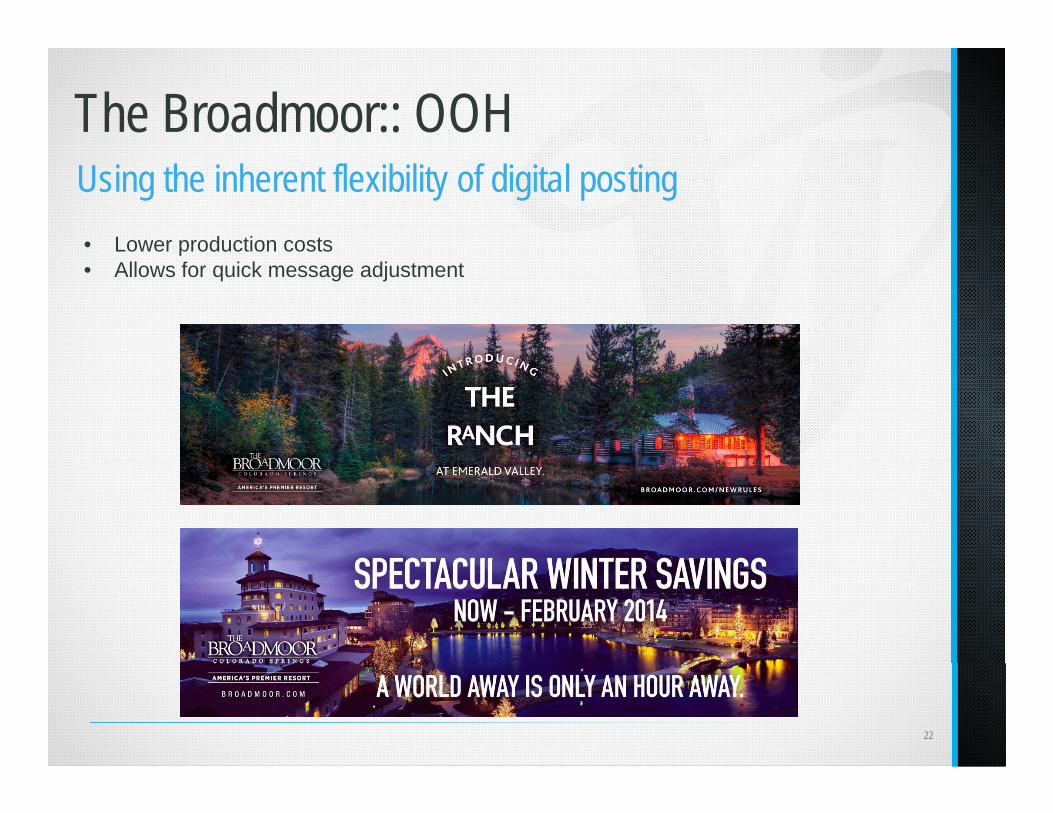

The Broadmoor:: OOHUsing the inherent flexibility of digital posting• Lower production costsp• Allows for quick message adjustment

22

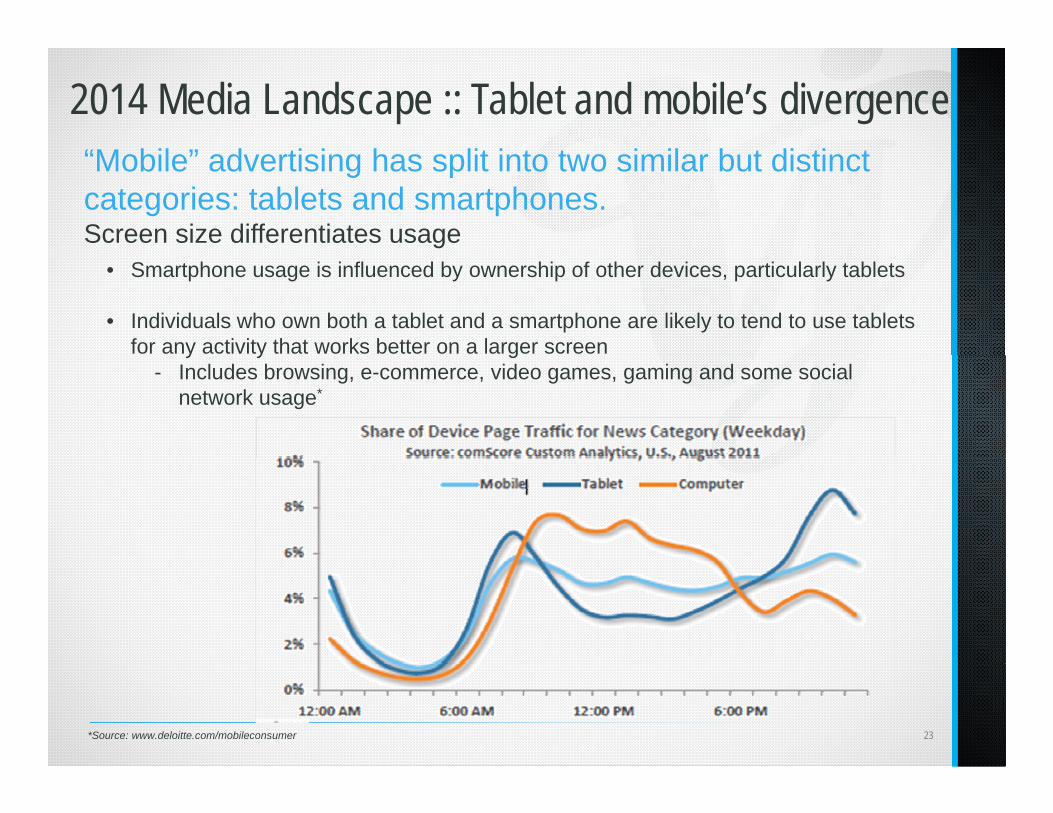

2014 Media Landscape :: Tablet and mobile’s divergence“M bil ” d ti i h lit i t t i il b t di ti t“Mobile” advertising has split into two similar but distinct categories: tablets and smartphones.Screen size differentiates usage

• Smartphone usage is influenced by ownership of other devices, particularly tablets

• Individuals who own both a tablet and a smartphone are likely to tend to use tablets for any activity that works better on a larger screeny y g

- Includes browsing, e-commerce, video games, gaming and some social network usage*

23*Source: www.deloitte.com/mobileconsumer

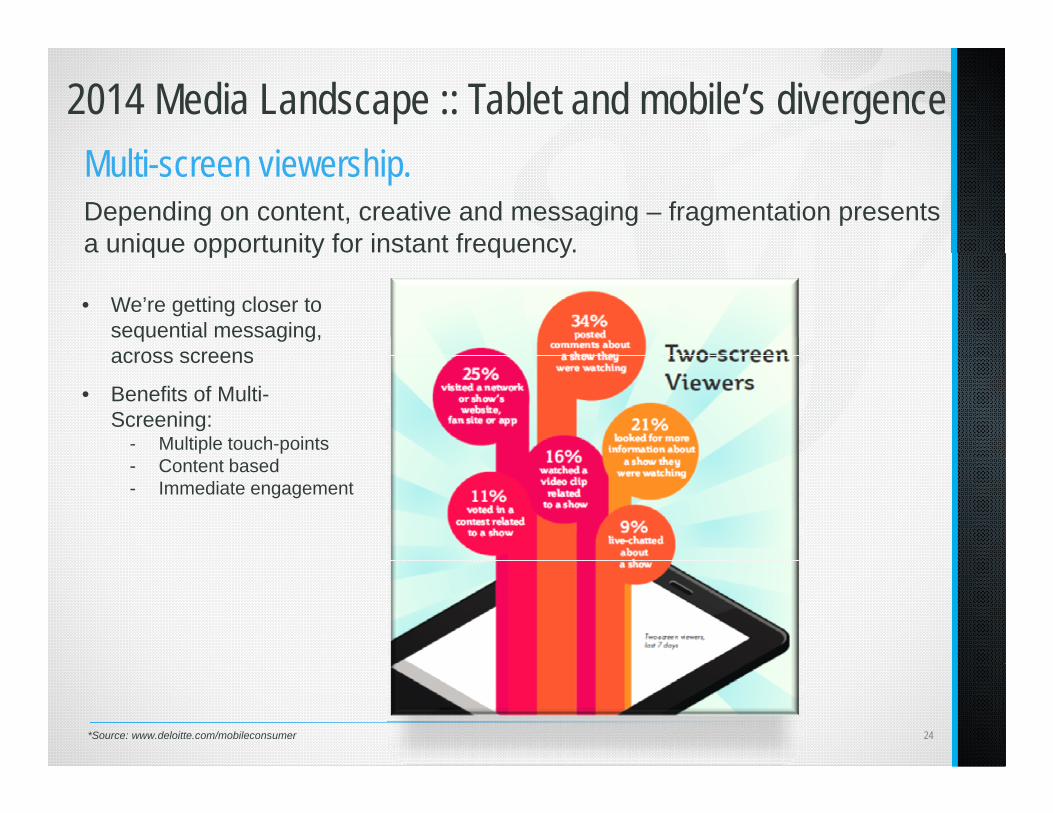

2014 Media Landscape :: Tablet and mobile’s divergenceM l i i hiMulti-screen viewership.Depending on content, creative and messaging – fragmentation presents a unique opportunity for instant frequency. q pp y q y

• We’re getting closer to sequential messaging, across screensacross screens

• Benefits of Multi-Screening:

- Multiple touch-points- Content based- Immediate engagement

24*Source: www.deloitte.com/mobileconsumer

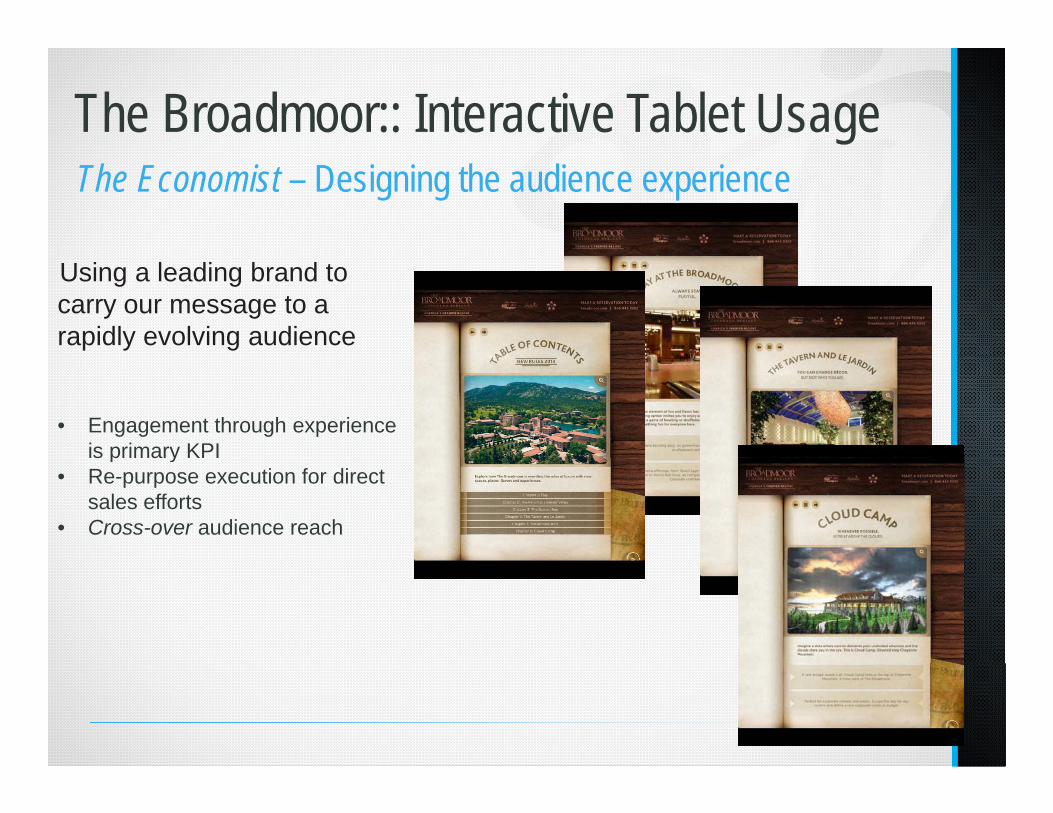

The Broadmoor:: Interactive Tablet UsageThe Economist – Designing the audience experience

Using a leading brand to carry our message to a rapidly evolving audience

• Engagement through experience is primary KPIs p a y

• Re-purpose execution for direct sales efforts

• Cross-over audience reach

25

2014 Media Landscape :: Digital’s… everythingNew is the new normNew is the new norm.

• Measurement continues to play catch up with technology• “Success” translates to established KPIsSuccess translates to established KPIs• Advertisers are understanding the rapid evolution

- Reach for awareness goalsg

- Connection for likeability

- Engagement for Brand affinityo Dwell timeo Dwell timeo Time spento Video completiono CTA

o Variable roles for Creativeo Variable roles for Creativeo Flash vs. Rich

o Linking Offline & Online metricso NAVIS & The Broadmoor

26

2014 Media Landscape :: Digital’s… everything

A rise of technology in buying as well.Programmatic and exchange-based purchase options

• In a real-time media world, understanding how much to pay to talk to someone is as critical as knowing which person to talk to

• DSPs, RTB, and ad exchanges proliferate in the current market• Best Practice for Implementation:

- Stay balanced- Success metrics- Automate – don’t autopilot

Programmatic

p- Data interpretation- Controlled optimization Real Time Bidding

Ad ExchangesAd Exchanges

27

2014 Media Landscape :: Digital’s… everything

Branded content is on the rise – still!Four drivers of branded contentFour drivers of branded content.

1. Classic revenue streams are eroding2. The “feed” creates a new norm3. Brands double down on content4. New Revenue – Product placement, stadium

naming, sponsored contribution

28

2014 Media Landscape :: Digital’s… everything

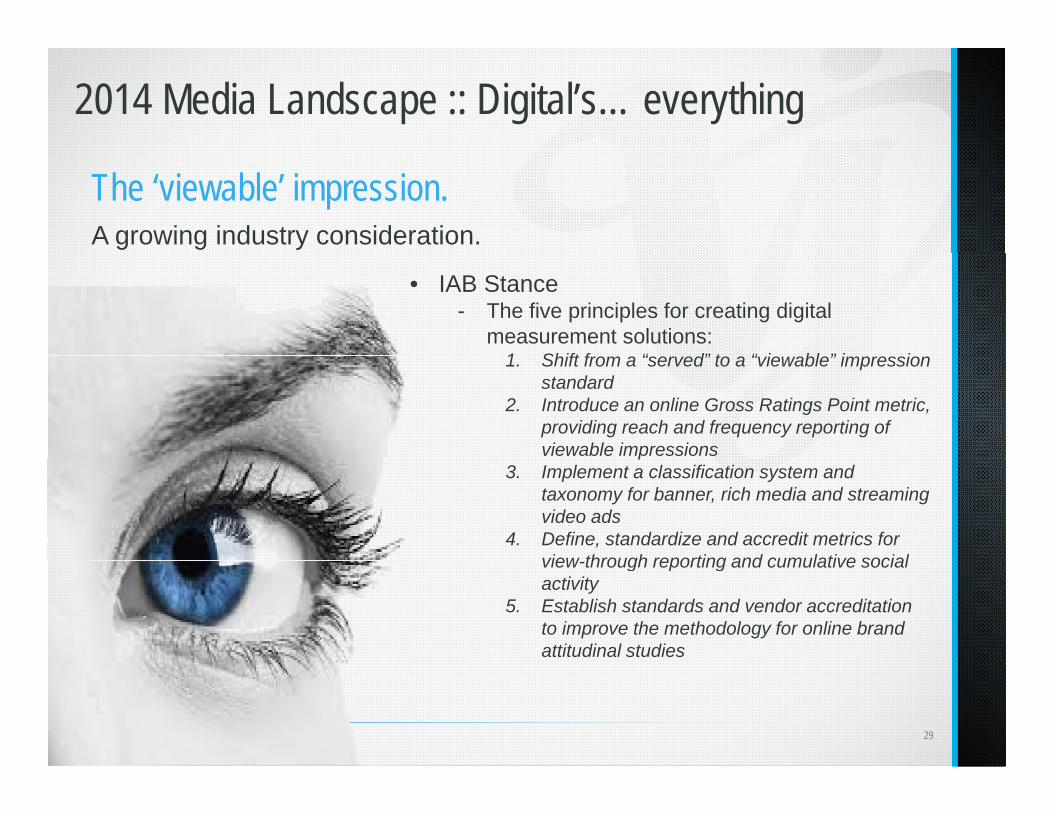

The ‘viewable’ impression.A growing industry consideration.

• IAB Stance- The five principles for creating digital

measurement solutions:1 Shift f “ d” t “ i bl ” i i1. Shift from a “served” to a “viewable” impression

standard2. Introduce an online Gross Ratings Point metric,

providing reach and frequency reporting of viewable impressionsp

3. Implement a classification system and taxonomy for banner, rich media and streaming video ads

4. Define, standardize and accredit metrics for view through reporting and cumulative socialview-through reporting and cumulative social activity

5. Establish standards and vendor accreditation to improve the methodology for online brand attitudinal studies

29

2014 Media Landscape :: Social’s ‘tween’ years

Declining influence… but a growth in initial reach. Social plays a dominant role in the post-view engagement process.

There is a tangible decline as consumers forgo the social networking

• Consumers are becoming more interested

• There is a tangible decline, as consumers forgo the social networking site in favor of visiting a brand’s website

in activities such as store locator usage• Learning about the brand,

and downloading relevant information• Visits to a brand’s Facebook page are aVisits to a brand s Facebook page are a

popular form of engagement- “Likes” are one-dimensional and offer no real

engagement- “Likes” have dropped by 9% over the last year Likes have dropped by 9% over the last year,

while visits to the advertiser’s website rose by more than 20%

30

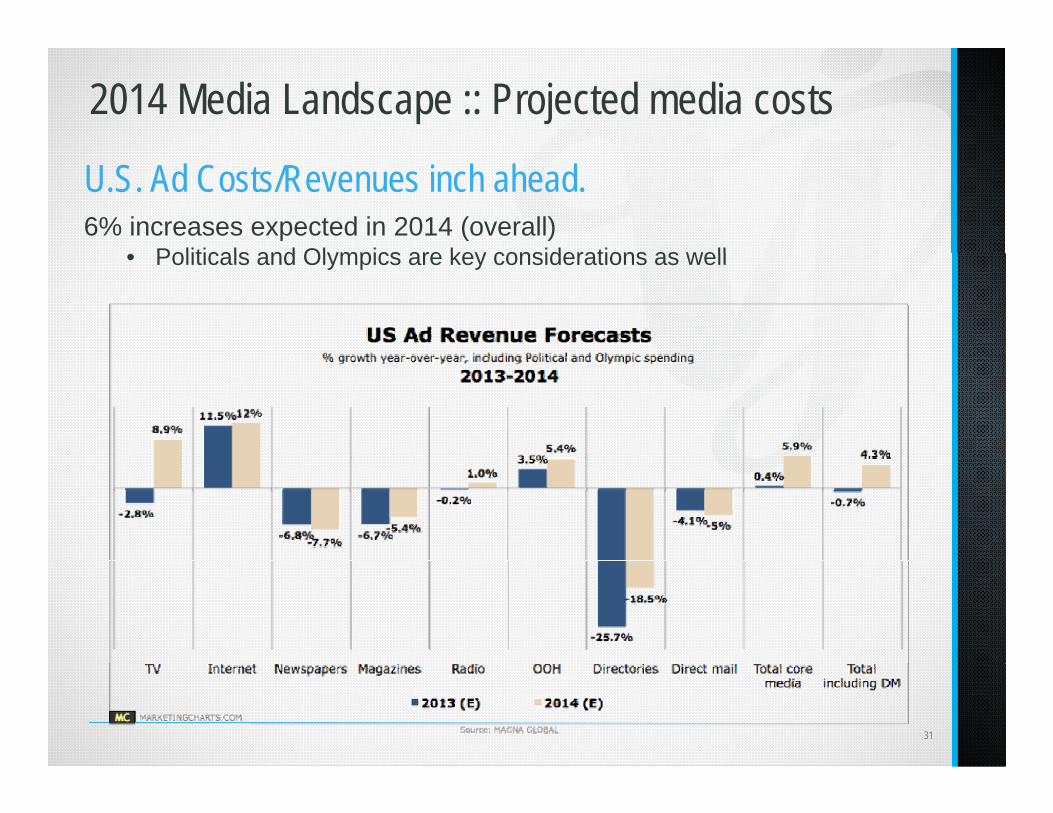

2014 Media Landscape :: Projected media costs

U.S. Ad Costs/Revenues inch ahead.6% increases expected in 2014 (overall)

Politicals and Olympics are key considerations as well• Politicals and Olympics are key considerations as well

31

2014 Media Landscape:: Big DataBig data is critical to developing a customer-centric culture.The cornerstone; part obstacle and part opportunity

Challenge Opportunityg pp y

32

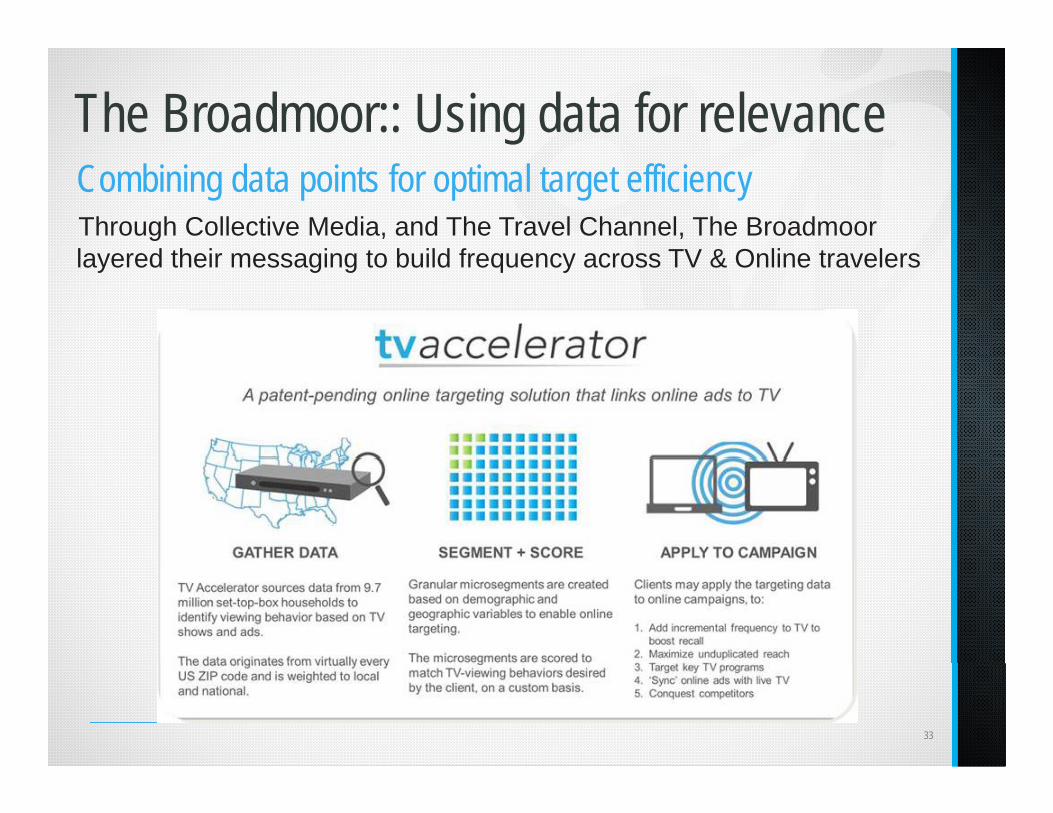

The Broadmoor:: Using data for relevanceCombining data points for optimal target efficiencyThrough Collective Media, and The Travel Channel, The Broadmoorl d th i i t b ild f TV & O li t llayered their messaging to build frequency across TV & Online travelers

33

2014 Media Landscape:: More Facebook changesVid h h f F b kVideo – the next change for Facebook.Originally slated for summer release, but was postponed to this fall

• Rumors of a new video ad unit, presented to every user on the Facebook platform, giving people no choice in receiving the ad

• Most likely short clips automatically playing without sound in News Feeds; a click on the ad would turn on volume and expand into a takeoverclick on the ad would turn on volume and expand into a takeover

- Planning to charge between $1MM–$2.5MM for 15-second video ads. To put things in perspective, 30-second ads for the 2013 Super Bowl hit a record $4 million.

- Additional changes include:o News Feed Updateso Story Bumpingo Last Actoro Last Actoro Chronological by Actoro Cancellation of EdgeRank

34

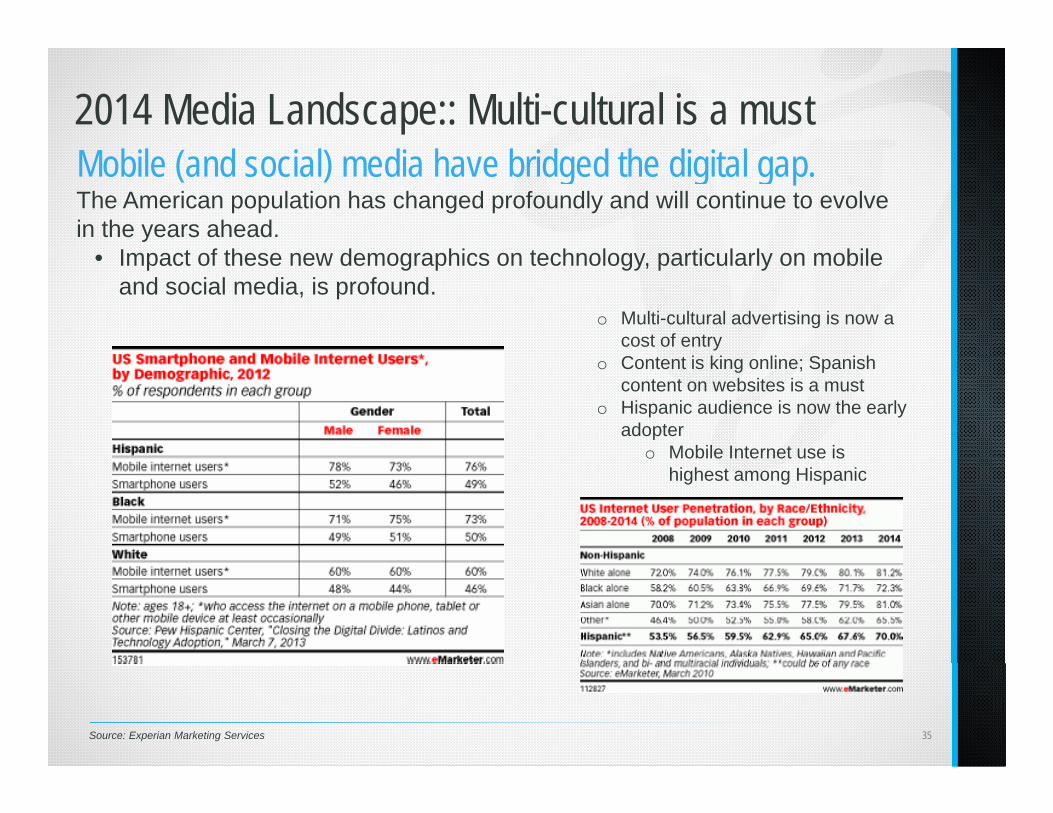

2014 Media Landscape:: Multi-cultural is a mustM bil ( d i l) di h b id d h di i l Mobile (and social) media have bridged the digital gap.The American population has changed profoundly and will continue to evolve in the years ahead.

I t f th d hi t h l ti l l bil• Impact of these new demographics on technology, particularly on mobile and social media, is profound.

o Multi-cultural advertising is now a cost of entryC So Content is king online; Spanish content on websites is a must

o Hispanic audience is now the early adopter

o Mobile Internet use iso Mobile Internet use is highest among Hispanic

Source: Experian Marketing Services 35

Appendix

Resources1. “Viacom Bundling TV, Digital Buys”: http://www.adweek.com/news/television/viacom-bundling-tv-

digital-buys-1390962. “Mobile and TV Watching Set to Change the Landscape of 2012”:

http://blog.mojiva.com/2012/03/mobile-and-tv-watching-set-to-change.html3. TV, Net Growth Propelled By Reach – On Any Screen: On Media4. Tablets Capturing Newspaper Viewers: Center for Media Research5. 30-60 Sec Video Ads Tops Engagement; 1-2 Minutes Tops Viewing: Center for Media Research6. Group M, Nielsen Partner For TV, Internet Metrics:

http://www mediapost com/publications/article/170455/group-m-nielsen-partner-for-tv-internet-http://www.mediapost.com/publications/article/170455/group-m-nielsen-partner-for-tv-internet-metrics.html?edition=44755#axzz2bOa5O6P0

7. Watch TV “On Your Own Schedule”?: Center for Media Research 8. “Streaming music seen as prime opportunity for advertisers”: IAB Smart Brief9. The Cross Platform Report 6/2013 – Nielsen

“10. “Video Monetization Report”: Free Wheel11. Pandora Teams With Strata, Mediaocean To Simplify Ad-Buying: Online Media Daily12. “Daily habits of tablet users”: Mobile Matters13. Print is Dead?: Forbes14. Magna Global 2014 Projections14. Magna Global 2014 Projections15. Crack the consumer code Hispanic market overview 201316. Cross-cultural report by Ogilvy and Mather17. http://www.informationweek.com/software/productivity-applications/googles-growth-path-6-

challenges/23250007818 eMarketer 2014 Forecast18. eMarketer 2014 Forecast19. http://stateofthemedia.org/2012/mobile-devices-and-news-consumption-some-good-signs-for-

journalism/38