2012 newsletter q1 abc dubai

DESCRIPTION

Newsletter ABC DubaiTRANSCRIPT

IT’S ALL ABOUT

TRADE

The first quarter has been buzzing

with of talk about trade in the

American business community, from

the surge in exports from the US to

the UAE, a 36% increase over the

previous year to the anti-corruption and economic sanctions seminar

presented by an ABC member law firm to the recent event with US

Department of Commerce, Assistant Secretary for Export

Enforcement, David Mills, (co-sponsored by the Dubai Chamber) to

the stunning rise in the UAE’s foreign trade to reach a record above

AED 1 trillion. Recovery and optimism is the talk of the town.

The American Business Council The American Business Council

INSIDE Doing Business in the UAE excerpt Anti-Corruption and Economic Sanctions Compliance:

Facts to protect your company Members’ Calendar

IT’S ALL ABOUT TRADE CONTINUED

The Foreign Trade Division of the US Census Bureau announced that exports from the United States to

the United Arab Emirates reached a record level of $15.89 billion in 2011, a 36% increase over exports

in 2010 of $11.67 billion. The UAE is once again America’s number one export market in the Middle

East North Africa (MENA) region and a top 20 destination for US goods worldwide. The previous re-

cord for exports from the US to the UAE of $14.4 billion occurred in 2008.

Trade between the US and the UAE also marked a record high of $18.34 billion in 2011. The UAE ex-

ported $2.44 billion worth of goods to the US in 2011, more than twice its export level to the US in

2010 of $1.15 billion.

Rising investment levels in the UAE across multiple economic sectors including manufacturing, avia-

tion and technology drove the export increase from the US. Aircraft, machinery and autos topped the

list of US exports arriving in the UAE in 2011. Goods manufactured in every state were exported to the

UAE, with December as the highest month for exports, totaling $1.824 billion. The top US export to

the UAE in 2011 was transportation equipment at $5.893 billion. Aluminum products are the single

largest export category from the UAE to the US.

According to Justin Siberell, US Consul General Dubai, “American businesses play a key role in the

commercial life of Dubai and the UAE. American companies have for decades encountered a welcom-

ing business climate here and have, as a result developed strong presence in many economic areas.”

As a large and growing market for US companies, the UAE’s policy of economic diversification and its

ideal geographic location continue to strengthen trade links between the two countries.

I. INTRODUCTION

A foreign company may conduct business in the

UAE by operating from "off-shore" (via an agent or

directly with customers), by operating in a "free

zone" and by operating directly in one or more of

the seven Emirates (but outside of a free zone).

There are both federal and Emirate-specific laws

and regulations, and there can be multiple regula-

tory authorities at the federal and Emirate levels.

Also, the discretionary policies, practices and pro-

cedures of these authorities supplement the official

laws and regulations and can affect business to a

great extent. Determining the most appropriate

alternative depends on many factors, including the

targeted customer base and the nature of the prod-

ucts or services to be offered. Set forth below is an

overview of the primary methods for foreign busi-

nesses to conduct business in the UAE, as well as a

summary of several other key considerations for

doing business in the UAE.

Doing Business in

the U.A.E.

This article will be published in the 2012 ABC Directory in its entirety.

It is supplied by ABC President's Club member

The UAE welcomes foreign direct investment by Ameri-can businesses. However, the rules and requirements for doing business in the UAE are complex and often misun-derstood. This overview identifies the different ways to do business in the UAE and points out important consid-erations, including some important US laws and regula-tions that apply to operations here.

Copyright 2012 - Fulbright & Jaworski L.L.P. The foregoing overview is not intended to substitute for legal advice on specific matters.

II. INDIRECT OPERATIONS – DEALING WITH AGENTS

Foreign entities generally may make private sector product

sales from off-shore directly into the UAE without participation

by a UAE party. In addition, UAE companies with foreign own-

ership may import and resell goods upon obtaining the appro-

priate licenses. However, only UAE nationals (or entities wholly

-owned by UAE nationals) may conduct certain "commercial

agency activities" as a registered commercial agent, with its

associated rights and privileges.

The UAE Commercial Agencies Law, Federal Law No. 18 of

1981, as amended by Federal Law No. 14 of 1988, and Federal

Law No. 13 of 2006 (the "2006 Amendments"), and Federal Law

No. 2 of 2010 (the "2010 Amendments") (collectively, the

"Commercial Agency Law"), regulates and governs the appoint-

ment of registered commercial agents, sales representatives

and distributors in the UAE. The Commercial Agency Law is

supplemented by, inter alia, the UAE Commercial Transactions

Law, Federal Law No. 18 of 1993 (the "Commercial Code"), im-

plementing regulations, custom and practice. Together, the

Commercial Agency Law and the Commercial Code provide the

primary regulatory framework for agency relationships through

which foreign businesses provide products and services in the

UAE.

The Commercial Agency Law is a federal law that applies

throughout the UAE and grants registered commercial agents

formidable statutory rights as detailed below. Certain public

sector sales require the involvement of a registered commercial

agent. Otherwise, a foreign company can choose alternative

means of selling into the UAE that do not involve a registered

commercial agent.

A. Registered commercial agents are entitled to

an exclusive territory covering at least one Emirate for the

specified products or services.

B. Unless otherwise agreed, registered commer-

cial agents are entitled to receive commissions on sales in their

designated territory irrespective of whether such sales are

made by or through the commercial agent.

C. Registered commercial agents are entitled to

prevent products subject to their agency from being imported

into the UAE if the commercial agent is not the consignee,

unless the UAE Council of Ministers has exempted the subject

products from application of the Commercial Agency Law. This

potential exemption of designated products was confirmed as

part of the 2006 Amendments. Products currently excluded

from the application of the Commercial Agency Law include the

following foodstuffs and related products: dry and condensed

milk, frozen and canned vegetables, children's foodstuffs, milk,

poultry, cooking oil, rice, flour, fish products, meat and its prod-

ucts, tea, coffee, cheese, pasta (macaroni, vermicelli), sugar

and diapers.

D. A principal may not terminate or fail to renew

the agency agreement unless there is a material reason justify-

ing such termination or non-renewal. Either party is entitled to

claim compensation for damages suffered and losses incurred

due to termination or non-renewal of a registered commercial

agency. In practice, this is a benefit to the commercial agent

only.

Furthermore, commercial agents are not limited to seeking

remedies under the Commercial Agency Law. For example, a

commercial agent might also claim damages for improper ter-

mination or non-renewal pursuant to the Commercial Code.

E. A registered commercial agent can preclude

the foreign principal from appointing a replacement registered

agent even if the registered agency was for a fixed term that

has expired, unless the former agent consents or the principal

obtains a favorable decision from the specialized agency dis-

putes committee or a court in the UAE.

In addition, the Commercial Agency Law provides that commer-

cial agency agreements shall be governed exclusively by UAE

law notwithstanding any provision to the contrary in the

agency agreement. Furthermore, UAE Cabinet Resolution No. 3

of 2011 Concerning the Commercial Agencies Committee re-

quires parties to submit their disputes to a specialized agency

disputes committee that has original jurisdiction over disputes

regarding registered commercial agency agreements, including

questions of agency de-registration. The committee may refer

disputes to the UAE courts, and parties may also challenge in

court decisions made by the committee.

According to the Commercial Agency Law, a commercial agent

has to register its agency agreement with the UAE Ministry of

Economy and Commerce (“Ministry of Economy”) to claim the

benefits of the Commercial Agency Law. But there have been

instances where some courts have applied the Commercial

Agency Law to unregistered commercial agency agreements in

certain contexts. The 2006 Amendments had led the interna-

tional business community to expect a trend towards more

liberalization in this area, but, the 2010 Amendments were a

step in the opposite direction and a clear signal of greater, or at

least continued, protectionism for UAE commercial agents.

The statutory protections for commercial agents under the

Commercial Agency Law create an obvious disincentive to for-

eign entities to do business through registered commercial

agencies if alternative means are available. The three most

common alternative means are: (i) to sell directly from over-

seas (i.e., "off-shore") to the end-user customer; (ii) to sell

through an agent other than a registered commercial agent;

and (iii) to establish a direct legal presence in the UAE.

Evaluating statutory protections and other commercial and

legal principles and practices are important not only in negoti-

ating new arrangements with UAE distributors, representatives

and agents, but also in ending any such relationships. Invaria-

bly, termination of agency relationships is contentious, time

consuming and expensive, even if the agent is not a registered

commercial agent.

III. DIRECT OPERATIONS

In addition to a foreign entity establishing an "indirect" busi-

ness presence in the UAE via an agency relationship, there are

several alternatives by which a foreign entity may be licensed

to undertake specified activities on a direct, permanent basis in

the UAE. The UAE Commercial Companies Law, Federal Law

No. 8 of 1984, as amended (the "Companies Law"), provides for

a number of different corporate structures. The primary alter-

natives for foreign entities to establish direct business opera-

tions in the UAE (outside the free zones) are (i) registration of a

branch office and (ii) incorporation of a limited liability com-

pany with a UAE national "partner".

By establishing a direct business presence in the UAE, a foreign

entity is permitted to engage in specified activities as licensed

by the relevant UAE authorities. Except for certain "free zone"

registrations and operations discussed below, entities engaging

in commercial activities in the UAE must be separately regis-

tered and licensed at the federal UAE level (subject to excep-

tions for certain branch offices, e.g., see Section III.A below), as

well as in each Emirate where they wish to operate. Commer-

cial entities must also be registered with, inter alia, the Immi-

gration Department of the UAE Ministry of Interior (the

"Immigration Department") and the UAE Ministry of Labor and Social

Affairs (the "Ministry of Labor") to secure employment/residency visas

(if necessary) and work permits for their personnel.

A. Branch Office

Through registration of a branch office, a foreign entity can

establish, on a wholly owned basis, a direct business presence

to perform specified activities in the Emirate where the branch

is licensed. No UAE participation is required other than utilizing

the services of a UAE national "local agent" to handle certain

administrative matters, as described below. Such a branch of-

fice is not a separate and distinct legal entity from the foreign

company. Rather, the foreign company itself is licensed locally

to undertake specified activities in the UAE through its branch

office. The foreign company is fully responsible for the liabili-

ties of the branch office.

Doing Business in the U.A.E. excerpt from the 2012 ABC membership Directory

II. INDIRECT OPERATIONS – DEALING WITH AGENTS

Foreign entities generally may make private sector product

sales from off-shore directly into the UAE without participation

by a UAE party. In addition, UAE companies with foreign own-

ership may import and resell goods upon obtaining the appro-

priate licenses. However, only UAE nationals (or entities wholly

-owned by UAE nationals) may conduct certain "commercial

agency activities" as a registered commercial agent, with its

associated rights and privileges.

The UAE Commercial Agencies Law, Federal Law No. 18 of

1981, as amended by Federal Law No. 14 of 1988, and Federal

Law No. 13 of 2006 (the "2006 Amendments"), and Federal Law

No. 2 of 2010 (the "2010 Amendments") (collectively, the

"Commercial Agency Law"), regulates and governs the appoint-

ment of registered commercial agents, sales representatives

and distributors in the UAE. The Commercial Agency Law is

supplemented by, inter alia, the UAE Commercial Transactions

Law, Federal Law No. 18 of 1993 (the "Commercial Code"), im-

plementing regulations, custom and practice. Together, the

Commercial Agency Law and the Commercial Code provide the

primary regulatory framework for agency relationships through

which foreign businesses provide products and services in the

UAE.

The Commercial Agency Law is a federal law that applies

throughout the UAE and grants registered commercial agents

formidable statutory rights as detailed below. Certain public

sector sales require the involvement of a registered commercial

agent. Otherwise, a foreign company can choose alternative

means of selling into the UAE that do not involve a registered

commercial agent.

A. Registered commercial agents are entitled to

an exclusive territory covering at least one Emirate for the

specified products or services.

B. Unless otherwise agreed, registered commer-

cial agents are entitled to receive commissions on sales in their

designated territory irrespective of whether such sales are

made by or through the commercial agent.

C. Registered commercial agents are entitled to

prevent products subject to their agency from being imported

into the UAE if the commercial agent is not the consignee,

unless the UAE Council of Ministers has exempted the subject

products from application of the Commercial Agency Law. This

potential exemption of designated products was confirmed as

part of the 2006 Amendments. Products currently excluded

from the application of the Commercial Agency Law include the

following foodstuffs and related products: dry and condensed

milk, frozen and canned vegetables, children's foodstuffs, milk,

poultry, cooking oil, rice, flour, fish products, meat and its prod-

ucts, tea, coffee, cheese, pasta (macaroni, vermicelli), sugar

and diapers.

D. A principal may not terminate or fail to renew

the agency agreement unless there is a material reason justify-

ing such termination or non-renewal. Either party is entitled to

claim compensation for damages suffered and losses incurred

due to termination or non-renewal of a registered commercial

agency. In practice, this is a benefit to the commercial agent

only.

Furthermore, commercial agents are not limited to seeking

remedies under the Commercial Agency Law. For example, a

commercial agent might also claim damages for improper ter-

mination or non-renewal pursuant to the Commercial Code.

E. A registered commercial agent can preclude

the foreign principal from appointing a replacement registered

agent even if the registered agency was for a fixed term that

has expired, unless the former agent consents or the principal

obtains a favorable decision from the specialized agency dis-

putes committee or a court in the UAE.

In addition, the Commercial Agency Law provides that commer-

cial agency agreements shall be governed exclusively by UAE

law notwithstanding any provision to the contrary in the

agency agreement. Furthermore, UAE Cabinet Resolution No. 3

of 2011 Concerning the Commercial Agencies Committee re-

quires parties to submit their disputes to a specialized agency

disputes committee that has original jurisdiction over disputes

regarding registered commercial agency agreements, including

questions of agency de-registration. The committee may refer

disputes to the UAE courts, and parties may also challenge in

court decisions made by the committee.

According to the Commercial Agency Law, a commercial agent

has to register its agency agreement with the UAE Ministry of

Economy and Commerce (“Ministry of Economy”) to claim the

benefits of the Commercial Agency Law. But there have been

instances where some courts have applied the Commercial

Agency Law to unregistered commercial agency agreements in

certain contexts. The 2006 Amendments had led the interna-

tional business community to expect a trend towards more

liberalization in this area, but, the 2010 Amendments were a

step in the opposite direction and a clear signal of greater, or at

least continued, protectionism for UAE commercial agents.

The statutory protections for commercial agents under the

Commercial Agency Law create an obvious disincentive to for-

eign entities to do business through registered commercial

agencies if alternative means are available. The three most

common alternative means are: (i) to sell directly from over-

seas (i.e., "off-shore") to the end-user customer; (ii) to sell

through an agent other than a registered commercial agent;

and (iii) to establish a direct legal presence in the UAE.

Evaluating statutory protections and other commercial and

legal principles and practices are important not only in negoti-

ating new arrangements with UAE distributors, representatives

and agents, but also in ending any such relationships. Invaria-

bly, termination of agency relationships is contentious, time

consuming and expensive, even if the agent is not a registered

commercial agent.

III. DIRECT OPERATIONS

In addition to a foreign entity establishing an "indirect" busi-

ness presence in the UAE via an agency relationship, there are

several alternatives by which a foreign entity may be licensed

to undertake specified activities on a direct, permanent basis in

the UAE. The UAE Commercial Companies Law, Federal Law

No. 8 of 1984, as amended (the "Companies Law"), provides for

a number of different corporate structures. The primary alter-

natives for foreign entities to establish direct business opera-

tions in the UAE (outside the free zones) are (i) registration of a

branch office and (ii) incorporation of a limited liability com-

pany with a UAE national "partner".

By establishing a direct business presence in the UAE, a foreign

entity is permitted to engage in specified activities as licensed

by the relevant UAE authorities. Except for certain "free zone"

registrations and operations discussed below, entities engaging

in commercial activities in the UAE must be separately regis-

tered and licensed at the federal UAE level (subject to excep-

tions for certain branch offices, e.g., see Section III.A below), as

well as in each Emirate where they wish to operate. Commer-

cial entities must also be registered with, inter alia, the Immi-

gration Department of the UAE Ministry of Interior (the

"Immigration Department") and the UAE Ministry of Labor and Social

Affairs (the "Ministry of Labor") to secure employment/residency visas

(if necessary) and work permits for their personnel.

A. Branch Office

Through registration of a branch office, a foreign entity can

establish, on a wholly owned basis, a direct business presence

to perform specified activities in the Emirate where the branch

is licensed. No UAE participation is required other than utilizing

the services of a UAE national "local agent" to handle certain

administrative matters, as described below. Such a branch of-

fice is not a separate and distinct legal entity from the foreign

company. Rather, the foreign company itself is licensed locally

to undertake specified activities in the UAE through its branch

office. The foreign company is fully responsible for the liabili-

ties of the branch office.

A branch office may conduct only those activities specified in its

license. The issuance of licenses to branch offices involves dis-

cretion on the part of the governmental authorities, including

with respect to whether they believe the foreign company is one

they desire to have operating in the UAE and in the applicable

Emirate, and the types and scope of activities they will allow.

A representative office is a type of branch office that is not sup-

posed to engage in sales, services or any other type of commer-

cial activity. Rather, a representative office is only supposed to

act as a liaison or administrative office to promote the com-

pany’s products and services and to facilitate business between

the foreign principal and its customers (or intermediaries).

Some direct contact with customers is permitted, but employees

at a representative office are not authorized to engage in sales

or perform services. The approvals for representative offices

generally can be obtained more quickly and with less govern-

mental scrutiny than for other types of branch offices.

Although exceptions were granted in the past, pursuant to Min-

isterial Resolution No. 377 of 2010 (“Resolution No. 377”)

branch offices may not engage in "trading" activities (i.e., buying

and/or importing for resale in the UAE). Thus, branch offices are

not allowed to engage in trading, but this should not affect trad-

ing licenses previously granted to branch offices.

Resolution No. 377 authorizes free zone entities to form branch

offices in the UAE, subject to satisfying licensing requirements.

Further, under Resolution No. 377 branch offices are not re-

quired to register at the Federal level (i.e., the Ministry of Econ-

omy) to perform a special purpose contract with a government

party in the UAE if the requisite license corresponding to the

contract is obtained from the relevant Emirate licensing author-

ity.

Dubai Law No. 13 of 2011 Regulating Economic Activities in Du-

bai (“Dubai Law No. 13”) also contemplates the possibility of

free zone entities establishing branch offices outside the free

zone in Dubai “proper.” Dubai Law No. 13 also provides that

free zone entities may be authorized to engage in their licensed

activities in Dubai proper, but under certain terms and condi-

tions to be issued by the Executive Council. Such terms and con-

ditions have not yet been clarified. Consequently it remains to

be seen how significantly the law will expand the ability of free

zone entities to operate outside the free zones in Dubai proper.

Under Ministerial Resolution No. 208 of 2011, a foreign com-

pany must deposit a sum of Dhs. 50,000 with the Ministry of

Economy for each branch office to be opened in the UAE. Previ-

ously, foreign companies were required to submit a bank guar-

antee for this amount from a bank operating in the UAE.

According to the Companies Law, a foreign entity is required to

appoint a UAE national "local agent" for its branch office. How-

ever, for certain registrations, such as branches providing ser-

vices to the military or financial services, the relevant special

purpose regulatory authority may choose to serve as a nominal

local agent. This determination is made by the relevant regula-

tory authority on a case by case basis.

The local agent is not permitted to own equity in the branch

office. Similarly, the local agent generally may not interfere in

the substantive management of the branch office, unless other-

wise agreed given that the terms of the agency relationship are

a matter of contract between the parties. In practice, a foreign

entity typically contracts with a local agent to provide specific

administrative services such as communicating with government

departments to process the registration and licensing renewals

for the foreign company, and processing visas and work permits

for its personnel. The level and form of compensation paid to

the local agent varies widely in practice and is a contractual mat-

ter to be agreed between the local agent and the foreign entity.

There is no specific level or form of compensation stated under

UAE law. Some local agents charge a fixed annual fee, while

others charge a percentage of revenue, in which case a cap on

compensation is advisable. As for all foreign intermediaries, US

companies should perform FCPA due diligence on the local

agent candidate.

B. Limited Liability Company

UAE limited liability companies ("LLCs") must have a minimum

of two and a maximum of 50 equity owners and a minimum of

51% equity ownership by UAE nationals (or entities wholly-owned

by UAE nationals). In this summary, we refer to such equity

owners as "partners", but parties commonly use "shareholder"

and "partner" interchangeably. The minimum capitalization

required by the Companies Law for a limited liability company

(e.g., Dhs. 150,000) was abolished in June 2009 pursuant to Fed-

eral Law No. 1 of 2009 on Amending Certain Provisions of Fed-

eral Law No. 8 of 1984 Concerning Commercial Companies. The

current requirement is to have sufficient capital for the busi-

ness, which is to be determined by the partners. However, in

practice, the authorities have discretion to impose their own

requirements (e.g., Dhs. 300,000 in Dubai, and also minimum

capitalization requirements for certain types of activities, such

as industrial and manufacturing operations). As a practical mat-

ter most businesses require a certain amount of capital to oper-

ate, often greater than Dhs. 150,000. Also, there is risk that

having no minimum amount of capital could potentially expose

partners to greater personal liability due to insufficiently capital-

izing the business. In any event, it will take time to assess the

practical impact of eliminating the minimum capitalization re-

quirement for an LLC.

Recent press reports indicate that the UAE Council of Ministers

has approved a new Companies Law that will relax existing for-

eign ownership restrictions (e.g., permit more than 49% foreign

ownership in an LLC), at least for certain sectors, and impose

minimum corporate governance standards. However, as of

early 2012 the new law has not been published in the official

gazette.

Pursuant to the Companies Law, LLCs may be licensed to engage

in a wide range of commercial activities, except for banking, in-

surance and the investment of money for third parties. For ex-

ample, an LLC may engage in trading. An LLC usually is the pre-

ferred vehicle for a joint venture between a foreign party and a

UAE party.

The creation, capitalization, and governance of an LLC is gov-

erned by the Companies Law and by its charter document (e.g.,

Articles or Memorandum of Association), an Arabic language

contract among the LLC partners that is registered with the local

authorities. This charter document usually is supplemented by

other agreements, such as joint venture agreements. The Com-

panies Law gives the partners a great degree of latitude to nego-

tiate the terms for governance of their LLC. But, in the event of

a conflict between any such supplemental agreements and ei-

ther the registered charter document or the Companies Law,

the latter likely will control.

Parties have implemented a variety of measures (some lawful

and some not) trying to ameliorate the limitations on foreign

ownership of LLCs imposed by the Companies Law. Although

the Companies Law requires at least 51% of the capital of an LLC

to be owned by UAE nationals, it also permits profits and losses

to be split by the LLC partners as they may agree. The various

Emirate licensing authorities impose restrictions in practice, of-

ten limiting to 80% the profits allocable to the foreign partners.

Some foreign parties have tried to engage UAE nationals to par-

ticipate in LLCs as mere "sponsors" or "nominees" (often re-

ferred to colloquially as "silent" or "sleeping" partners) solely for

the sake of appearing to satisfy the UAE national ownership re-

quirements imposed by the Companies Law. Such arrange-

ments typically commit the UAE national to relinquish all profits,

voting rights and other rights of ownership to the foreign party,

often by a "side agreement" not reflected in the registered char-

tered document. Such arrangements are not legal under the

Companies Law, and are criminal violations under Federal Law

No. 17 of 2004 on Combating of Commercial Concealment

(the "Commercial Concealment Law"), which proscribes such

arrangements and imposes stringent penalties on the UAE na-

tional "concealing party" as well as the foreign "concealed

party". Enforcement of the Commercial Concealment Law,

which originally was to be effective in November 2007, was de-

ferred until December 31, 2009 by UAE Cabinet Resolution No.

229/12 of 2007. We are not aware of any subsequent law or

resolution deferring the implementation of the Commercial Con-

cealment Law or issuance of any implementing regulations.

Thus, it would be advisable to assume that the Commercial Con-

cealment Law took effect as of January 1, 2010, although there

have not been reports of active public enforcement of that law.

Even if the authorities choose not to prosecute violators, foreign

parties need to understand that reliance on the types of ar-

rangements described above may be misplaced due to serious

questions about their enforceability and the potential account-

ing and disclosure complications related to securities matters for

the foreign partner and merger and acquisition activity relating

to the LLC.

Doing Business in the U.A.E. excerpt from the 2012 ABC membership Directory

A branch office may conduct only those activities specified in its

license. The issuance of licenses to branch offices involves dis-

cretion on the part of the governmental authorities, including

with respect to whether they believe the foreign company is one

they desire to have operating in the UAE and in the applicable

Emirate, and the types and scope of activities they will allow.

A representative office is a type of branch office that is not sup-

posed to engage in sales, services or any other type of commer-

cial activity. Rather, a representative office is only supposed to

act as a liaison or administrative office to promote the com-

pany’s products and services and to facilitate business between

the foreign principal and its customers (or intermediaries).

Some direct contact with customers is permitted, but employees

at a representative office are not authorized to engage in sales

or perform services. The approvals for representative offices

generally can be obtained more quickly and with less govern-

mental scrutiny than for other types of branch offices.

Although exceptions were granted in the past, pursuant to Min-

isterial Resolution No. 377 of 2010 (“Resolution No. 377”)

branch offices may not engage in "trading" activities (i.e., buying

and/or importing for resale in the UAE). Thus, branch offices are

not allowed to engage in trading, but this should not affect trad-

ing licenses previously granted to branch offices.

Resolution No. 377 authorizes free zone entities to form branch

offices in the UAE, subject to satisfying licensing requirements.

Further, under Resolution No. 377 branch offices are not re-

quired to register at the Federal level (i.e., the Ministry of Econ-

omy) to perform a special purpose contract with a government

party in the UAE if the requisite license corresponding to the

contract is obtained from the relevant Emirate licensing author-

ity.

Dubai Law No. 13 of 2011 Regulating Economic Activities in Du-

bai (“Dubai Law No. 13”) also contemplates the possibility of

free zone entities establishing branch offices outside the free

zone in Dubai “proper.” Dubai Law No. 13 also provides that

free zone entities may be authorized to engage in their licensed

activities in Dubai proper, but under certain terms and condi-

tions to be issued by the Executive Council. Such terms and con-

ditions have not yet been clarified. Consequently it remains to

be seen how significantly the law will expand the ability of free

zone entities to operate outside the free zones in Dubai proper.

Under Ministerial Resolution No. 208 of 2011, a foreign com-

pany must deposit a sum of Dhs. 50,000 with the Ministry of

Economy for each branch office to be opened in the UAE. Previ-

ously, foreign companies were required to submit a bank guar-

antee for this amount from a bank operating in the UAE.

According to the Companies Law, a foreign entity is required to

appoint a UAE national "local agent" for its branch office. How-

ever, for certain registrations, such as branches providing ser-

vices to the military or financial services, the relevant special

purpose regulatory authority may choose to serve as a nominal

local agent. This determination is made by the relevant regula-

tory authority on a case by case basis.

The local agent is not permitted to own equity in the branch

office. Similarly, the local agent generally may not interfere in

the substantive management of the branch office, unless other-

wise agreed given that the terms of the agency relationship are

a matter of contract between the parties. In practice, a foreign

entity typically contracts with a local agent to provide specific

administrative services such as communicating with government

departments to process the registration and licensing renewals

for the foreign company, and processing visas and work permits

for its personnel. The level and form of compensation paid to

the local agent varies widely in practice and is a contractual mat-

ter to be agreed between the local agent and the foreign entity.

There is no specific level or form of compensation stated under

UAE law. Some local agents charge a fixed annual fee, while

others charge a percentage of revenue, in which case a cap on

compensation is advisable. As for all foreign intermediaries, US

companies should perform FCPA due diligence on the local

agent candidate.

B. Limited Liability Company

UAE limited liability companies ("LLCs") must have a minimum

of two and a maximum of 50 equity owners and a minimum of

51% equity ownership by UAE nationals (or entities wholly-owned

by UAE nationals). In this summary, we refer to such equity

owners as "partners", but parties commonly use "shareholder"

and "partner" interchangeably. The minimum capitalization

required by the Companies Law for a limited liability company

(e.g., Dhs. 150,000) was abolished in June 2009 pursuant to Fed-

eral Law No. 1 of 2009 on Amending Certain Provisions of Fed-

eral Law No. 8 of 1984 Concerning Commercial Companies. The

current requirement is to have sufficient capital for the busi-

ness, which is to be determined by the partners. However, in

practice, the authorities have discretion to impose their own

requirements (e.g., Dhs. 300,000 in Dubai, and also minimum

capitalization requirements for certain types of activities, such

as industrial and manufacturing operations). As a practical mat-

ter most businesses require a certain amount of capital to oper-

ate, often greater than Dhs. 150,000. Also, there is risk that

having no minimum amount of capital could potentially expose

partners to greater personal liability due to insufficiently capital-

izing the business. In any event, it will take time to assess the

practical impact of eliminating the minimum capitalization re-

quirement for an LLC.

Recent press reports indicate that the UAE Council of Ministers

has approved a new Companies Law that will relax existing for-

eign ownership restrictions (e.g., permit more than 49% foreign

ownership in an LLC), at least for certain sectors, and impose

minimum corporate governance standards. However, as of

early 2012 the new law has not been published in the official

gazette.

Pursuant to the Companies Law, LLCs may be licensed to engage

in a wide range of commercial activities, except for banking, in-

surance and the investment of money for third parties. For ex-

ample, an LLC may engage in trading. An LLC usually is the pre-

ferred vehicle for a joint venture between a foreign party and a

UAE party.

The creation, capitalization, and governance of an LLC is gov-

erned by the Companies Law and by its charter document (e.g.,

Articles or Memorandum of Association), an Arabic language

contract among the LLC partners that is registered with the local

authorities. This charter document usually is supplemented by

other agreements, such as joint venture agreements. The Com-

panies Law gives the partners a great degree of latitude to nego-

tiate the terms for governance of their LLC. But, in the event of

a conflict between any such supplemental agreements and ei-

ther the registered charter document or the Companies Law,

the latter likely will control.

Parties have implemented a variety of measures (some lawful

and some not) trying to ameliorate the limitations on foreign

ownership of LLCs imposed by the Companies Law. Although

the Companies Law requires at least 51% of the capital of an LLC

to be owned by UAE nationals, it also permits profits and losses

to be split by the LLC partners as they may agree. The various

Emirate licensing authorities impose restrictions in practice, of-

ten limiting to 80% the profits allocable to the foreign partners.

Some foreign parties have tried to engage UAE nationals to par-

ticipate in LLCs as mere "sponsors" or "nominees" (often re-

ferred to colloquially as "silent" or "sleeping" partners) solely for

the sake of appearing to satisfy the UAE national ownership re-

quirements imposed by the Companies Law. Such arrange-

ments typically commit the UAE national to relinquish all profits,

voting rights and other rights of ownership to the foreign party,

often by a "side agreement" not reflected in the registered char-

tered document. Such arrangements are not legal under the

Companies Law, and are criminal violations under Federal Law

No. 17 of 2004 on Combating of Commercial Concealment

(the "Commercial Concealment Law"), which proscribes such

arrangements and imposes stringent penalties on the UAE na-

tional "concealing party" as well as the foreign "concealed

party". Enforcement of the Commercial Concealment Law,

which originally was to be effective in November 2007, was de-

ferred until December 31, 2009 by UAE Cabinet Resolution No.

229/12 of 2007. We are not aware of any subsequent law or

resolution deferring the implementation of the Commercial Con-

cealment Law or issuance of any implementing regulations.

Thus, it would be advisable to assume that the Commercial Con-

cealment Law took effect as of January 1, 2010, although there

have not been reports of active public enforcement of that law.

Even if the authorities choose not to prosecute violators, foreign

parties need to understand that reliance on the types of ar-

rangements described above may be misplaced due to serious

questions about their enforceability and the potential account-

ing and disclosure complications related to securities matters for

the foreign partner and merger and acquisition activity relating

to the LLC.

IV. OPERATION IN A UAE "FREE ZONE"

UAE free zones present a means to conduct business within the

territory of the UAE, but not within its import and customs

boundaries. Such free zones tend to be more "user-friendly"

and conducive to foreign investment than in the UAE proper.

For example, the relevant documents to establish and conduct

business in a free zone are in English. Early free zones included

the Jebel Ali Free Zone ("JAFZ"), which is a seaport and industrial

facility, and the Dubai Airport Free Zone ("DAFZ") at the Dubai

airport. UAE free zones account for a significant portion of for-

eign commercial activity in the UAE. These free zones have

been instrumental in positioning the UAE as the commercial hub

of the Arabian Gulf and as a leading international trans-

shipment center.

Each free zone has its own special purpose business regulatory

schemes, but the rules and practices for business activities are

quite similar from zone to zone. Among the investment incen-

tives generally available in the free zones are 100% foreign own-

ership, guaranteed income tax holidays and no restrictions on

repatriation of capital and profits. Moreover, as the names im-

ply, there generally are no customs or other import duties or

taxes with respect to imports into or exports out of the various

free zones, provided that goods are not then imported into the

UAE proper.

Free zones generally permit: (i) the registration of wholly-

owned branch offices of foreign companies; or (ii) the incorpora-

tion of single or multiple shareholder corporate entities with

100% foreign ownership. The types of activities usually permit-

ted in the various free zones are trading, industrial, and service

activities, although there are some exceptions.

Some free zones follow the economic cluster model focusing on

particular types of industries or services, such as: (i) Dubai Tech-

nology and Media Free Zone ("TECOM," which includes Dubai

Internet City, Dubai Media City, Dubai Knowledge Village, Dubai

International Academic City, Dubai Healthcare City and others);

(ii) Dubai International Financial Centre ("DIFC"); (iii) Dubai Multi

Commodities Centre and Jumeirah Lakes Towers; and (iv) Dubai

Silicon Oasis. It is important to note that free zone registrants

may not engage in business in the UAE proper absent independ-

ent licensing or some other legal arrangement permitting the

specific business activities outside the free zone. However, em-

ployees working for a free zone branch or company may live

anywhere in the UAE.

Other Emirates also have established free zones. Sharjah has a

seaport free zone (Hamriyah Free Zone) and an airport free zone

(Sharjah Airport International Free Zone). Ras Al Khaimah, Fu-

jairah, Ajman and Umm Al Quwain also have free zones. Abu

Dhabi has only recently begun to establish free zones. Abu

Dhabi has a media free zone called Twofour54, Masdar City,

which is intended to become a leading global centre for renew-

able energy research, development, implementation and invest-

ment, and Abu Dhabi Airports Company Skycity which operates

Abu Dhabi Airport Free Zones at the three main airports in Abu

Dhabi. In addition, Abu Dhabi has set up ZonesCorp to establish,

manage and operate specialized economic zones within Abu

Dhabi.

There is a wealth of information available on the Internet about

the various free zones in the UAE.

V. OTHER KEY CONSIDERATIONS

A. Monetary Policies

There are currently no foreign exchange control laws or other

legal restrictions on the repatriation of capital and earnings.

Currently, the UAE Dirham is pegged to the US Dollar and the

exchange rate has been approximately US $1 = UAE Dirhams

3.67 for many years.

The UAE Central Bank has adopted money laundering regula-

tions that impose certain restrictions, including reporting obliga-

tions on certain cash transactions. In addition, the Dubai Finan-

cial Services Authority acts as an independent regulator for cer-

tain entities that are registered in the DIFC.

B. Taxes

There are no special purpose income tax laws or regulations,

corporate or individual, issued at the UAE federal level. At the

local Emirate level, most of the Emirates have issued corporate

income tax decrees in some form. However, to date such tax

decrees have not been enforced and income taxes generally

have not been imposed by any of the Emirates except with re-

spect to: (i) certain companies engaged in the production of oil,

gas and/or petrochemicals; and (ii) foreign bank branches. Also,

currently there are no personal income tax laws enacted in any

of the Emirates.

There are also no withholding taxes, no payroll taxes, and no

value-added taxes or sales taxes, except with respect to certain

items such as alcohol and tobacco. But government authorities

may be seeking additional sources of revenue. As described in

Section V(F) below under Labor and Employment, the govern-

ment is now collecting payroll data that would enable it to im-

plement a payroll tax. Also, it has been rumored that a VAT will

be implemented in the future, but no developments in this re-

gard have occurred as of early 2012. There are taxes on items

such as services at hotels, as well as residential and commercial

premises leases (e.g., annual fees collected based on the value

of a lease).

Persons subject to tax in other jurisdictions, such as persons

subject to US tax on worldwide income, should consult their tax

advisors regarding the application of such taxes to their activi-

ties in the UAE. The UAE has entered into tax treaties with a

number of countries.

C. Intellectual Property

There are three primary federal laws related to the protection of

intellectual property rights in the UAE, namely: (i) the UAE Trade-

mark Law, Federal Law No. 8 of 2002, which amended Federal Law

No. 37 of 1992; (ii) the UAE Copyright Law, Federal Law No. 7 of

2002; and (iii) the UAE Patent Law, Federal Law No. 17 of 2002.

These primary intellectual property laws are supplemented by other

legislation, including Federal Law No. 4 of 1979 Regarding the Pre-

vention of Fraud and Deception in Commercial Transactions, the

Commercial Code, and various ministerial resolutions. In addition,

it is important to note that the UAE is a member of many interna-

tional treaties, including treaties related to intellectual property

such as the Berne Convention. Also of interest, the UAE has a fed-

eral consumer protection law, Federal Law No. 24 of 2006 Concern-

ing the Protection of Consumers. Various e-commerce related laws

have also been implemented at the federal level as well as within

several individual Emirates.

D. Real Estate

As is the case in many Middle East countries, real property is

afforded special "guarded" status in the UAE. Although the UAE

Constitution vests legislative authority over real estate owner-

ship with the UAE federal government, to date no UAE federal

real estate law has been passed. Federal Law No. 5 of 1985 Re-

garding the Civil Transactions Law (the "Civil Code") includes

provisions relating to real estate, but not with respect to fee

ownership. Thus, land ownership restrictions in the UAE are

generally established by rules and practices on an Emirate-by-

Emirate basis. In particular, each Emirate maintains its own poli-

cies and practices with respect to land ownership by non-UAE

nationals. In this regard, there have been significant legislative

and practice developments in nearly all of the Emirates. These

developments are expected to continue for real estate matters

throughout the UAE. The following provides only a brief over-

view of the landscape in Dubai and Abu Dhabi.

Look for the complete article in the 2012 ABC Membership

Directory, with topics including:

Dubai Freehold Property

Abu Dhabi Freehold Property

General Freehold Property Issues

Tenancy Issues

Financial Records and Accounting

Labor and Employment

Immigration

US and Other Regulatory Issues

Export Controls and Sanctions

Anti-Corruption

US Anti-boycott Regulations

Reporting Financial Accounts

Dispute Resolution

Choice of Foreign Law and Venue

Enforcement of Foreign Court Judgments

Enforcement Of Domestic And Foreign Arbitra-

tion Awards

DIFC Courts Expanded Jurisdiction

Personal Conduct

Doing Business in the U.A.E. excerpt from the 2012 ABC membership Directory

IV. OPERATION IN A UAE "FREE ZONE"

UAE free zones present a means to conduct business within the

territory of the UAE, but not within its import and customs

boundaries. Such free zones tend to be more "user-friendly"

and conducive to foreign investment than in the UAE proper.

For example, the relevant documents to establish and conduct

business in a free zone are in English. Early free zones included

the Jebel Ali Free Zone ("JAFZ"), which is a seaport and industrial

facility, and the Dubai Airport Free Zone ("DAFZ") at the Dubai

airport. UAE free zones account for a significant portion of for-

eign commercial activity in the UAE. These free zones have

been instrumental in positioning the UAE as the commercial hub

of the Arabian Gulf and as a leading international trans-

shipment center.

Each free zone has its own special purpose business regulatory

schemes, but the rules and practices for business activities are

quite similar from zone to zone. Among the investment incen-

tives generally available in the free zones are 100% foreign own-

ership, guaranteed income tax holidays and no restrictions on

repatriation of capital and profits. Moreover, as the names im-

ply, there generally are no customs or other import duties or

taxes with respect to imports into or exports out of the various

free zones, provided that goods are not then imported into the

UAE proper.

Free zones generally permit: (i) the registration of wholly-

owned branch offices of foreign companies; or (ii) the incorpora-

tion of single or multiple shareholder corporate entities with

100% foreign ownership. The types of activities usually permit-

ted in the various free zones are trading, industrial, and service

activities, although there are some exceptions.

Some free zones follow the economic cluster model focusing on

particular types of industries or services, such as: (i) Dubai Tech-

nology and Media Free Zone ("TECOM," which includes Dubai

Internet City, Dubai Media City, Dubai Knowledge Village, Dubai

International Academic City, Dubai Healthcare City and others);

(ii) Dubai International Financial Centre ("DIFC"); (iii) Dubai Multi

Commodities Centre and Jumeirah Lakes Towers; and (iv) Dubai

Silicon Oasis. It is important to note that free zone registrants

may not engage in business in the UAE proper absent independ-

ent licensing or some other legal arrangement permitting the

specific business activities outside the free zone. However, em-

ployees working for a free zone branch or company may live

anywhere in the UAE.

Other Emirates also have established free zones. Sharjah has a

seaport free zone (Hamriyah Free Zone) and an airport free zone

(Sharjah Airport International Free Zone). Ras Al Khaimah, Fu-

jairah, Ajman and Umm Al Quwain also have free zones. Abu

Dhabi has only recently begun to establish free zones. Abu

Dhabi has a media free zone called Twofour54, Masdar City,

which is intended to become a leading global centre for renew-

able energy research, development, implementation and invest-

ment, and Abu Dhabi Airports Company Skycity which operates

Abu Dhabi Airport Free Zones at the three main airports in Abu

Dhabi. In addition, Abu Dhabi has set up ZonesCorp to establish,

manage and operate specialized economic zones within Abu

Dhabi.

There is a wealth of information available on the Internet about

the various free zones in the UAE.

V. OTHER KEY CONSIDERATIONS

A. Monetary Policies

There are currently no foreign exchange control laws or other

legal restrictions on the repatriation of capital and earnings.

Currently, the UAE Dirham is pegged to the US Dollar and the

exchange rate has been approximately US $1 = UAE Dirhams

3.67 for many years.

The UAE Central Bank has adopted money laundering regula-

tions that impose certain restrictions, including reporting obliga-

tions on certain cash transactions. In addition, the Dubai Finan-

cial Services Authority acts as an independent regulator for cer-

tain entities that are registered in the DIFC.

B. Taxes

There are no special purpose income tax laws or regulations,

corporate or individual, issued at the UAE federal level. At the

local Emirate level, most of the Emirates have issued corporate

income tax decrees in some form. However, to date such tax

decrees have not been enforced and income taxes generally

have not been imposed by any of the Emirates except with re-

spect to: (i) certain companies engaged in the production of oil,

gas and/or petrochemicals; and (ii) foreign bank branches. Also,

currently there are no personal income tax laws enacted in any

of the Emirates.

There are also no withholding taxes, no payroll taxes, and no

value-added taxes or sales taxes, except with respect to certain

items such as alcohol and tobacco. But government authorities

may be seeking additional sources of revenue. As described in

Section V(F) below under Labor and Employment, the govern-

ment is now collecting payroll data that would enable it to im-

plement a payroll tax. Also, it has been rumored that a VAT will

be implemented in the future, but no developments in this re-

gard have occurred as of early 2012. There are taxes on items

such as services at hotels, as well as residential and commercial

premises leases (e.g., annual fees collected based on the value

of a lease).

Persons subject to tax in other jurisdictions, such as persons

subject to US tax on worldwide income, should consult their tax

advisors regarding the application of such taxes to their activi-

ties in the UAE. The UAE has entered into tax treaties with a

number of countries.

C. Intellectual Property

There are three primary federal laws related to the protection of

intellectual property rights in the UAE, namely: (i) the UAE Trade-

mark Law, Federal Law No. 8 of 2002, which amended Federal Law

No. 37 of 1992; (ii) the UAE Copyright Law, Federal Law No. 7 of

2002; and (iii) the UAE Patent Law, Federal Law No. 17 of 2002.

These primary intellectual property laws are supplemented by other

legislation, including Federal Law No. 4 of 1979 Regarding the Pre-

vention of Fraud and Deception in Commercial Transactions, the

Commercial Code, and various ministerial resolutions. In addition,

it is important to note that the UAE is a member of many interna-

tional treaties, including treaties related to intellectual property

such as the Berne Convention. Also of interest, the UAE has a fed-

eral consumer protection law, Federal Law No. 24 of 2006 Concern-

ing the Protection of Consumers. Various e-commerce related laws

have also been implemented at the federal level as well as within

several individual Emirates.

D. Real Estate

As is the case in many Middle East countries, real property is

afforded special "guarded" status in the UAE. Although the UAE

Constitution vests legislative authority over real estate owner-

ship with the UAE federal government, to date no UAE federal

real estate law has been passed. Federal Law No. 5 of 1985 Re-

garding the Civil Transactions Law (the "Civil Code") includes

provisions relating to real estate, but not with respect to fee

ownership. Thus, land ownership restrictions in the UAE are

generally established by rules and practices on an Emirate-by-

Emirate basis. In particular, each Emirate maintains its own poli-

cies and practices with respect to land ownership by non-UAE

nationals. In this regard, there have been significant legislative

and practice developments in nearly all of the Emirates. These

developments are expected to continue for real estate matters

throughout the UAE. The following provides only a brief over-

view of the landscape in Dubai and Abu Dhabi.

Look for the complete article in the 2012 ABC Membership

Directory, with topics including:

Dubai Freehold Property

Abu Dhabi Freehold Property

General Freehold Property Issues

Tenancy Issues

Financial Records and Accounting

Labor and Employment

Immigration

US and Other Regulatory Issues

Export Controls and Sanctions

Anti-Corruption

US Anti-boycott Regulations

Reporting Financial Accounts

Dispute Resolution

Choice of Foreign Law and Venue

Enforcement of Foreign Court Judgments

Enforcement Of Domestic And Foreign Arbitra-

tion Awards

DIFC Courts Expanded Jurisdiction

Personal Conduct

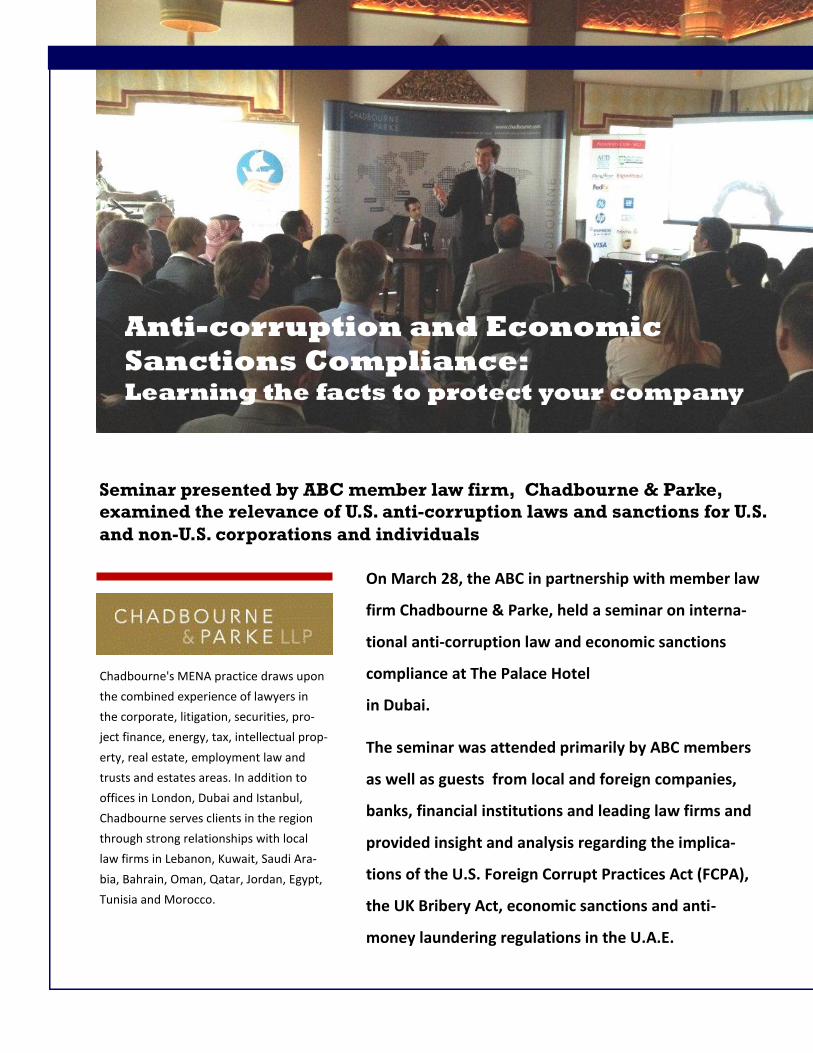

On March 28, the ABC in partnership with member law

firm Chadbourne & Parke, held a seminar on interna-

tional anti-corruption law and economic sanctions

compliance at The Palace Hotel

in Dubai.

The seminar was attended primarily by ABC members

as well as guests from local and foreign companies,

banks, financial institutions and leading law firms and

provided insight and analysis regarding the implica-

tions of the U.S. Foreign Corrupt Practices Act (FCPA),

the UK Bribery Act, economic sanctions and anti-

money laundering regulations in the U.A.E.

Anti-corruption and Economic

Sanctions Compliance: Learning the facts to protect your company

Chadbourne's MENA practice draws upon

the combined experience of lawyers in

the corporate, litigation, securities, pro-

ject finance, energy, tax, intellectual prop-

erty, real estate, employment law and

trusts and estates areas. In addition to

offices in London, Dubai and Istanbul,

Chadbourne serves clients in the region

through strong relationships with local

law firms in Lebanon, Kuwait, Saudi Ara-

bia, Bahrain, Oman, Qatar, Jordan, Egypt,

Tunisia and Morocco.

Seminar presented by ABC member law firm, Chadbourne & Parke,

examined the relevance of U.S. anti-corruption laws and sanctions for U.S.

and non-U.S. corporations and individuals

The seminar is one of a series on anti-corruption and economic sanctions presented in Istanbul and

Beirut by Chadbourne’s Dubai associate Ramsey Jurdi (and ABC board member) and Scott Peeler,

Chadbourne New York partner in response to the fast expanding needs of corporations in the region.

"Exciting developments are taking place in the U.A.E. and the Middle East," said Chadbourne partner

Scott Peeler. "In particular, foreign companies doing business in the Middle East are facing tougher

scrutiny and penalties than ever before. Companies and their employees and managers need to fully

appreciate the risk of non-compliance, and must implement the strictest anti-corruption controls

where they are needed."

"Anti-corruption laws and economic sanctions are important topics in the region," added Jack

Greenwald, head of Chadbourne's Dubai office. "The seminar in Dubai provided the members of the

ABC the opportunity to obtain important information and to benefit from Chadbourne's experience

and expertise in these fields."

Anti-corruption and Economic

Sanctions Compliance: Learning the facts to protect your company

Speakers, Scott Peeler, left photo, and Ramsey Jurdi, right

photo, give the facts on anti-corruption and sanctions com-

pliance.

MEMBERS’ CALENDAR

Don’t miss a great day of golf

on Dubai’s premiere course

Dubai Creek Golf & Yacht Club

April 21 The 21st Annual ABC Golf Tournament

Driven by

For details and to reserve your place go to our online calendar at

www.abcdubai.com

ABC is on the move!

Watch for exact details of the transition in the coming

weeks, but our offices will be moving to

The Emarat Atrium Building Sheikh Zayed Road

MEMBERS’ CALENDAR

SAVE THE DATE

The ABC Business Forum

May 8, 2012

Join us as we investigate the following business sectors with a view to

producing relevant white paper on ways to increase

opportunities for American Business.

* Healthcare & Insurance * Banking & Finance * Hospitality, Travel, & Tourism * Real Estate

Transportation *Education * Engineering, Construction, & Project Management * Legal Affairs

* Energy * Technology

MEMBERS’ NEWS

Tom Friedman and The Middle East’s Role on the New Silk Road

IHT Global Conversation: Dubai

May 2nd, 2012

Armani Hotel

To celebrate its 125th Anniversary, the International Herald Tribune is convening “The

Global Conversation,” a series of events bringing together high profile speakers and

IHT journalists for an evening of dinner and thought-provoking debate. Join us in Du-

bai, and hear The New York Times’ Foreign Affairs Correspondent Thomas Friedman

discuss whether the Middle East can focus on new economic opportunities through

this period of regional political upheaval, while patterns of global trade and capital

flows are changing dramatically.

Special discount for members code GCDAB

Visit

https://www.eiseverywhere.com/39008?discountcode=GCDAB

for more information or to register.