2011annual report - asx2011/10/31 · annual report for the year ended 30 june 2011 3 chairman’s...

TRANSCRIPT

AFRICAN IRON LTD

2011ANNUAL REPORTFOR THE YEAR ENDED 30 JUNE

For

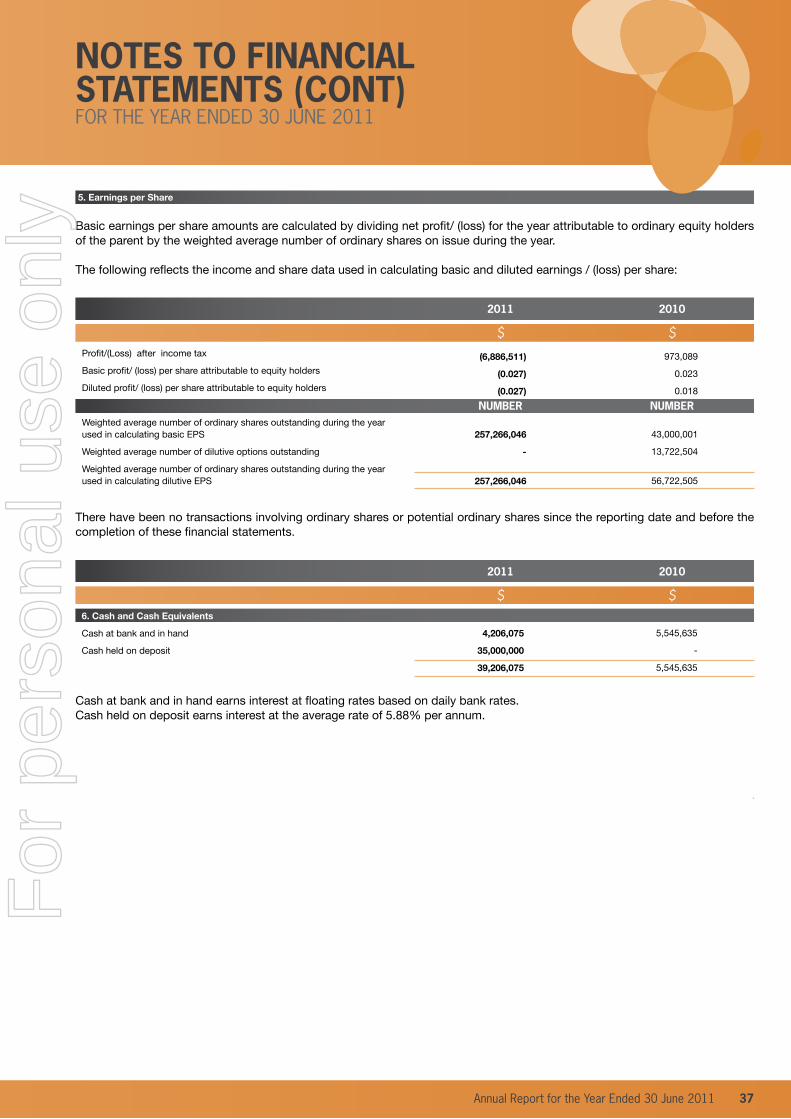

per

sona

l use

onl

y

Corporate DireCtory

Chairman’s letter

operations reVieW

DireCtors’ report

auDitor’s inDepenDenCe DeClaration

ConsoliDateD statement of ComprehensiVe inCome

ConsoliDateD statement of finanCial position

ConsoliDateD statement of Cash floWs

ConsoliDateD statement of Changes in equity

notes to the finanCial statements

DireCtors’ DeClaration

inDepenDent auDitor’s report

Corporate goVernanCe statement

asX aDDitional information

2

3

4

7

17

18

19

20

21

22

54

55

57

64

African Iron Limited(formerly Stirling Minerals Limited)

ABN 24 123 972 814

Annual ReportFor The Year Ended

30 June 2011

CONTENTS

Annual Report for the Year Ended 30 June 2011 1

AFRICAN IRON LTDF

or p

erso

nal u

se o

nly

REGISTERED OFFICEDIRECTORS

non eXeCutiVe Chairman Dr Ian Burston

non eXeCutiVe DireCtorMr Antony Sage

non eXeCutiVe DireCtorMr Joe Ariti

non eXeCutiVe DireCtor The Hon. John Moore AO

AUDITORS

Bentleys

Level 1, 12 Kings Park Road, West Perth, WA 6005

SOLICITORS

steinepreis paganin

Level 4, 16 Milligan Street, Perth WA 6000

WEbSITE

www.africanironlimited.com

COmpANy SECRETARy

Ms Claire Tolcon

bANKERS

hsBC Bank australia limiteD88 - 190 St Georges Terrace, Perth, WA 6000

ShARE REGISRTy

Computershare inVestor serViCes pty limiteD

GPO Box 2975

Melbourne, VIC 3001

T: 1300 85 05 05 (Aus)

T: +61 3 9415 4000 (Overseas)

STOCK ExChANGE

australian seCurities eXChange limiteD

Exchange Plaza

2 The Esplanade, Perth WA 6000

asX Code

AKI - Fully paid ordinary shares AKIO - Listed options

Level 1, 2 Ord Street, West Perth WA 6005

2 African Iron Limited and its controlled entities

AFRICAN IRON LTDCORpORATE DIRECTORyF

or p

erso

nal u

se o

nly

Dear Shareholders,

It is with great pleasure that I write to you as Chairman of our Company, African Iron Limited (“African Iron”), which in the past ten months, since relisting on ASX, has rapidly advanced the Mayoko Iron Ore Project in the Republic of Congo, West Africa (“Mayoko”).

In my view the story of African Iron can be succinctly summed up in three simple, yet important, phrases; quality partnerships, quality project and quality people.

Firstly, let me talk to you about quality partnerships. Our Company is firmly committed to building and maintaining proactive relationships with the key communities in which it operates, from the Ministerial, local government and infrastructure representatives in the capital Brazzaville, to the various communities that are in the immediate vicinity of our key project, Mayoko. These relationships are very important to everyone involved in the Company and pleasingly for all involved centre on a willingness of all parties working together to ensure the successful delivery of a project that benefits all key stakeholders.

As a Company, we also work hard building and maintaining other important partnerships, from our committed drilling contractors and other key technical advisors, who will play a major role in the success of Mayoko’s development, to our investors spread throughout the world who without their support we would not be a Company at all.

Partners are vital to our success and we will continually recognise and promote these wherever possible.

Secondly, I would like to convey to you the quality of Mayoko. I recognise it is hard as an investor to truly understand this project, given you are unable to “walk the ground and kick the rocks”, in essence you put your trust in the board and management to ensure your interests are protected and enhanced.

Mayoko , in which we recently lifted our holding from 80% to 92%, represents a near term direct shipping ore (“DSO”) development opportunity in the emerging iron ore province of West Africa. It is steadily being developed into a world class asset.

Mayoko has excellent infrastructure access with an underutilised, heavy haulage railway, in which African Iron has secured access, passing within 2km of the main prospect at Mt Lekoumou and terminating at the port of Pointe-Noire on the Atlantic coast. The Company’s objective is to develop an initial 5Mtpa DSO mining operation at Mayoko by mid-2013 leveraging off the project’s proximity to existing rail and port infrastructure.

Lastly, the other key aspect of your Company has been the attraction and retention of quality people to its operational and executive ranks.

We have spent considerable time as a Company ensuring we have the right people in place (both technically and corporately) to ensure our project is successfully developed in a timely fashion. Two of the most significant appointments the board has made in recent times have been that of the appointment of the Hon. John Moore AO to the board of directors, as an independent Non-Executive Director and Simon Youds as Chief Executive Officer.

The appointment of Mr Moore to the board of directors strengthened the independence of the board whilst providing additional capital markets and commercial skill sets.

Simon brings a wealth of general management and technical capabilities to the Company, having most recently worked as Managing Director Australia of unlisted manganese and chromite producer, Consolidated Minerals Limited. He has extensive experience in Africa and is someone with a strong track record of taking projects from development and into production. The board is pleased to have Simon as CEO and we believe, together with the other senior members of the executive, he will play a pivotal role in ensuring Mayoko enters production in 2013 as planned.

As your Chairman, I am supremely confident the quality partnerships we have built and will continue to maintain, together with the world-class team we are assembling, will ensure our Mayoko project continues to advance towards production.

In my view we have all the necessary ingredients to ensure success and I thank you for your support and look forward to updating you on our success over the coming 18 months.

Yours faithfully

Ian Burston Chairman

Annual Report for the Year Ended 30 June 2011 3

AFRICAN IRON LTDChAIRmAN’S LETTERF

or p

erso

nal u

se o

nly

hIGhLIGhTS• Acquired an additional 12% equity in the Mayoko iron ore project increasing the Company’s ownership to 92%;

• Commenced a 30,000 metre resource definition drilling program, and announced the first two batches of assay results;

• Renewed the Mayoko exploration licence (Mayoko-Lekoumou Exploration Permit) for a further two (2) years until April 2013;

• Completed an air borne geophysical survey over the remaining 780km2 of the Mayoko exploration licence, which resulted

in an 80% increase in the exploration target size to 1.6-2.6 billion tonnes at 30-65% Fe1;

• Commenced various infrastructure studies around developing a transport solution for the export of iron ore from the Mayoko project;

• Engaged with Chemin de Fer Congo Ocean (rail operator) and the Ministry of Transport around progressing the Company’s rail access and cooperation Memorandum of Understanding toward a formal rail access agreement to enable the transport of 5 million tonnes per annum of iron ore;

• Expanded the Company’s landholding by 94% to 1,944km2 with the addition of the 944km2 Ngoubou-Ngoubou Authority to Prospect; and

• Appointment of capable and competent in-country executive management, and the establishment of office, communications and other support infrastructure.

The past 10 months since the Company’s re-positioning as an iron ore development company and re-listing on the ASX in mid-January 2011, has seen significant progress made toward building a 5 million tonne per annum iron ore business based on developing its 92% owned Mayoko direct shipping iron ore project, located in the Republic of Congo (“RoC”), central West Africa (“Mayoko” or “Mayoko Project”).

At a strategic level, the Company was able to successfully increase its ownership of the Mayoko Project from 80 to 92%. This was considered important to achieve as early as possible to ensure the Company did not pay at a later date for the value it is creating through sole funding, and execution, of exploration and evaluation activities.

The key to developing our iron ore business is the definition of a larger JORC compliant iron ore mineral resource at the Mayoko Project. The project has an existing JORC compliant Inferred Mineral Resource of 33 million tonnes at 56% Fe of supergene direct shipping hematite based on shallow drilling completed in 1974-1975 by earlier explorers.

To enable the definition of a larger JORC complaint resource to underwrite an iron ore business, the Company has committed significant financial resources to a 30,000 metre resource definition program (“Resource Definition Program”). The Resource Definition Program commenced within six weeks of the Company re-listing on ASX. This was made possible through an arrangement with one of the Company’s drilling contractors, Partners Drilling International, whereby three drill rigs had been retained at Mayoko following the completion of the 2010 drilling program. The Company subsequently engaged a second drilling contractor increasing the at-project rig fleet to 5, with the objective of accelerating the Resource Definition Program.

The first two batches of drill assay results were subsequently announced in August and October 2011 respectively, and confirmed the average thickness (25-30 metres) and grade (55-58% Fe) of the overlying DSO, and average thickness (40-50 metres) and grade (40-45% Fe) of the underlying beneficiable DSO (“bDSO”). bDSO will require an additional mineral processing step to DSO crushing and screening, most likely dense media separation, to produce a marketable fines product.

Drill samples are assayed at the internationally accredited Ultra Trace laboratory located in Perth, Western Australia to ensure the highest possible standards of assay quality control are achieved. Batches of drill samples are regularly shipped from RoC to Perth and now that the logistics chain is full, shareholders can expect the regular release by the Company of assay results from the Definition Drilling Program.

1. The estimate of exploration target size should not be misunderstood or misconstrued as estimates of Mineral Resources. The estimates of exploration target size

is conceptual in nature and there has been insufficient results received from drilling completed to date to estimate a Mineral Resource in accordance with the

JORC Code (2004) guidelines. Furthermore, it is uncertain if further exploration will result in the determination of a Mineral Resource.

OpERATIONS REVIEW

4 African Iron Limited and its controlled entities

AFRICAN IRON LTD

For

per

sona

l use

onl

y

The Company has retained independent, global mining group Golder Associates to prepare its first JORC resource update. The resource update will build on the existing DSO resource by incorporating diamond drilling completed in 2010 and Resource Definition Program drill results received up to 30 September 2011. The resource update will also have a maiden JORC resource for part of the underlying bDSO. The resource update is expected to be released at the end of October 2011. Additional JORC resource updates will be completed at 3-6 monthly intervals as drill data permits.

During the period in review, the Company has also been able to successfully renew the Mayoko-Lekoumou Exploration Permit (which hosts the Mayoko Project) (“Mayoko Licence”) for an additional 2 years. The Mayoko Licence was originally granted in April 2008 for an initial period of 3 years, and may be renewed for two subsequent periods of 2 years each with up to a 50% reduction in land area required at each renewal. The first renewal was completed with an exemption from reducing the land area, reflecting the government of the RoC’s support for the Company’s progress on exploration and evaluation of Mayoko.

In June, the Company completed an airborne geophysical survey over the remaining 78% (780km2) of the Mayoko Licence, which had not been covered in the earlier 2009 survey. The survey identified a number of new magnetic targets that are prospective for hematite (both DSO and bDSO) and magnetite iron mineralisation. Consequently, an independent geophysical consultant modeled the new targets and the Company was able to increase its exploration target size by 80% to 1.6-2.6 billion tonnes at 30-65% Fe2. Importantly, the Company is now in the process of engaging additional exploration personnel to commence a regional exploration program with the objective of assessing the new exploration targets.

Contemporaneously with the commencement of the Resource Definition Program, the Company engaged global, infrastructure group Egis International to complete an assessment of the proposed transport solution for exporting iron ore from Mayoko (“Egis Study”). The transport solution proposed by the Company is to utilise the government of RoC owned, existing, underutilized purpose built heavy haulage railway that passes within 2km of Mayoko and to export iron ore from Pointe Indenne where the government has allocated land for a minerals port development, approximately 16km to the north of the port of Pointe Noire.

The Egis Study concluded the rail could transport 10 million tonnes per annum of iron ore in its current configuration with the opening of a number of closed stations to act as passing loops and with limited capital investment to install modern signals and telecommunications to manage the increased number of train sets proposed to operate on the line. At Pointe Indenne, the Company is proposing to construct an approximate 23km spur line branching off the existing rail network. At the port, Egis evaluated a barging solution rather than capital intensive fixed infrastructure whereby barges loaded with iron ore shuttle to and from a Panamax vessel (65-80,000 tonnes DWT). At Pointe Indenne, the Company has secured a land allocation to enable the unloading of train sets, stockpiling of iron ore and loading of barges. The Egis Study has confirmed the Company has a technically feasible transport solution, which will be further detailed and costed in 2012.

Following the completion of the Egis Study, the Company has engaged with Chemin de Fer Congo Ocean (rail operator) (“CFCO”) and the Ministry of Transport around progressing the Company’s rail access and cooperation Memorandum of Understanding toward a formal rail access agreement to enable the transport of a minimum 5 million tonnes per annum of iron ore. These discussions, and ongoing collaboration with CFCO and the Ministry of Transport, will continue throughout 2012.

2. The estimate of exploration target size should not be misunderstood or misconstrued as estimates of Mineral Resources. The estimates of exploration target size

is conceptual in nature and there has been insufficient results received from drilling completed to date to estimate a Mineral Resource in accordance with the

JORC Code (2004) guidelines. Furthermore, it is uncertain if further exploration will result in the determination of a Mineral Resource.

OpERATIONS REVIEW

Annual Report for the Year Ended 30 June 2011 5

AFRICAN IRON LTDF

or p

erso

nal u

se o

nly

In addition to the key focus of evaluating Mayoko for development, the Company has also been mindful to increase its landholding in RoC to leverage off its in-country management, know how and support infrastructure. To that end, the Company applied for and was granted an 85% interest in an Authority to Prospect over a 944km2 land package know as Ngoubou-Ngoubou, which is to the north of, and contiguous with, the Mayoko Licence. Prospect level exploration over Ngoubou-Ngoubou has identified artisanal blacksmith workings, which support the Company’s hypothesis that this land package is prospective for DSO iron ore. Following the completion of this prospect level exploration, the Company has commenced converting the Authority to Prospect to an exclusive Exploration Licence, and has commissioned an airborne magnetic survey over the whole area to define the extent of iron occurrences.

The outlook for 2012 is extremely positive for the Company as the iron ore market is forecast to remain buoyant and management continues to advance Mayoko toward a decision to mine through the delivery of a definitive feasibility study and engagement with government for the grant of an Exploitation Licence and attaching Mining Convention.

In closing, it is important to note that none of the above would have been possible without the dedicated and competent personnel that the Company has working for it in RoC. It is through their efforts that we have been able to achieve so much in such a short period of time. The board of directors extends its thanks to its RoC based personnel for their extraordinary efforts throughout 2011.

Competent Person Statement

The information in this Operations Review that relates to Exploration Results and Mineral Resources is based on information reviewed and compiled by Mr. Patrick Vekemans, who is a Member of the Australian Institute of Geosciences. Mr. Vekemans is a contractor to African Iron Limited and has sufficient experience which is relevant to the style of mineralisation and the type of deposit under consideration and to the activity which he is undertaking to qualify as a Competent Person as defined in the 2004 edition of the Australasian Code for Reporting of Exploration Results, Minerals Resources and Ore Reserves. Mr. Vekemans consents to the inclusion in this Operations Review of this information in the form and context in which it appears.

OpERATIONS REVIEW (CONT)

6 African Iron Limited and its controlled entities

AFRICAN IRON LTD

For

per

sona

l use

onl

y

Your Directors present their report on African Iron Limited (“African Iron” or the “Company”) and its controlled entities (the “Group”) for the financial year ended 30 June 2011.

DIRECTORSThe names of the Directors in office during the financial year and as at date of this report are as follows. All Directors were in office for the entire period unless stated otherwise:

COmpANy SECRETARyOn 10 January 2011, Ms Claire Tolcon was appointed as Company Secretary to replace Ms Rebecca Sandford who resigned on that date.

pRINCIpAL ACTIVITIESThe principal activity of the Group for the financial year ended 30 June 2011 was mineral exploration.

SIGNIFICANT ChANGES IN STATE OF AFFAIRSOn 5 November 2010, the Company entered into an agreement to acquire DMC Mining Ltd (“DMC Mining”) from Cape Lambert Resources Limited (“Cape Lambert”) (ASX: CFE). At that point in time, DMC Mining owned 80% of the Mayoko Iron Ore Project located in the Republic of Congo, West Africa (“Mayoko”).

On 17 December 2010, a prospectus to raise $96 million through the issue of 320 million shares at an issue price of $0.30 per share to fund the acquisition of DMC Mining and to fast-track exploration and feasibility at Mayoko was lodged with ASIC.

On 20 December 2010, the Company’s shareholders approved the acquisition of DMC Mining for $47 million in cash and 120 million fully paid ordinary shares in the Company, and the issue of 320 million shares pursuant to the prospectus.

On 7 January 2011, the Company successfully completed the capital raising under the prospectus and acquisition of 100% of DMC Mining settled on 10 January 2011.

On 10 January 2011, the Company changed its name from Stirling Minerals Limited to African Iron Limited to reflect its new direction, and appointed a new Board with an iron ore development and operations skill set, and a new Company Secretary. The Board appointed comprised Dr Ian Burston as Non-Executive Chairman, and Mr Joe Ariti and Mr Tony Sage as Non-Executive Directors. Mr Ariti acted as the Company’s Chief Executive Officer until the appointment of Mr Simon Youds in September 2011. Ms Claire Tolcon was appointed as Company Secretary.

The Company was re-admitted to official quotation on ASX on 14 January 2011.

Non Executive Chairman Dr Ian Burston appointed 10 January 2011Non Executive Director Mr Antony Sage appointed 10 January 2011Non Executive Director Mr Joe Ariti appointed 10 January 2011Non Executive Director The Hon. John Moore AO appointed 1 July 2011Executive Director Mr Tony King resigned 10 January 2011Non Executive Director Mr Jason Bontempo resigned 10 January 2011Non Executive Director Mr Stephen Brockhurst resigned 10 January 2011

DIRECTORS’ REpORT

Annual Report for the Year Ended 30 June 2011 7

AFRICAN IRON LTDF

or p

erso

nal u

se o

nly

REVIEW OF OpERATIONSAs set out above, the Company pursued a new direction and acquired its principal asset, being an 80% interest in the Mayoko Project, in January 2011.

The Mayoko Project represents a near term development opportunity in the emerging iron ore province of West Africa. Unlike other iron ore projects in the region, it has excellent infrastructure access with an underutilised, heavy haulage railway passing within 2km of the main prospect at Mt Lekoumou and terminating at the port of Pointe-Noire on the Atlantic coast.

The Company’s objective is to develop an initial 5Mtpa DSO operation at Mayoko by mid-2013 leveraging off the project’s proximity to existing rail and port infrastructure.

The following significant milestones were achieved during the current year subsequent to the Company acquiring its 80% interest in the Mayoko Project: • The government of the Republic of Congo renewed the Mayoko-Lekoumou iron ore exploration permit for a further period

of two years to April 2013 and the Company was granted an exemption from the requirement to relinquish up to 50% of the permit surface area on the first renewal.

• A 30,000m oxide, resource definition drilling program at the Mount Lekoumou and Mount Mipoundi prospects commenced with the objective of increasing the size and confidence of the existing supergene hematite, DSO Inferred Mineral Resource (33Mt at 56% Fe), and defining a maiden Inferred Mineral Resource for the underlying beneficiable DSO (“bDSO”) that together make up the weathered (oxide) mantle over the primary magnetite mineralisation.

• The Company has engaged independent, global mining consultant, Golder Associates Pty Ltd to prepare an interim JORC resource update to include the diamond drill results received from the 2010 drilling program, and the resource drilling definition program assay results received to 30 September 2011. The Company expects the interim resource update will be released to the market by the end of October 2011.

• The first batch of drill results has confirmed the thickness and grade of the supergene DSO iron “hat” with grades of 50-60% Fe (with reference to the 1975 drilling completed by earlier explorers) and that of the underlying bDSO at 40-45% Fe.

• Bateman Engineering Pty Ltd was appointed to manage a phase one metallurgical test work program. Davis Tube Recovery test work on magnetite banded iron formation samples remaining from the 2010 drilling program was completed and confirmed earlier results whereby high quality iron concentrates with an average 69.3% Fe and low levels of deleterious elements are produced at a coarse grind size with high average mass yields (43.5%).

• The Rail Memorandum of Understanding (“Rail MoU“) with Chemin de Fer Congo Ocean (“CFCO”) was extended and provides African Iron with access to CFCO’s heavy haulage mineral rail network, which passes within 2km of the Mayoko Project.

• Preliminary rail study completed by global infrastructure group, Egis International confirms the underutilised railway can transport a minimum 10 million tonnes per annum of iron ore.

• Preliminary studies for the rehabilitation of the Mayoko town airstrip commenced, with the aim of having it operational in 2011. The recommissioning of the airstrip will enable efficient transport of personnel and goods between Pointe-Noire and the Mayoko Project.

• Major airborne geophysics survey were completed over the remaining 780km2 of the Mayoko-Lekoumou Exploration Permit resulting in an 80% increase in the aggregate exploration target size1 to 1.6-2.6 billion tonnes at 30-65% Fe. Importantly, 320-520 million tonnes at 40-65% Fe represents potential direct shipping ore (“DSO”) and beneficiable DSO.

1. The estimates of exploration target sizes mentioned in this Annual Report should not be misunderstood or misconstrued as estimates of Mineral Resources. The

estimate of exploration target sizes are conceptual in nature and there has been insufficient exploration completed to date to determine the quantity and grade, and

estimate a Mineral Resource in accordance with JORC Code (2004) guidelines. Furthermore, it is uncertain if future exploration will result in the determination of a

Mineral Resource.

DIRECTORS’ REpORTCONTINUED

8 African Iron Limited and its controlled entities

AFRICAN IRON LTD

For

per

sona

l use

onl

y

In June 2011, ASX listed, Equatorial Resources Limited (“Equatorial”) acquired a 19.9% stake in African Iron. Equatorial is exploring for iron ore in the Republic of Congo and holds an exploration permit to the west of, and contiguous with, African Iron’s Mayoko-Lekoumou Exploration Permit.

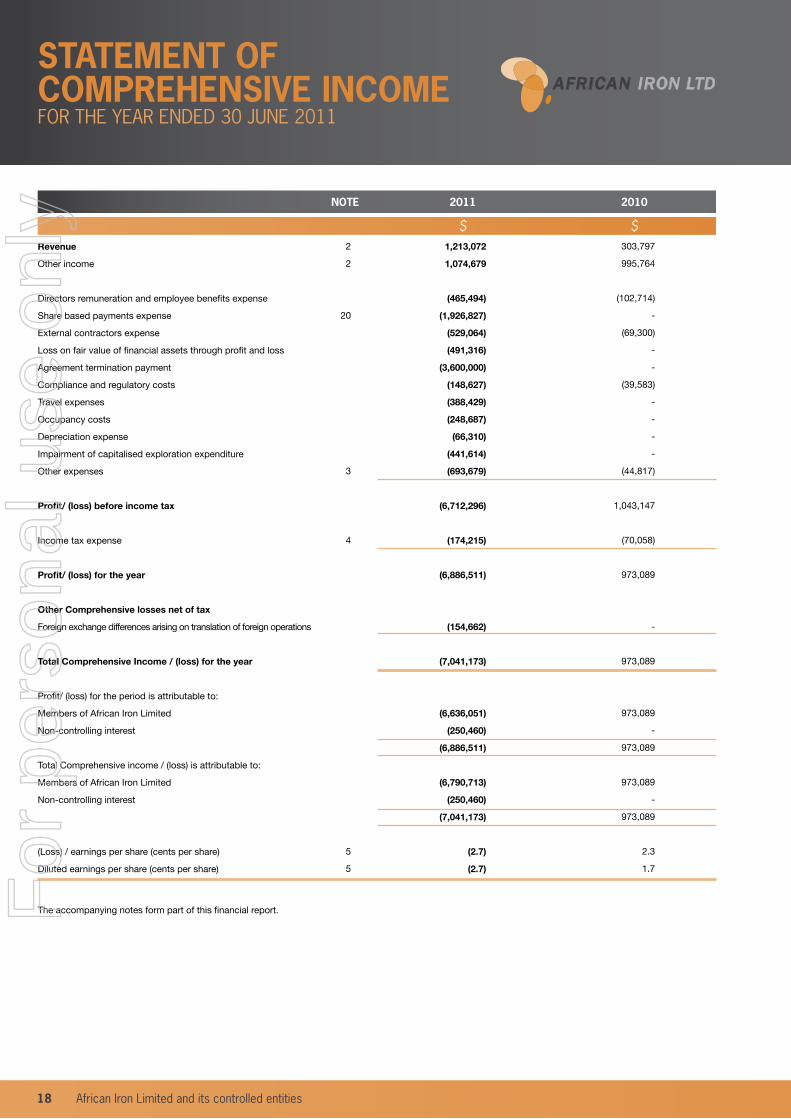

RESULTThe net loss attributable for the year ended 30 June 2011 was $6,886,511 (2010: net profit of $973,089).

DIVIDENDSNo dividend has been paid or recommended by the Directors since the commencement of the financial year.

SUbSEqUENT EVENTSIn July 2011, the independence of the board was strengthened by the appointment of the Hon. John Moore AO as an independent, Non-Executive Director.

In August 2011, the Company secured, through a new 85% owned Congolese subsidiary, an Authority to Prospect for iron ore in the Republic of Congo, West Africa (“Ngoubou-Ngoubou Permit”). The Ngoubou-Ngoubou permit covers an area of 944km2

and is the northern extension of the Company’s Mayoko-Lekoumou Exploration Permit, which hosts the Mayoko iron ore project.

The Company appointed Mr Simon Youds as its Chief Executive Officer with effect from 5 September 2011. Mr Youds is a professional mining engineer with extensive African and bulk commodities experience and a track record of taking mineral projects from concept to production.

On 14 September 2011, the Company completed the acquisition of an additional 12% of DMC Iron (Congo) SA. As a consequence of the acquisition, the Company now owns 92% of the Mayoko iron ore project. The consideration for the acquisition comprised:

• $5,800,000 in cash;

• 22,315,436 fully paid ordinary African Iron shares (subject to escrow restrictions for a period of 13 months from the date of issue) at a deemed issue price of $0.298 per share; and

• a deferred consideration of A$0.150 for each dry metric tonne of iron ore sold from the Mayoko Project.

Apart from the above, no matters or circumstances have arisen since the end of the financial year which significantly affected or may significantly affect the operations of the Group or the state of affairs of the Group in future financial years.

LIKELy DEVELOpmENTS AND ExpECTED RESULTSThe Group will continue its mineral exploration activity at its exploration projects with the object of identifying commercial resources.

ENVIRONmENTAL REGULATIONThe Group operates within the resources sector and aims to conduct its exploration activities in such a manner that ensures the highest standard of environmental care is achieved, and that it complies with all relevant environmental legislation.

DIRECTORS’ REpORTCONTINUED

Annual Report for the Year Ended 30 June 2011 9

AFRICAN IRON LTDF

or p

erso

nal u

se o

nly

INFORmATION ON DIRECTORS IN OFFICE AS AT ThE DATE OF ThIS REpORT

DR IAN bURSTON

mR JOE ARITI

qUALIFICATIONS

qUALIFICATIONS

ExpERIENCE

ExpERIENCE

INTEREST IN ShARES AND OpTIONS

INTEREST IN ShARES AND OpTIONS

FORmER DIRECTORShIpS hELD IN pAST ThREE yEARS

CURRENT DIRECTORShIpS

CURRENT DIRECTORShIpS

Degree in Mechanical Engineering, Diploma in Aeronautical Engineering, Honorary Doctor of Science

Bachelor of Science and Diploma in Mineral Science from Murdoch University; Masters Degree in Business Administration from the Edinburgh Business School (UK); and Member of the Australasian Institute of Mining and Metallurgy and Australian Institute of Company Directors.

Dr Ian Burston has more than 30 years of experience in Western Australian and international mining. Formerly, Ian Burston held positions as Managing Director of Hamersley Iron Pty Limited, Aurora Gold Limited and Portman Limited and Chief Executive Officer of Kalgoorlie Consolidated Mines Pty Limited. Previously he worked for the CRA Group (now part of Rio Tinto plc) for 22 years in various senior executive positions. Dr Burston was Non-Executive Chairman of Imdex Limited from 2000 to 2009 and served as Executive Chairman and Chief Executive Officer of Aztec Resources Limited between June 2003 and February 2006.

Mr Joe Ariti is a Metallurgist with over 25 years experience in technical, management and executive roles in assessing, developing and managing mining projects and companies in Australia and overseas. Mr Ariti has been involved in the development and management of both open cut and underground mining projects in Australia, Africa, Indonesia and Papua New Guinea.

4,000,000 unlisted options (exercisable at $0.30 each on or before 31 December 2012) (escrowed for 24 months from the date of re-quotation of the Company on ASX).

300,000 ordinary shares 6,000,000 unlisted options (exercisable at $0.30 each on or before 31 December 2012) (escrowed until 14 January 2013). 100,000 listed options (exercisable at $0.20 each on or before 1 December 2013)

Carrick Gold Limited (November 2009 to August 2010), Condor Nickel Limited (March 2010 to August 2010), Cape Lambert Resources Limited (July 2006 to August 2008), Auvex Resources Limited (January 2009 to September 2009), Imdex Limited (November 2000 to October 2009), Forescue Metals Group (October 2008 to August 2011).

Current directorships include Broome Port Authority (Chairman), Kanzai Mining Corporation (Director), NRW Holdings Limited (Chairman and Non-Executive Director since July 2007) and Mincor Resources NL (Non-Executive Director since January 2003).

Non-executive director of ASX listed entities Swick Mining Services Limited and Matrix Metals Limited.

non-eXeCutiVe Chairman (appointeD on 10 january 2011)

non-eXeCutiVe DireCtor (appointeD on 10 january 2011)

FORmER DIRECTORShIpS hELD IN pAST ThREE yEARS

Territory Resources Limited (from August 2008 to July 2011), Azumah Resources Limited (from September 2007 to October 2009), DMC Mining Limited (from August 2009 to September 2010), ABM Resources NL (from July 2008 to December 2008).

10 African Iron Limited and its controlled entities

AFRICAN IRON LTDDIRECTORS’ REpORTCONTINUED

For

per

sona

l use

onl

y

mR TONy SAGE

ThE hON. JOhN mOORE AO

qUALIFICATIONS

qUALIFICATIONS

ExpERIENCE

ExpERIENCE

INTEREST IN ShARES AND OpTIONS

INTEREST IN ShARES AND OpTIONS

FORmER DIRECTORShIpS hELD IN pAST ThREE yEARS

CURRENT DIRECTORShIpS

CURRENT DIRECTORShIpS

Bachelor of Commerce, FCPA, CA, FTIA

Bachelor of Commerce and Associate in Accountancy from the University of Queensland.

Mr Tony Sage has in excess of 24 years experience in the fields of corporate advisory services, funds management and capital raising. Mr Sage is based in Western Australia and has been involved in the management and financing of listed mining companies for the last 15 years.

The Hon. John Moore AO has had a distinguished career in Australian politics: John was the Federal Minister of Defence, the Minister for Industry, Science and Tourism and Vice President of the Executive Council.

Prior to entering politics, John was a stockbroker and member of the Brisbane Stock Exchange for 12 years. John has served on the board of many broking and banking related companies including Citinational Limited, Merril Lynch (Aust) Pty Ltd and Grindlays (Aust) Pty Ltd.

500,000 ordinary shares 8,000,000 unlisted options (exercisable at $0.30 each on or before 31 December 2012) (escrowed for 24 months from the date of re-quotation of the Company on ASX).

500,000 ordinary shares

ASX listedCape Lambert Resources Limited (December 2000 to present)Fe Limited (August 2009 to present)Chameleon Mining NL (September 2010 to present)Cauldron Energy Limited (June 2009 to present)Matrix Metals Limited (Dec 2010 to present)International Goldfields Limited (February 2009 to present)NSX listedInternational Petroleum Limited (January 2006 to present)African Petroleum Corporation Limited (October 2007 to present)

Chairman of ASX listed entities Cape Lambert Resources Limited, Cauldron Energy Limited, International Goldfields Limited, Fe Limited and NSX listed International Petroleum Limited. Non-Executive Deputy Chairman of NSX listed African Petroleum Corporation Limited. Non-Executive director ASX listed Chameleon Mining NL and Matrix Metals Limited.

Herencia Resources plc

non-eXeCutiVe DireCtor (appointeD on 10 january 2011)

non-eXeCutiVe DireCtor (appointeD on 10 january 2011)

FORmER DIRECTORShIpS hELD IN pAST ThREE yEARS

International Goldfields Limited (2006 to 30 June 2011)

COmpANy SECRETARyMs Claire Tolcon was appointed 10 January 2011. Ms Tolcon holds a Bachelor of Law and Bachelor of Commerce (Accounting) degree and is a member of FINSIA and has 14 years experience in the legal profession, primarily in the areas of equity capital markets, mergers and acquisitions, corporate restructuring, corporate governance and mining and resources. Ms Tolcon was a partner of a corporate law firm for a number of years before joining the Company.

Annual Report for the Year Ended 30 June 2011 11

AFRICAN IRON LTDDIRECTORS’ REpORTCONTINUED

For

per

sona

l use

onl

y

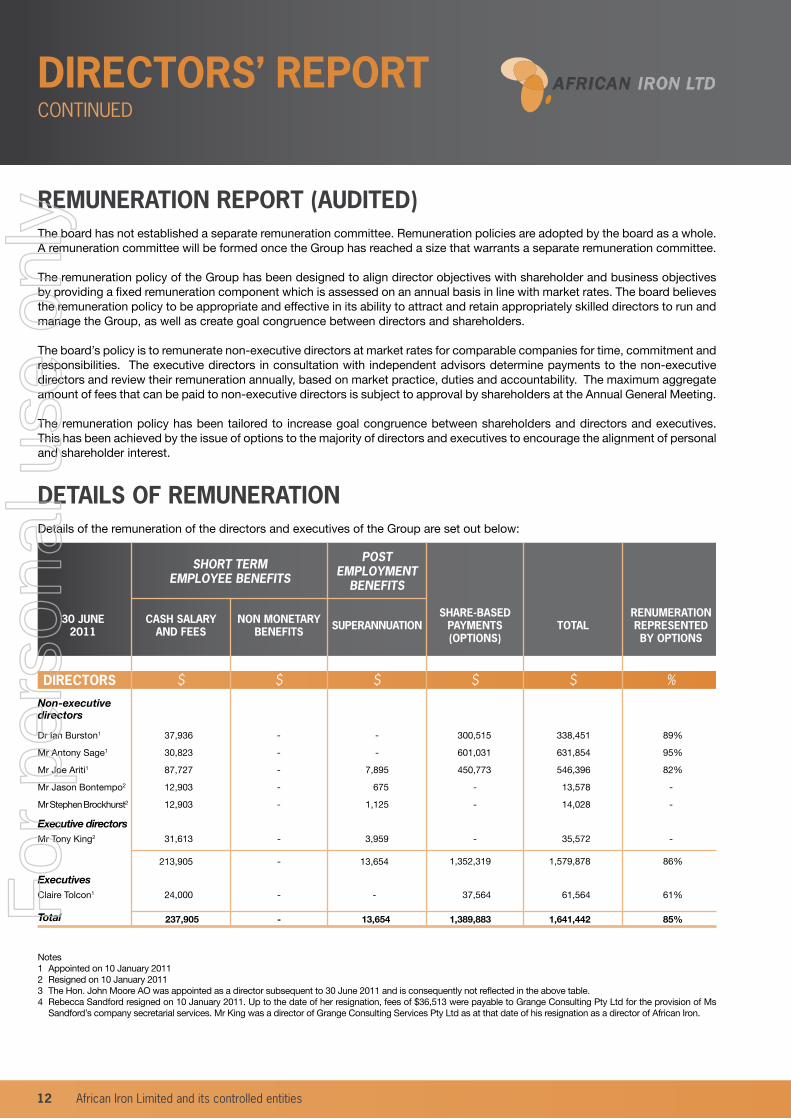

REmUNERATION REpORT (AUDITED)The board has not established a separate remuneration committee. Remuneration policies are adopted by the board as a whole. A remuneration committee will be formed once the Group has reached a size that warrants a separate remuneration committee.

The remuneration policy of the Group has been designed to align director objectives with shareholder and business objectives by providing a fixed remuneration component which is assessed on an annual basis in line with market rates. The board believes the remuneration policy to be appropriate and effective in its ability to attract and retain appropriately skilled directors to run and manage the Group, as well as create goal congruence between directors and shareholders.

The board’s policy is to remunerate non-executive directors at market rates for comparable companies for time, commitment and responsibilities. The executive directors in consultation with independent advisors determine payments to the non-executive directors and review their remuneration annually, based on market practice, duties and accountability. The maximum aggregate amount of fees that can be paid to non-executive directors is subject to approval by shareholders at the Annual General Meeting.

The remuneration policy has been tailored to increase goal congruence between shareholders and directors and executives. This has been achieved by the issue of options to the majority of directors and executives to encourage the alignment of personal and shareholder interest.

DETAILS OF REmUNERATIONDetails of the remuneration of the directors and executives of the Group are set out below:

CASh SALARy AND FEES

30 JUNE2011

Short term employee benefitS

poSt employment

benefitS

NON mONETARy bENEFITS

ShARE-bASED pAymENTS (OpTIONS)

RENUmERATION REpRESENTED by OpTIONS

TOTALSUpERANNUATION

DIRECTORS

Non-executive directors

Executive directors

Executives

Total

Dr Ian Burston1

Mr Antony Sage1

Mr Joe Ariti1

Mr Jason Bontempo2

Mr Stephen Brockhurst2

37,936

30,823

87,727

12,903

12,903

31,613

213,905

24,000

237,905

37,564

1,389,883 1,641,44213,654

61,564

13,654 1,352,319 1,579,878 86%

61%

85%

3,959 35,572-

-

-

-

-

- -

300,515

601,031

450,773

-

-

338,451

631,854

546,396

13,578

14,028

-

-

7,895

675

1,125

89%

95%

82%

-

-

-

-

-

-

-

Mr Tony King2

Claire Tolcon1

$ $ $ $ $ %

Notes1 Appointed on 10 January 20112 Resigned on 10 January 20113 The Hon. John Moore AO was appointed as a director subsequent to 30 June 2011 and is consequently not reflected in the above table.4 Rebecca Sandford resigned on 10 January 2011. Up to the date of her resignation, fees of $36,513 were payable to Grange Consulting Pty Ltd for the provision of Ms

Sandford’s company secretarial services. Mr King was a director of Grange Consulting Services Pty Ltd as at that date of his resignation as a director of African Iron.

12 African Iron Limited and its controlled entities

AFRICAN IRON LTDDIRECTORS’ REpORTCONTINUED

For

per

sona

l use

onl

y

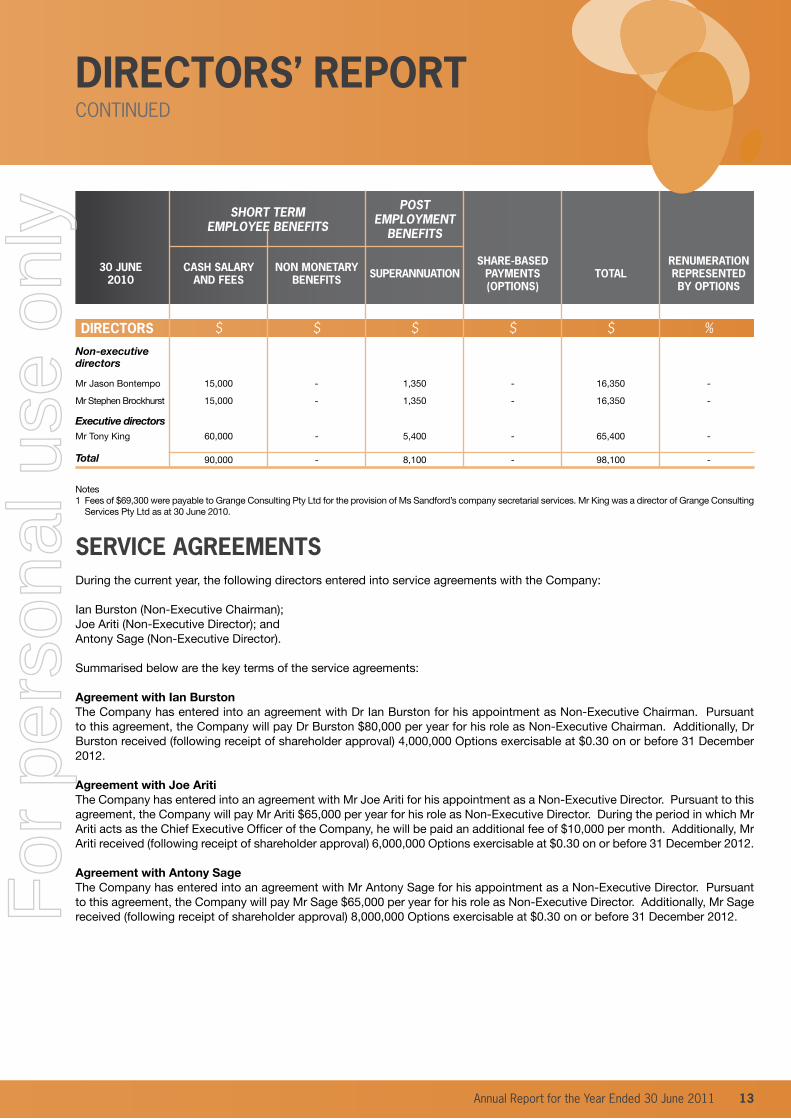

SERVICE AGREEmENTSDuring the current year, the following directors entered into service agreements with the Company:

Ian Burston (Non-Executive Chairman);Joe Ariti (Non-Executive Director); andAntony Sage (Non-Executive Director).

Summarised below are the key terms of the service agreements:

Agreement with Ian BurstonThe Company has entered into an agreement with Dr Ian Burston for his appointment as Non-Executive Chairman. Pursuant to this agreement, the Company will pay Dr Burston $80,000 per year for his role as Non-Executive Chairman. Additionally, Dr Burston received (following receipt of shareholder approval) 4,000,000 Options exercisable at $0.30 on or before 31 December 2012.

Agreement with Joe AritiThe Company has entered into an agreement with Mr Joe Ariti for his appointment as a Non-Executive Director. Pursuant to this agreement, the Company will pay Mr Ariti $65,000 per year for his role as Non-Executive Director. During the period in which Mr Ariti acts as the Chief Executive Officer of the Company, he will be paid an additional fee of $10,000 per month. Additionally, Mr Ariti received (following receipt of shareholder approval) 6,000,000 Options exercisable at $0.30 on or before 31 December 2012.

Agreement with Antony SageThe Company has entered into an agreement with Mr Antony Sage for his appointment as a Non-Executive Director. Pursuant to this agreement, the Company will pay Mr Sage $65,000 per year for his role as Non-Executive Director. Additionally, Mr Sage received (following receipt of shareholder approval) 8,000,000 Options exercisable at $0.30 on or before 31 December 2012.

Notes1 Fees of $69,300 were payable to Grange Consulting Pty Ltd for the provision of Ms Sandford’s company secretarial services. Mr King was a director of Grange Consulting

Services Pty Ltd as at 30 June 2010.

CASh SALARy AND FEES

30 JUNE2010

Short term employee benefitS

poSt employment

benefitS

NON mONETARy bENEFITS

ShARE-bASED pAymENTS (OpTIONS)

RENUmERATION REpRESENTED by OpTIONS

TOTALSUpERANNUATION

DIRECTORS

Non-executive directors

Executive directors

Total

Mr Jason Bontempo

Mr Stephen Brockhurst

15,000

15,000

1,350

1,350

90,000 - 98,1008,100 --

-

-

16,350

16,350

-

-

-

-

Mr Tony King

$ $ $ $ $ %

60,000 - 5,400 - 65,400 -

Annual Report for the Year Ended 30 June 2011 13

AFRICAN IRON LTDDIRECTORS’ REpORTCONTINUED

For

per

sona

l use

onl

y

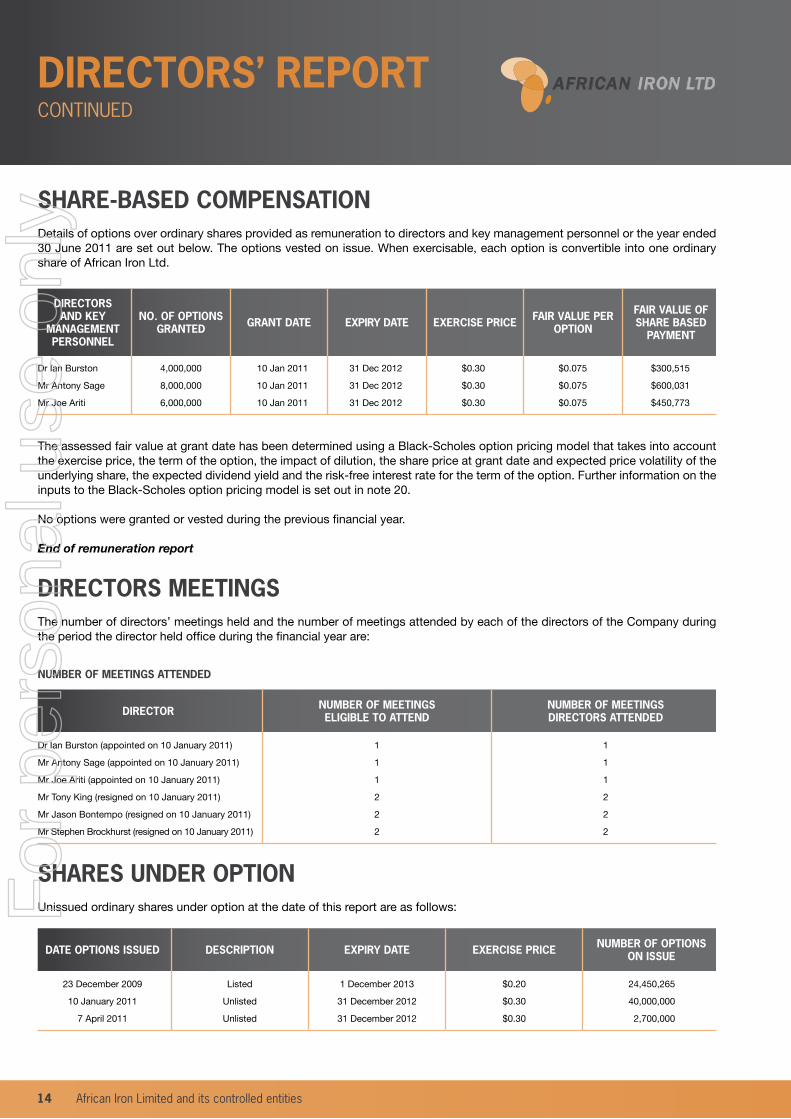

The assessed fair value at grant date has been determined using a Black-Scholes option pricing model that takes into account the exercise price, the term of the option, the impact of dilution, the share price at grant date and expected price volatility of the underlying share, the expected dividend yield and the risk-free interest rate for the term of the option. Further information on the inputs to the Black-Scholes option pricing model is set out in note 20.

No options were granted or vested during the previous financial year.

End of remuneration report

NO. OF OpTIONS GRANTED

DIRECTORS AND KEy

mANAGEmENTpERSONNEL

GRANT DATE ExERCISE pRICEFAIR VALUE OF ShARE bASED

pAymENT

FAIR VALUE pER OpTIONExpIRy DATE

Dr Ian Burston

Mr Antony Sage

Mr Joe Ariti

4,000,000

8,000,000

6,000,000

10 Jan 2011

10 Jan 2011

10 Jan 2011

31 Dec 2012

31 Dec 2012

31 Dec 2012

$0.30

$0.30

$0.30

$0.075

$0.075

$0.075

$300,515

$600,031

$450,773

ShARE-bASED COmpENSATION Details of options over ordinary shares provided as remuneration to directors and key management personnel or the year ended 30 June 2011 are set out below. The options vested on issue. When exercisable, each option is convertible into one ordinary share of African Iron Ltd.

DIRECTORS mEETINGSThe number of directors’ meetings held and the number of meetings attended by each of the directors of the Company during the period the director held office during the financial year are:

DIRECTOR

NUmbER OF mEETINGS ATTENDED

NUmbER OF mEETINGS ELIGIbLE TO ATTEND

NUmbER OF mEETINGS DIRECTORS ATTENDED

Dr Ian Burston (appointed on 10 January 2011)

Mr Antony Sage (appointed on 10 January 2011)

Mr Joe Ariti (appointed on 10 January 2011)

Mr Tony King (resigned on 10 January 2011)

Mr Jason Bontempo (resigned on 10 January 2011)

Mr Stephen Brockhurst (resigned on 10 January 2011)

1

1

1

2

2

2

1

1

1

2

2

2

DATE OpTIONS ISSUED DESCRIpTION ExpIRy DATE ExERCISE pRICE NUmbER OF OpTIONS ON ISSUE

23 December 2009

10 January 2011

7 April 2011

1 December 2013

31 December 2012

31 December 2012

$0.20

$0.30

$0.30

24,450,265

40,000,000

2,700,000

Listed

Unlisted

Unlisted

ShARES UNDER OpTIONUnissued ordinary shares under option at the date of this report are as follows:

14 African Iron Limited and its controlled entities

AFRICAN IRON LTDDIRECTORS’ REpORTCONTINUED

For

per

sona

l use

onl

y

ShARES ISSUED ON ThE ExERCISE OF OpTIONSThere were no options exercised during the financial year (2010: nil).

INSURANCE OF OFFICERSDuring the financial year, African Iron Limited paid the required premiums to insure the directors and officers of the Group.

The liabilities insured are legal costs that may be incurred in defending civil or criminal proceedings that may be brought against the officers in their capacity as officers of entities in the Group, and any other payments arising from liabilities incurred by the officers in connection with such proceedings. This does not include such liabilities that arise from conduct involving a wilful breach of duty by the officers or the improper use by the officers of their position or of information to gain advantage for them or someone else or to cause detriment to the Group. It is not possible to apportion the premium between amounts relating to the insurance against legal costs and those relating to other liabilities.

pROCEEDINGS ON bEhALF OF ThE GROUpNo person has applied to the Court under section 237 of the Corporations Act 2001 for leave to bring proceedings on behalf of the Group, or to intervene in any proceedings to which the Group is a party, for the purpose of taking responsibility on behalf of the Group for all or part of those proceedings.

No proceedings have been brought or intervened in on behalf of the Group with leave of the Court under section 237 of the Corporations Act 2001.

NON-AUDIT SERVICESThe Board of Directors is satisfied that the provision of any non-audit services by the Company’s auditors is compatible with the general standard of independence for auditors imposed by the Corporations Act 2001 because:

• All non-audit services are reviewed and approved by the Board of Directors prior to commencement to ensure they do not adversely affect the integrity and objectivity of the auditor; and

• The nature of the services provided is reviewed to ensure that hey do not compromise the general principles relating to auditor independence in accordance with APES 110: Code of Ethics for Professional Accountants set by the Accounting Professional and Ethical Standards Board.

During the current year $20,000 was paid (2010: Nil) to the auditor for non-audit services provided.

Annual Report for the Year Ended 30 June 2011 15

AFRICAN IRON LTDDIRECTORS’ REpORTCONTINUED

For

per

sona

l use

onl

y

COmpETENT pERSON STATEmENTThe information in this report that relates to Exploration Results and Mineral Resources is based on information reviewed and compiled by Mr Patrick Vekemans, who is a Member of the Australian Institute of Geosciences. Mr Vekemans is a contractor to African Iron Limited and has sufficient experience which is relevant to the style of mineralisation and the type of deposit under consideration and to the activity which he is undertaking to qualify as a Competent Person as defined in the 2004 edition of the Australasian Code for Reporting of Exploration Results, Minerals Resources and Ore Reserves. Mr Vekemans consents to the inclusion in this report of this information in the form and context in which it appears.

Auditor’s Independence Declaration

A copy of the auditors’ independence declaration as required under section 307C of the Corporations Act 2001 is set out on page 17.

This report of Directors, incorporating the Remuneration Report, is signed in accordance with a resolution of Directors.

Joe Ariti

Perth, Western Australia, 30 September 2011

16 African Iron Limited and its controlled entities

AFRICAN IRON LTDDIRECTORS’ REpORTCONTINUED

For

per

sona

l use

onl

y

To The Board of Directors

Auditor’s Independence Declaration under Section 307C of the Corporations Act 2001 This declaration is made in connection with our audit of the financial report of African Iron Limited and Controlled Entities for the year ended 30 June 2011 and in accordance with the provisions of the Corporations Act 2001. We declare that, to the best of our knowledge and belief, there have been: no contraventions of the auditor independence requirements of the Corporations Act

2001 in relation to the audit; no contraventions of the Code of Professional Conduct of the Institute of Chartered

Accountants in Australia in relation to the audit. Yours faithfully BENTLEYS CHRIS WATTS CA Chartered Accountants Director DATED at PERTH this 30th day of September 2011

Annual Report for the Year Ended 30 June 2011 17

AFRICAN IRON LTDAUDITOR’SINDEpENDENCEDECLARATION

For

per

sona

l use

onl

y

The accompanying notes form part of this financial report.

NOTE 20102011

Revenue

Other income

Directors remuneration and employee benefits expense

Share based payments expense

External contractors expense

Loss on fair value of financial assets through profit and loss

Agreement termination payment

Compliance and regulatory costs

Travel expenses

Occupancy costs

Depreciation expense

Impairment of capitalised exploration expenditure

Other expenses

Profit/ (loss) before income tax

Income tax expense

Profit/ (loss) for the year

Other Comprehensive losses net of tax

Foreign exchange differences arising on translation of foreign operations

Total Comprehensive Income / (loss) for the year

Profit/ (loss) for the period is attributable to:

Members of African Iron Limited

Non-controlling interest

Total Comprehensive income / (loss) is attributable to:

Members of African Iron Limited

Non-controlling interest

(Loss) / earnings per share (cents per share)

Diluted earnings per share (cents per share)

2

2

20

3

4

5

5

1,213,072

1,074,679

(465,494)

(1,926,827)

(529,064)

(491,316)

(3,600,000)

(148,627)

(388,429)

(248,687)

(66,310)

(441,614)

(693,679)

(6,712,296)

(174,215)

(6,886,511)

(154,662)

(7,041,173)

(6,636,051)

(250,460)

(6,886,511)

(6,790,713)

(250,460)

(7,041,173)

(2.7)

(2.7)

303,797

995,764

(102,714)

-

(69,300)

-

-

(39,583)

-

-

-

-

(44,817)

1,043,147

(70,058)

973,089

-

973,089

973,089

-

973,089

973,089

-

973,089

2.3

1.7

$$

18 African Iron Limited and its controlled entities

AFRICAN IRON LTDSTATEmENT OFCOmpREhENSIVE INCOmEFOR THE YEAR ENDED 30 JUNE 2011

For

per

sona

l use

onl

y

The accompanying notes form part of this financial report.

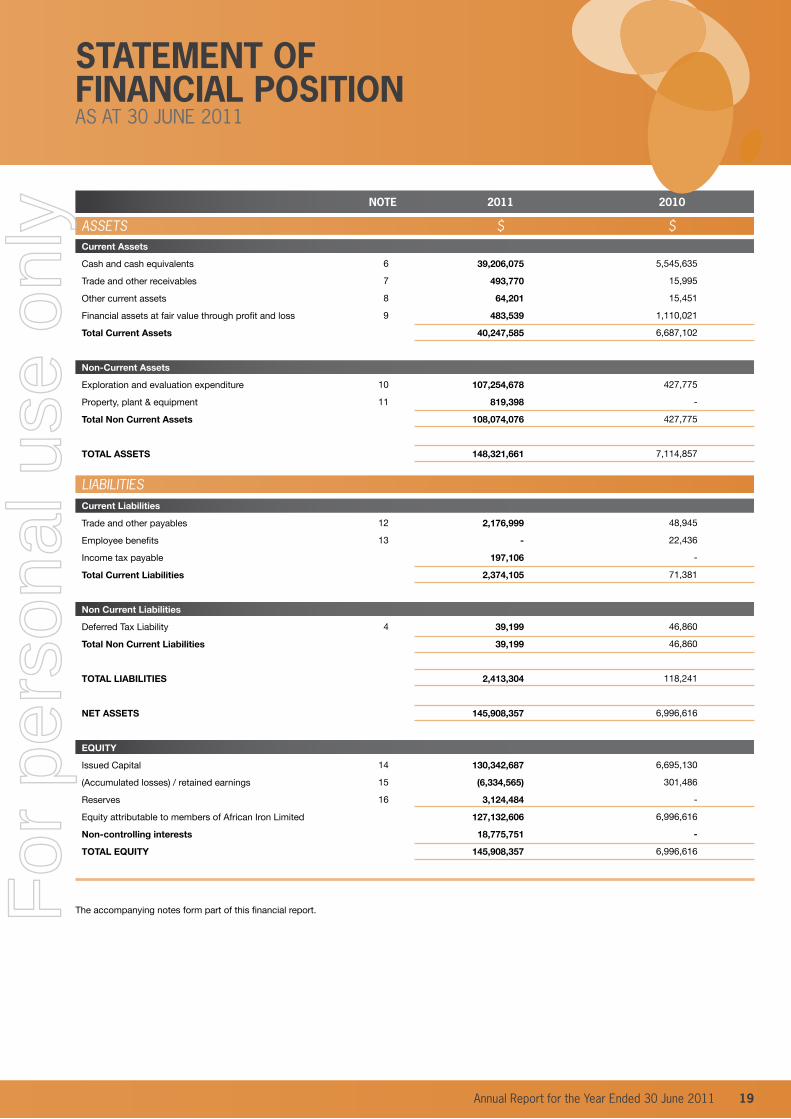

NOTE 20102011

Current Assets

Cash and cash equivalents

Trade and other receivables

Other current assets

Financial assets at fair value through profit and loss

Total Current Assets

Non-Current Assets

Exploration and evaluation expenditure

Property, plant & equipment

Total Non Current Assets

TOTAL ASSETS

Current Liabilities

Trade and other payables

Employee benefits

Income tax payable

Total Current Liabilities

Non Current Liabilities

Deferred Tax Liability

Total Non Current Liabilities

TOTAL LIABILITIES

NET ASSETS

EQUITY

Issued Capital

(Accumulated losses) / retained earnings

Reserves

Equity attributable to members of African Iron Limited

Non-controlling interests

TOTAL EQUITY

6

7

8

9

10

11

12

13

4

14

15

16

39,206,075

493,770

64,201

483,539

40,247,585

107,254,678

819,398

108,074,076

148,321,661

2,176,999

-

197,106

2,374,105

39,199

39,199

2,413,304

145,908,357

130,342,687

(6,334,565)

3,124,484

127,132,606

18,775,751

145,908,357

5,545,635

15,995

15,451

1,110,021

6,687,102

427,775

-

427,775

7,114,857

48,945

22,436

-

71,381

46,860

46,860

118,241

6,996,616

6,695,130

301,486

-

6,996,616

-

6,996,616

$$assets

liaBilities

Annual Report for the Year Ended 30 June 2011 19

AFRICAN IRON LTDSTATEmENT OFFINANCIAL pOSITIONAS AT 30 JUNE 2011

For

per

sona

l use

onl

y

The accompanying notes form part of this financial report.

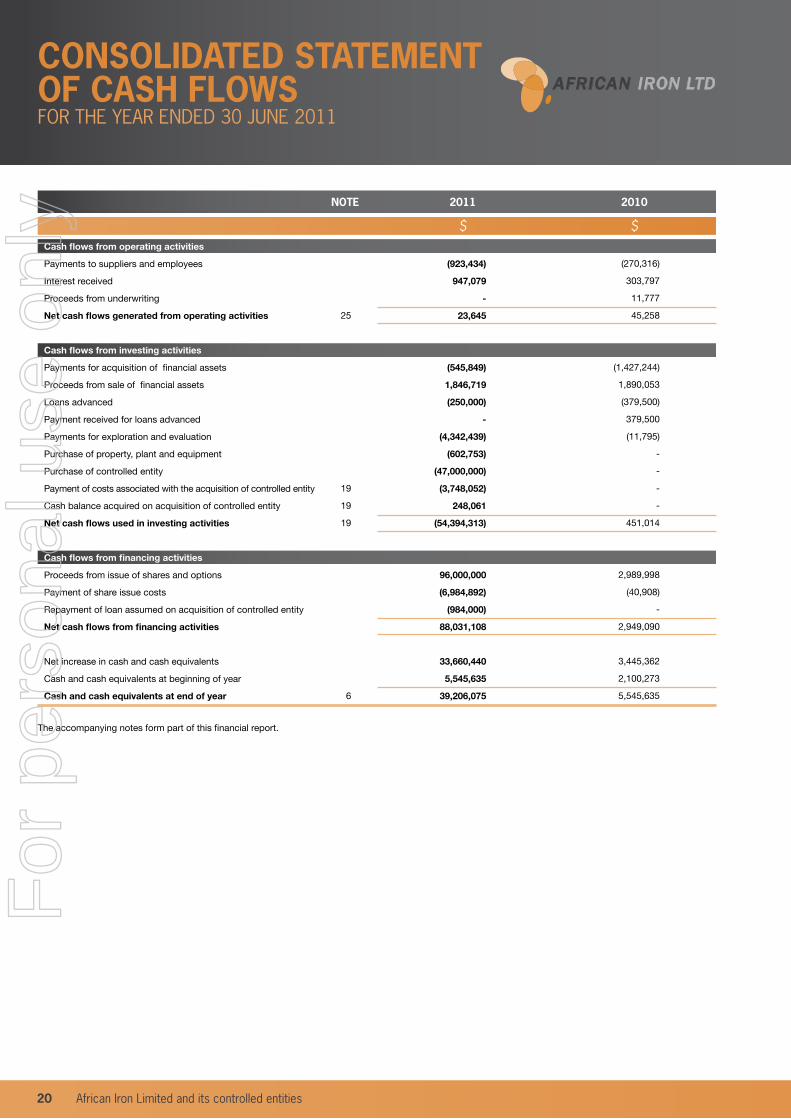

NOTE 20102011

Cash flows from operating activities

Payments to suppliers and employees

Interest received

Proceeds from underwriting

Net cash flows generated from operating activities

Cash flows from investing activities

Payments for acquisition of financial assets

Proceeds from sale of financial assets

Loans advanced

Payment received for loans advanced

Payments for exploration and evaluation

Purchase of property, plant and equipment

Purchase of controlled entity

Payment of costs associated with the acquisition of controlled entity

Cash balance acquired on acquisition of controlled entity

Net cash flows used in investing activities

Cash flows from financing activities

Proceeds from issue of shares and options

Payment of share issue costs

Repayment of loan assumed on acquisition of controlled entity

Net cash flows from financing activities

Net increase in cash and cash equivalents

Cash and cash equivalents at beginning of year

Cash and cash equivalents at end of year

25

19

19

19

6

(923,434)

947,079

-

23,645

(545,849)

1,846,719

(250,000)

-

(4,342,439)

(602,753)

(47,000,000)

(3,748,052)

248,061

(54,394,313)

96,000,000

(6,984,892)

(984,000)

88,031,108

33,660,440

5,545,635

39,206,075

(270,316)

303,797

11,777

45,258

(1,427,244)

1,890,053

(379,500)

379,500

(11,795)

-

-

-

-

451,014

2,989,998

(40,908)

-

2,949,090

3,445,362

2,100,273

5,545,635

$$

20 African Iron Limited and its controlled entities

AFRICAN IRON LTDCONSOLIDATED STATEmENTOF CASh FLOWSFOR THE YEAR ENDED 30 JUNE 2011

For

per

sona

l use

onl

y

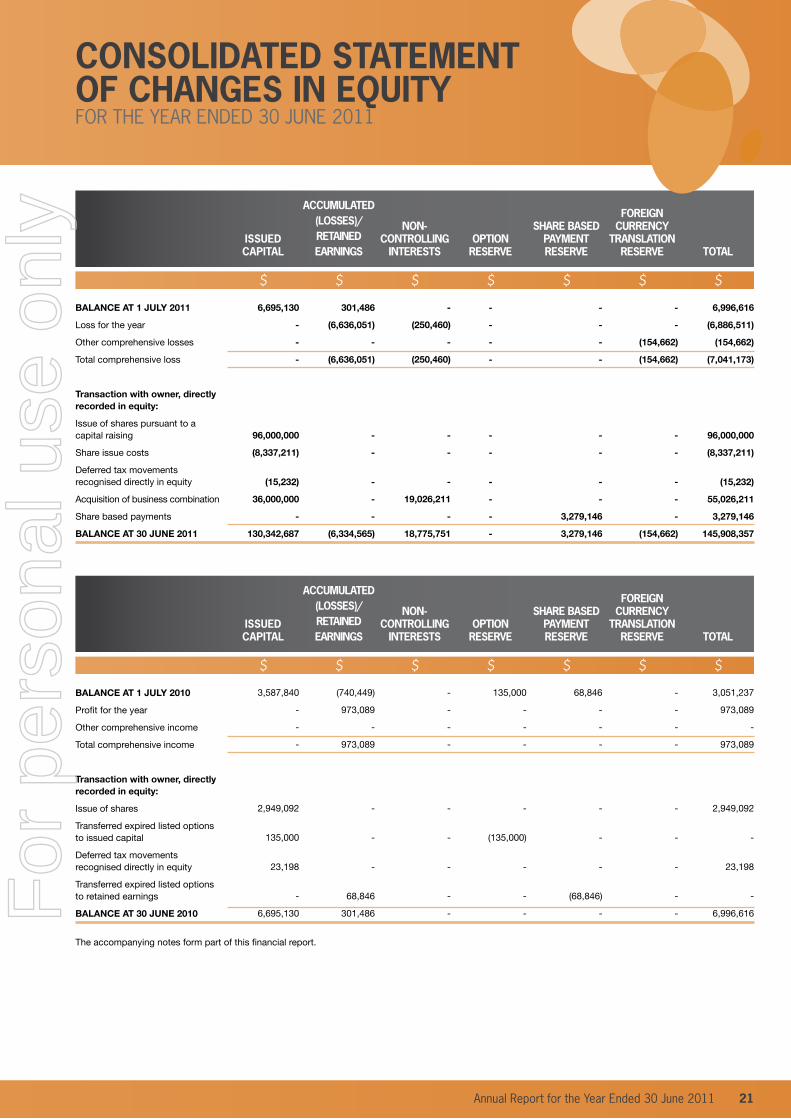

BALANCE AT 1 JULY 2011

Loss for the year

Other comprehensive losses

Total comprehensive loss

Transaction with owner, directly recorded in equity:

Issue of shares pursuant to a capital raising

Share issue costs

Deferred tax movements recognised directly in equity

Acquisition of business combination

Share based payments

BALANCE AT 30 JUNE 2011

6,996,616

(6,886,511)

(154,662)

(7,041,173)

96,000,000

(8,337,211)

(15,232)

55,026,211

3,279,146

145,908,357

6,695,130

-

-

-

96,000,000

(8,337,211)

(15,232)

36,000,000

-

130,342,687

301,486

(6,636,051)

-

(6,636,051)

-

-

-

-

-

(6,334,565)

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

3,279,146

3,279,146

-

-

(154,662)

(154,662)

-

-

-

-

-

(154,662)

-

(250,460)

-

(250,460)

-

-

-

19,026,211

-

18,775,751

ISSUEDCApITAL

ACCUmULATED(LOSSES)/RETAINEDEARNINGS

NON-CONTROLLING

INTERESTSOpTION

RESERVE

ShARE bASEDpAymENTRESERVE

FOREIGNCURRENCy

TRANSLATIONRESERVE TOTAL

$ $ $ $ $ $ $

The accompanying notes form part of this financial report.

BALANCE AT 1 JULY 2010

Profit for the year

Other comprehensive income

Total comprehensive income

Transaction with owner, directly recorded in equity:

Issue of shares

Transferred expired listed options to issued capital

Deferred tax movements recognised directly in equity

Transferred expired listed options to retained earnings

BALANCE AT 30 JUNE 2010

3,587,840

-

-

-

2,949,092

135,000

23,198

-

6,695,130

(740,449)

973,089

-

973,089

-

-

-

68,846

301,486

3,051,237

973,089

-

973,089

2,949,092

-

23,198

-

6,996,616

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

68,846

-

-

-

-

-

-

(68,846)

-

135,000

-

-

-

-

(135,000)

-

-

-

ISSUEDCApITAL

ACCUmULATED(LOSSES)/RETAINEDEARNINGS

NON-CONTROLLING

INTERESTSOpTION

RESERVE

ShARE bASEDpAymENTRESERVE

FOREIGNCURRENCy

TRANSLATIONRESERVE TOTAL

$ $ $ $ $ $ $

Annual Report for the Year Ended 30 June 2011 21

AFRICAN IRON LTDCONSOLIDATED STATEmENTOF ChANGES IN EqUITyFOR THE YEAR ENDED 30 JUNE 2011

For

per

sona

l use

onl

y

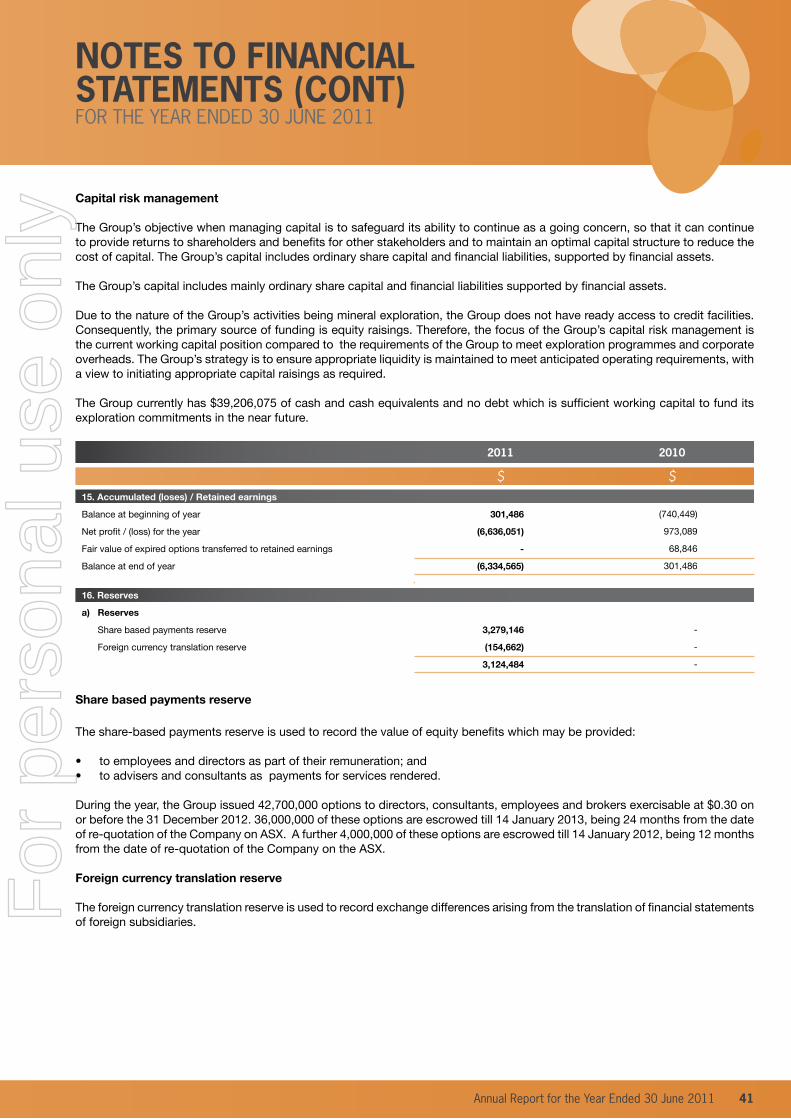

1. SUmmARy OF SIGNIFICANT ACCOUNTING pOLICIES The principal accounting policies adopted in the preparation of the financial statements are set out below. These policies have been consistently applied to all the years presented, unless otherwise stated.

A) bASIS OF pREpARATION

The financial report is a general purpose financial report that has been prepared in accordance with Australian Accounting Standards including Australian Accounting Interpretations, other authoritative pronouncements of the Australian Accounting Standards Board and the Corporations Act 2001.

The financial report has been prepared on the basis of historical cost, except for the revaluation of certain non-current assets and financial instruments. Cost is based on the fair values of the consideration given in exchange for assets.

The financial report is presented in Australian dollars.

The financial report covers African Iron Limited and its controlled entities (“the Group”). African Iron Limited is a public listed company, incorporated and domiciled in Australia.

Compliance with IFRS

The financial report complies with Australian Accounting Standards and International Financial Reporting Standards (IFRS).

b) bASIS OF CONSOLIDATION

The consolidated financial statements comprise the financial statements of African Iron Limited (“African Iron” or “Company”) and its subsidiaries (as outlined in note 22) as at and for the period ended 30 June each year.

Subsidiaries are those entities over which African Iron has the power to govern the financial and operating policies so as to obtain benefits from their activities. The existence and effect of potential voting rights that are currently exercisable or convertible are considered when assessing whether African Iron controls another entity.

The financial statements of the subsidiaries are prepared for the same reporting period as African Iron, using consistent accounting policies. In preparing the consolidated financial statements, all intercompany balances and transactions, income and expenses and profits and losses resulting from intra-group transactions have been eliminated in full.

Investments in subsidiaries held by African Iron are accounted for at cost in the separate financial statements of the parent less any impairment charges.

The acquisition of subsidiaries is accounted for using the acquisition method of accounting. The acquisition method of accounting involves recognising at acquisition, separately from goodwill, the identifiable assets acquired, the liabilities assumed and any non-controlling interest in the acquiree. The identifiable assets acquired and liabilities assumed are measured at their fair values at the date of acquisition. Any difference between the fair value of the consideration and the fair values of the identifiable net assets acquired is recognised as goodwill or a discount on acquisition.

A change in the ownership interest of a subsidiary that does not result in a loss of control is accounted for as an equity transaction.

22 African Iron Limited and its controlled entities

AFRICAN IRON LTDNOTES TO FINANCIALSTATEmENTSFOR THE YEAR ENDED 30 JUNE 2011

For

per

sona

l use

onl

y

Non-controlling interests are allocated their share of net profit after tax in the statement of comprehensive income and are presented with equity in the consolidated statement of financial position, separately from the equity of the owners of the parent.

If African Iron loses control over a subsidiary, it: • Derecognises the assets (including goodwill) and liabilities of the subsidiary; • Derecognises the carrying value of any non-controlling interest; • Derecognises the cumulative translation differences recorded in equity; • Recognises the fair value of the consideration received; • Recognises the fair value of any investment retained; • Recognises and surplus or deficit in the statement of comprehensive income; • Reclassifies the parent’s share of components previously recognised in other comprehensive income to profit or loss.

C) TRADE AND OThER RECEIVAbLES

Trade receivables are recognised initially at fair value and subsequently measured at amortised cost using the effective interest method, less provision for impairment. Trade receivables are generally due for settlement within 30 days. They are presented as current assets unless collection is not expected for more than 12 months after the reporting date.

Collectability of trade receivables is reviewed on an ongoing basis. Debts which are known to be uncollectible are written off by reducing the carrying amount directly. An allowance account (provision for impairment of trade receivables) is used when there is objective evidence that the group will not be able to collect all amounts due according to the original terms of the receivables. Significant financial difficulties of the debtor, probability that the debtor will enter bankruptcy or financial reorganisation, and default or delinquency in payments (more than 30 days overdue) are considered indicators that the trade receivable is impaired. The amount of the impairment allowance is the difference between the asset’s carrying amount and the present value of estimated future cash flows, discounted at the original effective interest rate. Cash flows relating to short-term receivables are not discounted if the effect of discounting is immaterial.

The amount of the impairment loss is recognised in profit or loss within other expenses. When a trade receivable for which an impairment allowance had been recognised becomes uncollectible in a subsequent period, it is written off against the allowance account. Subsequent recoveries of amounts previously written off are credited against other expenses in profit or loss.

D) INCOmE TAx

Current TaxCurrent tax is calculated by reference to the amount of income taxes payable or recoverable in respect of the taxable profit or tax loss for the period. It is calculated using tax rates and tax laws that have been enacted or substantively enacted by reporting date. Current tax for current and prior periods is recognised as a liability (or asset) to the extent that it is unpaid (or refundable).

Deferred TaxDeferred tax is accounted for using the comprehensive balance sheet liability method in respect of temporary differences arising from differences between the carrying amount of assets and liabilities in the financial statements and the corresponding tax base of those items.

In principle, deferred tax liabilities are recognised for all taxable temporary differences. Deferred tax assets are recognised to the extent that it is probable that sufficient taxable amounts will be available against which deductible temporary differences or unused tax losses and tax offsets can be utilised. However, deferred tax assets and liabilities are not recognised if the temporary differences giving rise to them arise from the initial recognition of assets and liabilities (other than as a result of a business combination) which affects neither taxable income nor accounting profit. Furthermore, a deferred tax liability is not recognised in relation to taxable temporary differences arising from goodwill.

Annual Report for the Year Ended 30 June 2011 23

AFRICAN IRON LTDNOTES TO FINANCIALSTATEmENTSFOR THE YEAR ENDED 30 JUNE 2011

For

per

sona

l use

onl

y

Deferred tax liabilities are recognised for taxable temporary differences arising on investments in subsidiaries, branches, associates and joint ventures except where the Group is able to control the reversal of the temporary differences and it is probable that the temporary differences will not reverse in the foreseeable future. Deferred tax assets arising from deductible temporary differences associated with these investments and interests are only recognised to the extent that it is probable that there will be sufficient taxable profits against which to utilise the benefits of the temporary differences and they are expected to reverse in the foreseeable future.

Deferred tax assets and liabilities are measured at the tax rates that are expected to apply to the period(s) when the asset and liability giving rise to them are realised or settled, based on tax rates (and tax laws) that have been enacted or substantively enacted by reporting date. The measurement of deferred tax liabilities and assets reflects the tax consequences that would follow from the manner in which the Group expects, at the reporting date, to recover or settle the carrying amount of its assets and liabilities.

Deferred tax assets and liabilities are offset when they relate to income taxes levied by the same taxation authority and the Company/Group intends to settle its current tax assets and liabilities on a net basis.

The Group has implemented the tax consolidation legislation. As a consequence, the members of the tax consolidated group are taxed as a single entity and the deferred tax assets and liabilities of these entities are set off in the consolidated financial statements.

Current and deferred tax for the period

Current and deferred tax is recognised as an expense or income in the statement of comprehensive income except when it relates to items credited or debited directly to equity, in which case the deferred tax is also recognised directly in equity.

E) pROpERTy, pLANT AND EqUIpmENT

Property, plant and equipment is stated at historical cost less accumulated depreciation and any accumulated impairment losses. Cost includes expenditure that is directly attributable to the acquisition of the item. In the event that settlement of all or part of the purchase consideration is deferred, cost is determined by discounting the amounts payable in the future to their present value as at the date of acquisition.

Depreciation is calculated on a straight-line basis over the estimated useful life of the specific assets as follows:

Plant and equipment – over 6 years

The assets’ residual values, useful lives and amortisation methods are reviewed, and adjusted if appropriate, at each financial year end.

F) ExpLORATION AND EVALUATION ExpENDITURE

Exploration, evaluation and development expenditure incurred is accumulated in respect of each identifiable area of interest. These costs are only carried forward to the extent that they are expected to be recouped through the successful development of the area or where activities in the area have not yet reached a stage that permits reasonable assessment of the existence of economically recoverable reserves.

Accumulated costs in relation to an abandoned area are written off in full against profit in the year in which the decision to abandon the area is made.

When production commences, the accumulated costs for the relevant area of interest are amortised over the life of the area according to the rate of depletion of the economically recoverable reserves.

A regular review is undertaken of each area of interest to determine the appropriateness of continuing to carry forward costs in relation to that area of interest.

24 African Iron Limited and its controlled entities

AFRICAN IRON LTDNOTES TO FINANCIALSTATEmENTS (CONT)FOR THE YEAR ENDED 30 JUNE 2011

For

per

sona

l use

onl

y

G) INVESTmENTS & FINANCIAL INSTRUmENTS

Investments are recognised and derecognised on trade date where purchase or sale of an investment is under a contract whose terms require delivery of the investment within the timeframe established by the market concerned, and are initially measured at fair value, net of transaction costs.

Other financial assets are classified into the following specified categories: financial assets ‘at fair value through profit or loss’, ‘held-to-maturity’ investments, ‘available-for-sale’ financial assets, and ‘loans and receivables’. The classification depends on the nature and purpose of the financial assets and is determined at the time of initial recognition. The Group has the following financial assets:

i. Financial assets at fair value through profit or loss Shares and options held for trading have been classified as financial assets at fair value through profit or loss.

Financial assets held for trading purposes are stated at fair value, with any resultant gain or loss recognised in profit or loss. The fair value of investments that are actively traded in organised financial markets is determined by reference to quoted market bid prices at the close of business on the reporting date. Assets in this category are classified as current assets if they are expected to be realised within 12 months otherwise they are classified as non-current assets.

ii. Loans and receivables Loans and other receivables are non-derivative financial assets with fixed or determinable payments that are not

quoted in an active market. They are recorded at amortised cost less impairment. Impairment is determined by review of the nature and recoverability of the loan or receivable with reference to its terms of repayments and capacity of the debtor entity to repay the debt. If the recoverable amount of a receivable is estimated to be less than its carrying amount, the carrying amount of receivable is reduced to its recoverable amount. An impairment loss is recognised in profit or loss immediately. They are included in current assets, other than those with maturities greater than 12 months from reporting date which are classified as non-current assets.

Financial assets are derecognised when the rights to receive cash flows from the financial assets have expired or have been transferred and the Group has transferred substantially all the risks and rewards of ownership.

h) FOREIGN CURRENCy

Foreign currency transactions and balances

All foreign currency transactions occurring during the financial year are recognised at the exchange rate in effect at the date of the transaction. Foreign currency monetary items at reporting date are translated at the exchange rate existing at reporting date. Non-monetary assets and liabilities carried at fair value that are denominated in foreign currencies are translated at the rates prevailing at the date when the fair value was determined.

Exchange differences are recognised in the profit or loss in the period in which they arise except those exchange differences which relate to assets under construction for future productive use which are included in the cost of those assets where they are regarded as an adjustment to interest costs on foreign currency borrowings.

Functional and presentation currency

Items included in the financial statements of each of the companies within the Group are measured using the currency of the primary economic environment in which they operate (“the functional currency”). The consolidated financial statements are presented in Australian dollars, which is African Iron’s functional and presentation currency.

Annual Report for the Year Ended 30 June 2011 25

AFRICAN IRON LTDNOTES TO FINANCIALSTATEmENTS (CONT)FOR THE YEAR ENDED 30 JUNE 2011

For

per

sona

l use

onl

y

h) FOREIGN CURRENCy (CONT)

Group companies

The results and financial position of all the Group entities (none of which has the currency of a hyperinflationary economy) that have a functional currency different from the presentation currency are translated into the presentation currency as follows:

i. assets and liabilities for each Statement of Financial Position presented are translated at the closing rate at the date of that Statement of Financial Position;

ii. income and expenses for each statement of comprehensive income are translated at average exchange rates (unless this is not a reasonable approximation of the cumulative effect of the rates prevailing on the transaction dates, in which case income and expenses are translated at the dates of the transactions); and

iii. all resulting exchange differences are recognised in other comprehensive income.

On consolidation, exchange differences arising from the translation of any net investment in foreign entities are recognised in other comprehensive income. When a foreign operation is sold, a proportionate share of such exchange differences is reclassified to profit or loss, as part of the gain or loss on sale where applicable.

Goodwill and fair value adjustments arising on the acquisition of a foreign entity are treated as assets and liabilities of the foreign entities and translated at the closing rate.

I) ImpAIRmENT OF ASSETS

Goodwill and intangible assets that have an indefinite useful life are not subject to amortisation and are tested annually for impairment or more frequently if events or changes in circumstances indicate that they might be impaired.

Other assets are tested for impairment whenever events or changes in circumstances indicate that the carrying amount may not be recoverable. An impairment loss is recognised for the amount by which the asset’s carrying amount exceeds its recoverable amount. The recoverable amount is the higher of an asset’s fair value less costs to sell and value in use. For the purposes of assessing impairment, assets are grouped at the lowest levels for which there are separately identifiable cash inflows which are largely independent of the cash inflows from other assets or groups of assets (cash-generating units). Non-financial assets other than goodwill that suffered impairment are reviewed for possible reversal of the impairment at the end of each reporting period.

J) EmpLOyEE bENEFITS

Provision is made for benefits accruing to employees in respect of wages and salaries, annual leave and long service leave when it is probable that settlement will be required and they are capable of being measured reliably.

Provisions made in respect of employee benefits expected to be settled within 12 months are measured at their nominal values using the remuneration rate expected to apply at the time of settlement.

Provisions made in respect of employee benefits which are not expected to be settled within 12 months are measured as the present value of the estimated future cash outflows to be made by the Group in respect of services provided by employees up to the reporting date.

The liability for long service leave is recognised in the provision for employee benefits and measured as the present value of expected future payments to be made in respect of services provided by employees up to the reporting date.

26 African Iron Limited and its controlled entities

AFRICAN IRON LTDNOTES TO FINANCIALSTATEmENTS (CONT)FOR THE YEAR ENDED 30 JUNE 2011

For

per

sona

l use

onl

y

Share-based paymentsEquity-settled share-based payments are measured at fair value at the date of grant. Fair value is measured by use of the Black-Scholes option pricing model. The expected life used in the model has been adjusted, based on management’s best estimate, for the effects of non-transferability, exercise restrictions, and behavioural considerations.

The fair value determined at the grant date of the equity-settled share-based payments is expensed on a straight-line basis over the vesting period, based on the Group’s estimate of shares that will eventually vest.

For cash-settled share-based payments, a liability equal to the portion of the goods or services received is recognised at the current fair value determined at each reporting date.

K) TRADE AND OThER pAyAbLES

Trade and other payables represent liabilities for goods and services provided to the Group prior to the end of financial year which are unpaid. The amounts are unsecured and are usually paid within 30 days of recognition. Trade and other payables are presented as current liabilities unless payment is not due within 12 months from the reporting date. They are recognised initially at their fair value and subsequently measured at amortised cost using the effective interest method.

L) pROVISIONS

Provisions are recognised when the Group has a present obligation, the future sacrifice of economic benefits is probable, and the amount of the provision can be measured reliably.

The amount recognised as a provision is the best estimate of the consideration required to settle the present obligation at reporting date, taking into account the risks and uncertainties surrounding the obligation. Where a provision is measured using the cash flows estimated to settle the present obligation, its carrying amount is the present value of those cash flows.

When some or all of the economic benefits required to settle a provision are expected to be recovered from a third party, the receivable is recognised as an asset if it is virtually certain that recovery will be received and the amount of the receivable can be measured reliably.