2010.06.16 - holx - initiation at neutral gleacher

TRANSCRIPT

8/3/2019 2010.06.16 - HOLX - Initiation at Neutral Gleacher

http://slidepdf.com/reader/full/20100616-holx-initiation-at-neutral-gleacher 1/20

Healthcare: Medical Devices and Diagnostics

Hologic, Inc. ($14.80, Neutral)HOLX: In Search of the Elusive Growth; Initiating with a Neutral

Investment Opinion: Initiating coverage of HOLX with a Neutral rating.

Fiscal Year Sep Fi scal Year Calendar Year Last Qtr. Cur r. Qtr. N ext Qtr.

Revenue (Net) (Current)

Revenue (Net)(Previous)

F0 9A F 10E F1 1E

1.6B 1.7B 1.8B

— — —

C09A C10E C11E

1.6B 1.7B 1.8B

— — —

2Q10A

418.1

—

3Q10E

417.5

—

4Q10E

419.3

—

EPS (Current)

EPS (Previous)

1.17 1.17 1.30

— — —

1.15 1.20 1.33

— — —

0.29

—

0.29

—

0.30

—

P/S

P/E

2.3 2.3 2.1

12.6 12.6 11.4

2.3 2.2 2.1

12.9 12.3 11.1

—

—

—

—

—

—

SUMMARY: On the company side, 1) HOLX offers an attractive FCF yield (11%)2) a digital mammography replacement cycle and new products (HPV, Adianamay eventually help stabilize current sales declines, and 3) new opportunities (3Dtomo) are nearing. From a macro perspective, we do not favor a cap equipbusiness model in this environment, but the majority of sales today (~70%) arerecurring and non-capex, while HOLX has very little exposure O-US (20%). Whilethere are real issues – foremost being lack of growth – the current FCF yield andrecurring nature of sales in this economic environment may keep some floor undeshares at these levels; however, there is still very little reason to own.

• FCF Declining. While FY10 FCF guidance of “roughly $500M” is alreadbelow the prior year of $515M, our analysis yields FCF even lower at $414Mas last year’s working capital and capex reductions prove difficult to repeat

However, even our lower estimate translates to an 11% yield – attractiverelative to peers (slightly offset by a 2.4x debt/EBITDA).

• Mammography Troubles. In terms of digital mammo, the market (as seenvia MQSA data) has been consistently deteriorating. Monthly declines havepretty much continued since August, and the market is now annualizing aroughly 1,200 units. At ~60-65% share, that’s sub-800 units for HOLX thisyear, a y/y decline again despite an abysmal 2009. We model anothedouble-digit decline for mammo in FY10.

• Replacement Cycle Soon. A digital replacement cycle will eventually helpbut these systems are now replaced just every 8-10 years. Only 451 digitasystems were installed from 2000 and 2003, limiting contribution until ~2012The new 3D tomo may also help long-term – PMA filing in early 2011 – buthere is high risk the study design isn't enough and the eventual marke

opportunity ends up significantly smaller (more below).• Macro Perspective. Just 20% of sales are O-US (most from Europe), bu

HOLX does not hedge and thus is slightly exposed. A bigger issue may beEuropean government austerity measures and healthcare budget pressureslimiting mammo system sales in the last remaining growth region.

• Why Own? Lastly, newer products (HPV and Adiana) will not materiallycontribute to sales, so the end result is a struggle to keep sales flat (let alonegrow) for the next 12-24 months. FCF yield saves the day on the downsidebut it is hard to be supportive of the name in light of current growth issues.

June 16, 2010

Initiation of Coverage

Amit Hazan212-273-7272

Jeremy Feffer 212- [email protected]

Ticker: HOLX

Rating Neutral

Price $14.80

Price Target: NA

52-wk High/Low: $19.72–$12.52

Shares Out.(mil): 256.5

Market Cap (M): 3,796.9Enterprise Val.(M):

$4,862.0

Company Description:Hologic, Inc.develops, manufactures, anddistributes medical imaging systems,and diagnostic and surgical productsfor serving the healthcare needs of women. The company operates infour segments: Breast Health,Diagnostics, GYN Surgical, andSkeletal Health.

Q1 Q2 Q3 Q1 Q21012

14161820

2010

1 Year Price History for HOLX

Created by BlueMatrix

Please see important disclosure information on pages 19 - 20 of this report.

Gleacher & Company Securities, Inc.

8/3/2019 2010.06.16 - HOLX - Initiation at Neutral Gleacher

http://slidepdf.com/reader/full/20100616-holx-initiation-at-neutral-gleacher 2/20

KEY INVESTMENT HIGHLIGHTS

We are initiating coverage of Hologic, Inc. (HOLX) with a Neutral rating. On the company

side, the stock offers an attractive FCF yield (11%), a digital mammography replacemen

cycle and new products (HPV, Adiana) may eventually help stabilize current sales

declines, and new opportunities (3D Tomo) may support valuation. From a macroperspective, we do not favor a capital equipment business model in this environment, bu

the majority of sales today (approximately 70%) are actually recurring and non-capex

while HOLX has very little exposure O-US (20%). So there are real issues, foremost being

lack of growth, but the current FCF yield and recurring nature of sales in this economic

environment should keep some floor under shares at these levels, but there is very little

reason to own.

The Macro: Currency Exposure Relatively Limited

HOLX has relatively limited exposure to foreign currency volatility, as roughly 80% of 2009

revenue was generated in the U.S. and only 12% of sales came from Europe. A significan

portion of European revenue does come from sales of Selenia digital mammography

systems, so they are capital equipment in nature. We address the currency risks and

economic risks below.

On Currency Risk Because of the small O-US exposure, HOLX does not hedge any of its foreign currency

risk, and the company actually has some natural hedges in place through its

manufacturing operation in Germany and international offices that are denominated in

local currencies. Another limiting factor for HOLX is that the bulk of European sales come

from Germany, the United Kingdom, and the Netherlands, meaning that some of the

company’s European sales are denominated in the British pound, which has been slightly

more stable than the euro.

On Economic Risk However, while HOLX is somewhat insulated from the weakening euro, this crisis

threatens to pose an entirely separate set of risks, namely the tightening of fiscal budgets

throughout Europe. While the debt crisis has had the greatest impact on the so-called

PIIGS (Portugal, Ireland, Italy, Greece, Spain) countries, it is likely that most European

governments will adopt some austerity measures that will involve healthcare spending

cutbacks. In this case, capital equipment sales would seem to be at risk as hospitals eithe

delay purchases of large ticket items or push back on price. We do not view this as an

immediate risk, but it is something we will watch more closely in the second half of 2010

and early next year as European governments set fiscal 2011 budgets. For HOLX, this

trend bears monitoring, but we note again the company’s limited exposure relative to othe

capital equipment names.

Guidance Guarded…Growth Elusive

On their most recent fiscal 2Q10 earnings release, HOLX reiterated sales and EPS

guidance of $1.640-$1.665 million / $1.16-$1.20 as well as operating expense guidance o

$490-$500 million. Roughly speaking, the guidance looks achievable to us, which is both

positive and negative, one could say. Positive in that estimates for this year are no longe

ahead of reality, yet negative in that growth rates this year (a recovery year from almost al

other stocks in our space) remain very sluggish at 2% for sales and 1% for EPS.

Pag

Gleacher & Company Securities, I

June 16, 20Hologic, Inc. : In Search of the Elusive Growth; Initiating with a Neu

Gleacher & Company

8/3/2019 2010.06.16 - HOLX - Initiation at Neutral Gleacher

http://slidepdf.com/reader/full/20100616-holx-initiation-at-neutral-gleacher 3/20

Thus, one has to expect a rebound to occur in 2011 in order to believe stock appreciation

can happen from current levels (there is no dividend here). Street estimates do call fo

accelerating growth for sales (+5%) and EPS (+11%) next year, and this essentially

highlights our less than positive thesis on shares, as we simply cannot see where

the growth will come from.

Figure 1: FY10 Guidance Vs. Street Estimates

FY2010

Old Guidance New Guidance StreetTotal Sales ($ in millions) $1,640-$1,665 $1,640-$1,665 $1,670

Gross Margin1 62-63% 61-62%

Operating Expense1 $490-$500 $490-$500

Interest Expense $125 $125

EPS2 $1.16-$1.20 $1.16-$1.20 $1.18

Source: Company reports, Street estimates.

Free cash flow is another issue, a key metric for all bulls on this name. We think

sustainability even at historical levels (let alone growth) may be difficult for the foreseeable

future. FCF was $515 million in FY09 and is guided to roughly $500 million in FY10

(currently a 13% yield), a slightly more conservatively worded guidance than the “ove

$500 million” given earlier in the year. However, even the new mark seems unlikely to be

achieved. Investors should recall that FY09 FCF was aided by $53 million in working

capital improvements and a decline in capex from $53 million in FY08 to $31 million in

FY09. We think guidance will be missed here, as we do not foresee similar benefits this

year. The company has guided capex to $60 million for FY10. Our FCF, therefore, is

modeled at $414 million in FY10 (approximately 10.5% yield), which is a noticeable

decline y/y. What is also notable in this free cash flow discussion is that HOLX’s

debt/EBITDA levels of 2.5x remain well above peers.

To summarize, it is partly free cash flow and it is partly our concern with the lack of long-term visible growth in the overall business that causes us to remain neutral on HOLX. The

Street, on the other hand, seems to be more comfortable with the potential return to

growth that would be fueled by a digital mammography replacement cycle, new products

(HPV, Adiana), or future opportunities (3D Tomo). But, in our opinion, a closer review

indicates the market is expecting too much and each of these items may disappoint. We

therefore initiate at Neutral for these reasons.

Breast Health Remains the Segment in Focus – and isStill Struggling

The Breast Health segment represents 45% of total HOLX sales, and includes the Selenia

full-field digital mammography (FFDM) system, computer-aided detection (CAD)MammoSite targeted radiation therapy, Suros breast biopsy systems, the SecurView DX

breast imaging workstation, and the MammoPad breast cushion in addition to service

sales.

The key product in this segment is Hologic’s Selenia digital mammography system

However, sales have seen significant declines stemming from the U.S. hospital spending

crisis and the penetration of digital systems in the field. We take a look at each below, as

Pag

Gleacher & Company Securities, I

June 16, 20Hologic, Inc. : In Search of the Elusive Growth; Initiating with a Neu

Gleacher & Company

8/3/2019 2010.06.16 - HOLX - Initiation at Neutral Gleacher

http://slidepdf.com/reader/full/20100616-holx-initiation-at-neutral-gleacher 4/20

well as the possibility that a replacement cycle could re-fuel sales, although, we think it’s

too early.

The Hospital Spending Crisis The hospital spending crisis had a big impact on this business, and cost pressures faced

by hospitals contributed to a 26% decline in Selenia orders in the U.S. in FY09 and a 15%

decline worldwide.

HOLX has also been hurt by a product mix shift, as a higher percent of Selenias sold were

low end de-featured units or international units (sold at a approximate 20% discount to

U.S. ASPs), a trend that has continued through 2Q10 as higher units sales were offset by

lower ASPs y/y. Management expects product mix and ASPs to improve as the

replacement market picks up over the next 12-18 months, but for now, we estimate the

replacement market for 2D digital is roughly 5% versus a normalized 10-15% as hospitals

continue to extend the life of capital equipment by delaying new purchases/upgrades.

Indeed, our spring 2010 survey of hospital CFOs (n=30) indicated that the average

replacement cycle for mammography equipment has increased from under seven years

(three years ago), to almost eight years currently. For hospitals in a position to increase

capex spending, many are catching up on purchases and projects delayed during the

worst of the crisis, and even those reinvesting in capital equipment, mammography is

typically a relatively low priority (it consistently places below MRI, CT, and Radiation

Therapy Machines in our quarterly surveys). Therefore even a stronger rebound in

hospital capital spending does not necessarily point to a sharp rebound in digita

mammography orders.

On the Tail End of a Product Cycle The FDA’s well kept monthly published MQSA data continues to be a close indicator of

digital mammography installations, and it carries a worrying sign. MQSA data released on

June 1st by the FDA indicated May 2010 rose sequentially for just the second month ou

of the last 10, as FFDM unit installations came in at 119 for the month, still near a multi-

year low (see chart below). The market is annualizing at roughly 1,200 units for 2010. Atapproximately 60-65% share, that is sub-800 units for HOLX this year, a y/y decline again

despite an abysmal 2009. In addition, the increase in the number of facilities with at leas

one FFDM unit (74) also posted a multi-year low. Both of these data points indicate that

the market still has not yet reached bottom. We expect another 21% worldwide sales

decline for mammography in FY10.

Pag

Gleacher & Company Securities, I

June 16, 20Hologic, Inc. : In Search of the Elusive Growth; Initiating with a Neu

Gleacher & Company

8/3/2019 2010.06.16 - HOLX - Initiation at Neutral Gleacher

http://slidepdf.com/reader/full/20100616-holx-initiation-at-neutral-gleacher 5/20

Figure 2: Monthly Increase in FFDM Unit Installations

80

100

120

140

160

180

200

220

240

Jul-08 Sep-08 Nov-08 Jan-09 Mar-09 May- 09 Jul-09 Sep-09 Nov-09 Jan- 10 Mar-10 May-10

Source: FDA

Replacement Market Remains a Few Years Out Those more positive on HOLX will tend to believe that MQSA data is becoming

increasingly inaccurate in predicting digital mammography sales, as it will not capture the

digital replacement cycle to come (i.e., digital replacement of digital, as MQSA only tracks

new digital units installed). We provide some context herein to refute the idea that a digita

mammography replacement cycle could help fuel growth any time in the near future.

First, note that digital mammography systems are generally replaced every 8-10 years

and today that replacement cycle is clearly weighted toward the longer end. A total of 451

systems were installed from 2000-2003, a vast majority of which were GE units. Marke

share for digital mammo tends to be sticky, as GE has had better success retaining digita

customers than it did with analog (these are the customers that remained with GE early

on, their best customers). As a result, we believe HOLX will be challenged to exceed 20-

30 replacement units annually any time soon.

Furthermore, a more significant ramp in unit installations occurred in 2004 and 2005, with

an enormous jump in 2006 (see chart below). This tells us that the real pickup in

replacement demand is still 3-5 years away.

Pag

Gleacher & Company Securities, I

June 16, 20Hologic, Inc. : In Search of the Elusive Growth; Initiating with a Neu

Gleacher & Company

8/3/2019 2010.06.16 - HOLX - Initiation at Neutral Gleacher

http://slidepdf.com/reader/full/20100616-holx-initiation-at-neutral-gleacher 6/20

Figure 3: US FFDM System Installations 2000-2006

100 145 171

327382

35

930

0

100

200

300

400

500

600

700

800

900

1000

2000 2001 2002 2003 2004 2005 2006

Source: FDA, AuntMinnie.com, Gleacher & Co. Estimates Installation estimates include all competitors in the U.S. market (GE, Fisher Imaging, and Hologic

3D Tomosynthesis (Tomo) Remains the Missing Great Hope HOLX has long been developing a new digital mammography product platform known as

tomosynthesis, which is a 3D breast screening/imaging tool that is expected to

significantly improve breast screening technology. Tomosynthesis images take the 11

angles used by x-ray and reconstruct them into layered, 3D image slices. Not only can

tomosynthesis capture better, more defined images, but it can also do this using less

radiation and in the same compression time. Since the image has reduced tissue overlap

and structure noise and can be viewed in a ciné loop, it is likely that radiological readings

will get faster after the learning curve is reached.

Gaining FDA approval for this technology, however, has been an insurmountable obstacle

thus far. It was only one year ago (May 2009) that HOLX announced critical doubts over

whether the FDA, as presently constituted, would grant 3D Tomo approval given existing

data and clinical studies. This was due to two key criticisms from the FDA:

1. Reducing recall rate alone isn’t enough, and clear improvement in sensitivity is

paramount. The FDA apparently had a problem using ROC as the way o

assessing performance, calling into question whether a reduction in recall rate

alone is enough to gain approval. The oddity here is that this was the FDA’s

request when the study was originally designed. The focus thus shifts to

sensitivity and the ability to better detect cancers than 2D alone.

2. 3D Tomo stand-alone data (not 2D+3D) is what is needed. Again, this was a

turnaround of sorts for the FDA and seems to us like an illogical request

considering the practical necessity for a radiologist to view both the 2D and the

new 3D image. Comparison of historical images also demands a new 2D image

to be available, so we are unsure why the FDA would now seek this route. But

apparently the FDA saw this as an issue, at least to some extent, because

radiologists in the study looked at an enriched set of data (with 2D as well).

Pag

Gleacher & Company Securities, I

June 16, 20Hologic, Inc. : In Search of the Elusive Growth; Initiating with a Neu

Gleacher & Company

8/3/2019 2010.06.16 - HOLX - Initiation at Neutral Gleacher

http://slidepdf.com/reader/full/20100616-holx-initiation-at-neutral-gleacher 7/20

Despite delays, 3D Tomo is still the absolute key opportunity for HOLX, but the

environment remains unfortunate. At the Radiological Society of North America (RSNA)

conference last December, the number of presentations and workshops for 3D Tomo was

higher than in prior years, and we perceived that physician confidence actually remained

strong for the product despite the regulatory setbacks. Yet the FDA today still seems as

timid and confused as ever on all things related to mammography.

HOLX is taking three different approaches in its current study (full-dose 3D+2D, half-dose

3D+2D, 3D alone) in the hope that one of them is acceptable. There seems to be

realization at HOLX that this new approximately 2,000 patients study (at ten locations) is

probably not enough to satisfy the FDA, but management is calculatingly taking its

chances that an FDA panel will be called and common sense will prevail. This appears to

be a risky approach to use, especially considering the recent radiation concerns at FDA

regarding other imaging modalities (radiation was a major concern for FDA in these

tomosynthesis studies).

But the show moves on. We expect enrollment to last most of 2010, with a PMA filed by

late 2010 / early 2011. An FDA panel would most likely take place sometime in 2011. Of

course, there remains significant risk that HOLX’ study design will not be enough, bu

even if it is, the most likely approval in 2011 would be for “diagnostic” (not screening)which would be a much smaller market opportunity, at least that is what the FDA and

management have voiced.

To complicate matter further, the FDA has transitioned its Radiological Devices Branch

from the Office of Device Evaluation (ODE) to the Office of In Vitro Diagnostic Device

Evaluation and Safety (OIVD). The move is aimed at easing tensions between the two

departments over how in vitro and in vivo diagnostics have been handled at the FDA. The

practical impact to HOLX should be neutral to slightly negative, however, as mos

personnel have moved over to OIVD, and are the same people who handled the 3D Tomo

process last year.

Theoretical Market is Large, But Would Take Time. When and if approved, it is

important to note that the main driver for tomosynthesis adoption will still be robust clinica

data and reimbursement. In the conversion from analog to digital earlier in the decade, fo

example, a significant clinical study (DMIST, September 2005) including nearly 50,000

women was the catalyst needed to get penetration off the ground. The Tomo trial is

significantly smaller, but the market opportunity is smaller than the analog to digital switch

Our best estimation for addressable U.S. facilities who might acquire 3D Tomo in the early

years is about 900, which includes leading teaching institutions (about 400) and “early

adopter” high volume facilities (urban-based hospitals with 400+ beds). At about 1.5 units

per average MQSA facility, this is an addressable “early adopter” opportunity of roughly

1,500 units.

We also note that the Tomo component is mainly software and carries gross margins in

the 90% range. At roughly $100-$150k ASP, and considering the estimated unit ordersthis could be a meaningful opportunity to both top and bottom line, assuming HOLX wins

full diagnostic and screening approval.

MammoSite Losing Steam MammoSite, a balloon catheter used in radiation therapy for breast cancer treatment, has

seen sales growth steadily fall over the last several quarters, culminating in a 7% decline

over the last twelve months by our estimation. HOLX has been losing share to SenoRx

which makes the EnCor breast biopsy system, the Gel Mark line of breast tissue markers,

Pag

Gleacher & Company Securities, I

June 16, 20Hologic, Inc. : In Search of the Elusive Growth; Initiating with a Neu

Gleacher & Company

8/3/2019 2010.06.16 - HOLX - Initiation at Neutral Gleacher

http://slidepdf.com/reader/full/20100616-holx-initiation-at-neutral-gleacher 8/20

and the Contura balloon catheter (MammoSite’s largest competitor). SenoRx was recently

acquired by C.R. Bard, putting a larger sales and marketing effort behind the product. We

expect MammoSite to continue to lose share.

Added through the 2007 acquisition of Cytyc, MammoSite is a targeted radiation therapy

for breast cancer treatment. After the cancer tumor is removed via lumpectomy, the

MammoSite balloon is attached to a catheter and inserted into the lumpectomy cavity. Theballoon is inflated with a saline solution to fit in the cavity, and following treatment planning

with the radiation oncologist, the radiation seed is inserted through the catheter. The seed

is removed once the therapy is complete, and this process is repeated over a five-day

period. Following the fifth treatment, the balloon and catheter are removed.

Suros Stable The newest product in the breast biopsy segment is Eviva (launched in 2008), which is the

first completely integrated biopsy solution that offers features not available in legacy

stereotactic biopsy devices. While Eviva has increased market share, management noted

on the 2Q10 earnings call that a reduction in mammography volumes has led to a

reduction in breast biopsy procedures, due mainly to continued high unemployment and a

resetting of deductibles and co-pays. Growth in this product segment will depend on

improvements in macroeconomic trends, so this will bear watching going forward.

HOLX launched its breast biopsy business with the 2006 acquisition of Suros, a

manufacturer of minimally invasive interventional products for breast biopsy, tissue

removal, and biopsy site marking. Its technology, which includes a patented fluid

management system, allows the removal of tissue or biopsy samples in a fast, safe, and

simple manner using stereotactic x-ray, ultrasound, and MRI systems. Suros designs

manufactures, and markets patient-focused and physician-inspired “Compassionate

Technologies” through its Automated Tissue Excision and Collection (ATEC) product line

including percutaneous, automatic vacuum-assisted breast biopsy collection systems, a

disposable handpiece used to collect samples, and biopsy sit markets. The ATEC line

offers three units, each providing fast and easy biopsy capabilities: the Sapphire (all-in

one biopsy system), the Emerald (MRI-only system), and the Pearl (mainly stereotactic x-

ray and ultrasound).

Service is a Rare (and Solid) Positive The sole source of growth in the Breast Health segment over the last several quarters has

been service revenue, which has grown as the installed base has increased and as

hospitals delay purchasing new systems. One of the consequences of the hospita

spending crisis has been that average replacement cycles for many large capita

equipment items have lengthened, especially digital mammography. While capita

spending budgets have begun to recover somewhat, many hospitals are still faced with

the challenge of prioritizing spending and catching up on projects put on hold as spending

was frozen. Hospitals therefore continue to delay purchasing replacement units, investing

instead on service and maintenance of existing units. This helped mitigate order

weakness for HOLX over the last several quarters and is expected to continue to do soover the rest of 2010. Service, however, carries lower a gross margin (approximately 38%

in the March 2010 quarter), which, while significantly improved over the last several years

is still lower than product gross margin.

Pag

Gleacher & Company Securities, I

June 16, 20Hologic, Inc. : In Search of the Elusive Growth; Initiating with a Neu

Gleacher & Company

8/3/2019 2010.06.16 - HOLX - Initiation at Neutral Gleacher

http://slidepdf.com/reader/full/20100616-holx-initiation-at-neutral-gleacher 9/20

Diagnostics Division – Can Expectations Be Met?

The diagnostics division represents 34% of total company sales. The bread and butter o

this division remains liquid-based Pap (LBP) testing, an approximately $250 million annua

U.S. business for Hologic (which has about 70% of the market). This business is mature

and no longer grows, but has been a steady cash flow generator for the company. Growth

if any, for the division will have to come from either the new Cervista HPV testing platformor the automated imager (related to Pap). Our view is that Cervista HPV will struggle to

convert large accounts due to platform limitations in automation, and that imager growth

has now reached an end. At best, we see growth in this division being in the mid to single

range, and believe secular changes in Pap testing may put a great deal of pressure on

growth in the long term.

HPV Platform Needs to Start Contributing HOLX’ acquisition of Third Wave in 2008 brought with it the Cervista HPV and Invade

chemistry technology. HOLX received FDA approval for all three HPV markets (primary

secondary, and genotyping) for Cervista in March 2009, making it the second entrant in

the U.S. market after Qiagen’s Hybrid Capture 2 (HC2) – who continues to have a near

monopoly over the U.S. market. The QGEN test is supported by a significant amount ofclinical data, which is viewed as a positive, but there is plenty of data to suggest that

Cervista is at least equivalent. Cervista was officially launched toward the end of FY2009

and management estimates that market share is approaching 10% in the U.S.

Advantages of Invader Platform Outweighted by Lack of Automation. One of the

advantages of Cervista HPV on the Invader platform is its claim that less volume of pap

sample is required for performing its HPV test (versus Qiagen's), which reduces the

percentage of "quantity not sufficient" (QNS) samples that need to be re-done; these are

time consuming and more expensive for the lab. To be specific, both Qiagen’s HC2 and

Hologic’s Invader require a minimum amount of the liquid cytology following the liquid-

based Pap. Hologic's advantage is that Invader requires half that amount (2mm versus

4mm for HC2). Our discussions with industry contacts over the past few years support this

claim, and show that QNS for Qiagen can be as high as 5% of samples. This issue has adirect relationship with the possible occurrence of false negative readings that could be a

direct result of insufficient sample cellularity.

Cervista also has an internal control mechanism that minimizes the insufficient sample

issue before it is read as an actual result. This is a feature unique to Invader. The interna

control enables the lab to differentiate between a negative test and a negative reading due

to insufficient amount of cervical cells.

The problem, as we see it, is that the Invader platform is currently only approved as a

manual process (versus semi-automatic for QGEN), so high-volume labs would have to

buy other automation equipment to competitively run the Invader platform. Both

companies have been working on fully automated platforms that should be out in the nex

1-2 years. To first consider the Qiagen assay, the reason it is not capable of fulautomation today is sample processing, or the upfront naturation step, which is stil

manual. This alone can be an incredibly time-consuming process step. Alternatively, righ

now the Invader assay is sold totally manual. Therefore, what a lab could do is automate

the process via third-party equipment. The first part of this would be to use an automated

extraction system, such as EasyMAG from BioMerieux, among others, and then the

pipetting can be automated via Hamilton equipment or the like. One problem is that once

the lab automates with third-party equipment, it is going outside of the FDA-cleared

protocols, which means the lab has to do extensive validations for the procedure. HOLX

Pag

Gleacher & Company Securities, I

June 16, 20Hologic, Inc. : In Search of the Elusive Growth; Initiating with a Neu

Gleacher & Company

8/3/2019 2010.06.16 - HOLX - Initiation at Neutral Gleacher

http://slidepdf.com/reader/full/20100616-holx-initiation-at-neutral-gleacher 10/20

says a more automated system is forthcoming later in the year, but we continue to see this

issue as a significant limitation on share gains.

Genotyping May Become a Key Advantage. There were no FDA products approved in

the U.S. for genotyping prior to Hologic, making this a key differentiator. In general, HPV

genotyping will enable physicians to diagnose specific HPV types and to better assess the

risks associated with the specific HPV types (i.e., high vs. low-risk). Specifically, types 16and 18 are believed to occur in nearly 70% of all cervical cancer cases. In thinking about

this opportunity, we divide the genotyping market into three servable sub-markets: 1) Pap

negative/ HPV positive supplemental testing; 2) women under the age of 30; and 3)

testing to determine whether one of the HPV vaccines (which are specifically agains

subtypes 16 and 18) is appropriate. We are not sure yet how the reimbursement for the

labs would work, but it seems intuitive to us that genotyping would potentially garne

additional testing reimbursement in time.

In the first segment, we think genotyping would be performed on all samples that yield

negative Pap results and positive HPV results, so that a determination can be made as to

whether further diagnosis is necessary. We estimate this result comes up only about 3%

of the time for all combination Pap/HPV tests, or about 300-400k tests annually in the U.S

right now (and a one million test addressable market). Assuming the ASP is the same asthe screening test ($19), that translates to an annual U.S. potential market size of $20

million.

Second, the specific information in genotyping may open up the opportunity for HPV

testing of cancer-causing types (16 and 18 most likely) in women under 30. Currently

ACOG guidelines recommend HPV testing for women over 30, as many benign strains o

HPV common in younger women resolve on their own before this age. Lowering the

recommended age by two years could increase the screening volume by nearly 2.5 million

tests, as the compliance with screening guidelines increases with younger age. This

change in recommended age guidelines could add over $50 million in annual market size

for each two years the screening age is lowered.

Third, with such a high prevalence of HPV in the young population, it may be of value to

test for type 16 and 18 prior to or after the administration of the HPV vaccine; Merck’s

Gardasil vaccinates against type 16 and 18. This may not become standard practice, bu

could add incremetal volume. Both Qiagen and Roche are working on an HPV genotyping

capability, but neither product will likely make it to market until late 2010/2011.

U.S. Secondary Screening Market. We estimate that of the roughly 60 million Pap

smears performed annually in the U.S., about 6% result in atypical squamous cells o

undetermined significance (ASCUS) classification and are candidates for an HPV test

This is what we define as the "secondary" HPV opportunity. At an estimated ASP of $19

we peg the current U.S. market opportunity for equivocal Paps at $60 million (we assume

a maximum of 90% penetration). Currently, we believe about 82% of this market is already

penetrated by existing HPV tests. Importantly, the Hologic PMA approval should allow itsnew HPV test to be used with any liquid-based pap smear test, including Hologic's

ThinPrep and Becton Dickinson’s SurePath, an advantage over QGEN's offering, which is

only approved from Cytyc's sample vial.

U.S. Primary Screening Market. The U.S. primary screening market opportunity is much

larger at approximately $645 million, derived as follows: of the 60 million Pap

examinations performed each year in the U.S., there are approximately 33 million exams

associated with women over the age of 30 (for whom the HPV test is indicated), and we

estimate an ASP of roughly $19 (the same as QGEN's product today). This market wil

Page

Gleacher & Company Securities, I

June 16, 20Hologic, Inc. : In Search of the Elusive Growth; Initiating with a Neu

Gleacher & Company

8/3/2019 2010.06.16 - HOLX - Initiation at Neutral Gleacher

http://slidepdf.com/reader/full/20100616-holx-initiation-at-neutral-gleacher 11/20

possibly be further decreased by two occurrences. First, ASPs will eventually decline due

to competitive dynamics entering the market, and $15 may be a more accurate long-term

price to use. This would have the effect of reducing the long-term addressable U.S

primary market to $500 million. We feel this is an accurate long-term market number.

Second, ACOG guidelines suggest HPV tests be administered once every three years (if

the test results are negative). In theory, some will argue that the 30 million annual Papexams performed are only one-third of that size (10 million annual exams for three years)

We do not take that view. We do not believe that testing intervals will change very much

during the next several years, and we highlight the following observations as to why: 1)

Women today in the U.S. are on average getting their annual check-ups (and annual Pap

exams) every 19 months, so the testing interval is already well beyond one year. 2)

Current reimbursement for HPV testing does not carry any limitation of insuring only one

exam every three years when results are negative. As long as the insurance companies

are paying, we feel doctors will prescribe the test. 3) Physicians could face significant

liability for not examining a patient on an annual visit. 4) Patients change jobs, move

geographically, or switch insurance carriers, and holding someone to testing once every

three years would be very difficult. For these reasons, we do not decrease our estimate o

the primary market opportunity for a widening of testing intervals.

ThinPrep Pap Testing in a Secular Decline ThinPrep is HOLX’ liquid-based Pap test for cervical cancer screening that is also

approved for HPV, gonorrhea, and Chlamydia. The ThinPrep Imager provides a screening

review of the ThinPrep test vial, highlighting cells of interest for the cytotechnologist to

examine upon second review.

Last November (2009), the American College of Obstetricians and Gynecologists (ACOG)

released new screening guidelines for Pap testing with three key recommendations: 1)

Women should have their Pap screening beginning at age 21 2) Women age 21-30 should

be screened biannually rather than annually and 3) Women age 30 and over should have

a Pap or cytology screening every 2-3 years if they have three consecutive negative Pap

tests. Results from our recent women’s health survey indicated that fewer OB/Gyn’s

reported recommending Pap tests for low risk patients on a regular basis. In our spring

survey, 41% of respondents said testing intervals depend on age or other risk factors, up

from 26% last quarter. The figure was 23% for high risk patients, versus 13% in Decembe

2009.

Going forward, we expect Pap volumes to decline as HPV testing continues to gain share

as a primary screening tool. This is a negative for the ThinPrep Pap Test but theoretically

a positive for Cervista HPV if it were to grab market share. However, we remain less

optimistic that market share can be won easily (even with the more automated platform

tentative mid-2010 release), but do believe small lab contracts are out there to be won. In

addition, Imager, which is already more than 70% penetrated in the U.S., is not expected

to grow significantly going forward.

Gyn Surgical Growth Remains Positive

The Gyn Surgical (16% of total revenue) consists primarily of two products: NovaSure, the

endometrial ablation device used to treat excessive menstrual bleeding, and Adiana, the

permanent contraception device that competes directly with CPTS’ Essure. While Adiana

is still in the early stages of it full launch, NovaSure has been a steady grower for HOLX,

and the next generation product has been fully rolled out.

Page

Gleacher & Company Securities, I

June 16, 20Hologic, Inc. : In Search of the Elusive Growth; Initiating with a Neu

Gleacher & Company

8/3/2019 2010.06.16 - HOLX - Initiation at Neutral Gleacher

http://slidepdf.com/reader/full/20100616-holx-initiation-at-neutral-gleacher 12/20

NovaSure Stable HOLX added its Gyn Surgical segment through the 2007 acquisition of Cytyc. Cytyc’s

flagship product is NovaSure, which serves as a minimally invasive alternative to a

hysterectomy. Excessive menstrual bleeding affects an estimated seven million women

and the company believes that endometrial ablation could be a $1.5 billion opportunity in

the U.S.; NovaSure generated revenue of approximately $250 million in the U.S. in

FY2009. The advantage of endometrial ablation is that it serves as a permanent cure andcan be performed in a doctor’s office in 5-10 minutes with a relatively short recovery time.

HOLX sees two drivers of growth for NovaSure in the U.S., making it easier to perform the

procedure in the doctor’s office and increasing awareness of the procedures among

women. On the physician side, HOLX is working with doctors on such issues as

reimbursement, process flow, and anesthesia to make the in-office procedure more

efficient and effective. As for patient awareness, the company is set to launch a campaign

aimed at educating women on the existence of endometrial ablation as a lower-cost, less-

invasive alternative to hysterectomy. This is important, as there are a number of

competitive products on the market, including Bayer’s Mirena for menorrhagia, Ferring’s

Lysteda, and Boston Scientific’s Genesys HTA endometrial ablation system.

In our recent gynecologist survey, 67% (n=111) indicated that they perform endometria

ablation procedures. Among their patients, 46% of excessive menstrual bleeding patients

are candidates for endometrial ablation and of those candidates, 33% currently receive

this procedure. Somewhat positively, our doctors believe that 35% of these candidates wi

receive endometrial ablations, a good sign for future growth/penetration.

Figure 4: % of Candidates Received Endometrial Ablation

Today In One Year

Average 33.2% 35.4%

Median 25.0% 30.0%

High 90.0% 90.0%

Low0.0% 0.0%

Source: Gleacher & Co. Survey Results

Among doctors who expect volume to change over the next year, 38% attribute the

change to increased patient awareness, while 33% said an improvement in the economy

increase in the number of insured and 21% cited easier access to the procedure (i.e.

more in-office procedures).

Figure 5: Reasons for Change in EA Patients

Responses % of Total

Patient Awareness 16 38%

Easier Access 9 21%

Number of Insured 8 19%

Economy 6 14%

Physician Experience 3 7% Source: Gleacher & Co. Survey Results

Page

Gleacher & Company Securities, I

June 16, 20Hologic, Inc. : In Search of the Elusive Growth; Initiating with a Neu

Gleacher & Company

8/3/2019 2010.06.16 - HOLX - Initiation at Neutral Gleacher

http://slidepdf.com/reader/full/20100616-holx-initiation-at-neutral-gleacher 13/20

U.S. growth has been driven by increased adoption of NovaSure as an office-based

procedure, increasing patient awareness, and on a large portion of the business from

standing monthly order agreements. NovaSure is key for HOLX because Adiana’s (see

below) launch is targeting physicians who already perform the NovaSure procedure. We

model 3.5% sales growth and 3.5% unit growth for NovaSure in CY2010, which may be

conservative.

Adiana – Small Share Gains Near Since the limited launch of Adiana in July of last year, very few Adiana procedures have

been performed. But the scope of the launch increased through the March 2010 quarter

and we believe that HOLX reached full launch by late February / early March. Indeed

management indicated on the 2Q10 earnings call that the full sales team is focused on

training doctors and selling the device.

The overall strategy is to partner with gynecologists to advance in-office utilization of both

NovaSure and Adiana and to drive patient awareness of both procedures as compelling

alternatives to existing options. The U.S. market opportunity for permanent sterilization is

frequently sized at the roughly 700,000 tubal ligations performed annually (based on data

from 2004), but we are more cautious regarding the actual addressable market. We

consider a few mitigating factors:

• To begin with, about 100,000 of the tubal ligations performed each year are done

in conjunction with a caesarian birth, as the procedure can be performed through

the incision already made; these procedures should be excluded from the

opportunity. A large increase in the number of C-sections in the U.S. has been

increasingly highlighted in publications and news reports recently, and it is likely

that the number is much higher today.

• Additionally, ACOG statistics indicate that nearly half of all tubal ligations are

performed postpartum (1-2 days after birth) when the still-enlarged uterus

presses the fallopian tubes up, just under the abdominal wall. A small 1/2- to 1-

inch incision through the relaxed abdominal wall is all that is required for a docto

to complete a tubal in this state, and the procedure takes only around 30 minutes

and generally does not lengthen the mother’s hospital stay.

• Lastly, intra-uterine devices like Mirena and Paragard have seen resurgence in

growth in recent years, and the addressable patient population for these devices

has a large overlap with Essure and Adiana.

If we solely consider caesarian and postpartum tubal ligations in our market calculation, it

leaves a more realistic annual addressable procedure market of roughly 300,000

Essure’s current ASP is just over $1,350, but we expect that to drop to just over $1,000-

$1,100 in the longer term (due to competitive pressures), suggesting that the rea

addressable market at full penetration is around $300-$350 million.

As for Adiana’s opportunity, there are roughly 89,000 Essure procedures performed each

year, but HOLX believes it can pick up some share by touting Adiana’s compatibility with

NovaSure. While the product is still very much in its early ramp, management believes

that it achieved high-single digit market share in the March 2010 quarter.

Early marketing efforts appear to have taken hold, as 55% of respondents to our spring

Women’s Health Survey said they were familiar with Adiana, including 75% of Essure

users. Across the entire survey population, gynecologists are forecasting 5% Adiana

Page

Gleacher & Company Securities, I

June 16, 20Hologic, Inc. : In Search of the Elusive Growth; Initiating with a Neu

Gleacher & Company

8/3/2019 2010.06.16 - HOLX - Initiation at Neutral Gleacher

http://slidepdf.com/reader/full/20100616-holx-initiation-at-neutral-gleacher 14/20

market share in six months and 7% share in 12 months. Note below that both Essure and

Adiana are seen to be taking share away from tubal ligation, albeit at a rather slow rate

compared to historical gains.

Figure 6: Permanent Contraception Procedure Share – Among All Respondents

Survey Date Sep 09 Dec 09 Mar 10

Current 6 Months 12 Months Current 6 Months 12 Months Current 6 Months 12 Months

Tubal ligation 68.5% 62.5% 58.9% 75.1% 69.2% 67.0% 65.5% 61.6% 58.6%

Essure 31.1% 34.2% 36.8% 23.7% 26.8% 27.0% 20.9% 24.3% 25.0%

Adiana 0.4% 3.3% 4.3% 1.2% 4.0% 6.1% 3.4% 5.1% 7.1%

Other 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 10.2% 9.1% 9.3%

Source: Gleacher & Co. Survey Results

Inside these numbers, however, if we focus only on those doctors who currently perform

Essure procedures, then Adiana’s market share looks better - with 6% share in six months

and 9% in 12 months (again, still including tubal ligations).

Figure 7: Permanent Contraception Procedure Share – Among Current Essure Users

Survey Date Sep 09 Dec 09 Mar 10

Current 6 Months 12 Months Current 6 Months 12 Months Current 6 Months 12 Months

Tubal ligation 43.3% 38.9% 36.2% 54.7% 49.0% 45.7% 53.9% 50.9% 48.9%

Essure 56.0% 56.4% 58.1% 43.1% 44.8% 44.6% 40.0% 41.0% 39.9%

Adiana 0.8% 4.7% 5.7% 2.2% 6.2% 9.7% 3.7% 5.9% 8.7%

Other 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 2.4% 2.2% 2.6%

Source: Gleacher & Co. Survey Results

If we focus solely on the two permanent sterilization devices, we see Adiana taking more

meaningful share away from Essure, going from 8% of procedures currently to 13% in sixmonths and 18% in 12 months.

Figure 8: Permanent Sterilization Procedure Share – Essure/Adiana Market Segment Only

Survey Date Sep 09 Dec 09 Mar 10

Current 6 Months 12 Months Current 6 Months 12 Months Current 6 Months 12 Months

Essure 98.7% 92.3% 91.0% 95.2% 87.8% 82.2% 91.6% 87.3% 82.1%

Adiana 1.3% 7.7% 9.0% 4.8% 12.2% 17.8% 8.4% 12.7% 17.9%

Source: Gleacher & Co. Survey Results

So while the total permanent sterilization pie should grow as share is taken away from

tubal ligation, Adiana is expected to grab a bigger piece of that pie as more physicians are

trained and more units are placed. HOLX currently estimates that Adiana has already

achieved market share in the high single digits. For now, we model this opportunity

conservatively, as it will take a lot of training and marketing efforts to drive meaningfu

sales.

Page

Gleacher & Company Securities, I

June 16, 20Hologic, Inc. : In Search of the Elusive Growth; Initiating with a Neu

Gleacher & Company

8/3/2019 2010.06.16 - HOLX - Initiation at Neutral Gleacher

http://slidepdf.com/reader/full/20100616-holx-initiation-at-neutral-gleacher 15/20

Skeletal Health

The smallest of the four product segments at just 5% of total revenue, the Skeletal Health

business includes products for the screening and diagnosis of osteoporosis. Products in

this segment include the Discovery and Explorer bone densitometers, Mini C-arm low

intensity x-ray imaging system, an Extremity MRI system, and General Radiography

Skeletal Health sales totaled $95.5 million (-11% y/y) in FY2009 and $21.5 million in 2Q10(-6.7%). The declines have been attributed to generally weaker osteoporosis assessmen

and mini c-arm sales as hospital capex budgets and reimbursement challenges still make

this a difficult segment. Decreased demand has shifted the market toward the lower-end

bone densitometry systems that carry low ASPs. Management noted on the last earnings

call, however, that recent reimbursement changes for abundance cytometry systems are

more benign than expectations, which the company hopes should help drive some growth

We model another y/y decline in sales for FY2010 with limited growth thereafter.

VALUATION

HOLX trades at 11.0x CY11E EPS and 7.3x CY11E EV/EBITDA, both of which are below

the peer group market cap weighted averages of 13.0x and 7.9x. However, HOLX’ fla

sales and EPS growth justify the slight discount.

Where HOLX is most compelling is on a FCF basis, with a CY10E FCF yield of 10.5%

versus the peer group’s market cap weighted average of 7.5%. Mitigating FCF yield

somewhat is HOLX’ debt/EBITDA of 2.4x, which is also higher than the group, but is still a

an attractive level, especially in the current environment.

Figure 9: HOLX Valuation Comps

6/14/2010 Mkt Earnings P/E EV EV/Rev EV/EBITDA Debt to EBITDA FCF Yield Cash /

Company Name Ticker Rating PRICE Cap 10E 11E 10E 11E NTM 10E 11E NTM 10E 11E 10E 11E 10E 11E ShareHOLOGIC INC HOLX Neutral 14 .67 3 ,836 1.20 1.33 12.2x 11.0x 4 ,863 2.8x 2.9x 2 .7x 7.2x 7 .8x 7.3x 2.4x 2.2x 10.5% 12.4% $1.65

AMERICAN MEDICAL SYSTMS HLDS AMMD NR 23.02 1,735 1.25 1.41 18.5x 1 6.4x 1,989 3.5x 3.6x 3.4x 10.4x 1 0.7x 10.1x 1.6x 1.5x 6.7% 7.3% $0.67

BARD (C.R.) INC BCR NR 79.80 7,589 5.57 6.16 14.3x 13.0x 7,064 2.5x 2.6x 2.4x 7.9x 8.2x 7.6x 0.2x 0.2x 7.6% 8.0% $7.09

BECKMAN COULTER INC BEC Buy 59.29 4,156 4.36 4.82 13.6x 12.3x 5,199 1.4x 1.4x 1.3x 5.8x 6.0x 5.6x 1.6x 1.4x 6.5% 8.0% $4.23

CAREFUSION CORP CFN NR 25.55 5,680 1.54 1.76 16.6x 14.5x 5,897 1.4x 1.5x 1.4x 7.5x 7.9x 7.2x 1.9x 1.7x 13.6% 6.1% $5.29COOPER COMPANIES INC COO NR 36.92 1,719 2.63 3.03 14.0x 12.2x 2,418 2.0x 2.1x 2.0x 8.5x 9.1x 7.9x 2.7x 2.3x 9.0% 9.5% $0.30

COVIDIEN PLC COV NR 41.58 20,843 3.40 3.75 12.2x 11.1x 22,338 2.0x 2.1x 1.9x 7.6x 7.9x 7.3x 1.0x 1.0x 8.4% 9.1% $2.93

DENTSPLY INTERNATL INC XRAY NR 31.27 4,576 1.93 2.11 16.2x 14.8x 4,603 2.1x 2.1x 2.0x 9.5x 9.8x 9.2x 1.0x 0.9x 5.8% 6.3% $3.08

ELEKTA KTA.B-S NR 199.40 2,630 1 0.55 11.96 18.9x 1 6.7x 1 9,211 2.3x 2.4x 2.2x 11 .6x 1 2.3x 10.9x 1.0 x 0.9x 5.0% 5.7% $8.97

HILL-ROM HOLDINGS INC HRC NR 29.53 1,864 1 .45 1.66 20.4x 17.8x 1 ,823 1.2x 1.2x 1.2x 6.7x 7.0x n/a 0.6x nmf 5.2% 6.2% $3.12

HOSPIRA INC HSP NR 53.91 8,943 3.48 4.02 15.5x 13.4x 9,733 2.4x 2.4x 2.3x 8.7x 9.1x 8.2x 1.6x 1.5x 7.0% 7.6% $5.70INTEGRA LIFESCIENCES HLDGS IART Neut ral 38.8 0 1,125 2.69 2.99 14.4x 13.0x 1,426 1.9x 2.0x 1.8x 8.8x 9.3x 8.2x 2.4 x 2.1x 5.2% 5.9% $2.48

INVERNESS MEDICAL INNOVATNS IMA NR 27.91 2,346 2 .70 3.12 10.3x 8 .9x 3,997 1.9x 1.9x 1.7x 7.0x 7.2x 6.8x 3.8x 3.6x nmf nmf $5.90

KINETIC CONCEPTS INC KCI NR 39.97 2,866 4 .06 4.55 9.9x 8.8x 3,839 1.8x 1.9x 1.8x 5.8x 6.0x 5.6x 1.9x 1.8x 9.8% 14.3% $3.67

LABORATORY CP OF AMER HLDGS LH NR 78.81 8,196 5.45 6.04 14.5x 13.0x 9,376 1.9x 1.9x 1.8x 7.5x 7.7x 7.2x 1.1x 1.0x 9.1% 8.9% $1.43

LIFE TECHNOLOGIES CORP LIFE NR 50.02 9,134 3.45 3.86 14.5x 13.0x 11,121 3.0x 3.1x 2.9x 8.2x 8.4x 8.1x 2.0x 1.9x 6.1% 8.3% $3.55

MYRIAD GENETICS INC MYGN Sell 18.04 1,764 1.23 1.23 14.7x 14.6x 1,447 3.7x 3.7x 3.3x 8.8x 9.4x 8.0x nmf 0.0x 5.3% 5.9% $3.24

QUEST DIAGNOSTICS INC DGX NR 52.91 9,520 4.18 4.59 12.6x 11.5x 12,101 1.6x 1.6x 1.5x 7.2x 7.3x 6.9x 1.9x 1.8x 9.9% 9.7% $2.97

STERIS CORP STE NR 32.15 1,905 2.17 2.37 14.8x 13.6x 1,900 1.4x 1.5x 1.4x 6.8x 7.0x 6.3x 0.8x 0.7x 7.2% 7.9% $3.63

THERMO FISHER SCIENTIFIC INC TMO NR 52.1 6 21,358 3.48 3.91 15.0x 13.3x 21,865 2.0x 2.0x 1.9x 9.6x 10.0x 9.2x 0.9 x 0.9x 6.9% 7.4% $3.84

VARIAN MEDICAL SYSTEMS INC VAR Neutral 50.31 6,215 2.97 3.34 16.9x 15.1x 5,691 2.3x 2.4x 2.2x 9.0x 9.5x 8.5x 0.0x 0.0x 5.8% nmf $4.48

WATERS CORP WAT NR 68.86 6,400 3.94 4.44 17.5x 1 5.5x 6,482 4.0x 4.0x 3.8x 11.8x 1 2.3x 11.2x 1.3x 1.2x 6.1% 6.9% $6.78

Mean 15.0x 13.4x 2.2x 2.2x 2.1x 8.3x 8.7x 8.0x 1.5x 1.3x 7.3% 7.8%

Median 14.7x 13.3x 2.0x 2.1x 1.9x 8.2x 8.4x 8.0x 1.4x 1.3x 6.8% 7.6%

Market Cap Weighted Mean 14.6x 13.0x 2.2x 2.2x 2.1x 8.4x 8.7x 7.9x 1.3x 1.2x 7.5% 7.5%

Source: FactSet and Gleacher & Co. Estimates

Page

Gleacher & Company Securities, I

June 16, 20Hologic, Inc. : In Search of the Elusive Growth; Initiating with a Neu

Gleacher & Company

8/3/2019 2010.06.16 - HOLX - Initiation at Neutral Gleacher

http://slidepdf.com/reader/full/20100616-holx-initiation-at-neutral-gleacher 16/20

COMPANY DESCRIPTION

Founded in 1985, Hologic, Inc. has grown to become a leading developer, manufacturer

and supplier of premium diagnostic products, medical imaging systems, and surgica

products created specifically to address the healthcare needs of women throughout the

world.

HOLX’ comprehensive suite of products spans nine key areas: mammography and breas

biopsy; radiation treatment for early-stage breast cancer; cervical cancer screening

treatment for menorrhagia; permanent contraception; osteoporosis assessment; preterm

birth risk assessment; mini C-arms for extremity imaging; as well as molecular diagnostic

products, including human papillomavirus (HPV) testing and reagents for a variety of DNA

analysis applications. The company’s core business units are focused on breast health

diagnostics, GYN surgical, and skeletal health.

Bull Case

• Despite limited sales and EPS growth in the near term, HOLX still generates

significant free cash flow, with a yield (10% for CY10) above its peers.

• A budding digital mammography replacement cycle could help stabilize sales

over the next 12-18 months, and a 3D Tomo approval could drive growth beyond

• Products such as NovaSure, Adiana and Cervista HPV are growing modestly

taking share in their respective markets (albeit slowly), and helping to stabilize

sales.

Bear Case

• FFDM (full-field digital mammography) market penetration may not continue

growing as it has in the past. The adoption of digital mammography from analog

has been robust in the past two years, driven in large part by the positive

outcomes of the DMIST study. We believe that over time, digital mammographysystems will be the standard of care for breast cancer screening, but continued

new unit growth may be encumbered by the significantly higher upfront cos

differential in comparison to conventional film-based mammography products.

• Competition should continue to be intense in the breast imaging market. There

are already several companies that compete or will compete with HOLX's

products. Several competitors have considerably larger operations with greate

financial resources and an even broader range of product offerings. Increasing

competition may not only hinder new unit sales but also reduce system pricing. In

comparison to other manufacturers, Selenia ASPs have remained relatively

stable so far, but competitive pressures may lead to higher than expected ASP

erosion.

• Reimbursement levels for digital mammography have been favorable to date

and we believe this trend will continue in the longer term. However, this does notmean that future cuts are impossible. Further, the company's other products are

also subject to varying reimbursement levels, including breast biopsy, CAD and

bone density assessment. Future reimbursement cuts or other adverse changes

in reimbursement policies for the use of these could prove to be detrimental to

future sales growth.

• We believe that there are substantial expectations for the sales and earnings

power of a combined HOLX/CYTC. Aside from the growing pains associated with

the integration of the two companies, we believe there are several Cytyc-specific

Page

Gleacher & Company Securities, I

June 16, 20Hologic, Inc. : In Search of the Elusive Growth; Initiating with a Neu

Gleacher & Company

8/3/2019 2010.06.16 - HOLX - Initiation at Neutral Gleacher

http://slidepdf.com/reader/full/20100616-holx-initiation-at-neutral-gleacher 17/20

risks to be mindful of, including increasing competition for ThinPrep and

NovaSure, slowing growth of the Imager product, and a Pap market that is close

to full penetration levels.

Public Companies Mentioned:

Becton Dickinson (BDX, $70.19, NR)Boston Scientific (BSX, $5.82, NR)

Conceptus (CPTS, $17.12, Neutral)

CR Bard (BCR, $79.80, NR)

General Electric (GE, $15.39, NR)

Merck (MRK, 35.02, NR)

Qiagen (QGEN, $20.82, NR)

SenoRx (SENO, $10.92, NR)

Bayer (BAYZF, $58.60, NR)

Page

Gleacher & Company Securities, I

June 16, 20Hologic, Inc. : In Search of the Elusive Growth; Initiating with a Neu

Gleacher & Company

8/3/2019 2010.06.16 - HOLX - Initiation at Neutral Gleacher

http://slidepdf.com/reader/full/20100616-holx-initiation-at-neutral-gleacher 18/20

8/3/2019 2010.06.16 - HOLX - Initiation at Neutral Gleacher

http://slidepdf.com/reader/full/20100616-holx-initiation-at-neutral-gleacher 19/20

Q1 Q2 Q3 Q1 Q2 Q3 Q1 Q2 Q3 Q1 Q20

8

16

24

32

40

2008 2009 2010

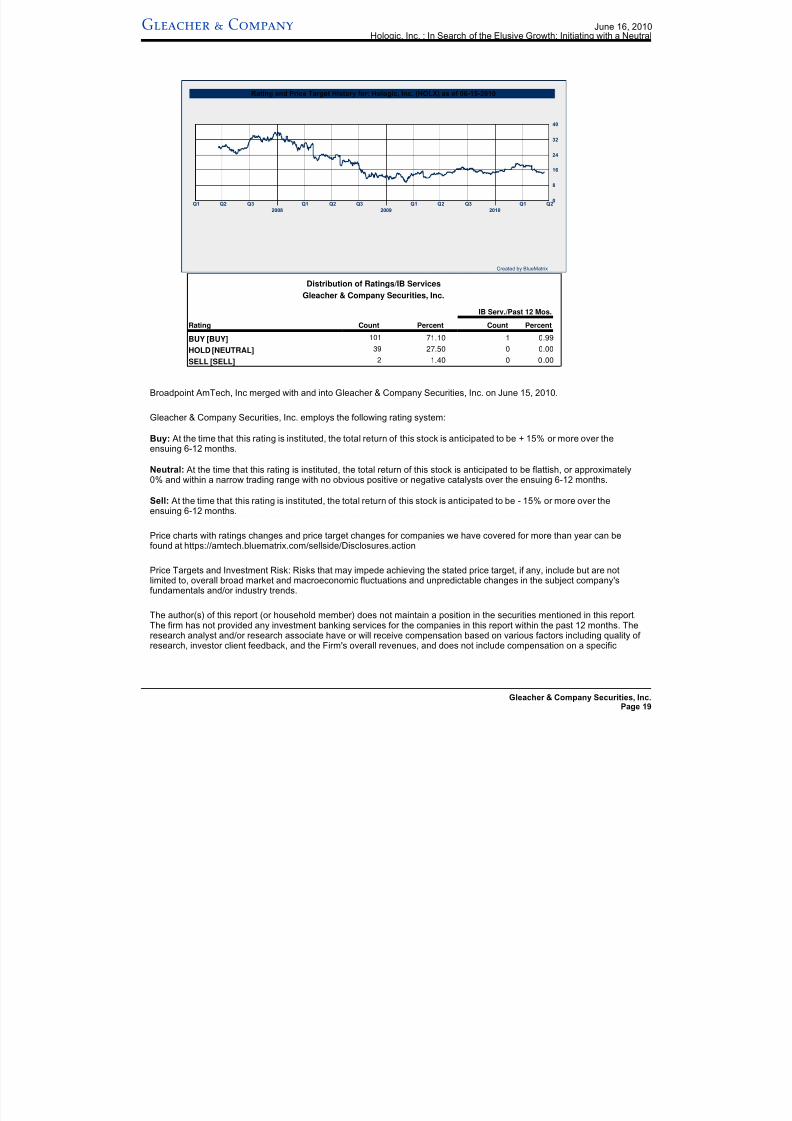

Rating and Price Target History for: Hologic, Inc. (HOLX) as of 06-15-2010

Created by BlueMatrix

Distribution of Ratings/IB Services

Gleacher & Company Securities, Inc.

IB Serv./Past 12 Mos.

Rating Count Percent Count Percent

BUY [BUY] 101 71.10 1 0.99

HOLD [NEUTRAL] 39 27.50 0 0.00

SELL [SELL] 2 1.40 0 0 .00

Broadpoint AmTech, Inc merged with and into Gleacher & Company Securities, Inc. on June 15, 2010.

Gleacher & Company Securities, Inc. employs the following rating system:

Buy: At the time that this rating is instituted, the total return of this stock is anticipated to be + 15% or more over theensuing 6-12 months.

Neutral: At the time that this rating is instituted, the total return of this stock is anticipated to be flattish, or approximately0% and within a narrow trading range with no obvious positive or negative catalysts over the ensuing 6-12 months.

Sell: At the time that this rating is instituted, the total return of this stock is anticipated to be - 15% or more over theensuing 6-12 months.

Price charts with ratings changes and price target changes for companies we have covered for more than year can befound at https://amtech.bluematrix.com/sellside/Disclosures.action

Price Targets and Investment Risk: Risks that may impede achieving the stated price target, if any, include but are notlimited to, overall broad market and macroeconomic fluctuations and unpredictable changes in the subject company'sfundamentals and/or industry trends.

The author(s) of this report (or household member) does not maintain a position in the securities mentioned in this report.The firm has not provided any investment banking services for the companies in this report within the past 12 months. Theresearch analyst and/or research associate have or will receive compensation based on various factors including quality ofresearch, investor client feedback, and the Firm's overall revenues, and does not include compensation on a specific

PageGleacher & Company Securities, I

June 16, 20Hologic, Inc. : In Search of the Elusive Growth; Initiating with a Neu

Gleacher & Company

8/3/2019 2010.06.16 - HOLX - Initiation at Neutral Gleacher

http://slidepdf.com/reader/full/20100616-holx-initiation-at-neutral-gleacher 20/20

investment banking services transaction.

Information in this report is intended for use only by professional or institutional investors. Any opinion expressed in thisreport is subject to change and Gleacher & Company Securities, Inc. is under no obligation to update or keep current theinformation contained herein. Gleacher & Company Securities, Inc. accepts no liability whatsoever for any loss or damageof any kind arising from use of this report.

Gleacher & Company Securities, Inc is a member of the FINRA and a member of SIPC. Gleacher & Company Securities,Inc. has prepared this document. Information contained herein has been obtained from sources believed to be reliable, butthe accuracy and completeness of the information, and that of the opinions based thereon, are not guaranteed. This reportis not an offer to buy or sell or a solicitation of an offer to buy or sell the securities mentioned or related securities.Gleacher & Company Securities, Inc. is a registered broker-dealer. Gleacher & Company Securities, Inc., and its entitiesand persons associated with it, may have long or short positions in or effect transactions in the securities of companiesmentioned in this report. Do not change or reproduce any of this report without the express written consent of Gleacher &Company Securities, Inc. Additional information on recommended securities is available on request.

Gleacher & Company Securities, Inc.

1290 Avenue of the Americas

New York, NY 10104

©2010 Gleacher & Company Securities, Inc. All rights reserved.

I, Amit Hazan, as the analyst responsible for this report, certify that:1) All Views expressed in this research Reportaccurately reflect my personal views about any and all of the subject securities or issuers discussed; and 2) No part of mycompensation was, is, or will be, directly or indirectly, related to the specific recommendations or views expressed by me inthis research report.

I, Jeremy Feffer, as the analyst responsible for this report, certify that:1) All Views expressed in this research Reportaccurately reflect my personal views about any and all of the subject securities or issuers discussed; and 2) No part of mycompensation was, is, or will be, directly or indirectly, related to the specific recommendations or views expressed by me inthis research report.

June 16, 20Hologic, Inc. : In Search of the Elusive Growth; Initiating with a Neu

Gleacher & Company