2007 interim results - investis cmsfiles.investis.com/cadbury_ir/2007interimresultsam.pdf · ·...

TRANSCRIPT

2

2007 Interim Results1 August 2007

This material may be deemed to include forward-looking statements within the meaning of Section 27A of the US Securities Act of

1933 and Section 21E of the US Securities Exchange Act of 1934. These forward-looking statements are only predictions and you

should not rely unduly on them. Actual results might differ materially from those projected in any such forward-looking statements,

which involve known and unknown risks, uncertainties and other factors that may cause our or our industry’s actual results, levels of

activity, performance or achievements to be materially different from any future results, levels of activity, performance or

achievements expressed or implied by the forward-looking statements. In evaluating forward-looking statements, which are

generally identifiable by use of the words “may”, “will”, “should”, “expect”, “anticipate”, “estimate”, “believe”, “intend” or “project”

or the negative of these words or other variations on these words or comparable terminology, you should consider various factors

including the risks outlined in our Form 20-F filed with the SEC. Although we believe the expectations reflected in forward-looking

statements are reasonable we cannot guarantee future results, levels of activity, performance or achievements. This presentation

should be viewed in conjunction with our periodic interim and annual reports and registration statements filed with the Securities

and Exchange Commission, copies of which are available from Cadbury Schweppes plc, 25 Berkeley Square, London W1J 6HB, UK.

Results Overview and Operating Review

Todd StitzerChief Executive Officer

4

Today’s Agenda

• Overview

• Half Year Regional Performance Review

• Half Year Financial Review

• 2007 Full Year Outlook

• Conclusion

5

2007 Half Year Overview

• Good first half performance from continuing businesses

• Announced separation of Americas Beverages

• Ambitious new confectionery plans

• Bolt-on acquisitions to strengthen existing confectionery positions

and enter new emerging markets

• Exit low-growth non-core businesses

• Americas Beverages sale process extended

6

Half Year Performance Highlights

• Revenue +6%, driven by double-digit growth from gum and

emerging markets

• Strengthened performance in developed markets

• Higher contribution from pricing

• Margin reflects investment behind successful growth initiatives

Top 13brands+9%

FocusMarkets

+7%

Top GlobalCustomers

+8%

7

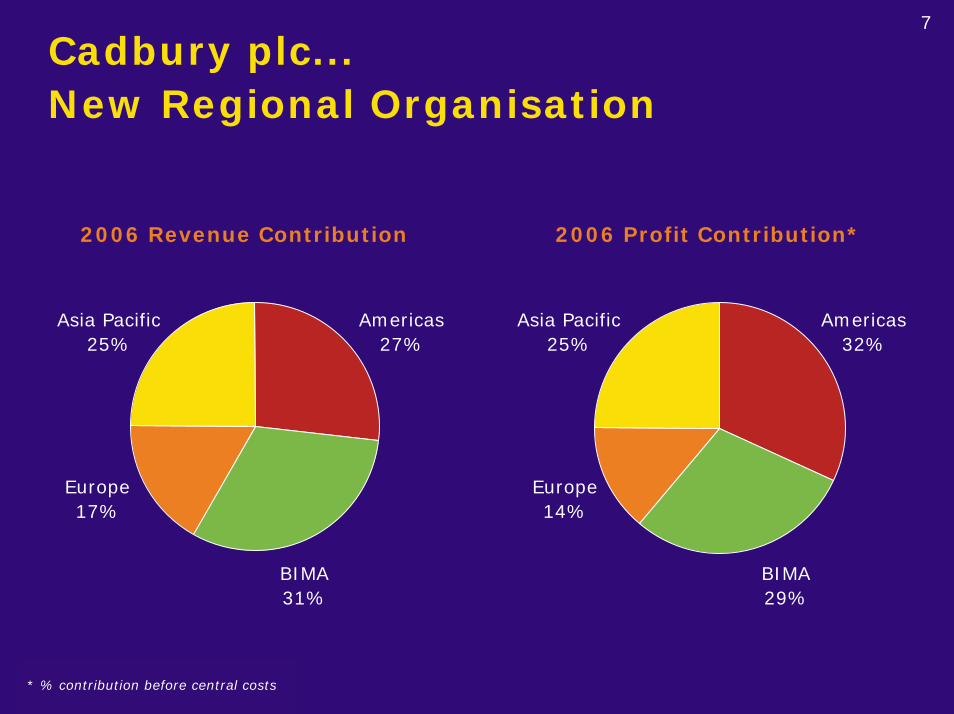

Cadbury plc...New Regional Organisation

2006 Revenue Contribution

Asia Pacific25%

Americas27%

Europe17%

BIMA31%

Asia Pacific25%

Americas32%

Europe14%

BIMA29%

2006 Profit Contribution*

* % contribution before central costs

8

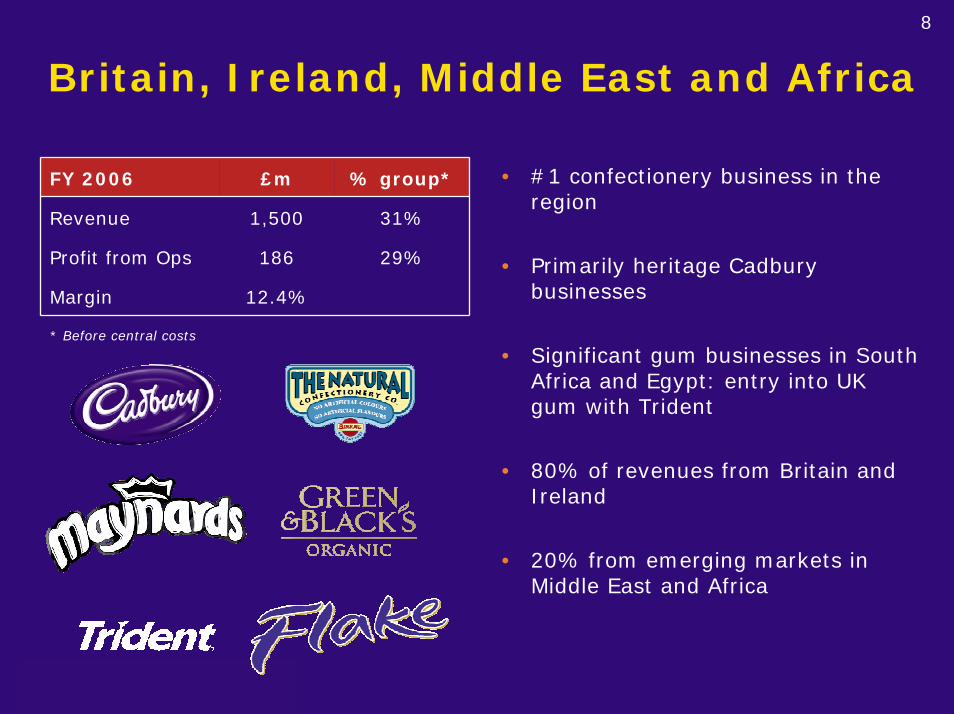

Britain, Ireland, Middle East and Africa

• #1 confectionery business in the region

• Primarily heritage Cadbury businesses

• Significant gum businesses in South Africa and Egypt: entry into UK gum with Trident

• 80% of revenues from Britain and Ireland

• 20% from emerging markets in Middle East and Africa

FY 2006 £m % group*

Revenue 1,500 31%

Profit from Ops 186 29%

Margin 12.4%

* Before central costs

9

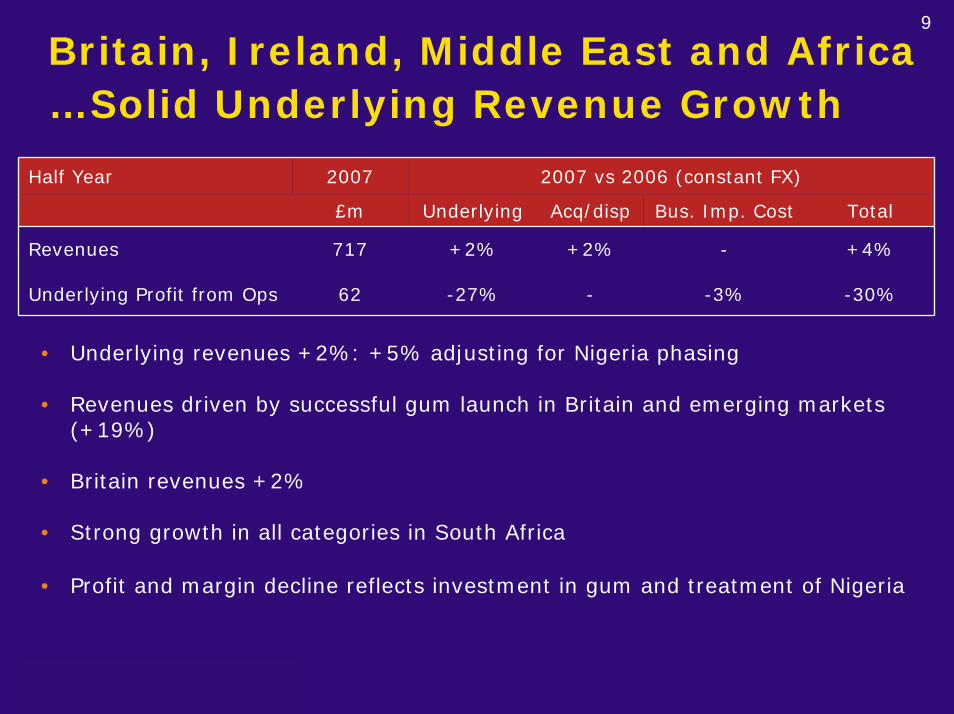

Britain, Ireland, Middle East and Africa …Solid Underlying Revenue Growth

Half Year 2007 2007 vs 2006 (constant FX)

£m Underlying Acq/disp Bus. Imp. Cost Total

Revenues 717 +2% +2% - +4%

Underlying Profit from Ops 62 -27% - -3% -30%

• Underlying revenues +2%: +5% adjusting for Nigeria phasing

• Revenues driven by successful gum launch in Britain and emerging markets (+19%)

• Britain revenues +2%

• Strong growth in all categories in South Africa

• Profit and margin decline reflects investment in gum and treatment of Nigeria

10

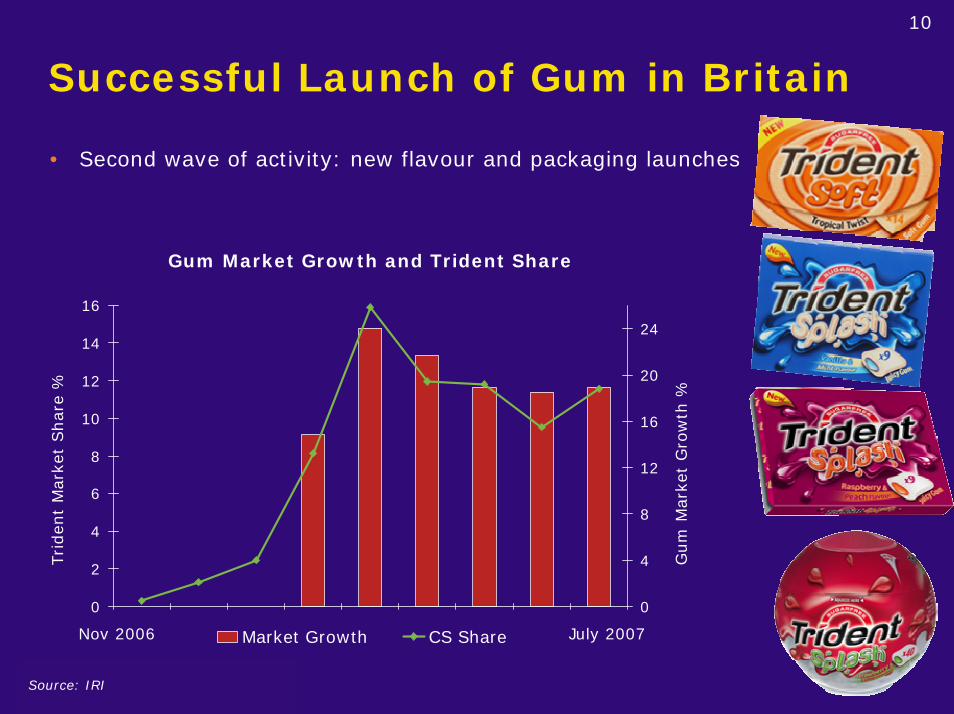

Successful Launch of Gum in Britain

• Second wave of activity: new flavour and packaging launches

Gum Market Growth and Trident Share

Nov 2006 July 2007

Gum

Mar

ket

Gro

wth

%Source: IRI

0

2

4

6

8

10

12

14

16

0

4

8

12

16

20

24

Market Growth CS Share

Triden

t M

arke

t Share

%

11

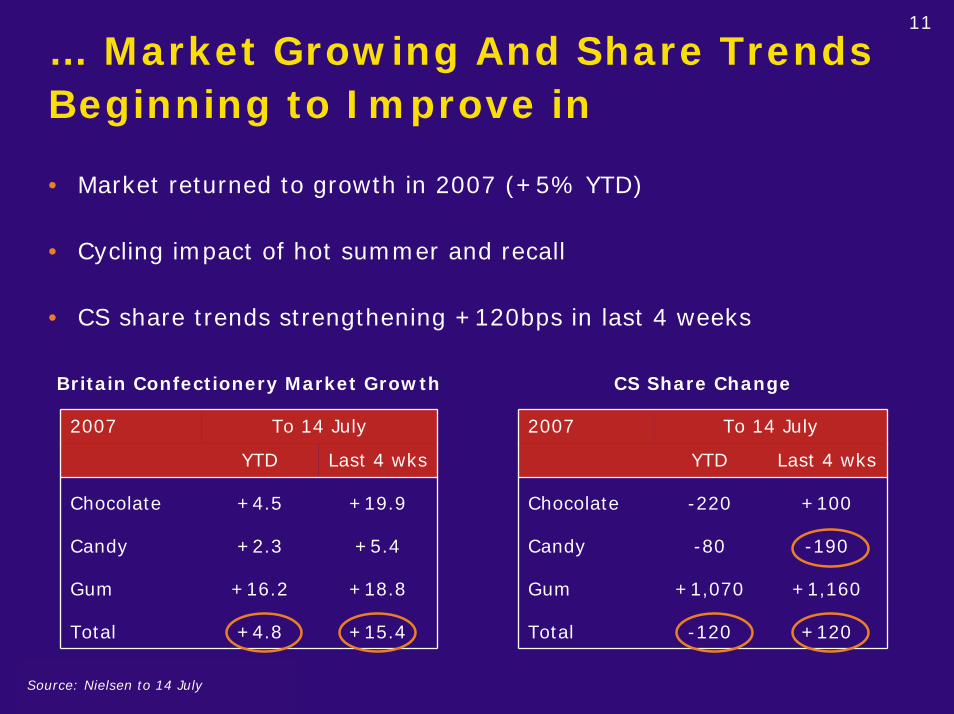

… Market Growing And Share Trends Beginning to Improve in

• Market returned to growth in 2007 (+5% YTD)

• Cycling impact of hot summer and recall

• CS share trends strengthening +120bps in last 4 weeks

Britain Confectionery Market Growth CS Share Change

2007 To 14 July

YTD Last 4 wks

+19.9

+5.4

+18.8

Total +4.8 +15.4

Gum

Chocolate +4.5

Candy +2.3

+16.2

2007 To 14 July

YTD Last 4 wks

+100

-190

+1,160

Total -120 +120

Gum

Chocolate -220

Candy -80

+1,070

Source: Nielsen to 14 July

12

Europe

• Includes all our businesses in W and E Europe, Russia and Turkey

• Largest market is France

• Revenues split 50:50 developed / emerging markets

• Top 10 brands = 65% of revenue

• Primarily gum and pocket candy

• Chocolate presence mainly in Poland and now Romania

* Before central costs

FY 2006 £m % group*

Revenue 818 17%

Profit from Ops 90 14%

Margin 11.0%

13

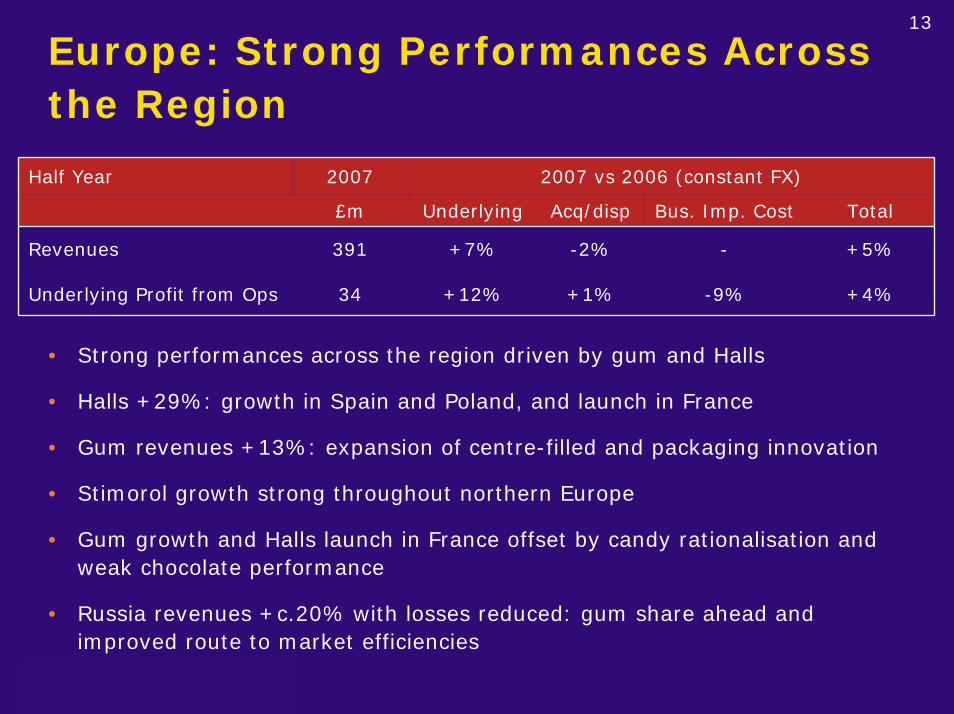

Europe: Strong Performances Across the Region

Half Year 2007 2007 vs 2006 (constant FX)

£m Underlying Acq/disp Bus. Imp. Cost Total

Revenues 391 +7% -2% - +5%

Underlying Profit from Ops 34 +12% +1% -9% +4%

• Strong performances across the region driven by gum and Halls

• Halls +29%: growth in Spain and Poland, and launch in France

• Gum revenues +13%: expansion of centre-filled and packaging innovation

• Stimorol growth strong throughout northern Europe

• Gum growth and Halls launch in France offset by candy rationalisation and weak chocolate performance

• Russia revenues +c.20% with losses reduced: gum share ahead and improved route to market efficiencies

14

Americas

• Includes all our businesses North and Latin America

• 55% developed / 45% emerging markets

• #1 confectionery business in Latin America

• Primarily a gum and pocket candy business

• Significant Cadbury chocolate presence in Canada

• Highly concentrated brand portfolio: top 4 brands = 65% of revenues

* Before central costs

FY 2006 £m % group*

Revenue 1,330 27%

Profit from Ops 207 32%

Margin 15.6%

15

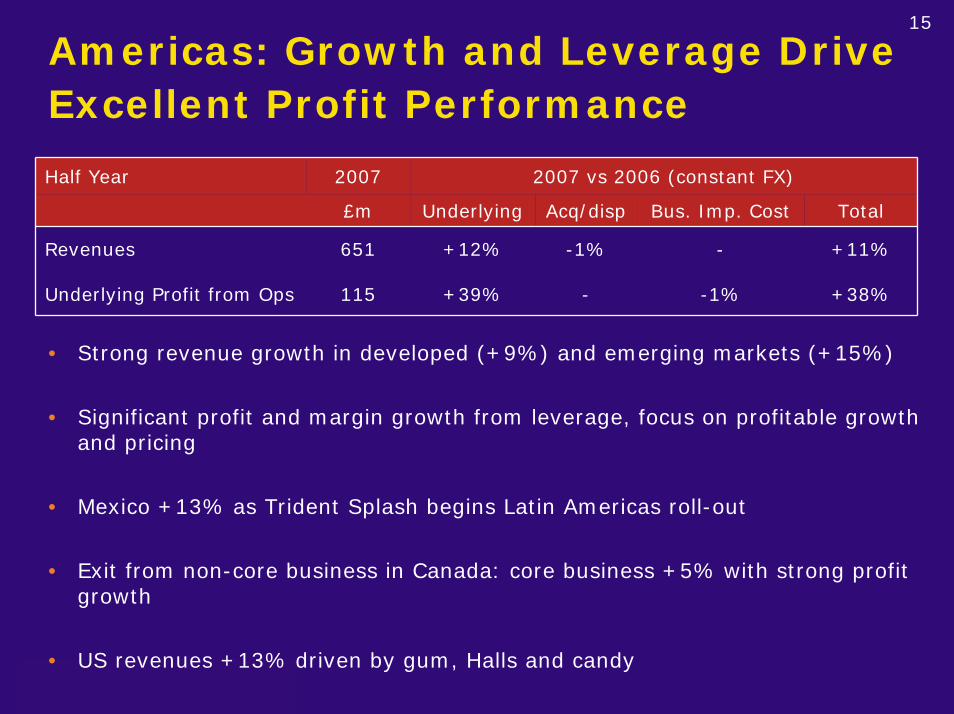

Americas: Growth and Leverage Drive Excellent Profit Performance

Half Year 2007 2007 vs 2006 (constant FX)

£m Underlying Acq/disp Bus. Imp. Cost Total

Revenues 651 +12% -1% - +11%

Underlying Profit from Ops 115 +39% - -1% +38%

• Strong revenue growth in developed (+9%) and emerging markets (+15%)

• Significant profit and margin growth from leverage, focus on profitable growth and pricing

• Mexico +13% as Trident Splash begins Latin Americas roll-out

• Exit from non-core business in Canada: core business +5% with strong profit growth

• US revenues +13% driven by gum, Halls and candy

16

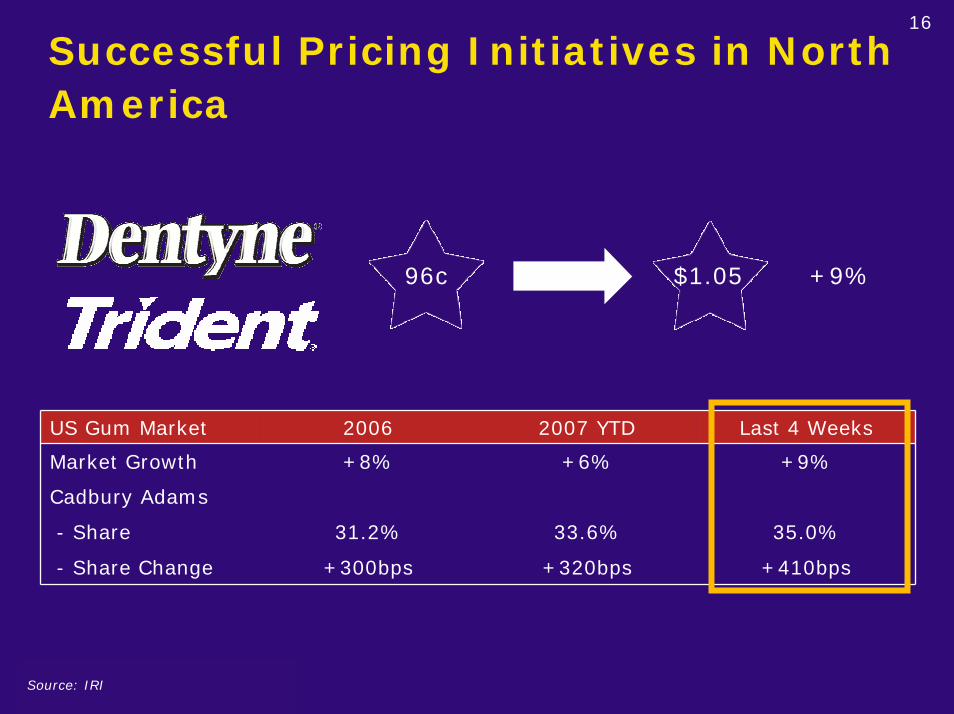

Successful Pricing Initiatives in North America

96c $1.05 +9%

US Gum Market 2006 2007 YTD Last 4 Weeks

Market Growth +8% +6% +9%

Cadbury Adams

- Share 31.2% 33.6% 35.0%

- Share Change +300bps +320bps +410bps

Source: IRI

17

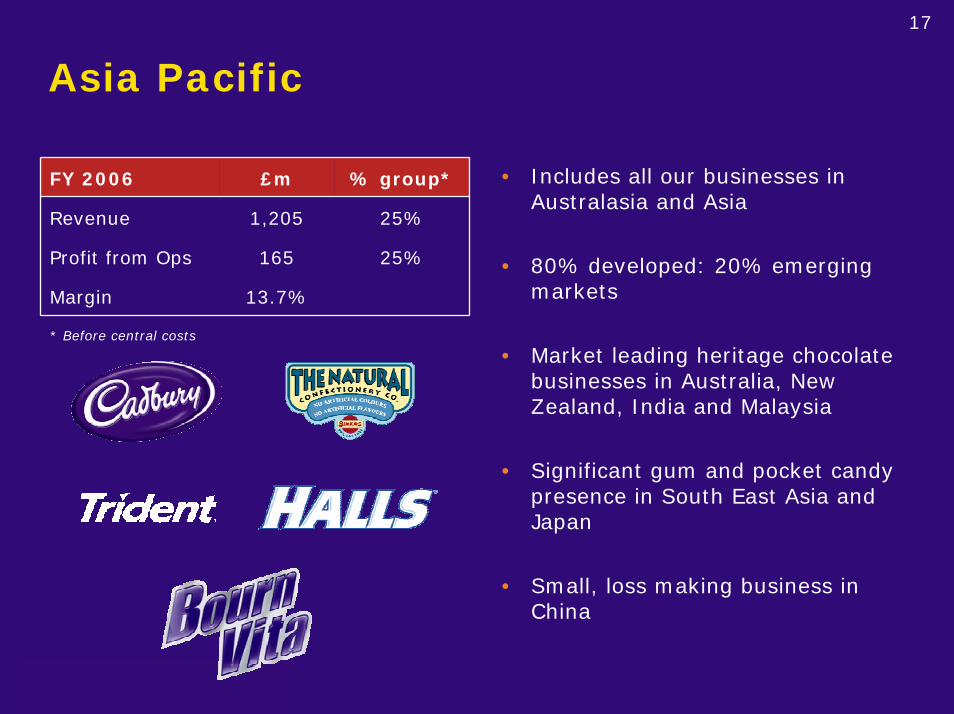

Asia Pacific

• Includes all our businesses in Australasia and Asia

• 80% developed: 20% emerging markets

• Market leading heritage chocolate businesses in Australia, New Zealand, India and Malaysia

• Significant gum and pocket candy presence in South East Asia and Japan

• Small, loss making business in China

* Before central costs

FY 2006 £m % group*

Revenue 1,205 25%

Profit from Ops 165 25%

Margin 13.7%

18

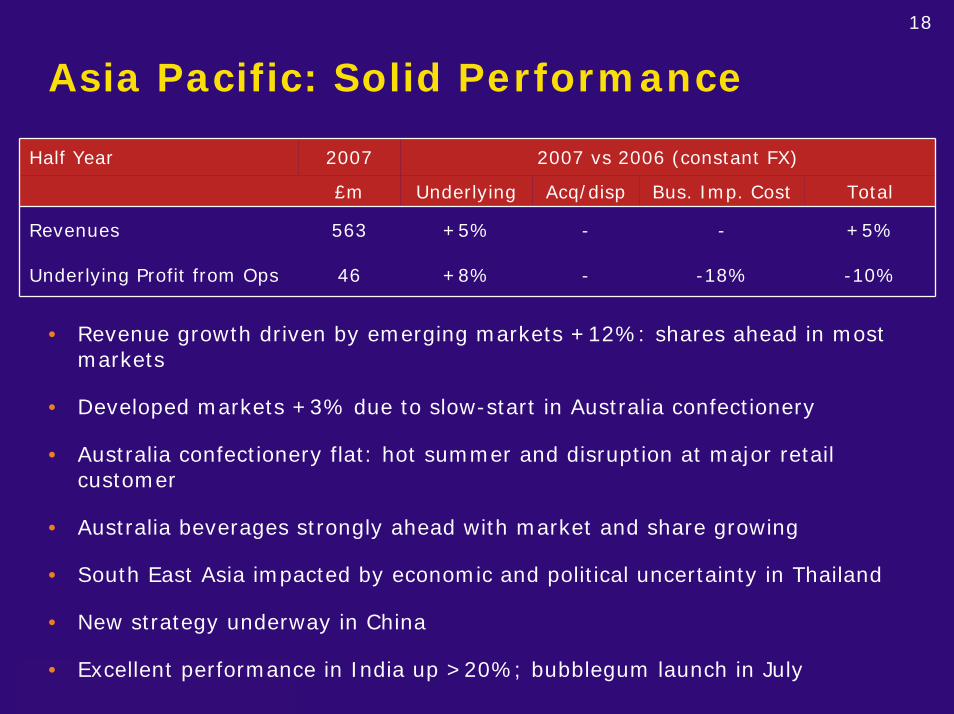

Asia Pacific: Solid Performance

Half Year 2007 2007 vs 2006 (constant FX)

£m Underlying Acq/disp Bus. Imp. Cost Total

Revenues 563 +5% - - +5%

Underlying Profit from Ops 46 +8% - -18% -10%

• Revenue growth driven by emerging markets +12%: shares ahead in most markets

• Developed markets +3% due to slow-start in Australia confectionery

• Australia confectionery flat: hot summer and disruption at major retail customer

• Australia beverages strongly ahead with market and share growing

• South East Asia impacted by economic and political uncertainty in Thailand

• New strategy underway in China

• Excellent performance in India up >20%; bubblegum launch in July

Financial Review

Ken HannaChief Financial Officer

20

Agenda

• Americas Beverages update

• Underlying revenue growth and margin analyses

• Income statement

• Cash flow

• Outlook 2007

21

Americas Beverages Update

• Performance in line with expectations; revenue growth +5%

• YTD CSD share up 70 bps; non-CSD share up 20 bps

• Investing behind new product launches

- Snapple super premium and mainstream teas

- Accelerade

• Price increases to cover higher input costs

• Trading margin down reflecting launch investments

• Sale process ongoing – extended timetable due to debt market volatility

22

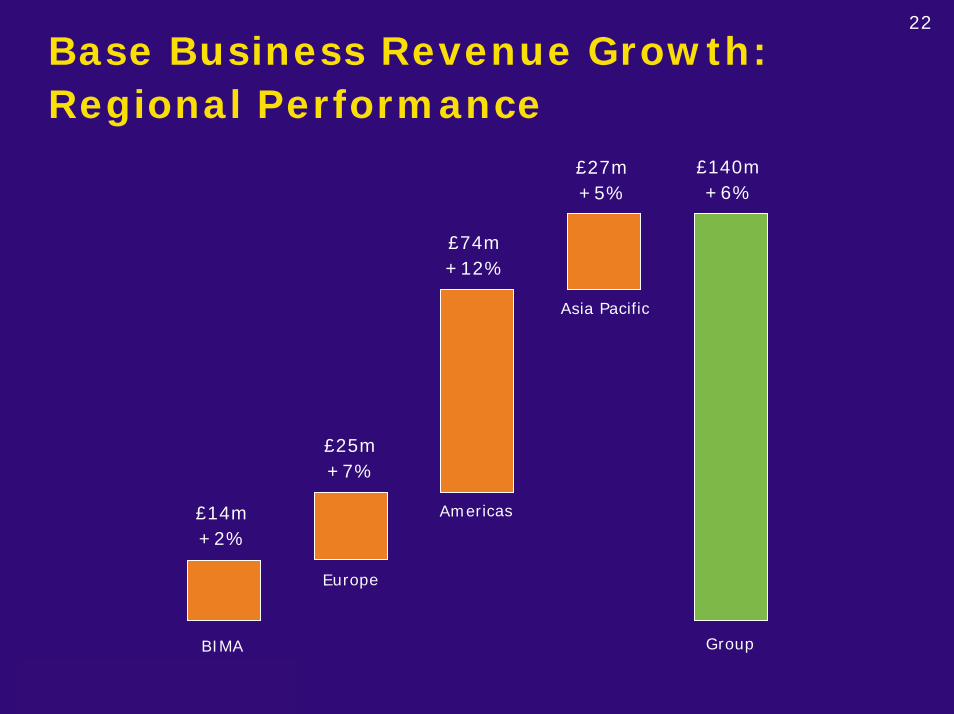

Base Business Revenue Growth: Regional Performance

£140m+6%

£27m+5%

£74m+12%

Asia Pacific

£25m+7%

Americas£14m+2%

Europe

GroupBIMA

23

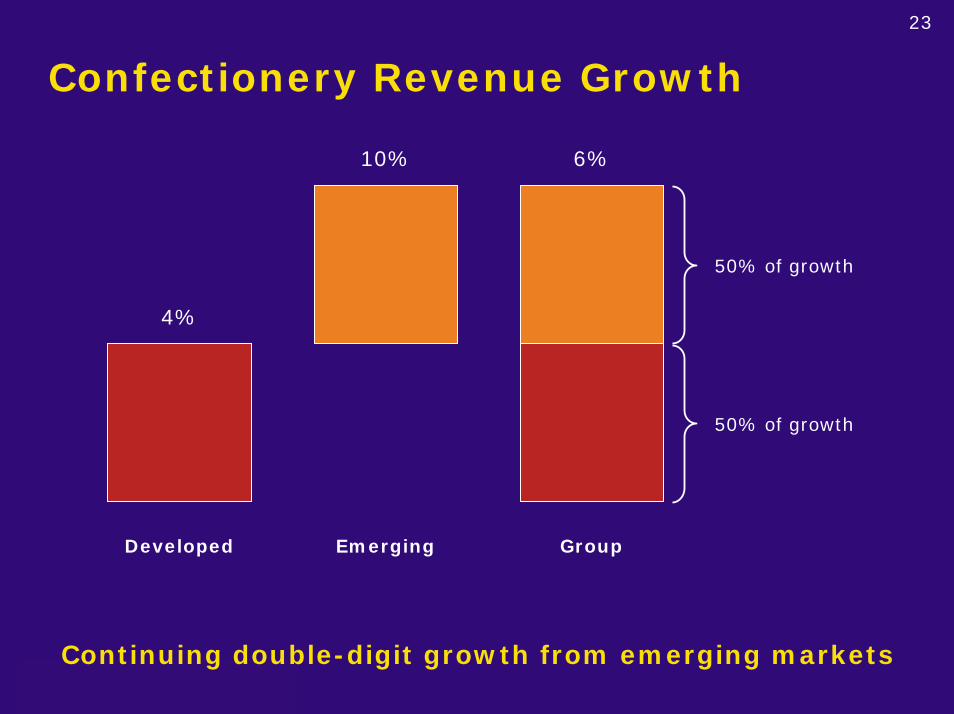

Confectionery Revenue Growth

10% 6%

50% of growth

4%

50% of growth

Developed Emerging Group

Continuing double-digit growth from emerging markets

24

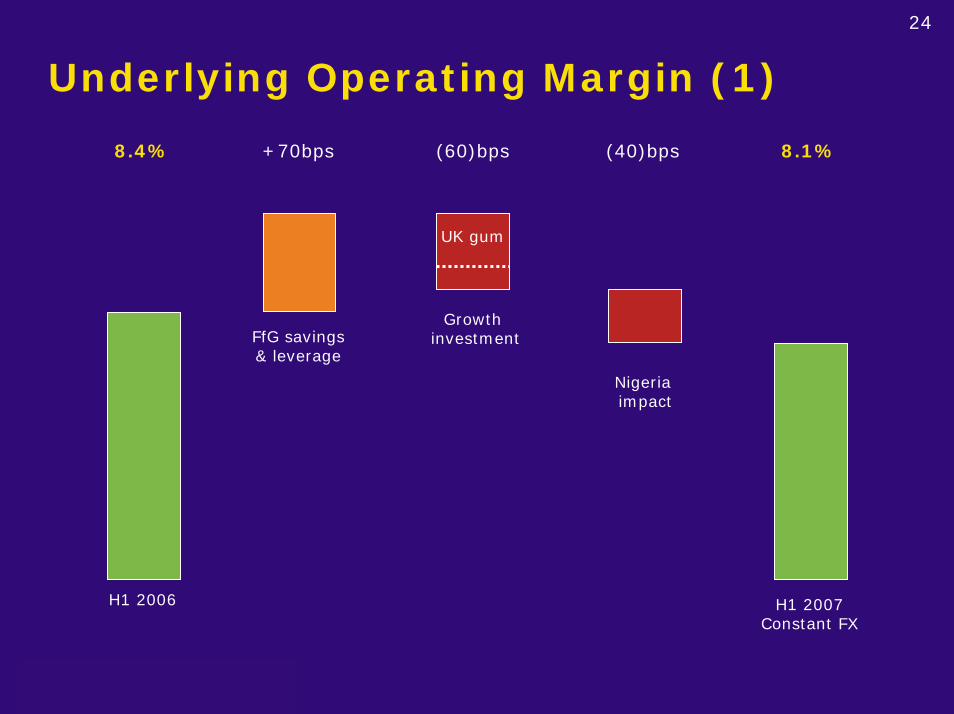

Underlying Operating Margin (1)

8.4% +70bps (60)bps (40)bps 8.1%

UK gum

GrowthinvestmentFfG savings

& leverage

Nigeriaimpact

H1 2006 H1 2007 Constant FX

25

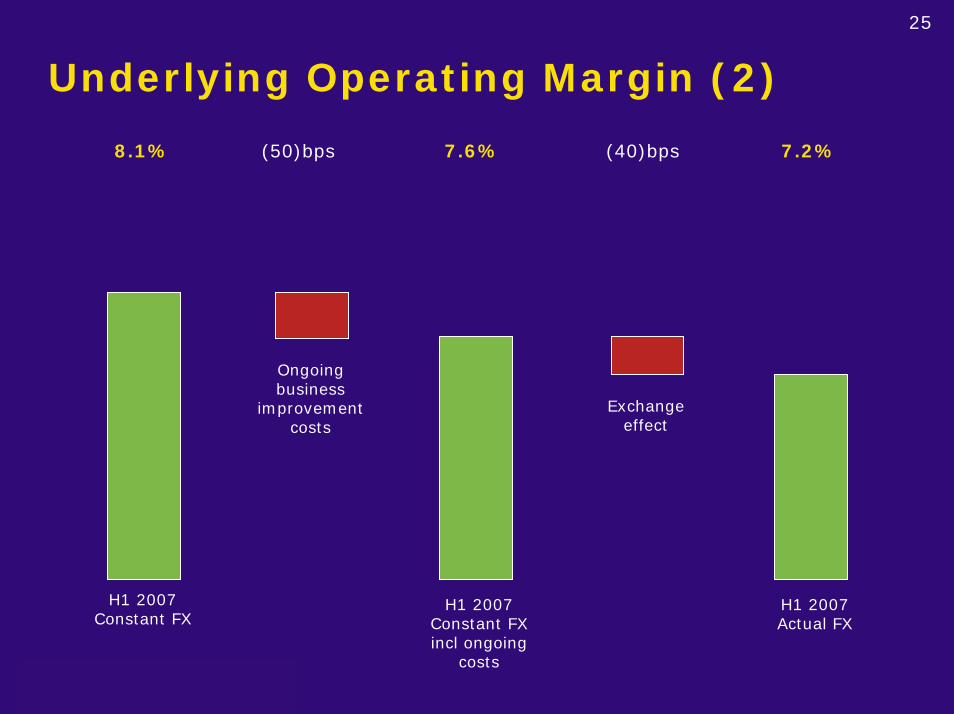

Underlying Operating Margin (2)

8.1% (50)bps 7.6% (40)bps 7.2%

Ongoing business

improvement costs

Exchange effect

H1 2007Constant FX

H1 2007 Constant FXincl ongoing

costs

H1 2007 Actual FX

26

Growth-Related Investment

• Investment in UK gum c£10m

• Other marketing spend c£10m

- UK chocolate

- Centre-filled gum in Europe

- Stride in US

• Total marketing: sales +20bps

• Incremental growth investment c£10m

- New product listings and increased S&T resources

- Strengthening RTM in Latin America & Russia

27

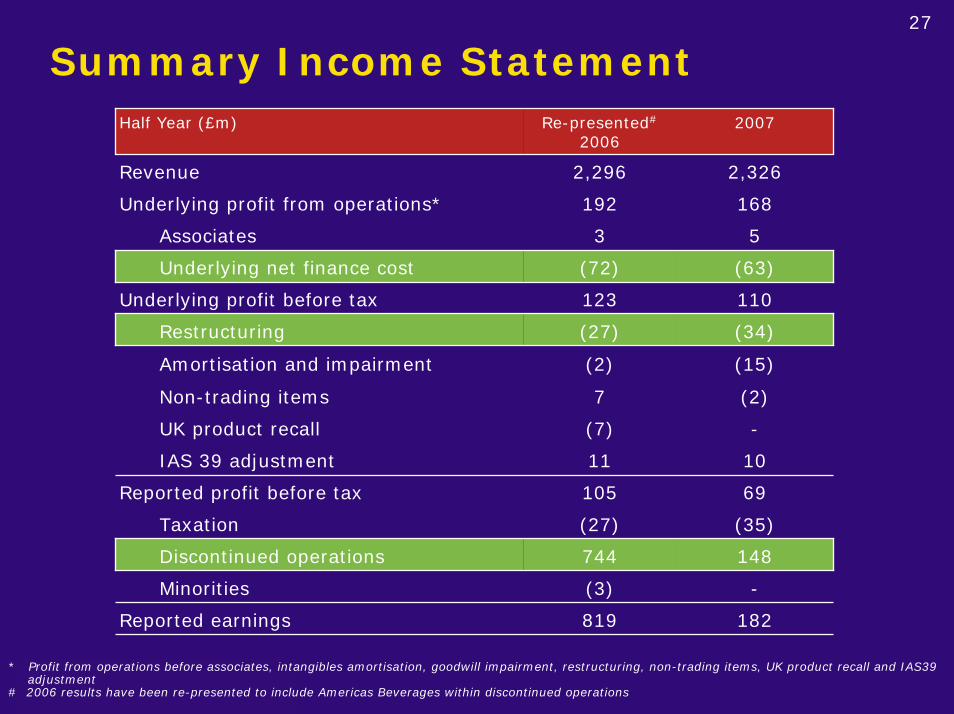

Summary Income StatementHalf Year (£m) Re-presented#

20062007

Revenue 2,296 2,326

Underlying profit from operations* 192 168

Associates 3 5

Underlying net finance cost (72) (63)

Underlying profit before tax 123 110

Restructuring (27) (34)

Amortisation and impairment (2) (15)

Non-trading items 7 (2)

UK product recall (7) -

IAS 39 adjustment 11 10

Reported profit before tax 105 69

Taxation (27) (35)

Discontinued operations 744 148

Minorities (3) -

Reported earnings 819 182

* Profit from operations before associates, intangibles amortisation, goodwill impairment, restructuring, non-trading items, UK product recall and IAS39 adjustment

# 2006 results have been re-presented to include Americas Beverages within discontinued operations

28

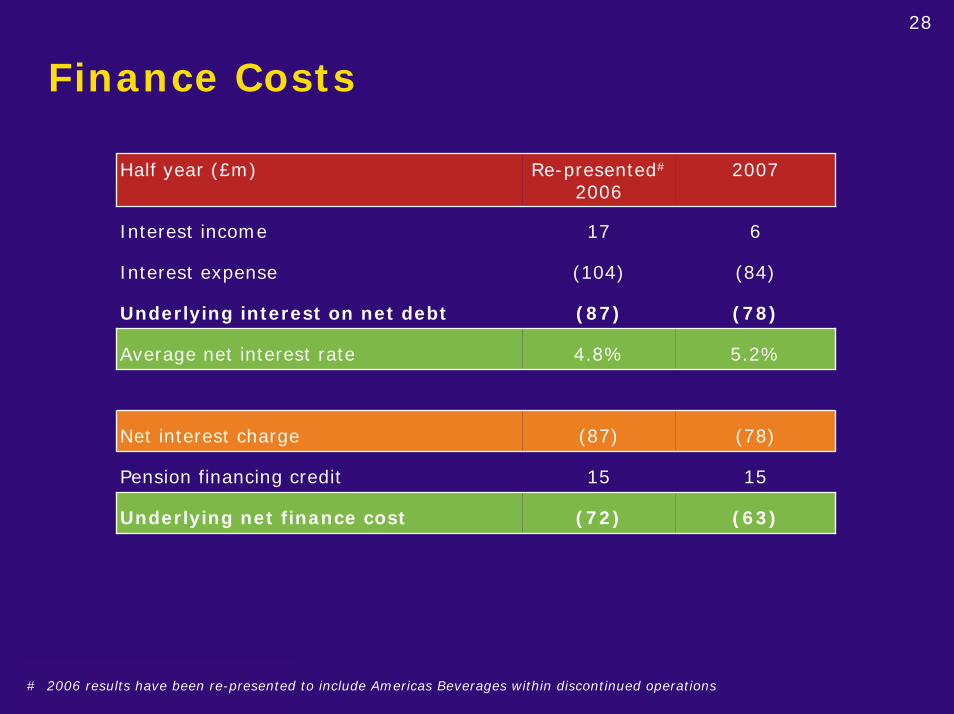

Finance Costs

Half year (£m) Re-presented#

20062007

Interest income 17 6

Interest expense (104) (84)

Underlying interest on net debt (87) (78)

Average net interest rate 4.8% 5.2%

Net interest charge (87) (78)

Pension financing credit 15 15

Underlying net finance cost (72) (63)

# 2006 results have been re-presented to include Americas Beverages within discontinued operations

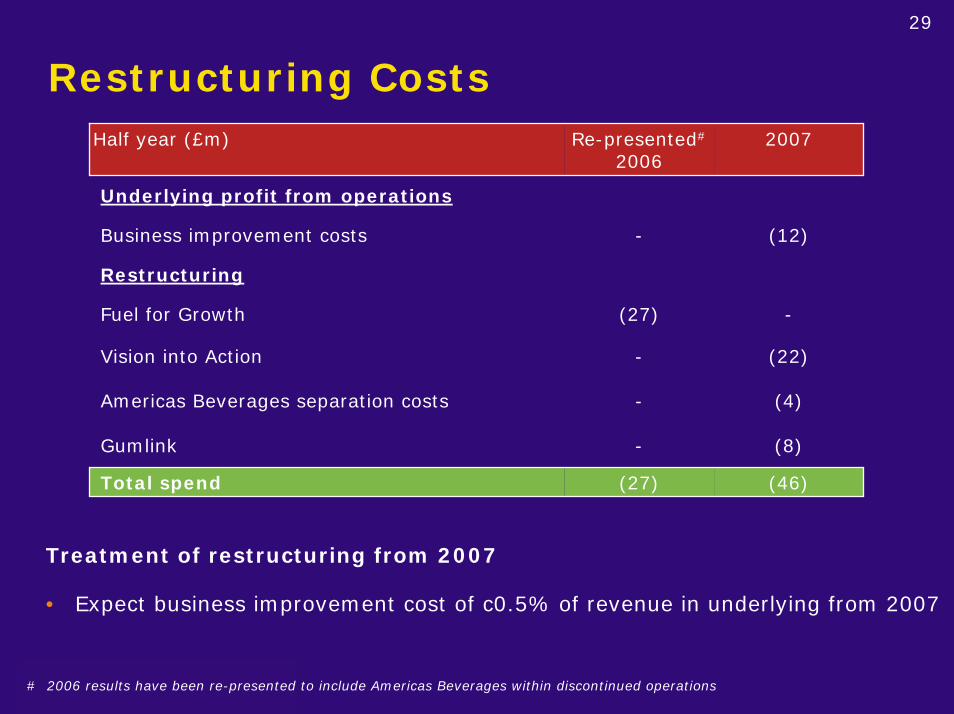

29

Restructuring CostsHalf year (£m) Re-presented#

20062007

Underlying profit from operations

Business improvement costs - (12)

Restructuring

Vision into Action - (22)

Americas Beverages separation costs - (4)

Fuel for Growth (27) -

Gumlink - (8)

Total spend (27) (46)

Treatment of restructuring from 2007

• Expect business improvement cost of c0.5% of revenue in underlying from 2007

# 2006 results have been re-presented to include Americas Beverages within discontinued operations

30

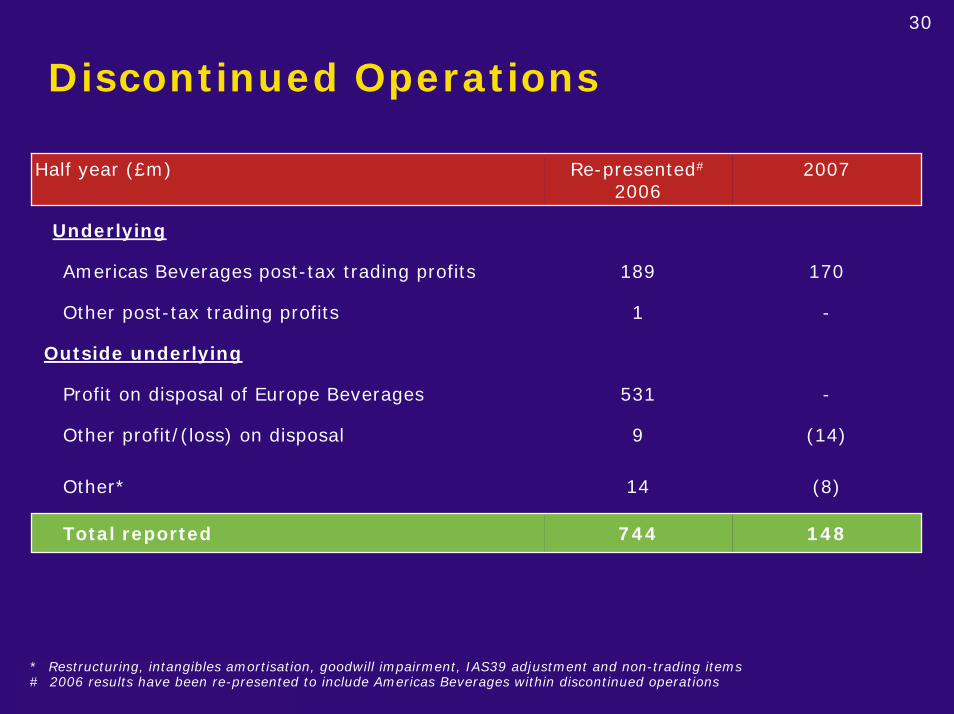

Discontinued Operations

Half year (£m) Re-presented#

20062007

Underlying

Americas Beverages post-tax trading profits 189 170

Other profit/(loss) on disposal 9 (14)

Other post-tax trading profits 1 -

Outside underlying

Other* 14 (8)

531

Total reported 744 148

Profit on disposal of Europe Beverages -

* Restructuring, intangibles amortisation, goodwill impairment, IAS39 adjustment and non-trading items# 2006 results have been re-presented to include Americas Beverages within discontinued operations

31

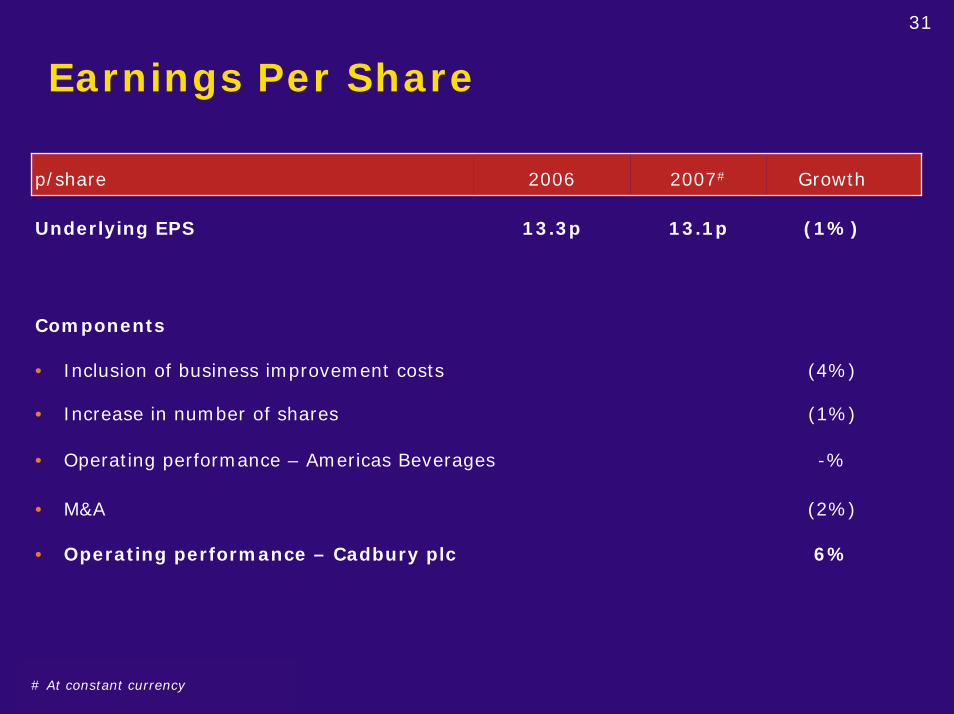

Earnings Per Share

p/share 2006 2007# Growth

Underlying EPS 13.3p 13.1p

• Operating performance – Americas Beverages -%

Components

• Inclusion of business improvement costs (4%)

• M&A (2%)

• Increase in number of shares (1%)

• Operating performance – Cadbury plc 6%

(1%)

# At constant currency

32

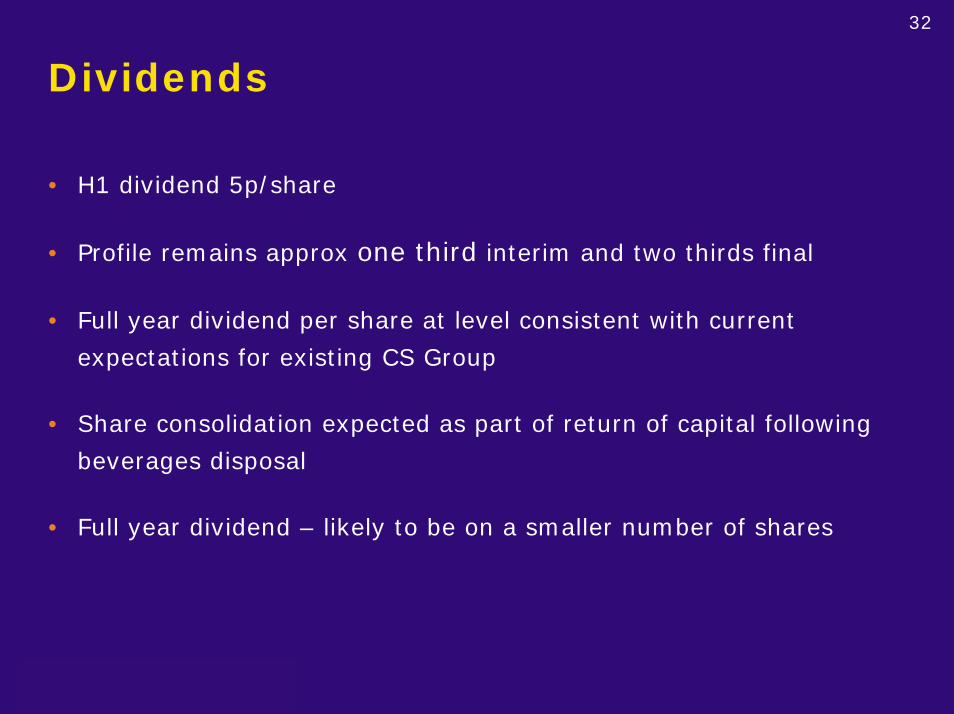

Dividends

• H1 dividend 5p/share

• Profile remains approx one third interim and two thirds final

• Full year dividend per share at level consistent with current

expectations for existing CS Group

• Share consolidation expected as part of return of capital following

beverages disposal

• Full year dividend – likely to be on a smaller number of shares

33

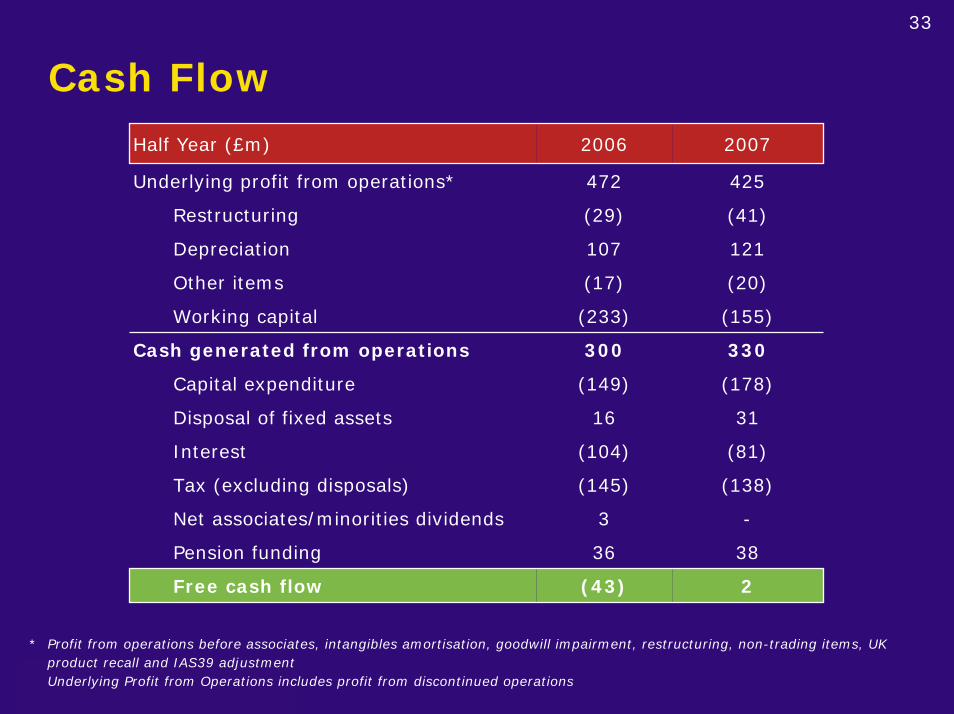

Cash FlowHalf Year (£m) 2006 2007

Underlying profit from operations* 472 425

Restructuring (29) (41)

Depreciation 107 121

Other items (17) (20)

Working capital (233) (155)

Tax (excluding disposals) (145) (138)

Net associates/minorities dividends 3 -

Cash generated from operations 300 330

Capital expenditure (149) (178)

Disposal of fixed assets 16 31

Interest (104) (81)

Pension funding 36 38

Free cash flow (43) 2

* Profit from operations before associates, intangibles amortisation, goodwill impairment, restructuring, non-trading items, UK product recall and IAS39 adjustmentUnderlying Profit from Operations includes profit from discontinued operations

34

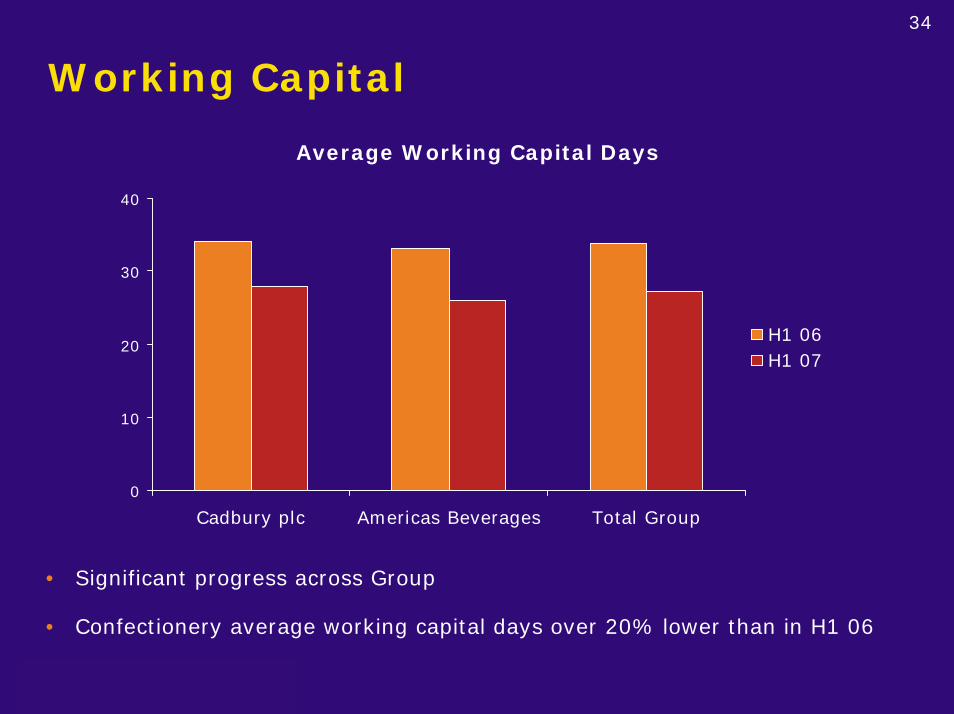

Working Capital

0

10

20

30

40

Cadbury plc Americas Beverages Total Group

H1 06H1 07

• Significant progress across Group

• Confectionery average working capital days over 20% lower than in H1 06

Average Working Capital Days

35

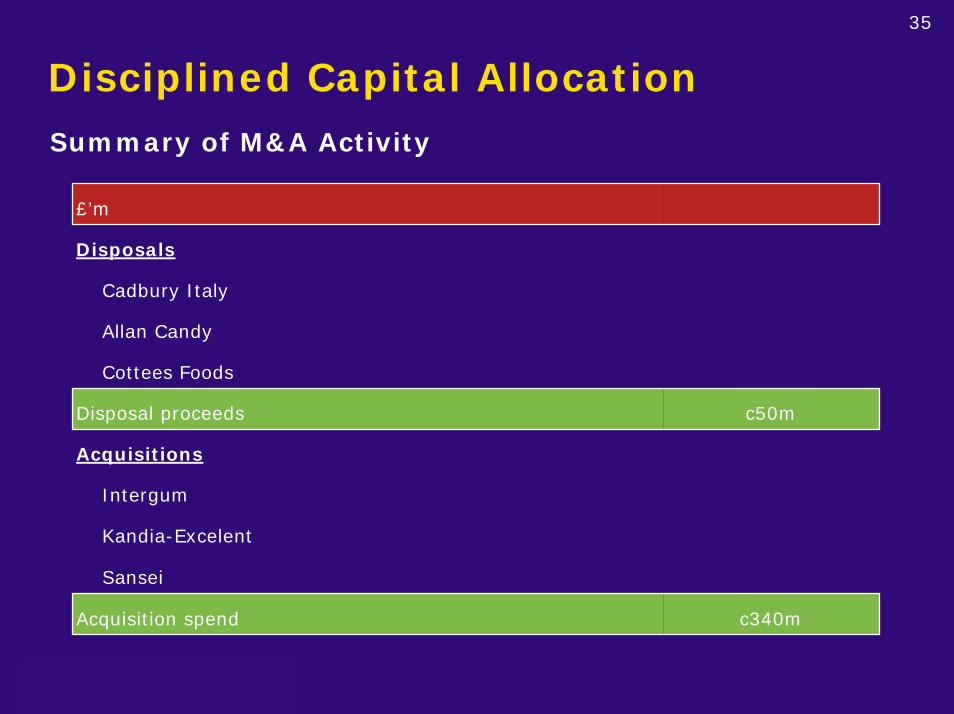

Disciplined Capital AllocationSummary of M&A Activity

£’m

Disposals

Cadbury Italy

Allan Candy

Intergum

Kandia-Excelent

Sansei

Cottees Foods

Disposal proceeds

Acquisitions

Acquisition spend

c50m

c340m

36

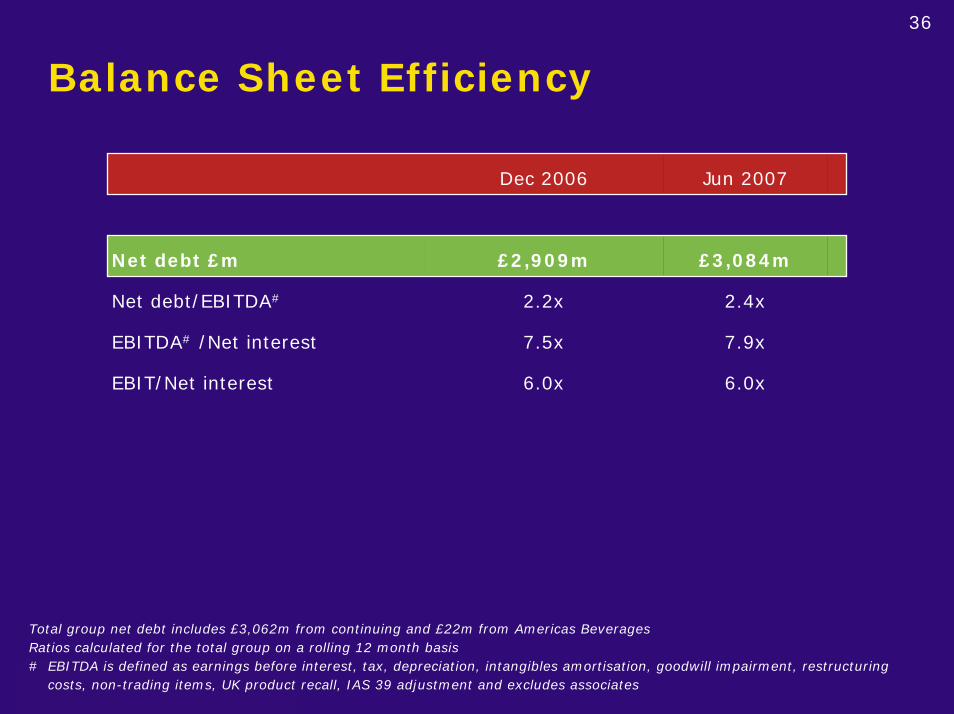

Balance Sheet Efficiency

Dec 2006 Jun 2007

£2,909m

2.2x

7.5x

EBIT/Net interest 6.0x 6.0x

Net debt £m £3,084m

EBITDA# /Net interest 7.9x

Net debt/EBITDA# 2.4x

Total group net debt includes £3,062m from continuing and £22m from Americas BeveragesRatios calculated for the total group on a rolling 12 month basis# EBITDA is defined as earnings before interest, tax, depreciation, intangibles amortisation, goodwill impairment, restructuring

costs, non-trading items, UK product recall, IAS 39 adjustment and excludes associates

37

2007 Outlook

• Regional overview

• Dairy costs

- Two thirds liquid; one third powdered

- Average 20% cost increase

- Pricing actions anticipated

38

BIMA - 2007 Factors

• UK business

- Full year of gum launch

- Lapping recall and hot summer in H2 06

- Sheffield flood

• Nigeria lapping full year accounting correction in H2 06

• Continuing strong momentum from Africa/Middle East

39

Europe - 2007 Factors

• Strong gum category momentum

• Good momentum and improving results in Russia

• Integrating Intergum and Kandia acquisitions

40

Americas - 2007 Factors

• Strong performance in H1

• Excellent category and share momentum

• Significant competitor activity in H2 behind new launches

41

Asia Pacific - 2007 Factors

• Making good progress

• Withdrawal from co-packing arrangement

• Aggressive ANZ retailer environment

• Political & economic uncertainty in Thailand

• Strong momentum from other emerging markets

42

Conclusion

• Key guidance factors since June 19

- Increase in dairy costs

- Flooding in Sheffield

• Material SG&A cost reductions start in 2008

• Continuing to invest behind growth

• Unlikely to report margin progression for the full year

• Business momentum remains strong

Supplementary Information

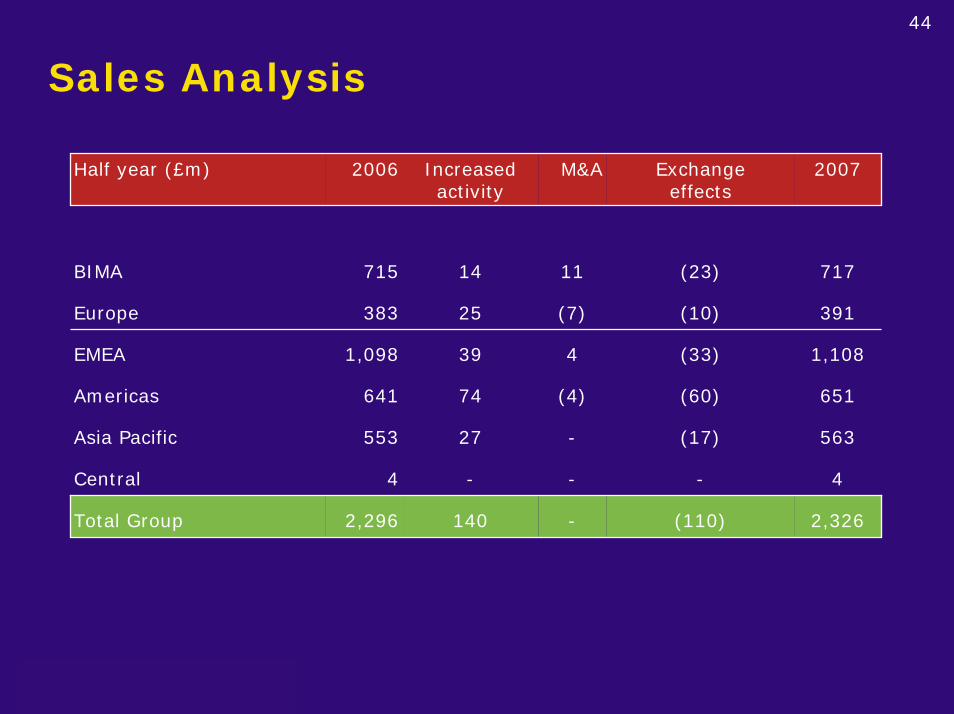

44

Sales Analysis

Half year (£m) 2006 Increasedactivity

M&A Exchange effects

2007

BIMA 715 14 11 (23) 717

Europe 383 25 (7) (10) 391

EMEA 1,098 39 4 (33) 1,108

Americas 641 74 (4) (60) 651

Asia Pacific 553 27 - (17) 563

Central 4 - - - 4

Total Group 2,296 140 - (110) 2,326

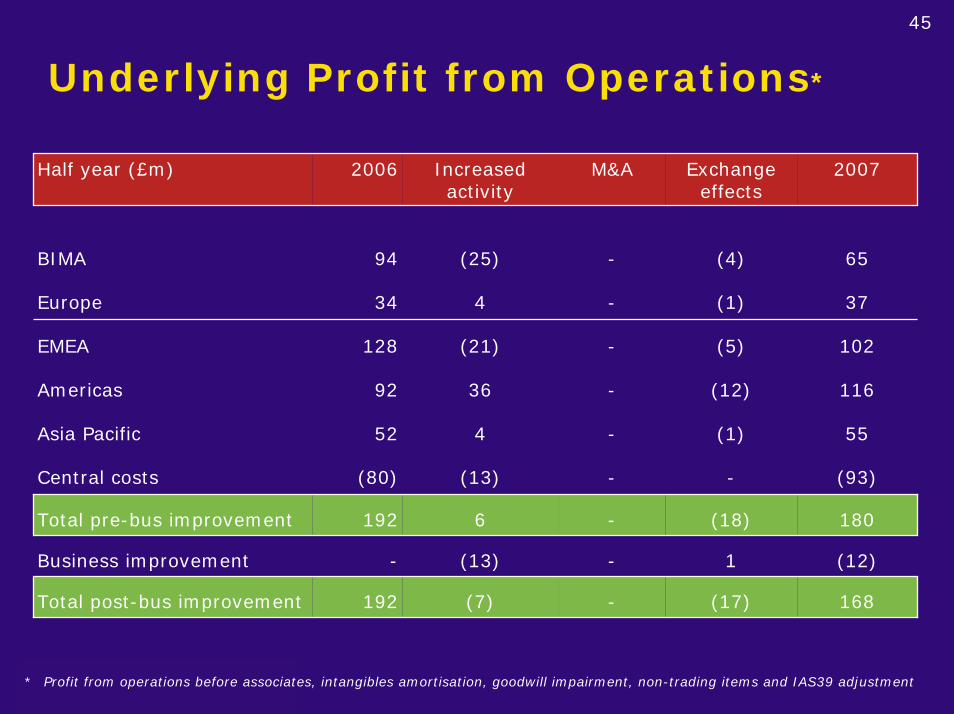

45

Underlying Profit from Operations*

Half year (£m) 2006 Increased activity

M&A Exchange effects

2007

BIMA 94 (25) - (4) 65

Europe 34 4 - (1) 37

EMEA 128 (21) - (5) 102

Americas 92 36 - (12) 116

Total pre-bus improvement 192 6 - (18) 180

Business improvement - (13) - 1 (12)

Asia Pacific 52 4 - (1) 55

Central costs (80) (13) - - (93)

Total post-bus improvement 192 (7) - (17) 168

* Profit from operations before associates, intangibles amortisation, goodwill impairment, non-trading items and IAS39 adjustment

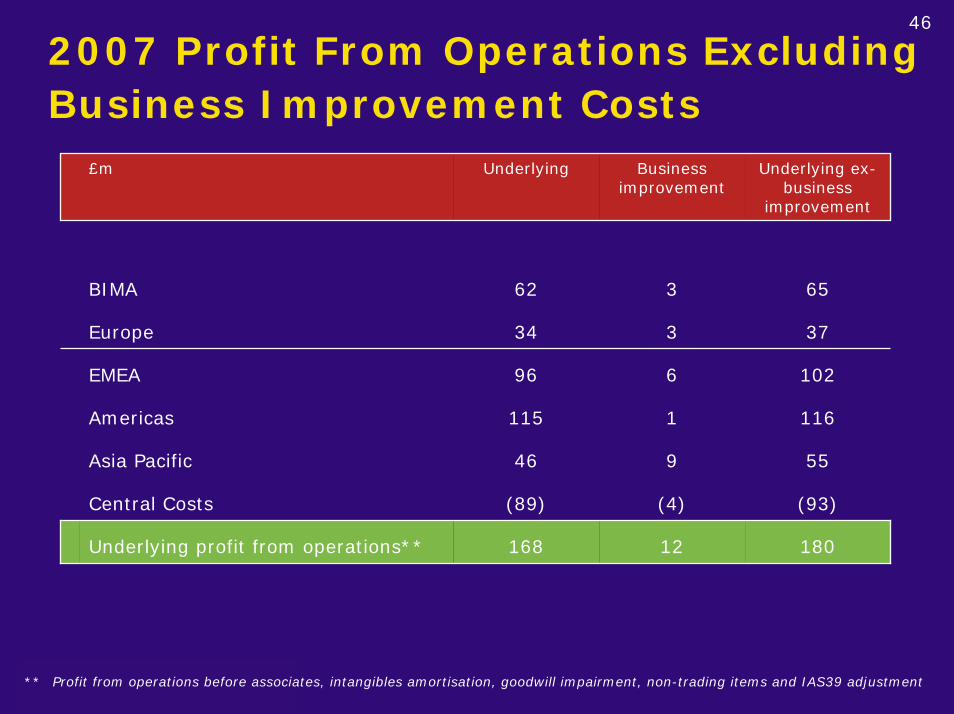

46

2007 Profit From Operations Excluding Business Improvement Costs

£m Underlying Business improvement

Underlying ex-business

improvement

Europe 34 3 37

BIMA 62 3 65

EMEA 96 6 102

Americas 115 1 116

Asia Pacific 46 9 55

Central Costs (89) (4) (93)

Underlying profit from operations** 168 12 180

** Profit from operations before associates, intangibles amortisation, goodwill impairment, non-trading items and IAS39 adjustment

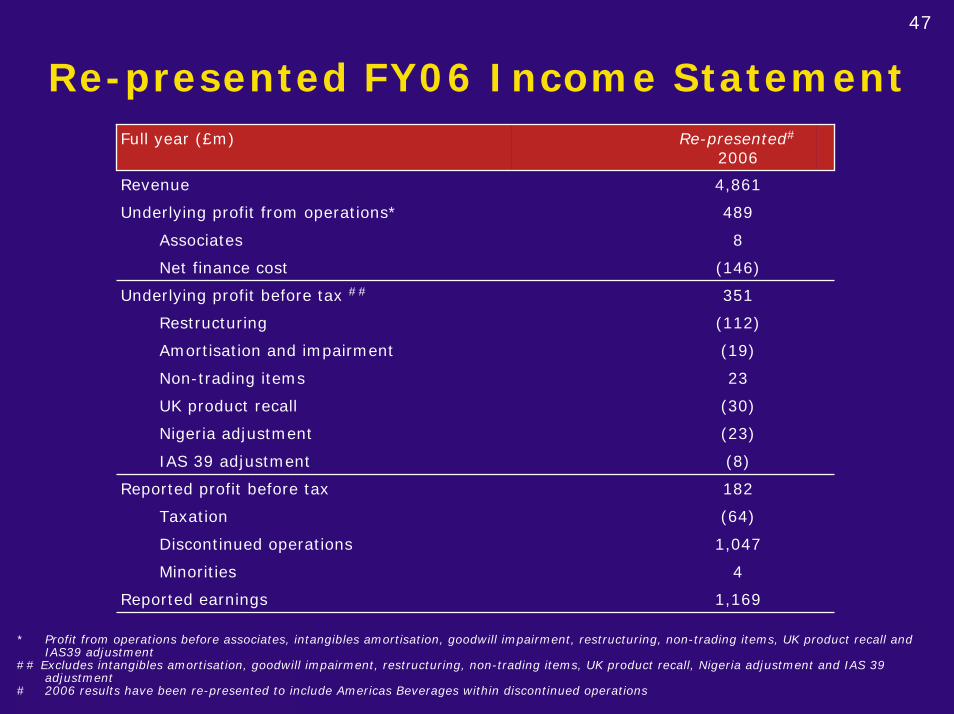

47

Re-presented FY06 Income StatementFull year (£m) Re-presented#

2006

Revenue 4,861

Non-trading items 23

UK product recall (30)

Underlying profit from operations* 489

Associates 8

Net finance cost (146)

Underlying profit before tax ## 351

Restructuring (112)

Amortisation and impairment (19)

Nigeria adjustment (23)

IAS 39 adjustment (8)

Reported profit before tax 182

Taxation (64)

Discontinued operations 1,047

Minorities 4

Reported earnings 1,169

* Profit from operations before associates, intangibles amortisation, goodwill impairment, restructuring, non-trading items, UK product recall and IAS39 adjustment

## Excludes intangibles amortisation, goodwill impairment, restructuring, non-trading items, UK product recall, Nigeria adjustment and IAS 39 adjustment

# 2006 results have been re-presented to include Americas Beverages within discontinued operations

48

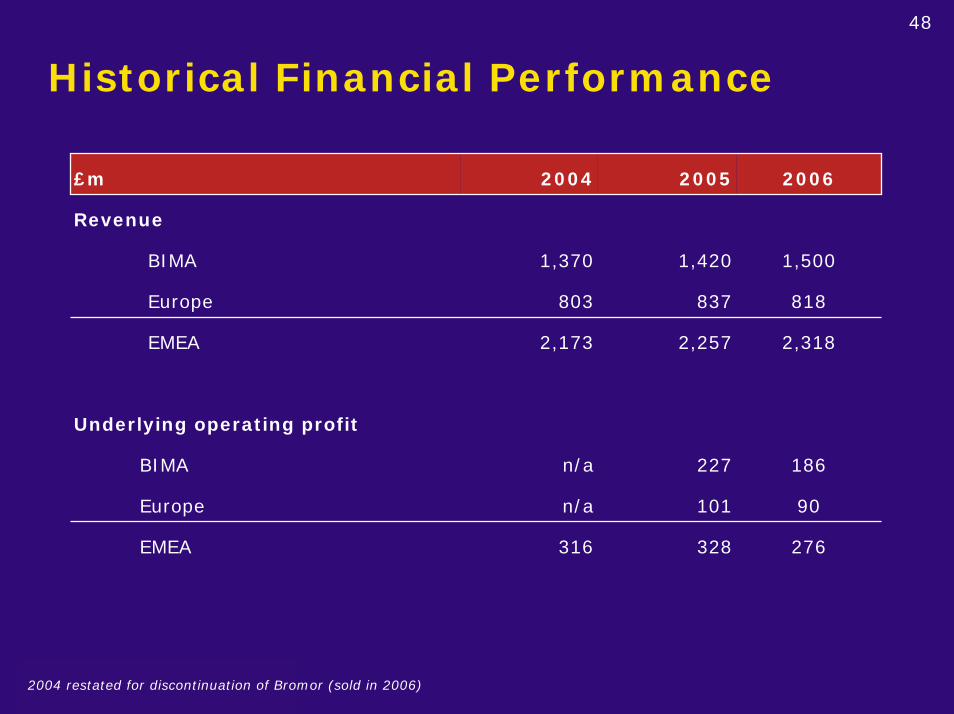

Historical Financial Performance

£m 2004 2005 2006

Revenue

BIMA 1,370 1,420 1,500

BIMA

Europe n/a 101 90

EMEA

803

EMEA 2,173 2,257 2,318

n/a 227 186

316 328 276

Europe 837 818

Underlying operating profit

2004 restated for discontinuation of Bromor (sold in 2006)

49

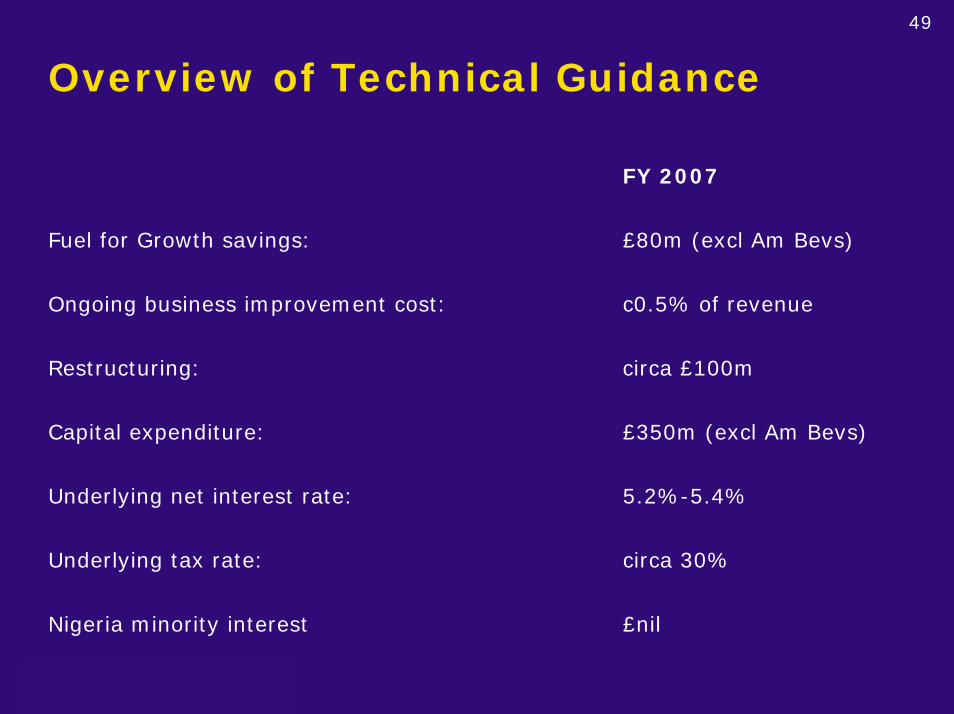

Overview of Technical Guidance

FY 2007

Fuel for Growth savings: £80m (excl Am Bevs)

Ongoing business improvement cost: c0.5% of revenue

Restructuring: circa £100m

Capital expenditure: £350m (excl Am Bevs)

Underlying net interest rate: 5.2%-5.4%

Underlying tax rate: circa 30%

Nigeria minority interest £nil

50

M&A Activity – Non-Core DisposalsCompleted

Cadbury Italy February 2007

Allan Candy (Canada) June 2007

Announced

Piasten (Germany) June 2005

Holland House Cooking Wines (US) December 2005

Grandma’s Molasses (US) January 2006

Europe Beverages Division February 2006

Slush Puppie (US) April 2006

Syria Beverages April 2006

Bromor (S. Africa) August 2006

Cottees Foods (Australia) July 2007

Monkhill (UK)

Americas Beverages (US)

51

M&A Activity – Confectionery Acquisitions

Completed

Sansei Foods (Japan) July 2007

Intergum (Turkey)

Green & Black’s (UK) May 2005

Cadbury Nigeria (majority) February 2006

30% Kent (Turkey) April 2006

Dan Products (S.Africa) June 2006

Announced

Kandia-Excelent (Romania) June 2007

52

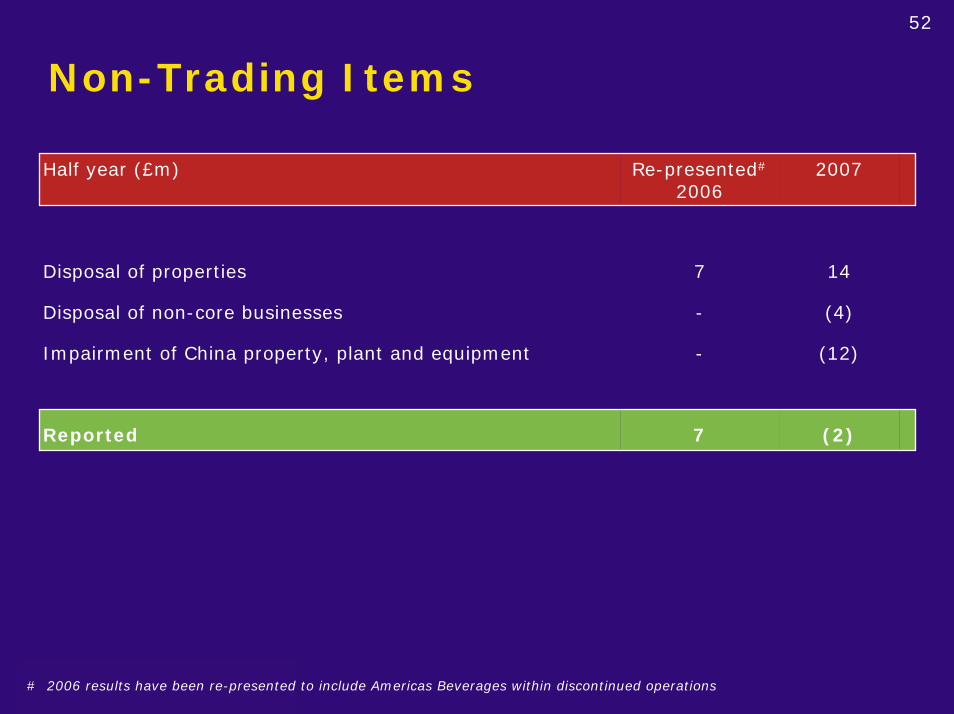

Non-Trading Items

Half year (£m) Re-presented#

20062007

Disposal of properties 7 14

Impairment of China property, plant and equipment - (12)

-

Reported 7 (2)

Disposal of non-core businesses (4)

# 2006 results have been re-presented to include Americas Beverages within discontinued operations

53

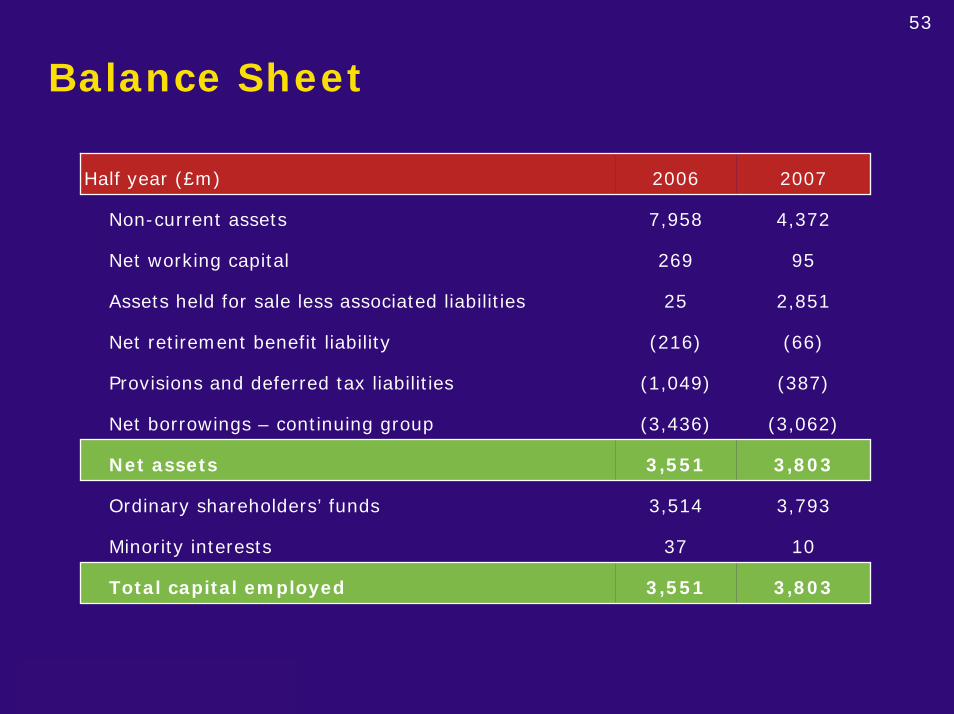

Balance Sheet

Half year (£m) 2006 2007

Non-current assets 7,958

269

25

Net retirement benefit liability (216) (66)

Provisions and deferred tax liabilities (1,049) (387)

Net borrowings – continuing group (3,436) (3,062)

Net assets 3,551 3,803

Ordinary shareholders’ funds 3,514 3,793

Minority interests 37 10

Total capital employed 3,551 3,803

4,372

Net working capital 95

Assets held for sale less associated liabilities 2,851

54

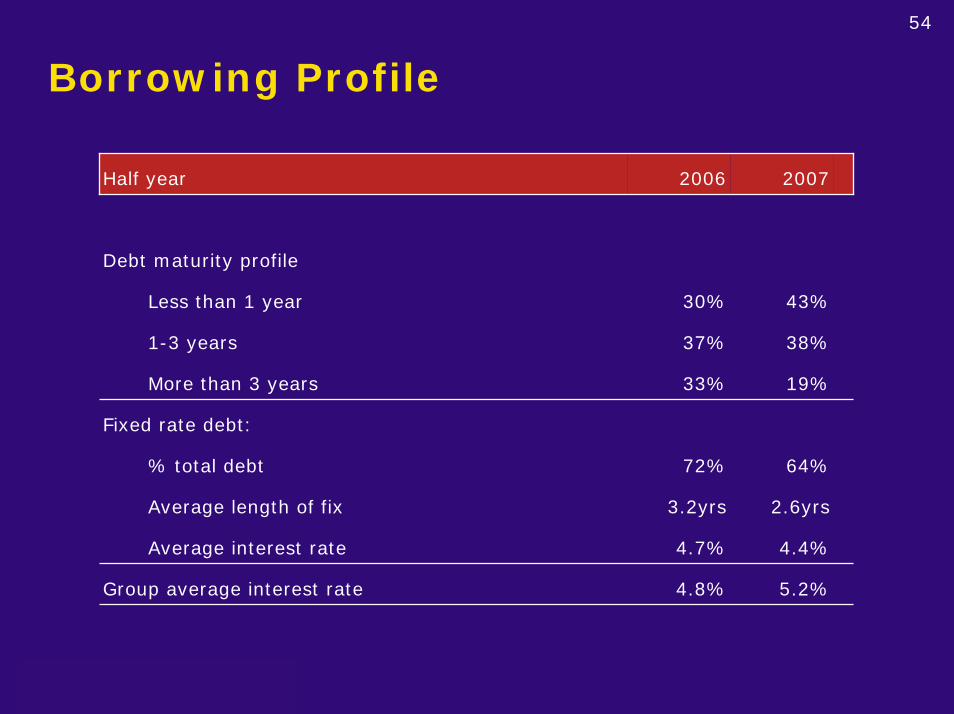

Borrowing Profile

Half year 2006 2007

30%

37%

33%

72%

3.2yrs

Average interest rate 4.7% 4.4%

Group average interest rate 4.8% 5.2%

More than 3 years 19%

Fixed rate debt:

% total debt 64%

Average length of fix 2.6yrs

Debt maturity profile

Less than 1 year 43%

1-3 years 38%

55

Sales, Profits and Borrowings by Currency

Half year (£m) 2007 %

Sales generated in:US dollars 244 11%Sterling 509 22%

Australian dollars 349 15%

Australian dollars 31 18%

Other (254) (8%)

Other 111 66%

Other 938 40%

Euro 286 12%

39(53)40

2,302551

Euro 463 15%

Euro 24%

Net borrowing held in:Dollar block 75%Sterling 18%

Underlying operating profit* generated in:US dollars 23%Sterling (31%)

* Profit from operations before associates, intangibles amortisation, goodwill impairment, restructuring, non-trading items and IAS39 adjustment

56

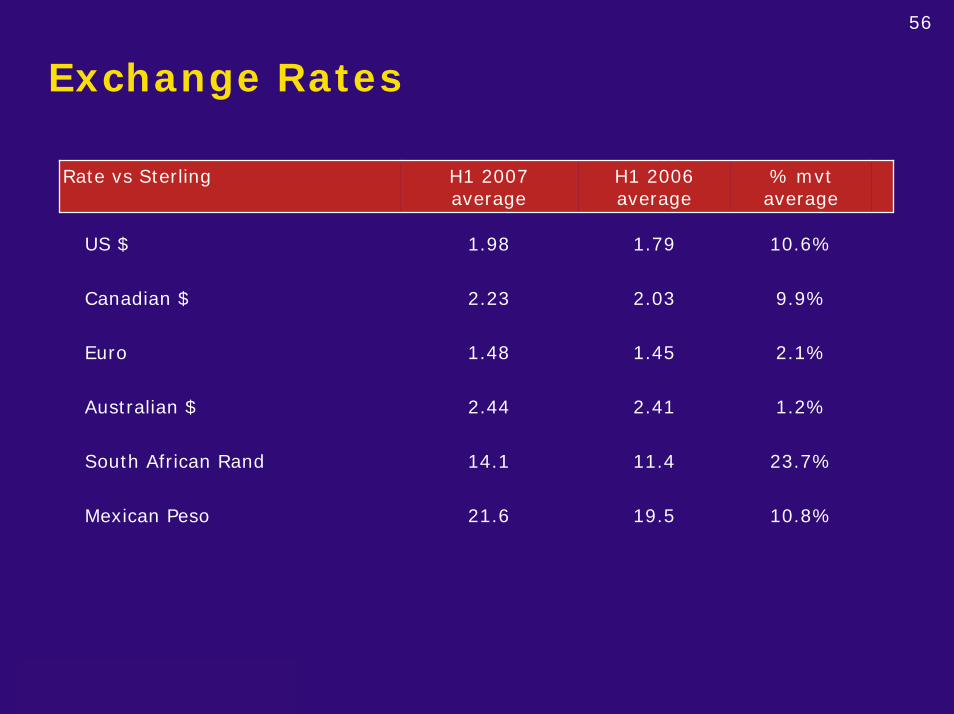

Exchange Rates

Rate vs Sterling H1 2007average

H1 2006average

% mvtaverage

US $ 1.98 1.79

2.03

1.45

2.41

South African Rand 14.1 11.4 23.7%

Mexican Peso 21.6 19.5 10.8%

10.6%

Canadian $ 2.23 9.9%

Euro 1.48 2.1%

Australian $ 2.44 1.2%

Closing Remarks

Todd StitzerChief Executive Officer

58

Summary and Conclusion

• Separation of beverages to focus on confectionery

• Significant under-exploited confectionery potential

• Step change in margins by reconfiguring confectionery business

model

• Focus on delivering aggressive SG&A reductions in 2008

• Revenues continue to benefit from investment in growth