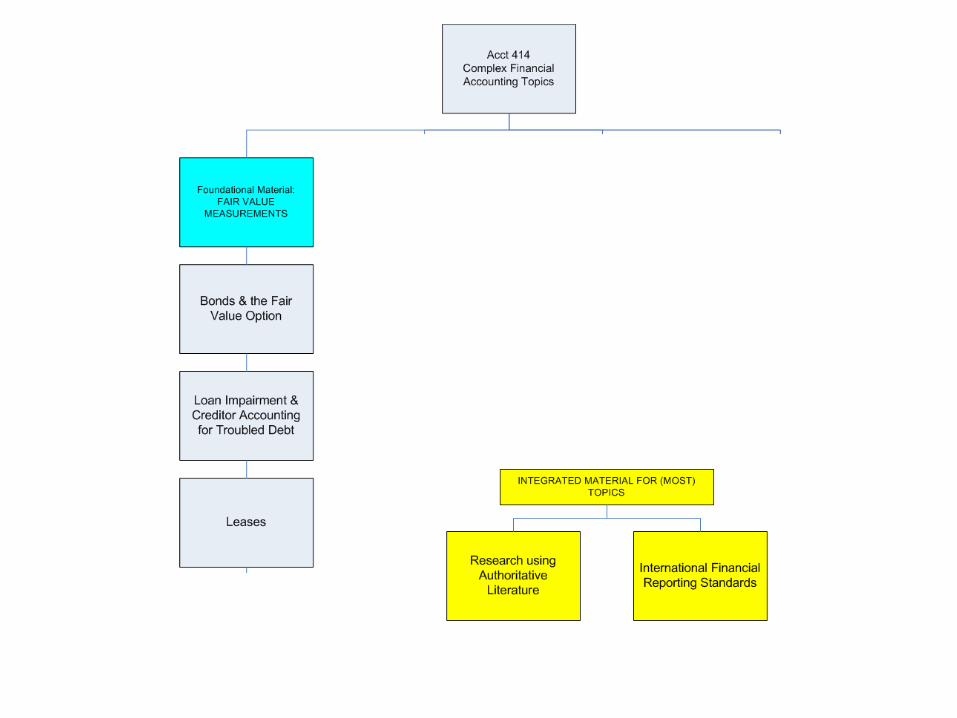

2 accounting for leases chapter 21 intermediate accounting 12th edition kieso, weygandt, and...

TRANSCRIPT

2

Accounting for LeasesAccounting for Leases

Chapter

21Intermediate Accounting

12th EditionKieso, Weygandt, and Warfield

Prepared by Coby Harmon, University of California, Santa Barbara

Introductory Lecture – Includes Flow Introductory Lecture – Includes Flow ChartsCharts

3

1. Explain the nature, economic substance, and advantages of lease transactions.

2. Describe the accounting criteria and procedures for capitalizing leases by the lessee.

3. Contrast the operating and capitalization methods of recording leases.

4. Identify the classifications of leases for the lessor.

5. Describe the lessor’s accounting for direct-financing leases.

6. Identify special features of lease arrangements that cause unique accounting problems.

7. Describe the effect of residual values, guaranteed and unguaranteed, on lease accounting.

8. Describe the lessor’s accounting for sales-type leases.

9. List the disclosure requirements for leases.

Learning ObjectivesLearning Objectives

4

Teresa’s Specific ObjectivesTeresa’s Specific Objectives

Be able to classify a lease from the perspective of lessor and lessee

Be able to prepare journal entries for lessor and lessee – for both operating and capital-type leases

Be able to research FARS to resolve complications not mentioned in text

6

The lease is a contractual agreement between the lessor and the lessee.

The lease gives the lessee the right to use specific property.

The lease specifies the duration of the lease and rental payments.

The obligations for taxes, insurance, and maintenance may be assumed by the lessor or the lessee.

7

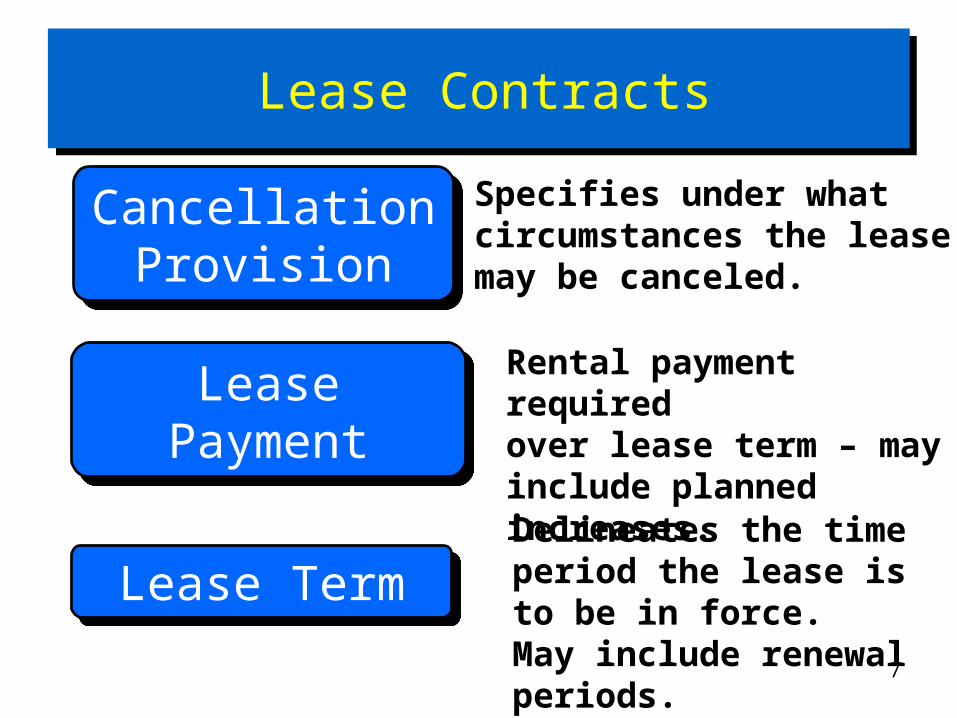

Lease ContractsLease Contracts

Cancellation Provision

Cancellation Provision

Specifies under whatcircumstances the leasemay be canceled.

Lease TermLease TermDelineates the time period the lease is to be in force. May include renewal periods.

Rental payment requiredover lease term – may include planned increases.

Lease PaymentLease Payment

8

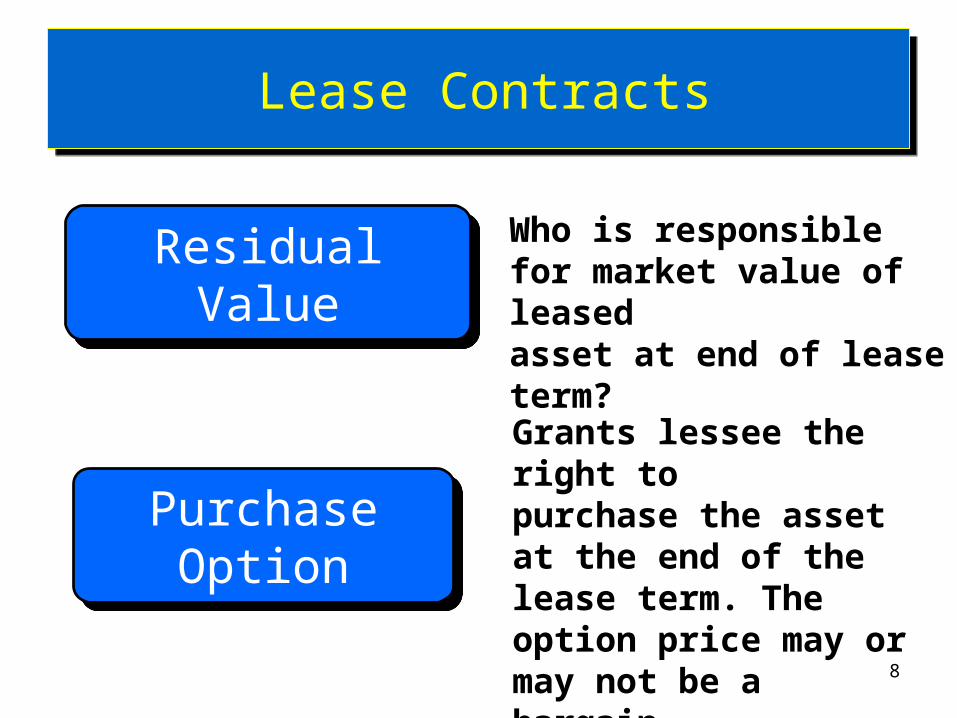

Lease ContractsLease Contracts

Residual ValueResidual Value Who is responsible for market value of leasedasset at end of lease term?

Purchase Option

Purchase Option

Grants lessee the right topurchase the asset at the end of the lease term. The option price may or may not be a bargain.

9

Other Terms You Will LearnOther Terms You Will Learn

Contingent rentals Bargain renewal option Bargain purchase option Nonrenewal penalty Guaranteed residual

value Interest rate implicit in the

lease

Unguaranteed residual value

Executory costs Initial direct costs Minimum lease payments Incremental borrowing

rate

10

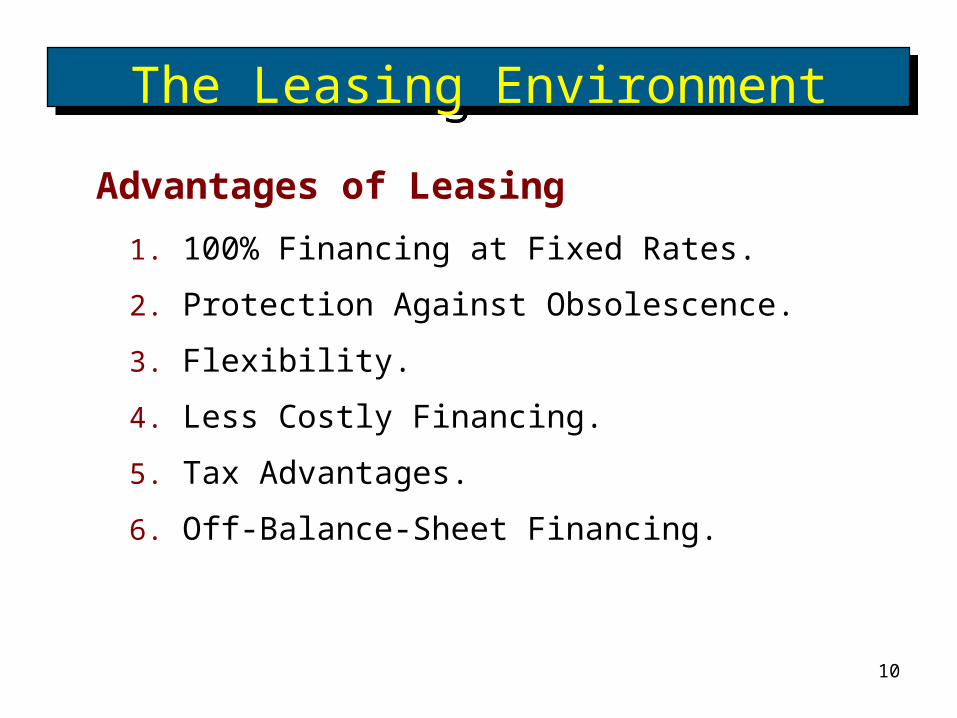

1. 100% Financing at Fixed Rates.

2. Protection Against Obsolescence.

3. Flexibility.

4. Less Costly Financing.

5. Tax Advantages.

6. Off-Balance-Sheet Financing.

The Leasing EnvironmentThe Leasing Environment

Advantages of Leasing

11

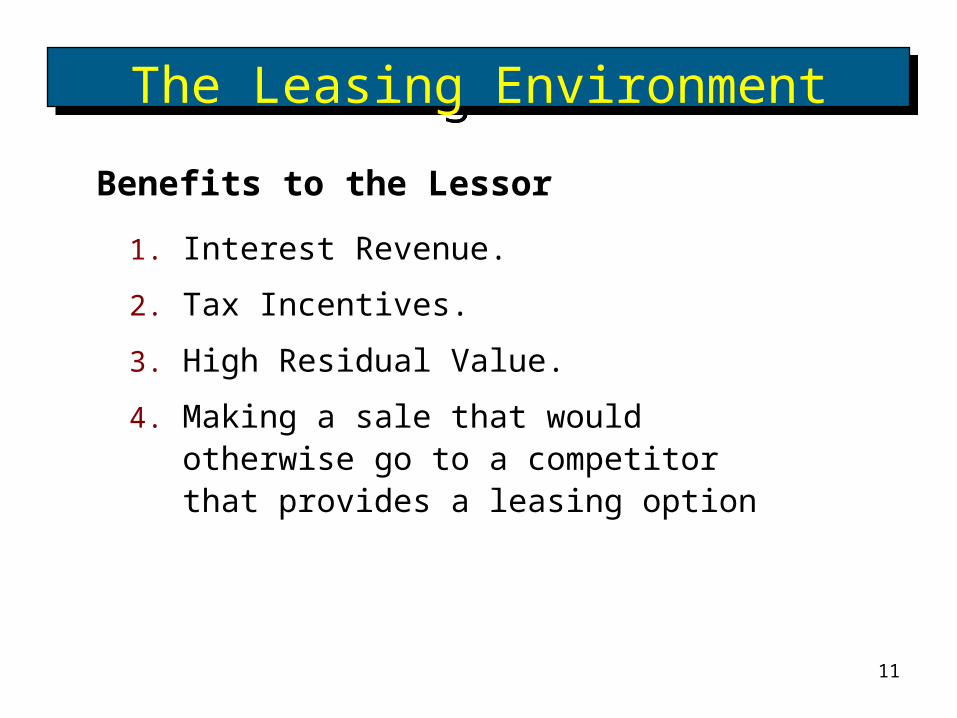

1. Interest Revenue.

2. Tax Incentives.

3. High Residual Value.

4. Making a sale that would otherwise go to a competitor that provides a leasing option

The Leasing EnvironmentThe Leasing Environment

Benefits to the Lessor

12

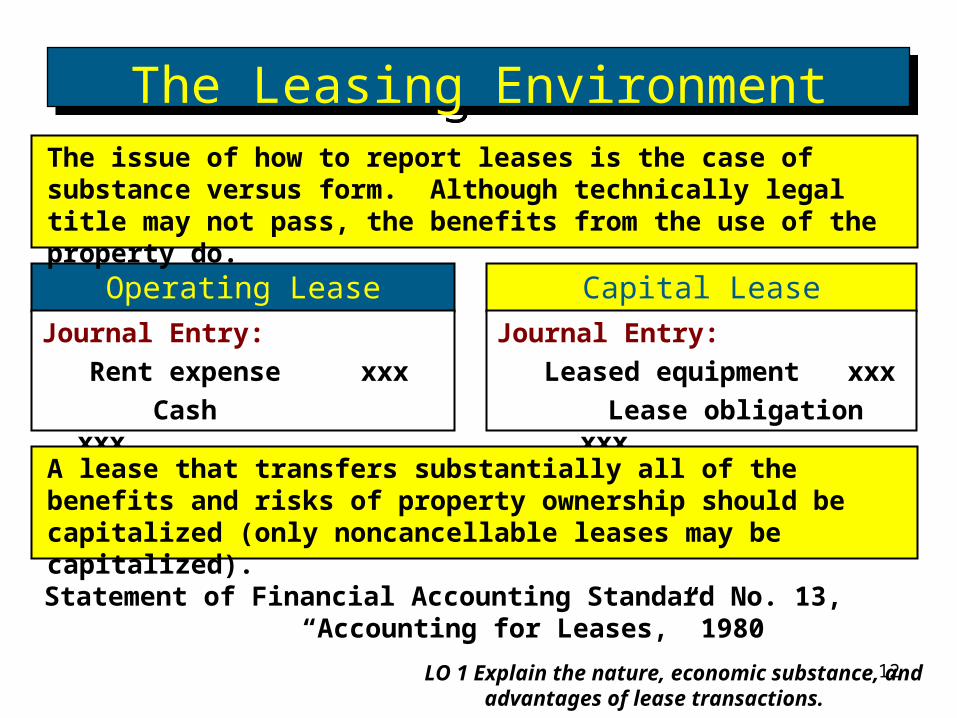

Operating Lease Capital LeaseJournal Entry: Rent expense xxx Cash xxx

Journal Entry: Leased equipment xxx Lease obligation

xxx

The issue of how to report leases is the case of substance versus form. Although technically legal title may not pass, the benefits from the use of the property do.

Statement of Financial Accounting Standard No. 13, “Accounting for Leases,” 1980

A lease that transfers substantially all of the benefits and risks of property ownership should be capitalized (only noncancellable leases may be capitalized).

The Leasing EnvironmentThe Leasing Environment

LO 1 Explain the nature, economic substance, and advantages of lease transactions.

13

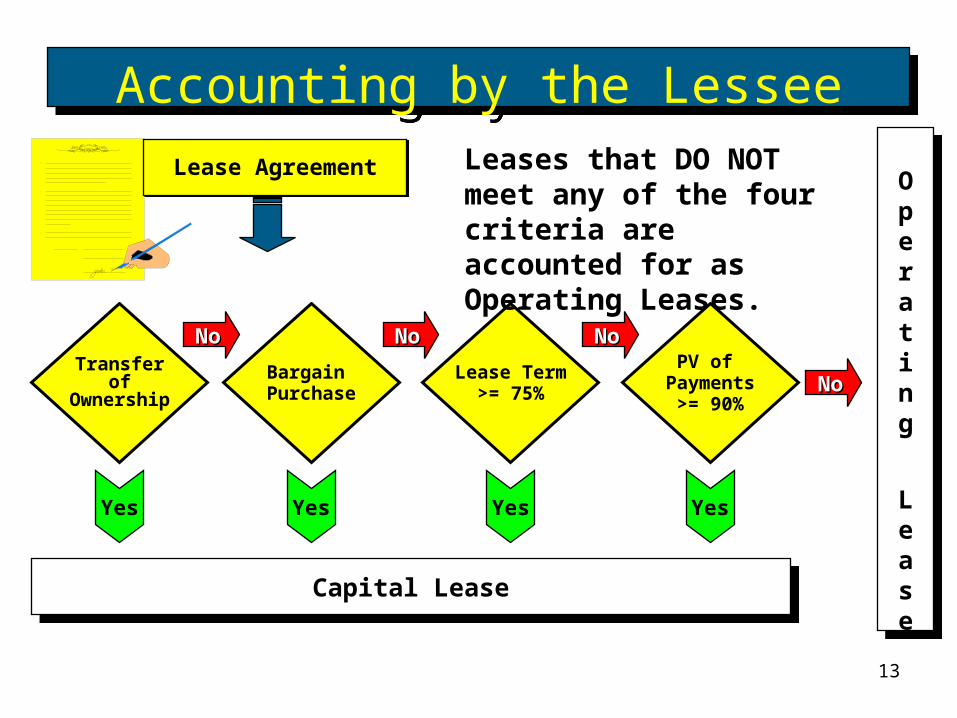

Transferof

Ownership

Bargain Purchase

Lease Term>= 75%

PV of Payments

>= 90%

Operat ing

Lease

NoNo NoNo NoNo

NoNo

Yes

Capital Lease

Lease Agreement

Yes Yes Yes

Leases that DO NOT meet any of the four criteria are accounted for as Operating Leases.

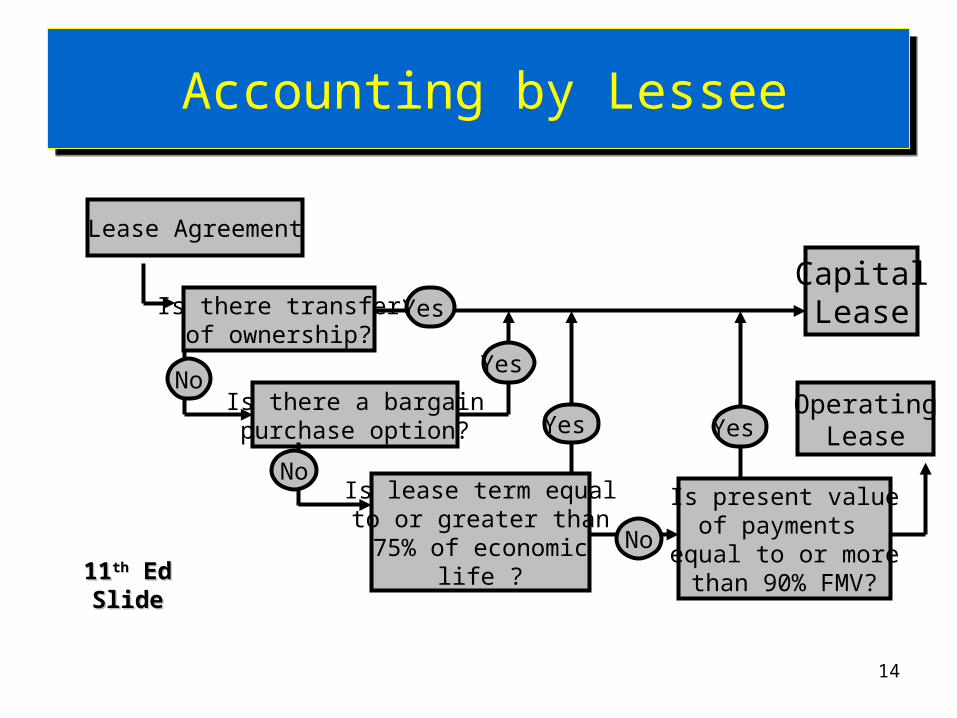

Accounting by the LesseeAccounting by the Lessee

14

Lease Agreement

Is there transferof ownership?

Yes

Is there a bargainpurchase option?

Yes No

Is lease term equalto or greater than75% of economic

life ?

Yes

No

CapitalLease

OperatingLease

Is present valueof payments

equal to or morethan 90% FMV?

Yes

No1111thth Ed Ed SlideSlide

Accounting by LesseeAccounting by Lessee

15

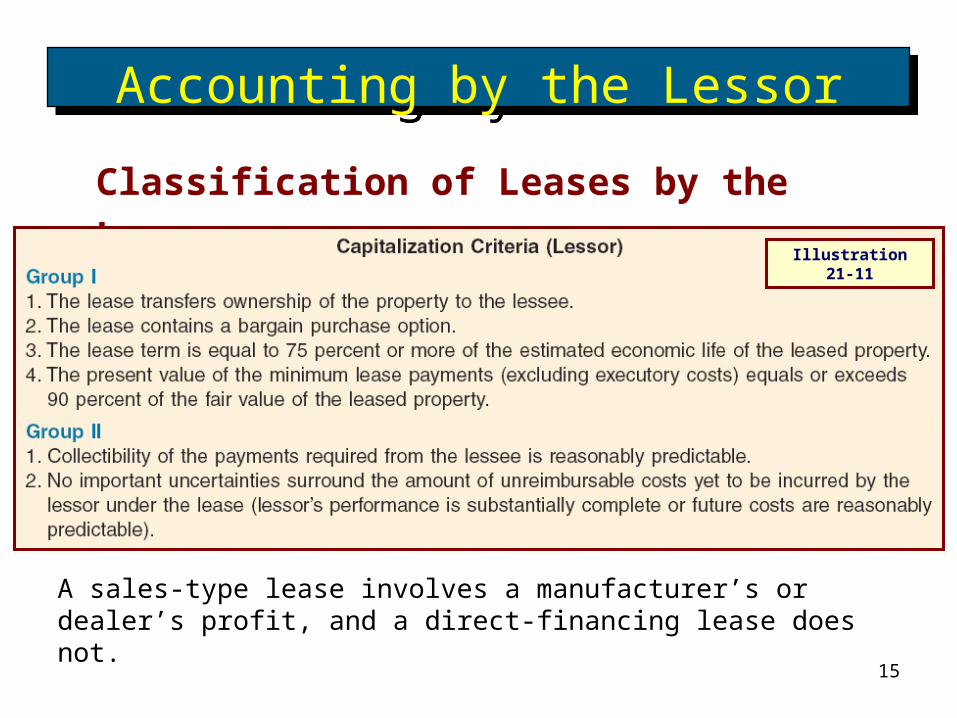

Classification of Leases by the Lessor

Accounting by the LessorAccounting by the Lessor

A sales-type lease involves a manufacturer’s or dealer’s profit, and a direct-financing lease does not.

Illustration 21-11

16

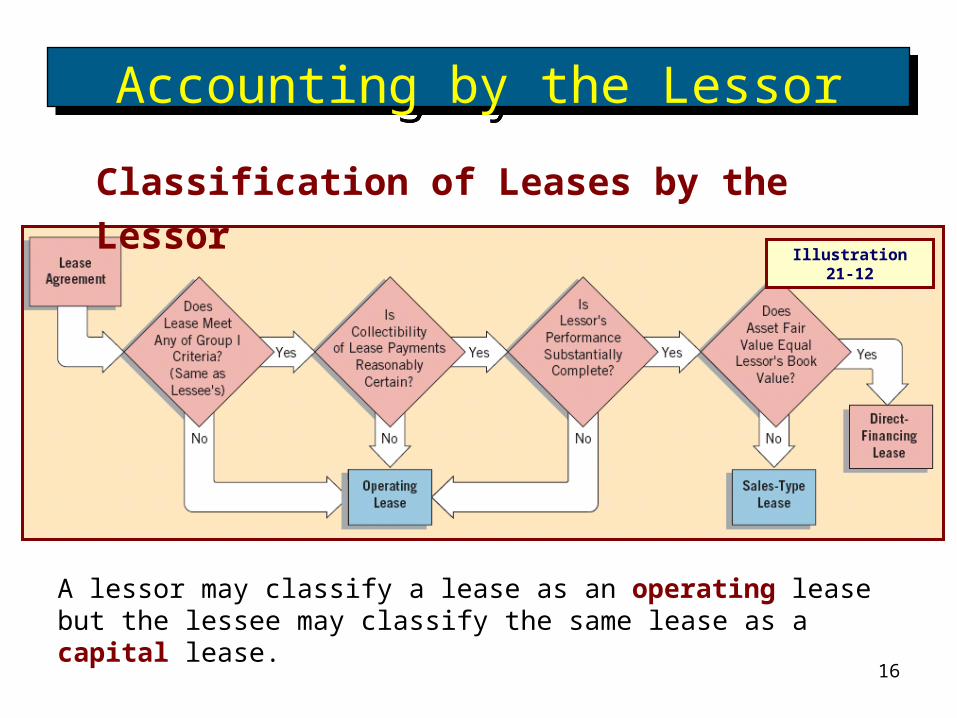

Classification of Leases by the Lessor

Accounting by the LessorAccounting by the Lessor

A lessor may classify a lease as an operating lease but the lessee may classify the same lease as a capital lease.

Illustration 21-12

17

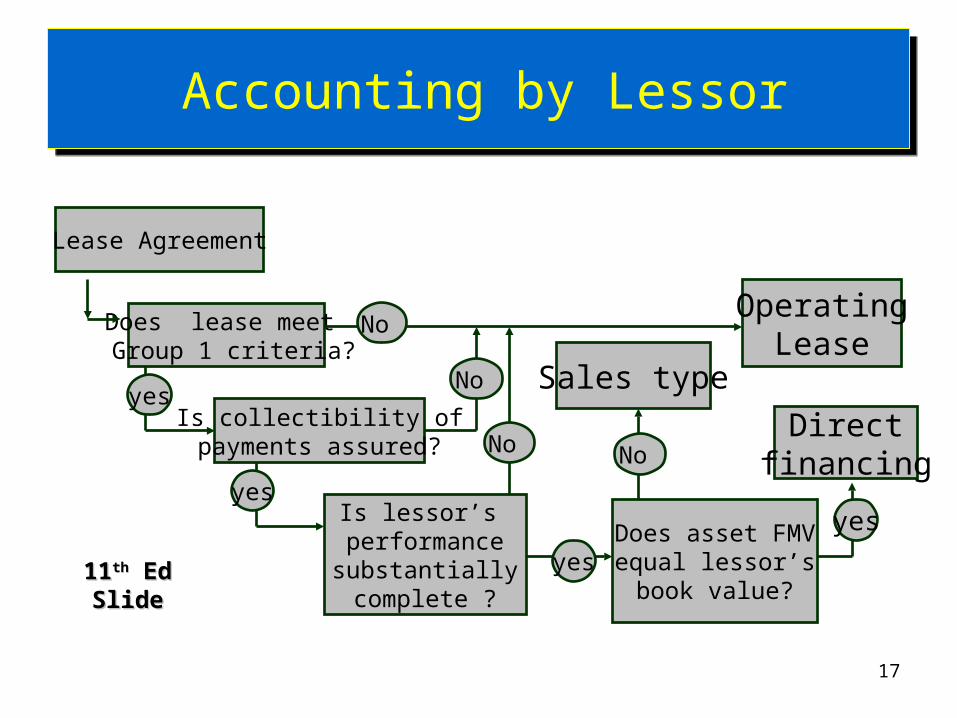

Lease Agreement

Does lease meet Group 1 criteria?

No

Is collectibility ofpayments assured?

No yes

Is lessor’s performancesubstantiallycomplete ?

No

yes

OperatingLease

Directfinancing

yes

yesDoes asset FMVequal lessor’sbook value?

No

Sales type

Accounting by LessorAccounting by Lessor

1111thth Ed Ed SlideSlide

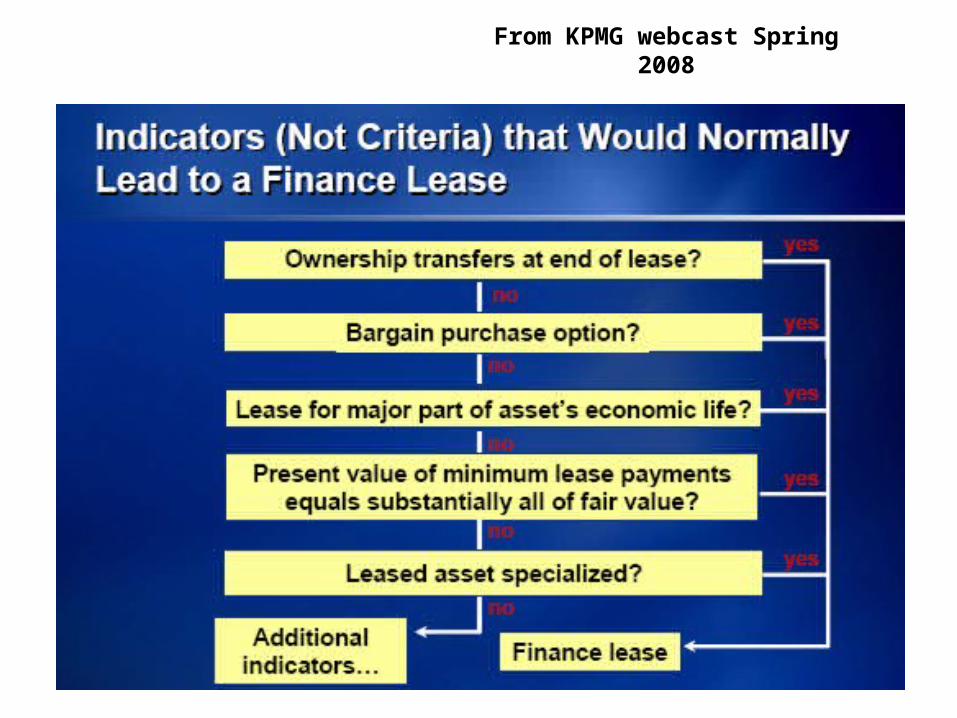

IFRS FLOWCHARTIFRS FLOWCHARTLater we’ll talk about International Financial Reporting Standards

18

From KPMG webcast Spring 2008