1q 2017 earnings presentation

TRANSCRIPT

Color

Scheme

234 93 46

109 179 63

235 235 235

0 75 141

253 185 36

Accent

Color

31 179 179

192 0 0

1Q17 Earnings Results Presentation

April 21, 2017

“This presentation contains forward-looking statements. These statements are made under the “safe harbor” provisions established

by the U.S. Private Securities Litigation Reform Act of 1995. Forward-looking statements involve inherent risks and uncertainties.

The forward-looking statements in this presentation reflect the expectations of the Bank’s management and are based on currently

available data; however, actual experience with respect to these factors is subject to future events and uncertainties, which could

materially impact the Bank’s expectations. A number of factors could cause actual performance and results to differ materially from

those contained in any forward-looking statement, including but not limited to the following: the anticipated growth of the Bank’s

credit portfolio, including its trade finance portfolio; the continuation of the Bank’s preferred creditor status; the impact of increasing

interest rates and of the macroeconomic environment in the Region on the Bank’s financial condition; the execution of the Bank’s

strategies and initiatives, including its revenue diversification strategy; the adequacy of the Bank’s allowance for credit losses; the

need for additional provisions for credit losses; the Bank’s ability to achieve future growth, the Bank’s ability to reduce its liquidity

levels and increase its leverage; the Bank’s ability to maintain its investment-grade credit ratings; the availability and mix of future

sources of funding for the Bank’s lending operations; potential trading losses; the possibility of fraud; and the adequacy of the

Bank’s sources of liquidity to replace large deposit withdrawals.”

2

Financial Performance Overview

Stronger than usual seasonality in credit demand in most of the Region during

1Q17, with abundant liquidity available

Overall economic performance of the Region appears to have hit bottom; base

case scenario points to moderate recovery in 2017

WTO trade leading indicators (container shipping throughput, world export

orders and GDP estimates) are up in the early months of 2017

Pacific Alliance countries remain growth focus for Bladex amidst stiff

competition. Making headway in Mexico, where economy remains strong

LatAm debt capital markets have rebounded with significant appetite for strong

names

Environment Highlights

3

Financial Performance Overview

Profit of $23.5 MM up 76% vs. previous quarter (stable YoY), on lower provisions for expected

credit losses (“ECL”) and enhanced efficiency

Fees & other income up +31% YoY and -22% QoQ on improved and more diversified client

demand in L/C business. No closings in the loan structuring and syndication business during the

quarter, with several transactions slated for completion in 2Q, and during the second half of the

year

Resilient NIM at 2.02% (-3bps QoQ and -4bps YoY) despite shorter tenors, and de-risking

measures over the last several quarters, mitigated by increased market rates (LIBOR) and stable

funding spreads

Average loan portfolio (-9% QoQ and -11% YoY) reflects both stronger than usual seasonality in

market demand in most of the Region, and continued efforts to reduce risk concentrations.

Deposit balances reached $3.2B, up +14% QoQ and +4% YoY, representing 53% of total liabilities

Non-performing loan portfolio (NPL) was stable at $65.4 MM QoQ compared to $28.0 MM as of

1Q16. 1Q17 provisions for ECL reflect ongoing protracted restructuring proceedings

Reserve coverage ratio increased to 1.89% (+16 bps QoQ; +49 bps YoY) on incremental

provisions for ECL and lower Commercial Portfolio balances

Bladex Board of Directors declared a $0.385/share quarterly dividend, representing an attractive

yield (5.5%)

1Q17 Results Highlights

4

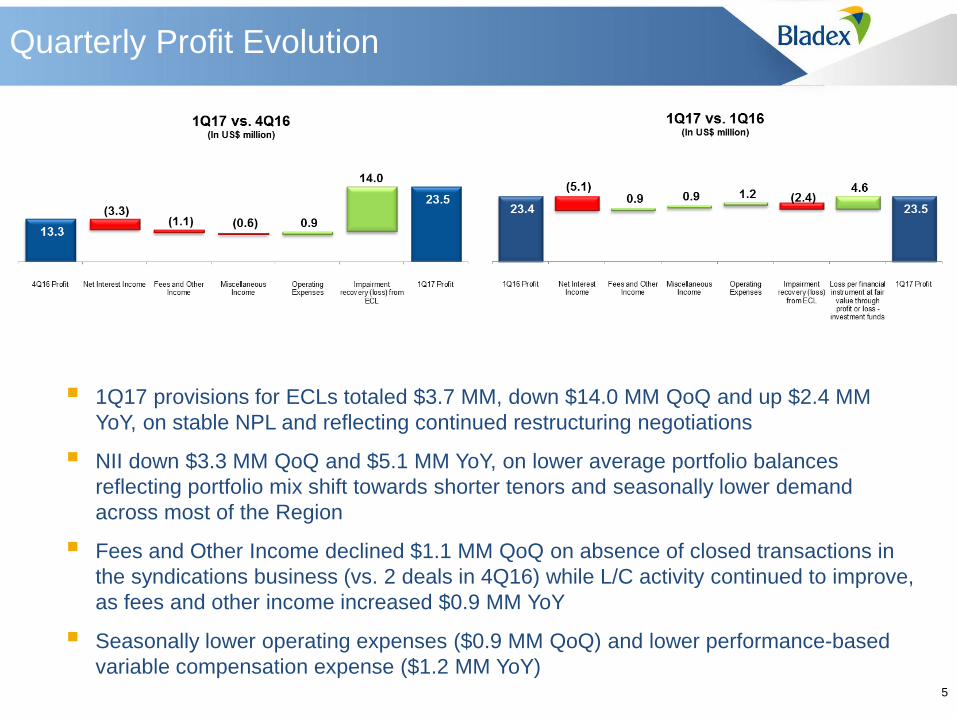

1Q17 provisions for ECLs totaled $3.7 MM, down $14.0 MM QoQ and up $2.4 MM

YoY, on stable NPL and reflecting continued restructuring negotiations

NII down $3.3 MM QoQ and $5.1 MM YoY, on lower average portfolio balances

reflecting portfolio mix shift towards shorter tenors and seasonally lower demand

across most of the Region

Fees and Other Income declined $1.1 MM QoQ on absence of closed transactions in

the syndications business (vs. 2 deals in 4Q16) while L/C activity continued to improve,

as fees and other income increased $0.9 MM YoY

Seasonally lower operating expenses ($0.9 MM QoQ) and lower performance-based

variable compensation expense ($1.2 MM YoY) 5

Quarterly Profit Evolution

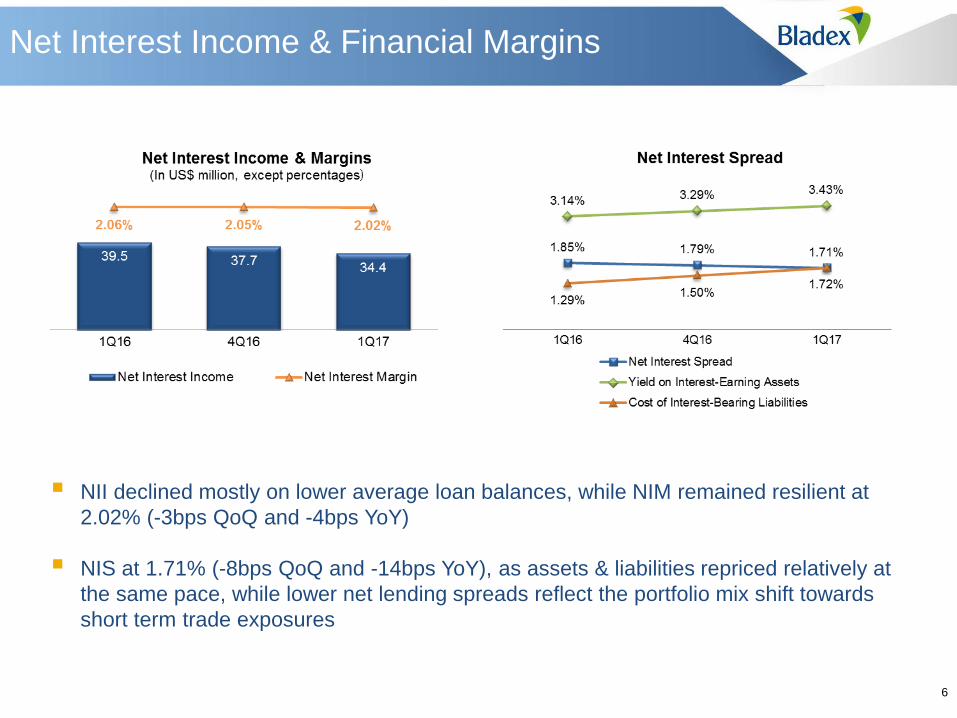

NII declined mostly on lower average loan balances, while NIM remained resilient at

2.02% (-3bps QoQ and -4bps YoY)

NIS at 1.71% (-8bps QoQ and -14bps YoY), as assets & liabilities repriced relatively at

the same pace, while lower net lending spreads reflect the portfolio mix shift towards

short term trade exposures

6

Net Interest Income & Financial Margins

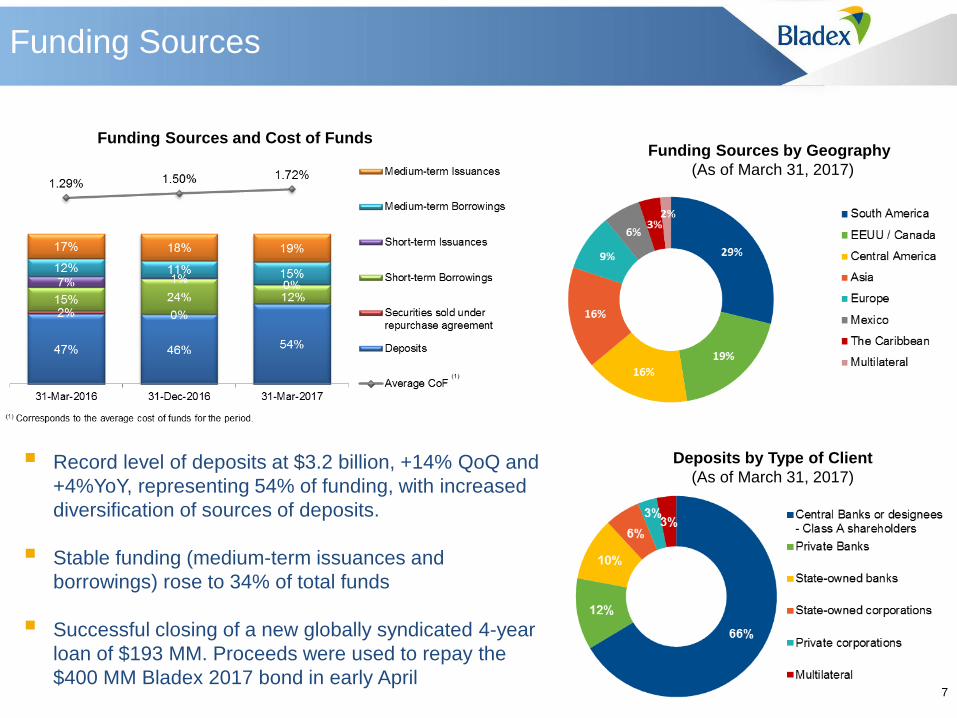

Record level of deposits at $3.2 billion, +14% QoQ and

+4%YoY, representing 54% of funding, with increased

diversification of sources of deposits.

Stable funding (medium-term issuances and

borrowings) rose to 34% of total funds

Successful closing of a new globally syndicated 4-year

loan of $193 MM. Proceeds were used to repay the

$400 MM Bladex 2017 bond in early April

Funding Sources and Cost of Funds

Deposits by Type of Client

(As of March 31, 2017)

Funding Sources by Geography

(As of March 31, 2017)

Funding Sources

7

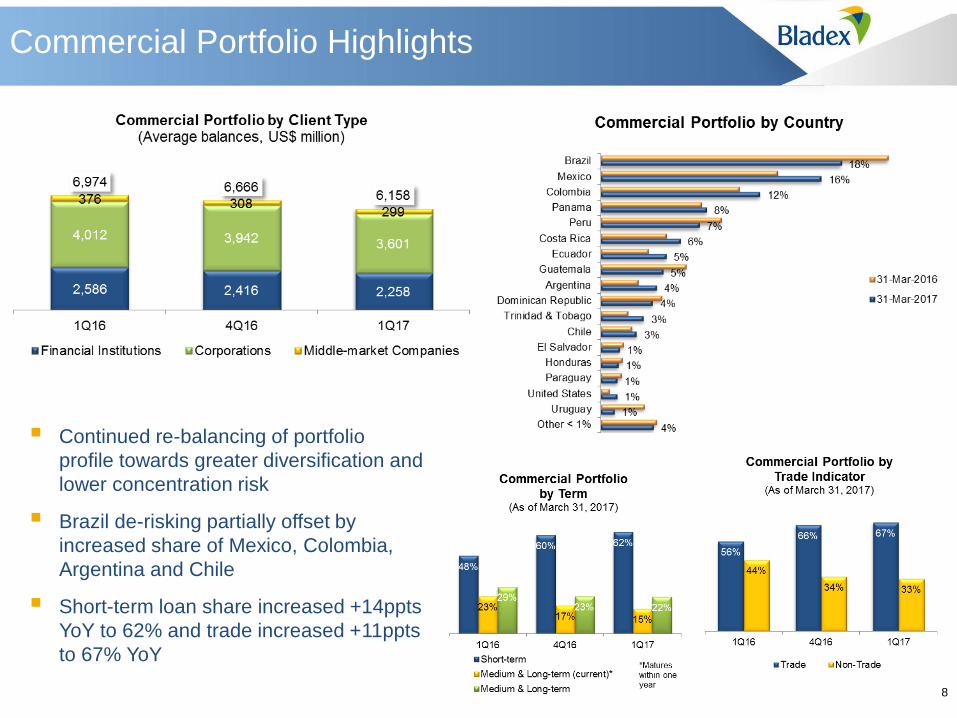

Continued re-balancing of portfolio

profile towards greater diversification and

lower concentration risk

Brazil de-risking partially offset by

increased share of Mexico, Colombia,

Argentina and Chile

Short-term loan share increased +14ppts

YoY to 62% and trade increased +11ppts

to 67% YoY

8

Commercial Portfolio Highlights

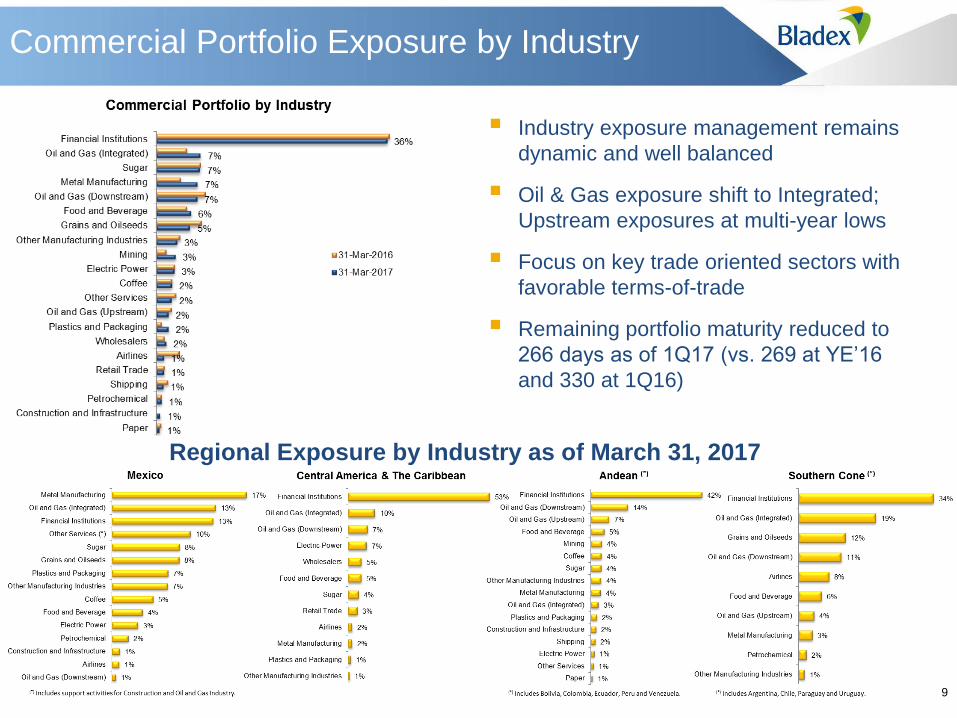

Industry exposure management remains

dynamic and well balanced

Oil & Gas exposure shift to Integrated;

Upstream exposures at multi-year lows

Focus on key trade oriented sectors with

favorable terms-of-trade

Remaining portfolio maturity reduced to

266 days as of 1Q17 (vs. 269 at YE’16

and 330 at 1Q16)

Regional Exposure by Industry as of March 31, 2017

9

Commercial Portfolio Exposure by Industry

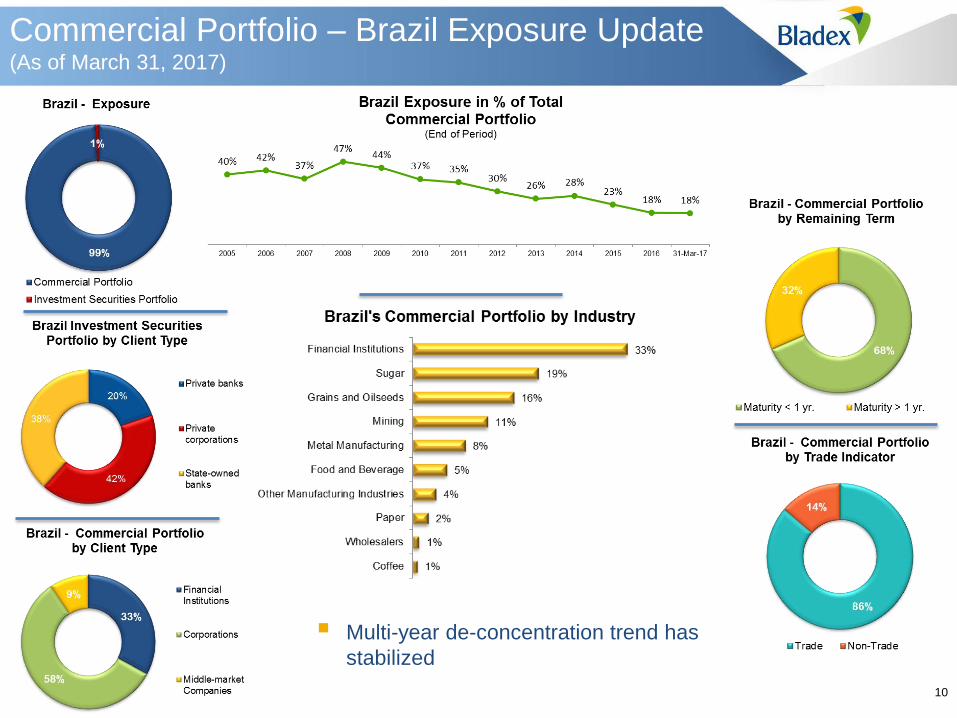

Multi-year de-concentration trend has

stabilized

10

Commercial Portfolio – Brazil Exposure Update (As of March 31, 2017)

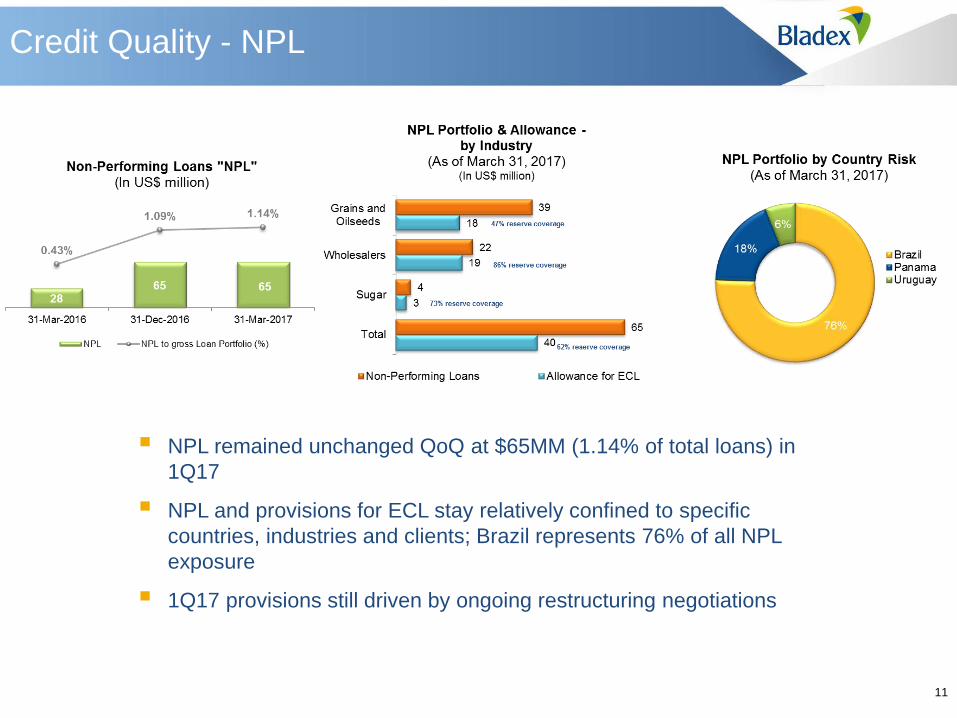

NPL remained unchanged QoQ at $65MM (1.14% of total loans) in

1Q17

NPL and provisions for ECL stay relatively confined to specific

countries, industries and clients; Brazil represents 76% of all NPL

exposure

1Q17 provisions still driven by ongoing restructuring negotiations

11

Credit Quality - NPL

IFRS Rule 9 - Stage 1: Collectively assessed performing exposures based on 12-

month ECL; IFRS Rule 9 - Stage 2: Performing exposures assessed based on

lifetime ECL; IFRS Rule 9 - Stage 3: Credit-impaired financial assets (“NPL”) based

on lifetime ECL

Total allowance for ECL on loans of

$109.9MM, an increase of $3.9MM QoQ,

explained by:

- (+) Higher provision for NPL (Stage 3)

reflecting ongoing restructurings

- (+) Higher provision for performing loans

on lifetime expected losses (Stage 2)

- (-) Lower requirement for performing

loans on 12-month expected losses

(Stage 1), on decreased loan balances

12

Credit Quality - Allowances

QoQ Variation:

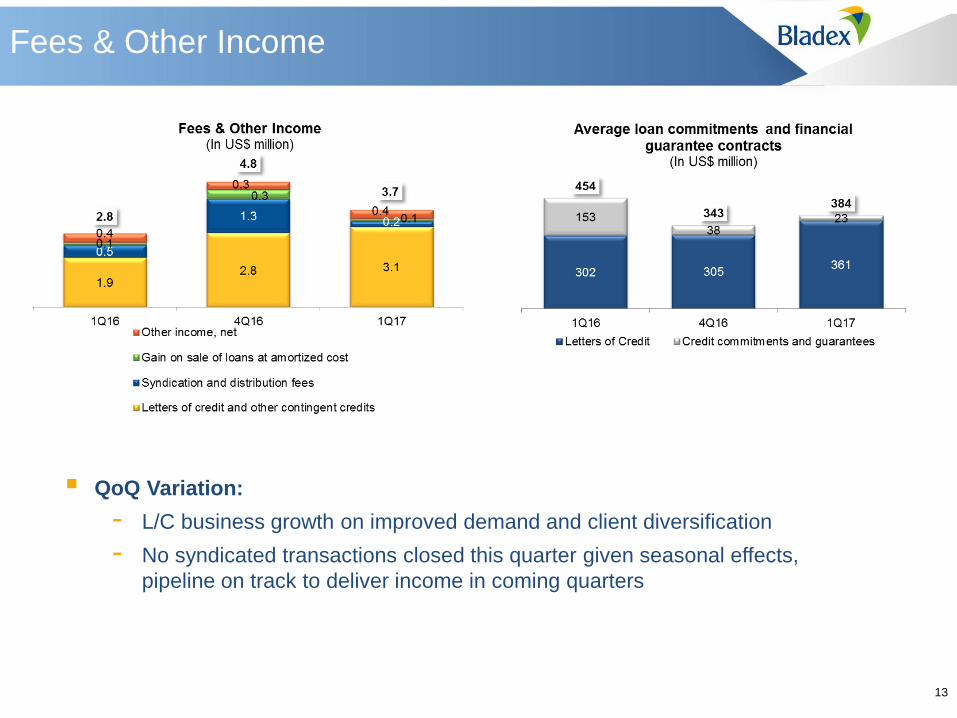

- L/C business growth on improved demand and client diversification

- No syndicated transactions closed this quarter given seasonal effects,

pipeline on track to deliver income in coming quarters

13

Fees & Other Income

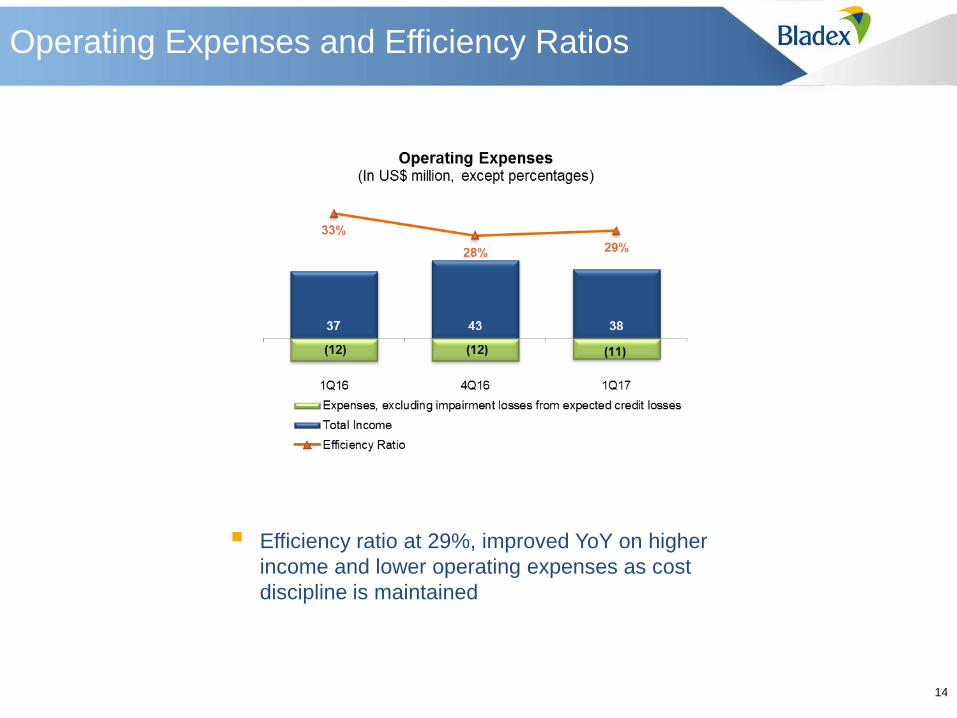

Efficiency ratio at 29%, improved YoY on higher

income and lower operating expenses as cost

discipline is maintained

14

Operating Expenses and Efficiency Ratios

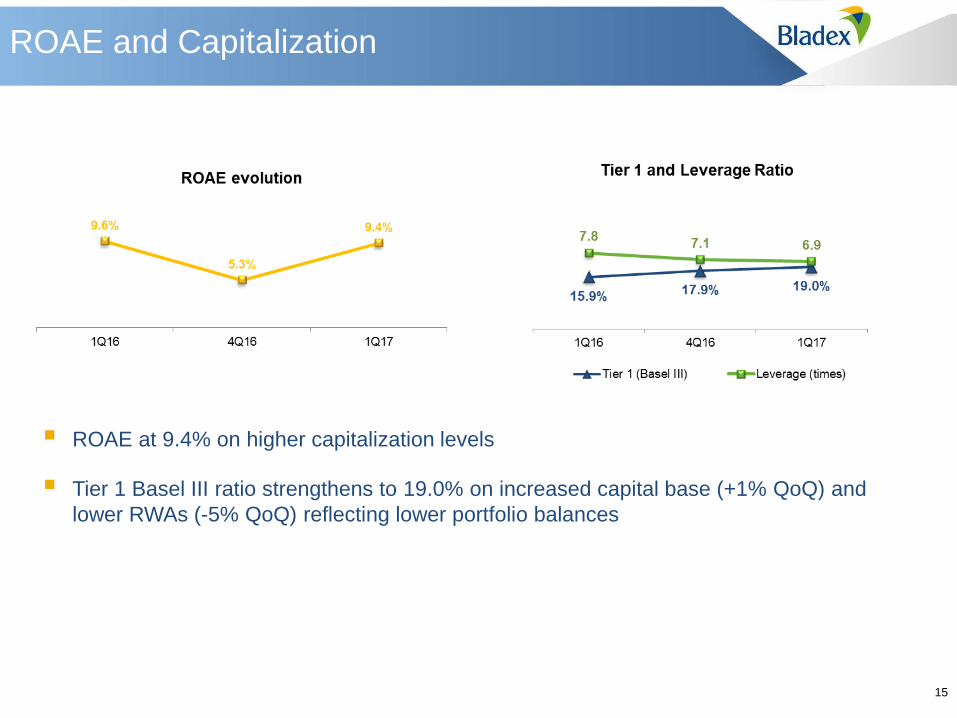

ROAE at 9.4% on higher capitalization levels

Tier 1 Basel III ratio strengthens to 19.0% on increased capital base (+1% QoQ) and

lower RWAs (-5% QoQ) reflecting lower portfolio balances

15

ROAE and Capitalization

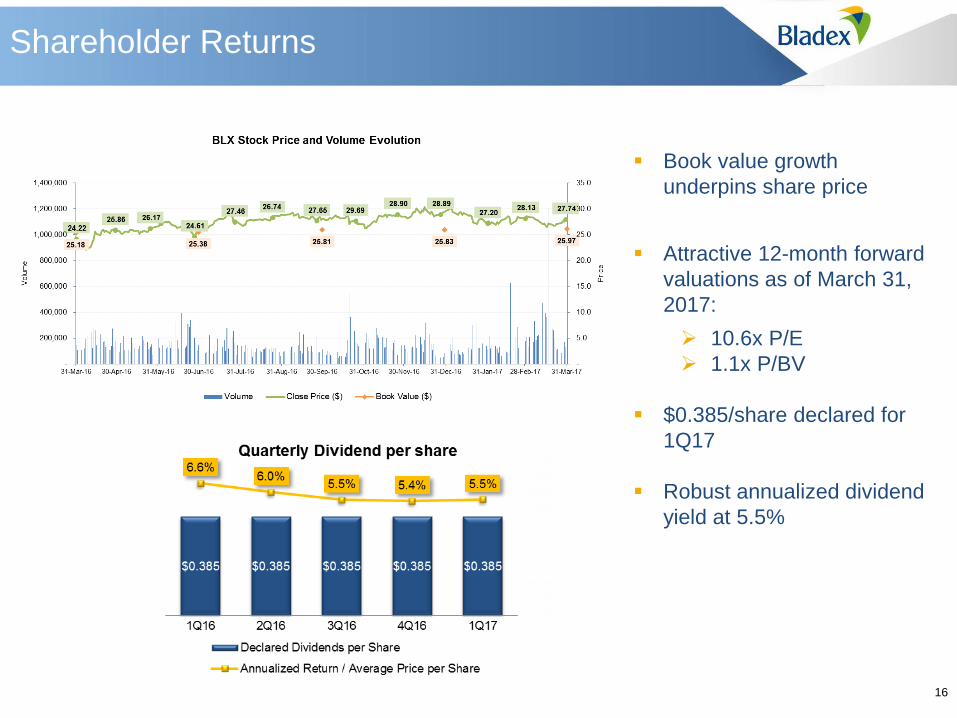

Book value growth

underpins share price

Attractive 12-month forward

valuations as of March 31,

2017:

10.6x P/E

1.1x P/BV

$0.385/share declared for

1Q17

Robust annualized dividend

yield at 5.5%

16

Shareholder Returns

Thank You

17

Appendix

18

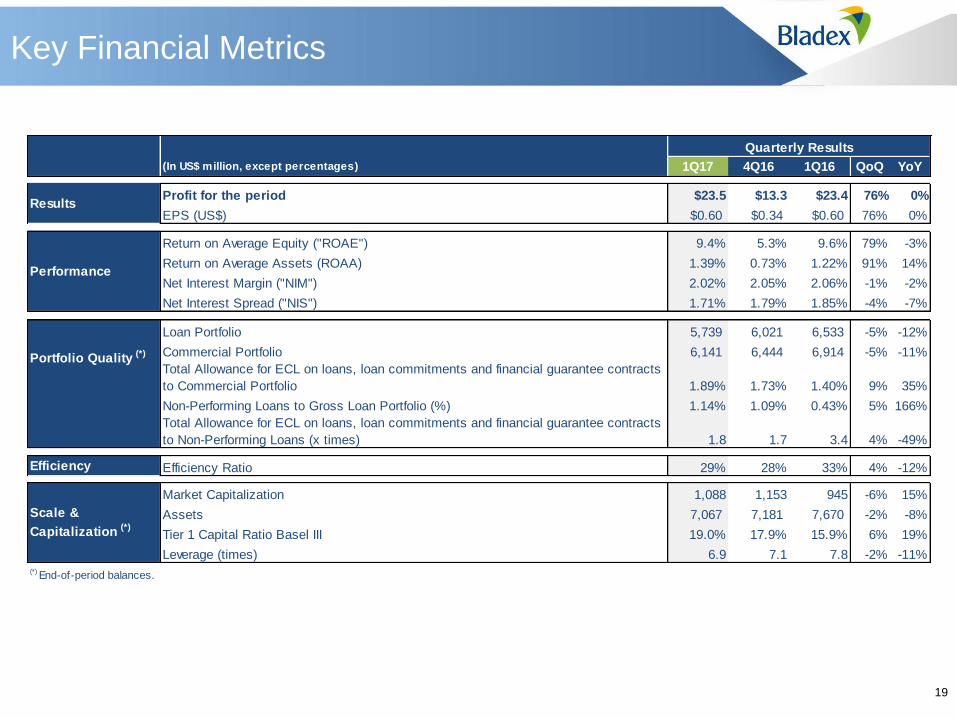

Key Financial Metrics

19

Quarterly Results Year to Date Results

(In US$ million, except percentages) 1Q17 4Q16 1Q16 QoQ YoY

Profit for the period $23.5 $13.3 $23.4 76% 0%

EPS (US$) $0.60 $0.34 $0.60 76% 0%

Return on Average Equity ("ROAE") 9.4% 5.3% 9.6% 79% -3%

Return on Average Assets (ROAA) 1.39% 0.73% 1.22% 91% 14%

Net Interest Margin ("NIM") 2.02% 2.05% 2.06% -1% -2%

Net Interest Spread ("NIS") 1.71% 1.79% 1.85% -4% -7%

Loan Portfolio 5,739 6,021 6,533 -5% -12%

Commercial Portfolio 6,141 6,444 6,914 -5% -11%

Total Allowance for ECL on loans, loan commitments and financial guarantee contracts

to Commercial Portfolio 1.89% 1.73% 1.40% 9% 35%

Non-Performing Loans to Gross Loan Portfolio (%) 1.14% 1.09% 0.43% 5% 166%

Total Allowance for ECL on loans, loan commitments and financial guarantee contracts

to Non-Performing Loans (x times) 1.8 1.7 3.4 4% -49%

Efficiency Ratio 29% 28% 33% 4% -12%

Market Capitalization 1,088 1,153 945 -6% 15%

Assets 7,067 7,181 7,670 -2% -8%

Tier 1 Capital Ratio Basel III 19.0% 17.9% 15.9% 6% 19%

Leverage (times) 6.9 7.1 7.8 -2% -11%(*) End-of-period balances.

Results

Performance

Portfolio Quality (*)

Efficiency

Scale &

Capitalization (*)