15th grace emea fcc technology conference...15th grace emea fcc technology conference european...

TRANSCRIPT

15th Grace EMEA FCC Technology Conference

© Refino España April 2015

Repsol Overview

Spanish Refining System

Summary

15th Grace EMEA FCC Technology Conference

2

1

© 2

Spanish Refining System

European Refining Business

2

3

Repsol Overview

Spanish Refining System

Summary

15th Grace EMEA FCC Technology Conference

2

1

© 3

Spanish Refining System

European Refining Business

2

3

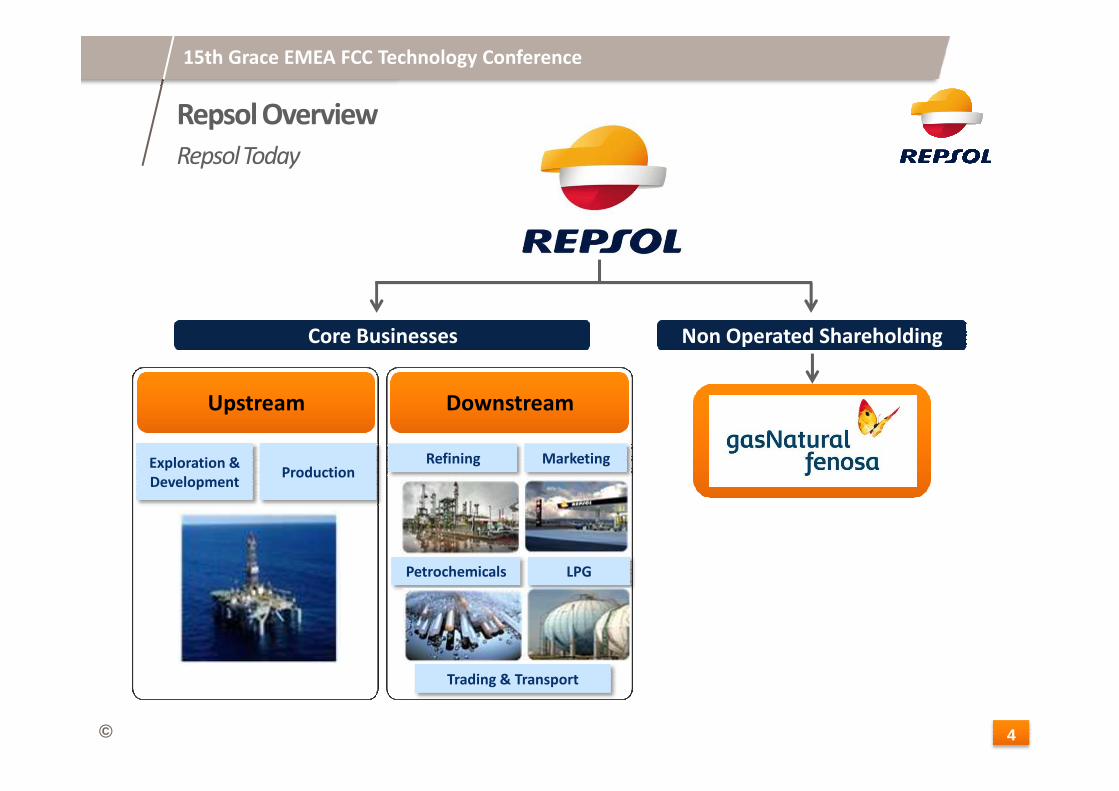

Repsol Overview

Repsol Today

15th Grace EMEA FCC Technology Conference

Upstream Downstream

Core Businesses Non Operated Shareholding

© 4

Upstream Downstream

Exploration & Development

ProductionRefining Marketing

Petrochemicals LPG

Trading & Transport

Repsol Overview

Shareholders Structure

15th Grace EMEA FCC Technology Conference

© 5

Number of Shares: 1.374 billions (march 2015)

Repsol Overview

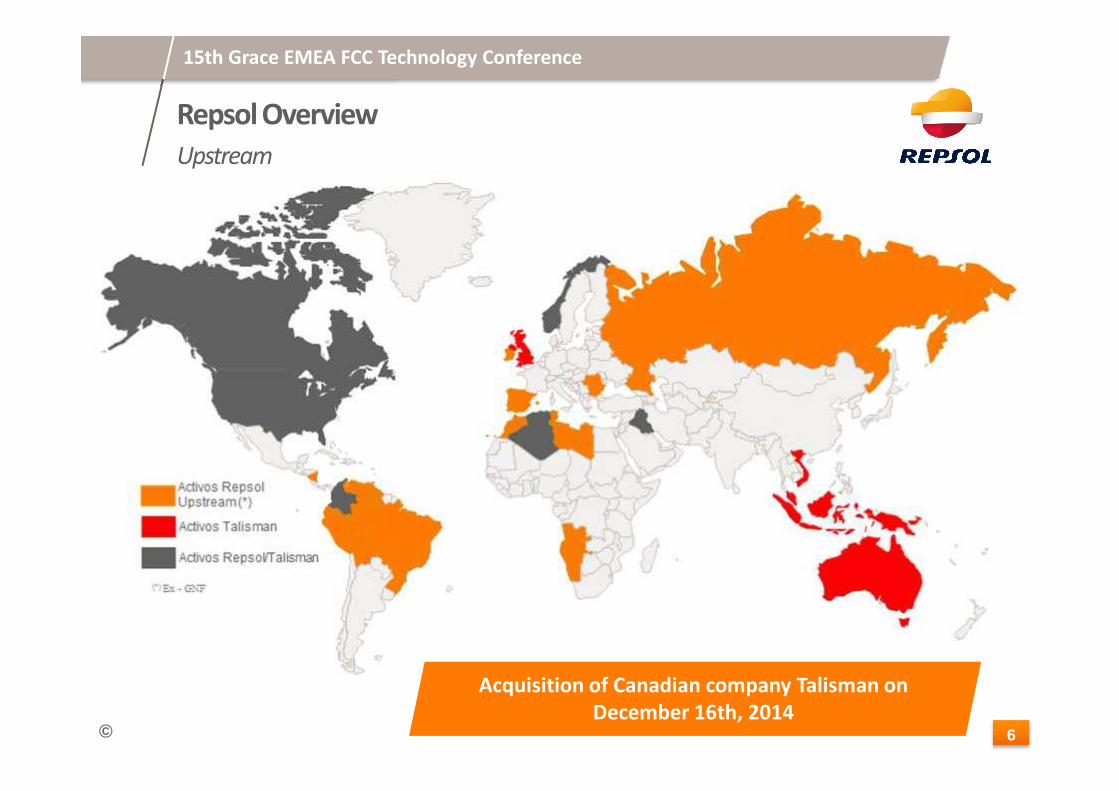

Upstream

15th Grace EMEA FCC Technology Conference

© 6

Acquisition of Canadian company Talisman on December 16th, 2014

CORUÑA BILBAO

TARRAGONA

Refineries Repsol

Other refineries

Oil pipelines CLH

Oil pipeline Repsol

Refining – Leadership positionPetrochemicals – Regional focus and

integration

Repsol Overview

Downstream

15th Grace EMEA FCC Technology Conference

© 7

E&P Activity in 31 countries (operator in 23)

� #1 Refiner in Spain

� Integrated refining system with high conversion level in Spain

� Leading Refiner in Peru

- Integrated with marketing

� First producer in Iberian peninsula

� Leading market shares in Iberia High integration with refining

� All sites co-located with refineries to maximize value of streams

CARTAGENA

ALGECIRASHUELVA

TARRAGONA

CASTELLONPUERTOLLANO

Repsol Overview

Downstream

15th Grace EMEA FCC Technology Conference

Marketing and Trading – Highly efficient and integrated

LPG – World leader focus in core markets

© 8

� Efficient network of 4.649 service stations all over the world.

� Repsol has 3.585 service stations in Spain, 440 in Portugal, 374 in Perú and 250 in Italy

� Leadership position in Peru

� Market position in key markets where we operate

� A leader LPG operational productivity

Repsol Overview

Strategic Objectives

15th Grace EMEA FCC Technology Conference

� UPSTREAM GROWTH

� MAXIMIZE DOWNSTREAM RETURN ON CAPITAL

� FINANCIAL STRENGTH

Growth engine

Operational excellence and margin optimization

© 9

� FINANCIAL STRENGTH

� ATRACTIVE REMUNERATION TO OUR SHAREHOLDERS

Credit rating and international investitors confidence

Value creation

Sale of non-strategic actives

Monetization of YPF’s compensation

Upstream company acquisition: Talisman

Repsol Overview

Spanish Refining System

Summary

15th Grace EMEA FCC Technology Conference

2

1

© 10

Spanish Refining System

European Refining Business

2

3

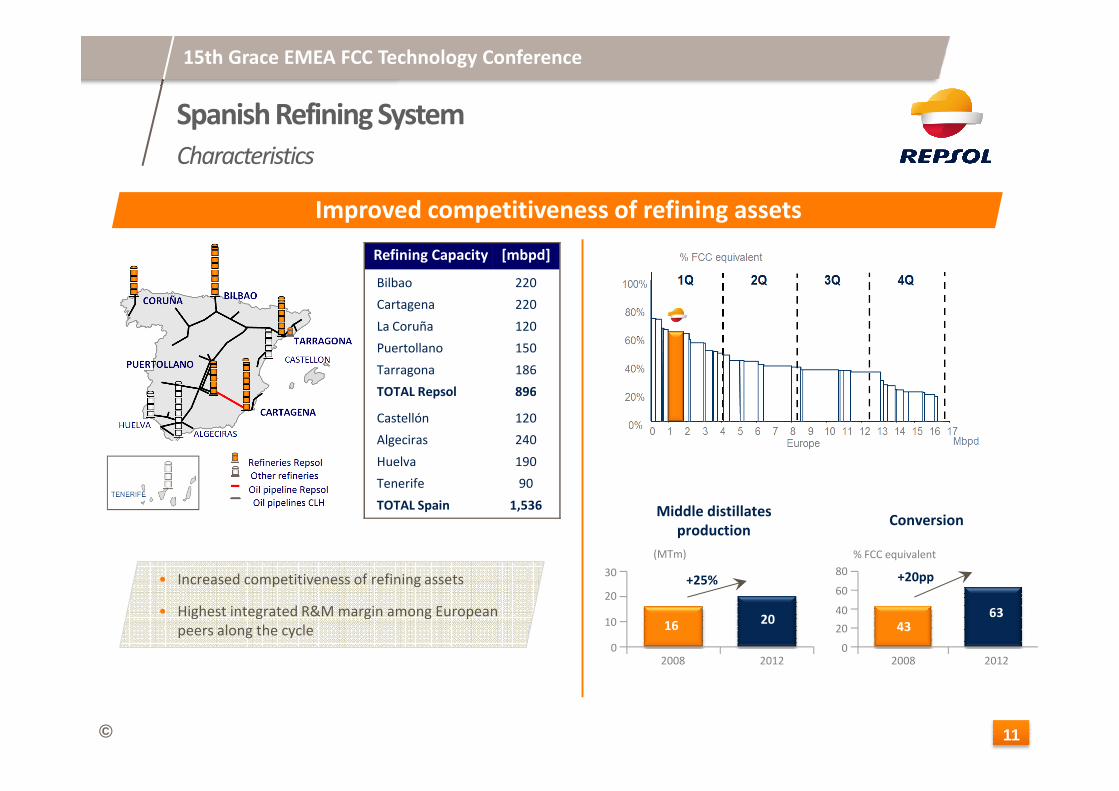

Improved competitiveness of refining assets

Spanish Refining System

Characteristics

15th Grace EMEA FCC Technology Conference

Refining Capacity [mbpd]

Bilbao

Cartagena

La Coruña

Puertollano

Tarragona

TOTAL Repsol

220

220

120

150

186

896

© 11

(MTm)

30

20

10

02012

20

2008

16

% FCC equivalent

80

60

40

20

02012

63

2008

43

ConversionMiddle distillates

production

+25% +20pp• Increased competitiveness of refining assets

• Highest integrated R&M margin among European

peers along the cycle

TOTAL Repsol 896

Castellón

Algeciras

Huelva

Tenerife

TOTAL Spain

120

240

190

90

1,536

Marketing Chemicals Lubricants Asphalts

• • •

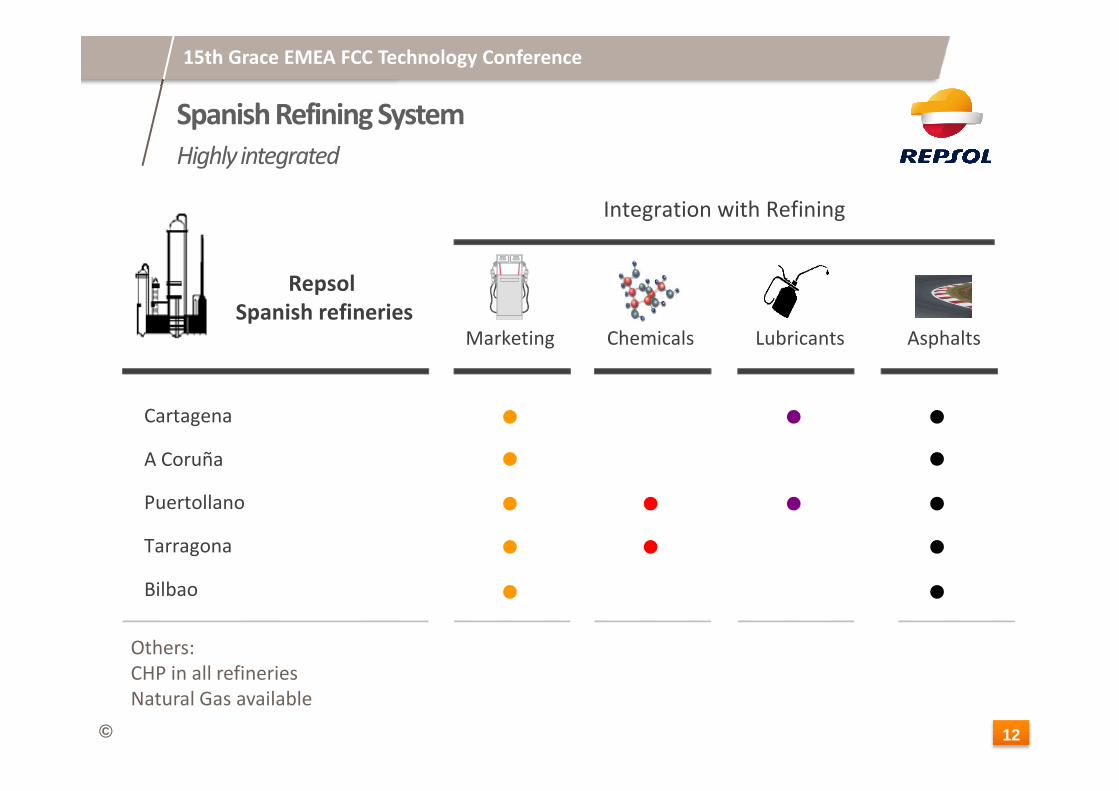

Repsol Spanish refineries

Integration with Refining

Spanish Refining System

Highly integrated

15th Grace EMEA FCC Technology Conference

© 12

Cartagena • • •A Coruña • •Puertollano • • • •Tarragona • • •Bilbao • •

Others:

CHP in all refineries

Natural Gas available

Spanish Refining System

CLH Logistics

15th Grace EMEA FCC Technology Conference

© 13

Repsol Overview

Spanish Refining System2

1

Summary

15th Grace EMEA FCC Technology Conference

© 14

Spanish Refining System

European Refining Business

2

3

European Refining Business

Demand forecasts

15th Grace EMEA FCC Technology Conference

Global Oil demand

© 15

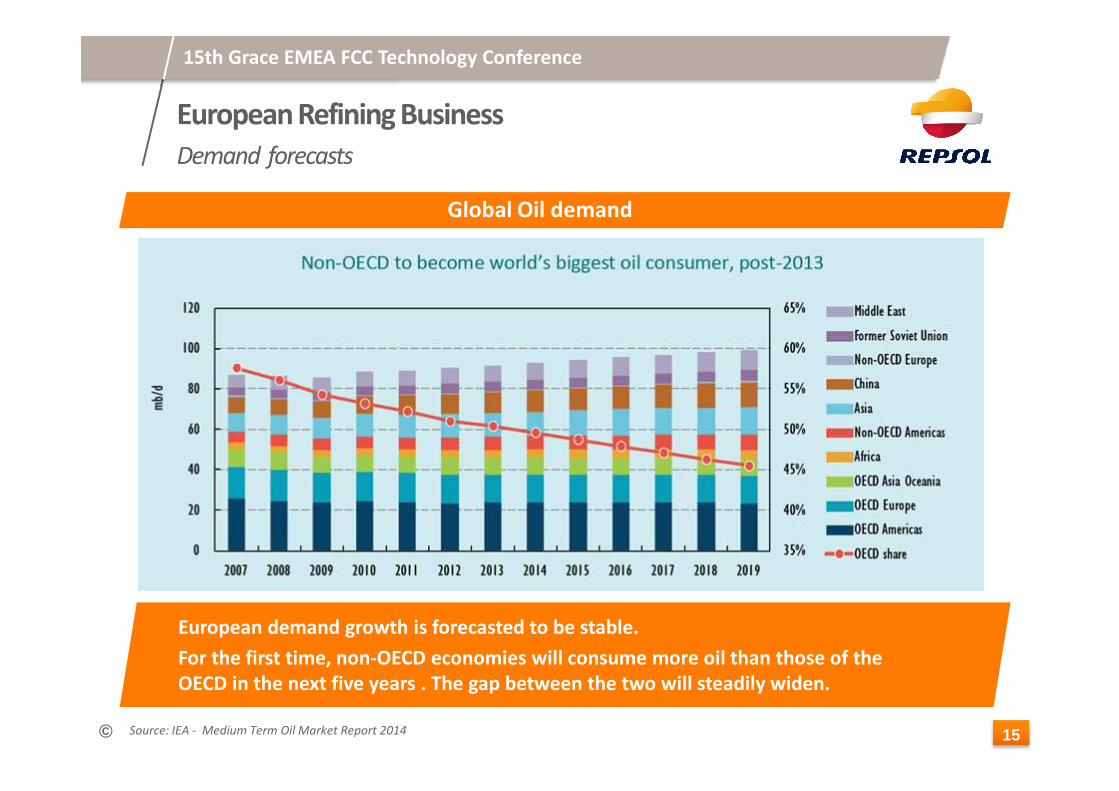

European demand growth is forecasted to be stable.

For the first time, non-OECD economies will consume more oil than those of the OECD in the next five years . The gap between the two will steadily widen.

Source: IEA - Medium Term Oil Market Report 2014

European Refining Business

Distillation Capacity

15th Grace EMEA FCC Technology Conference

© 16

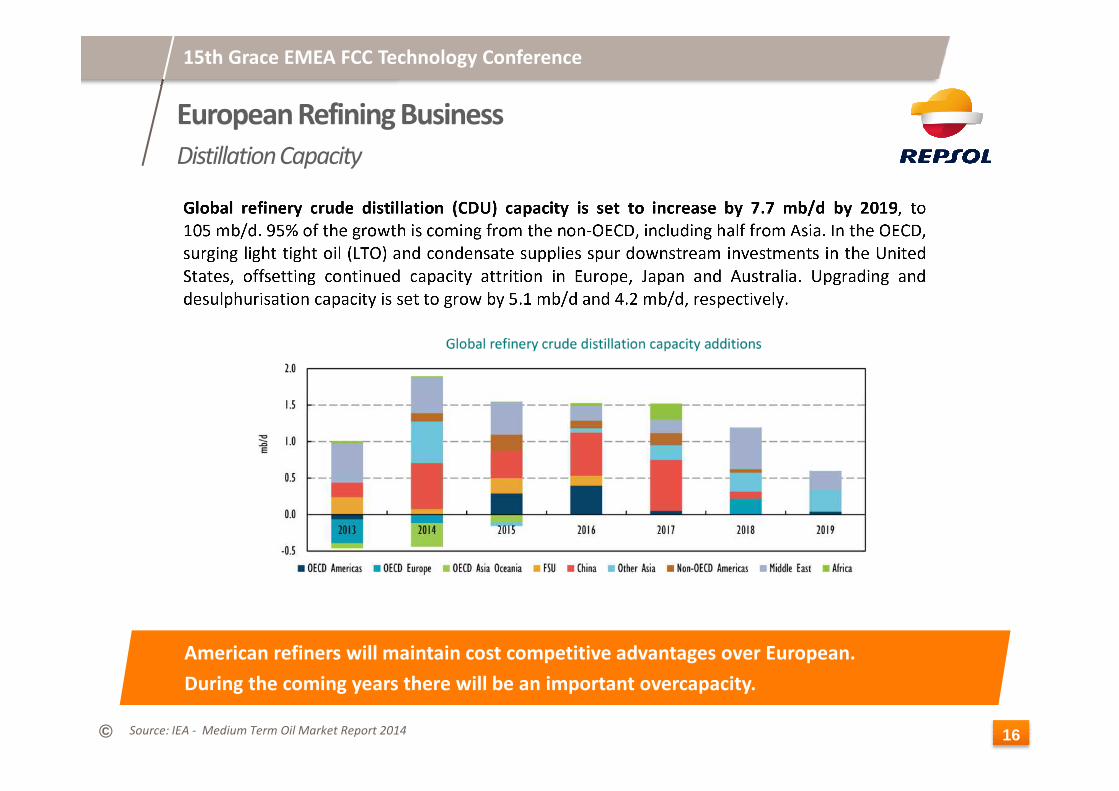

American refiners will maintain cost competitive advantages over European.

During the coming years there will be an important overcapacity.

Source: IEA - Medium Term Oil Market Report 2014

European Refining Business

Refinery closures in Europe

15th Grace EMEA FCC Technology Conference

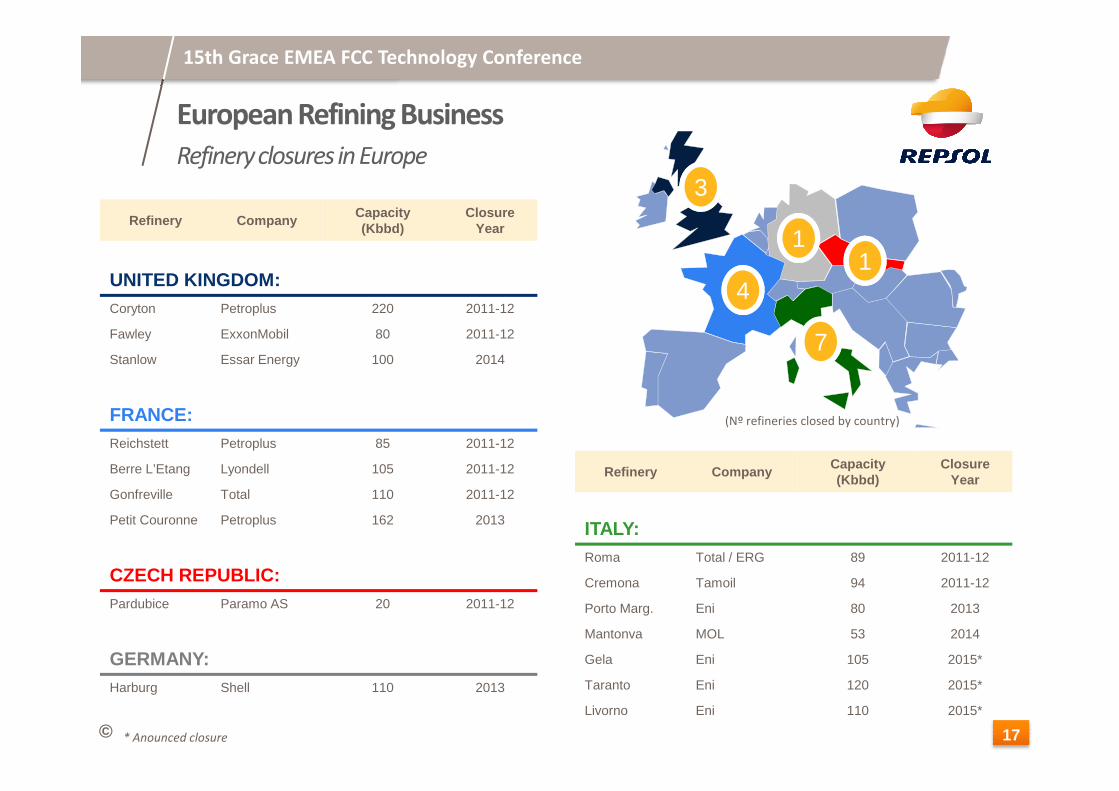

Refinery CompanyCapacity(Kbbd)

ClosureYear

UNITED KINGDOM:Coryton Petroplus 220 2011-12

Fawley ExxonMobil 80 2011-12

Stanlow Essar Energy 100 2014

3

4

11

7

© 17

FRANCE:Reichstett Petroplus 85 2011-12

Berre L’Etang Lyondell 105 2011-12

Gonfreville Total 110 2011-12

Petit Couronne Petroplus 162 2013

CZECH REPUBLIC:Pardubice Paramo AS 20 2011-12

GERMANY:Harburg Shell 110 2013

Refinery CompanyCapacity(Kbbd)

ClosureYear

ITALY:Roma Total / ERG 89 2011-12

Cremona Tamoil 94 2011-12

Porto Marg. Eni 80 2013

Mantonva MOL 53 2014

Gela Eni 105 2015*

Taranto Eni 120 2015*

Livorno Eni 110 2015*

(Nº refineries closed by country)

* Anounced closure

European Refining Business

Global forecast

15th Grace EMEA FCC Technology Conference

© 18

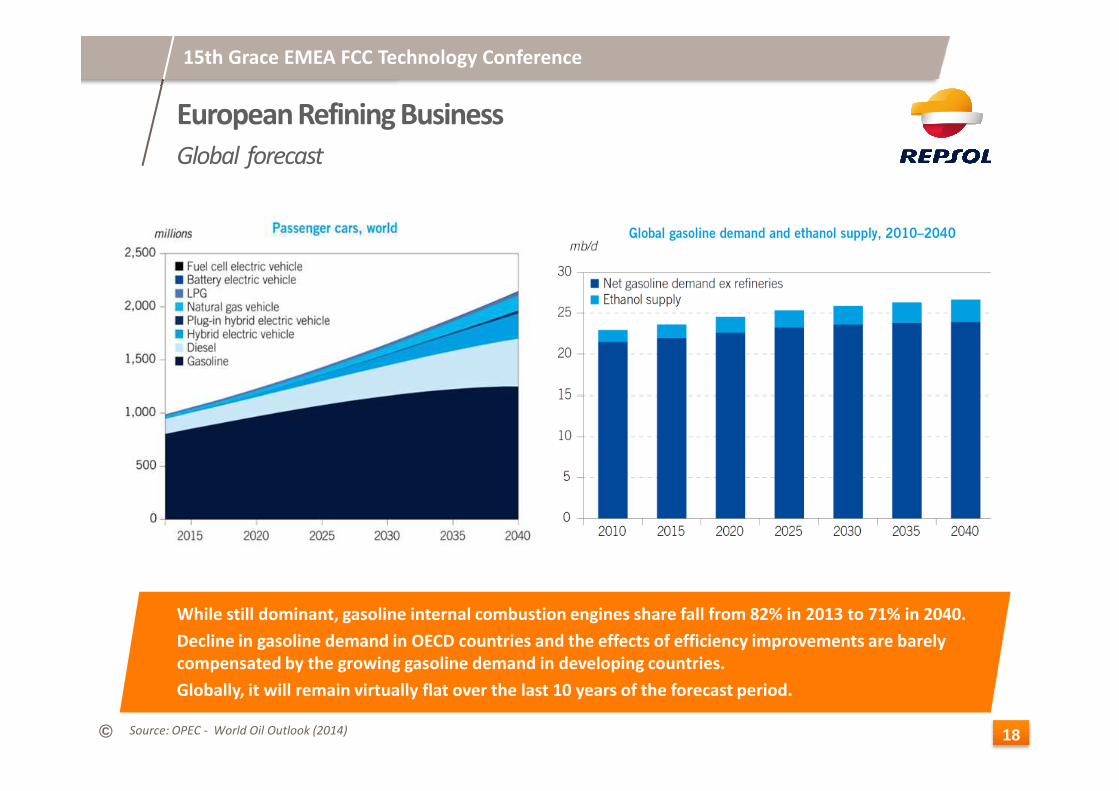

While still dominant, gasoline internal combustion engines share fall from 82% in 2013 to 71% in 2040.

Decline in gasoline demand in OECD countries and the effects of efficiency improvements are barely compensated by the growing gasoline demand in developing countries.

Globally, it will remain virtually flat over the last 10 years of the forecast period.

Source: OPEC - World Oil Outlook (2014)

European Refining Business

World gasoline trade forecast

15th Grace EMEA FCC Technology Conference

© 19

Europe will decrease its excess of gasoline and reduce its exports to North America by 2020.

Source: Wood Mackenzie - Short Term Oils Market Seminar 2014

European Refining Business

World naphta trade forecast

15th Grace EMEA FCC Technology Conference

© 20

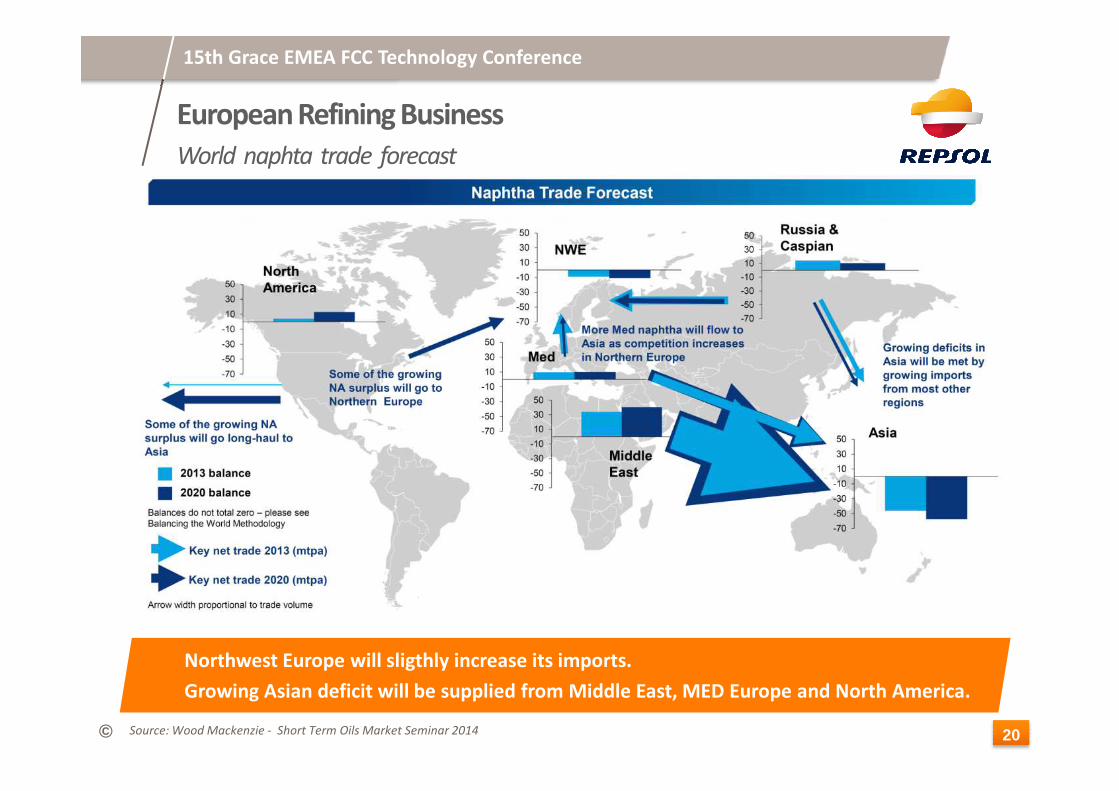

Northwest Europe will sligthly increase its imports.

Growing Asian deficit will be supplied from Middle East, MED Europe and North America.

Source: Wood Mackenzie - Short Term Oils Market Seminar 2014

European Refining Business

World diesel/gasoil trade forecast

15th Grace EMEA FCC Technology Conference

© 21

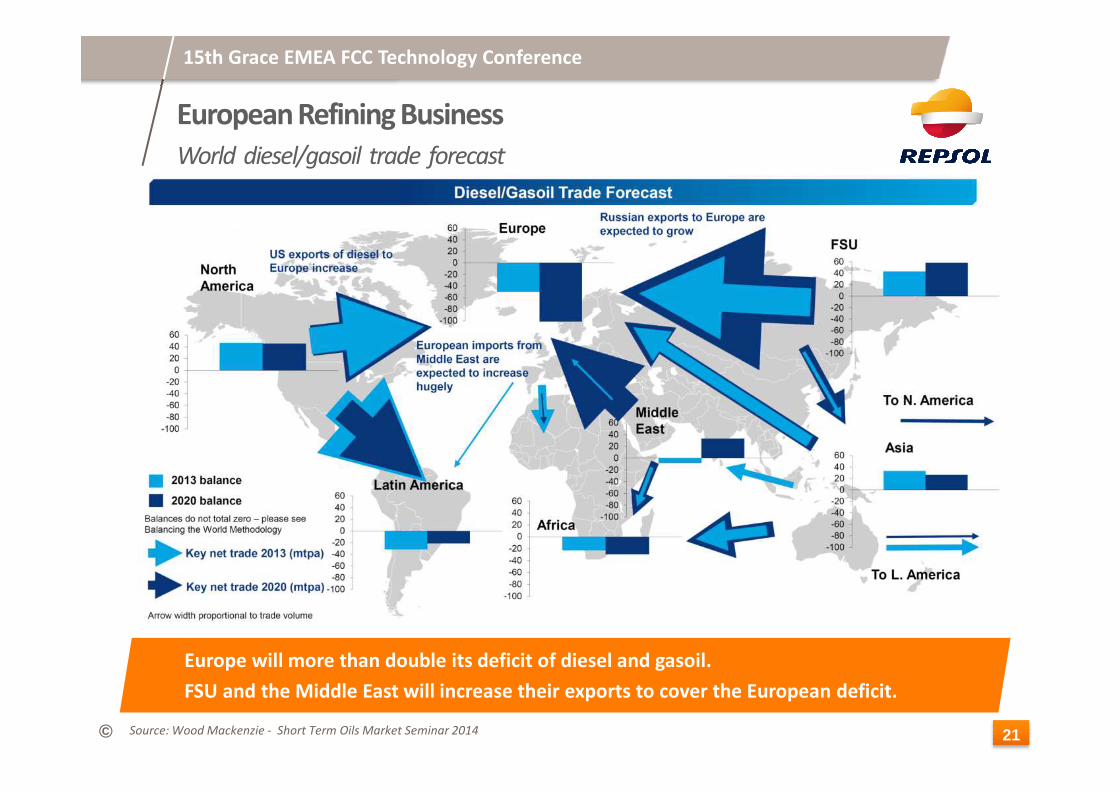

Europe will more than double its deficit of diesel and gasoil.

FSU and the Middle East will increase their exports to cover the European deficit.

Source: Wood Mackenzie - Short Term Oils Market Seminar 2014

European Refining Business

Evolution of European specifications

15th Grace EMEA FCC Technology Conference

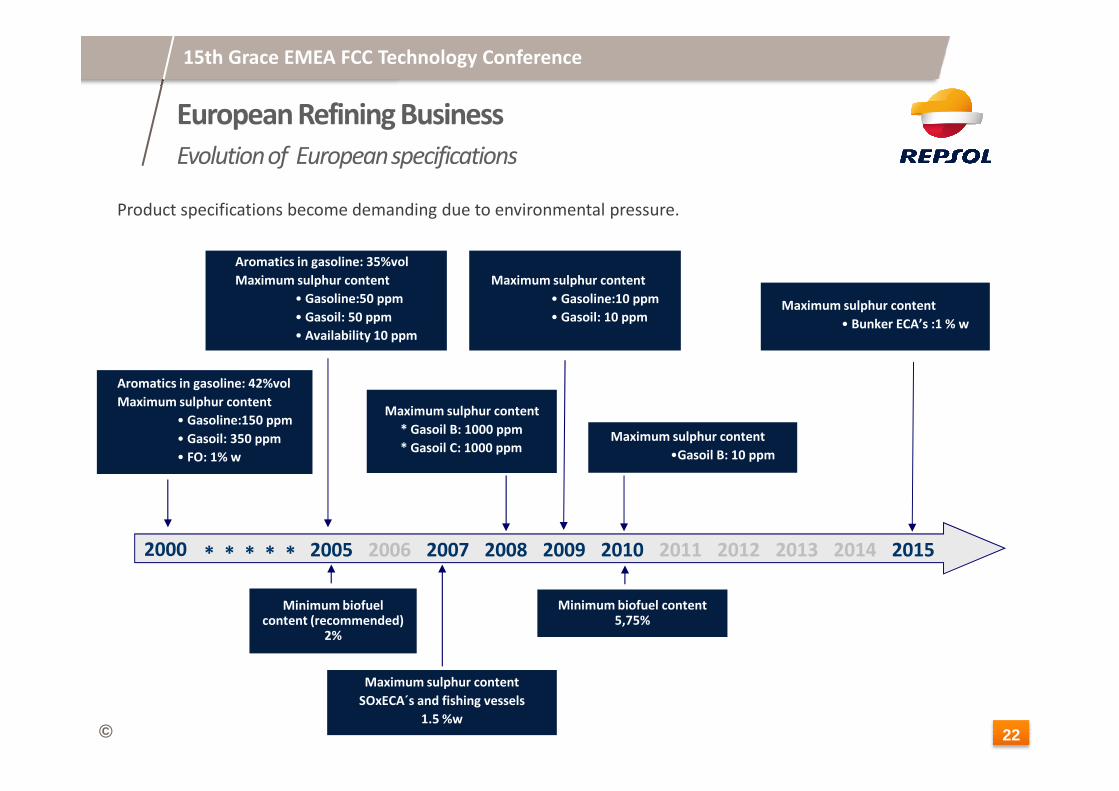

Product specifications become demanding due to environmental pressure.

Aromatics in gasoline: 42%vol

Maximum sulphur content

Aromatics in gasoline: 35%vol

Maximum sulphur content

• Gasoline:50 ppm

• Gasoil: 50 ppm

• Availability 10 ppm

Maximum sulphur content

• Gasoline:10 ppm

• Gasoil: 10 ppmMaximum sulphur content

• Bunker ECA’s :1 % w

© 22

Europe will more than double its deficit of diesel and gasoil.

FSU and the Middle East will increase their exports to cover the European deficit.

20092005

Minimum biofuel content (recommended)

2%

Maximum sulphur content

• Gasoline:150 ppm

• Gasoil: 350 ppm

• FO: 1% w

2000 2006 2007 2008 2010 2011 2012

Maximum sulphur content

* Gasoil B: 1000 ppm

* Gasoil C: 1000 ppm

Maximum sulphur content

SOxECA´s and fishing vessels

1.5 %w

Minimum biofuel content 5,75%

* * * * * 2013 2014 2015

Maximum sulphur content

•Gasoil B: 10 ppm

European Refining Business

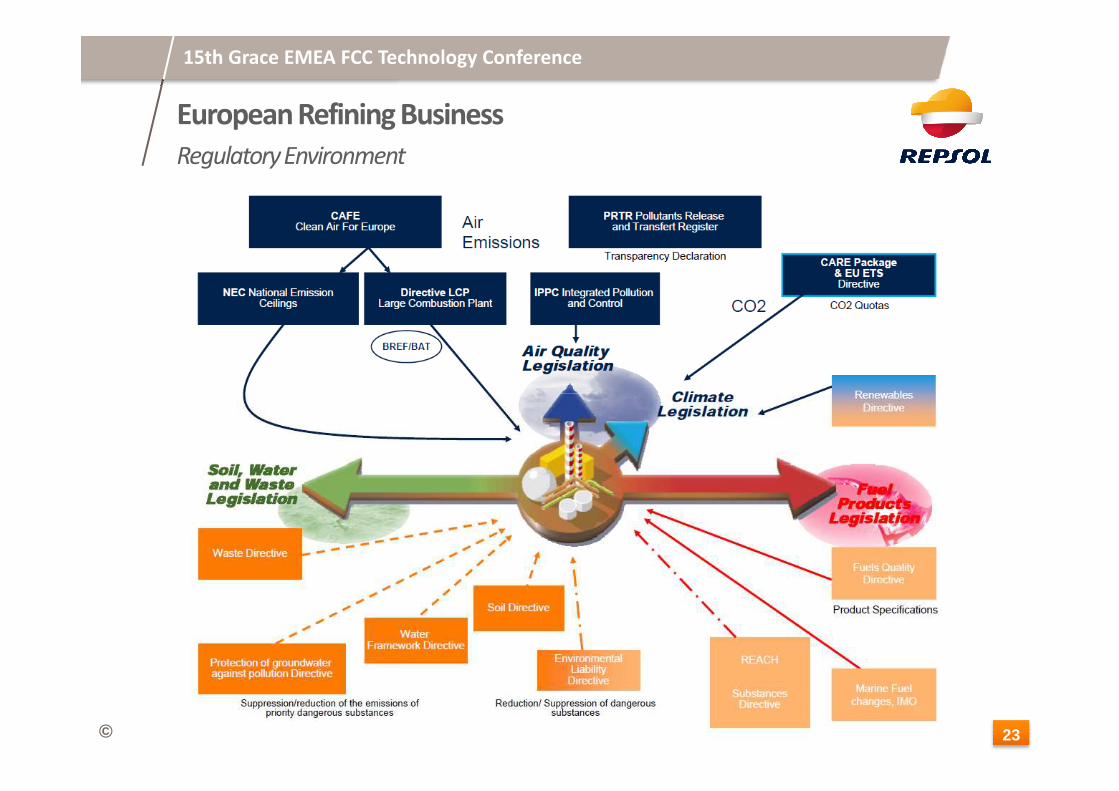

Regulatory Environment

15th Grace EMEA FCC Technology Conference

© 23

15th Grace EMEA FCC Technology Conference

European Refining Business

Highlights

o World oil demand continues to grow, while European demand is nearly stagnant.

o Refining system racionalisation: 16 closures in Europe until now.

o Gasoline exports:

• Europe closures reduce gasoline surplus

• Increase in North American competitiveness lower gasoline imports

© 24

Northwest Europe will sligthly increase its imports.

Growing Asian deficit will be supplied from Middle East, MED Europe and North America.

• Increase in North American competitiveness lower gasoline imports

o Regulatory environment: Renewable policies, IPPC, BREF, ETS Directive…

� Safety and Availability

� CO₂ Reduction plan

� Markets & Logistics

� Competitiveness

� Innovation

� People