111125 mtg corporate presentation final

TRANSCRIPT

1

Modern Times Group MTG AB

“A Modern Media Group

for Modern Times”

November 2011

2

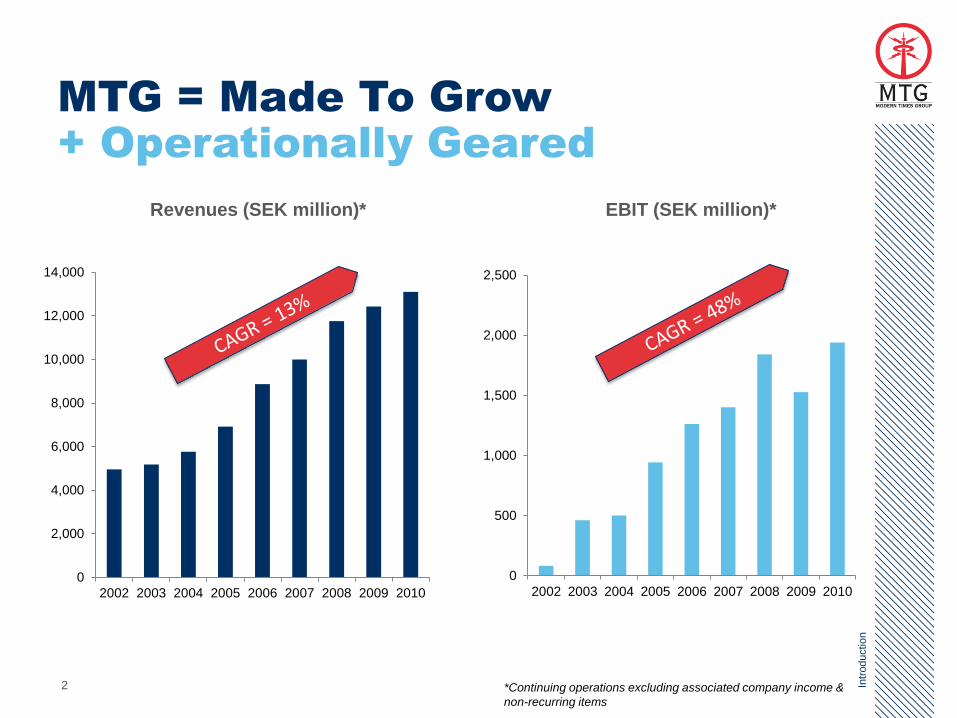

MTG = Made To Grow

+ Operationally Geared

Intr

oductio

n

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2002 2003 2004 2005 2006 2007 2008 2009 2010

0

500

1,000

1,500

2,000

2,500

2002 2003 2004 2005 2006 2007 2008 2009 2010

Revenues (SEK million)* EBIT (SEK million)*

*Continuing operations excluding associated company income &

non-recurring items

3

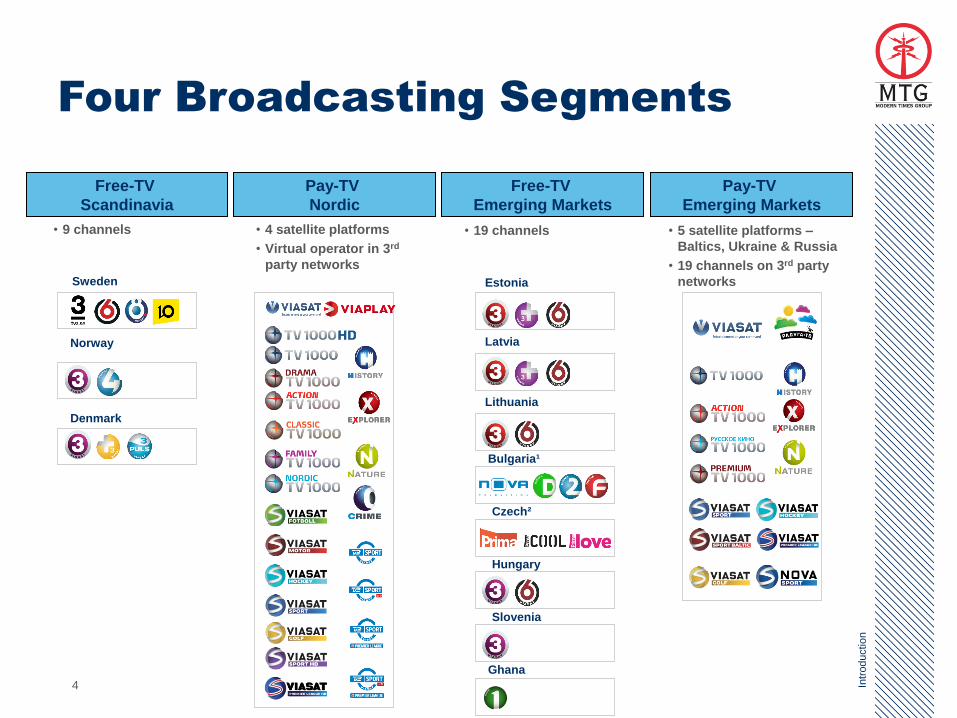

Operating 29 free-TV channels in 11 countries &

38 pay-TV channels in 34 countries

Unrivalled Broadcast Footprint

Spanning 4 continents

Intr

oductio

n

Four Broadcasting Segments

Sweden

Norway

Denmark

Estonia

Latvia

Lithuania

Bulgaria¹

Czech²

Hungary

Slovenia

Ghana

• 4 satellite platforms

• Virtual operator in 3rd

party networks

• 19 channels • 5 satellite platforms –

Baltics, Ukraine & Russia

• 19 channels on 3rd party

networks

• 9 channels

Free-TV

Scandinavia

Pay-TV

Nordic

Free-TV

Emerging Markets

Pay-TV

Emerging Markets

4 Intr

oductio

n

5

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2006 2007 2008 2009 2010

Free-TV Scandinavia Pay-TV Nordic Emerging Markets

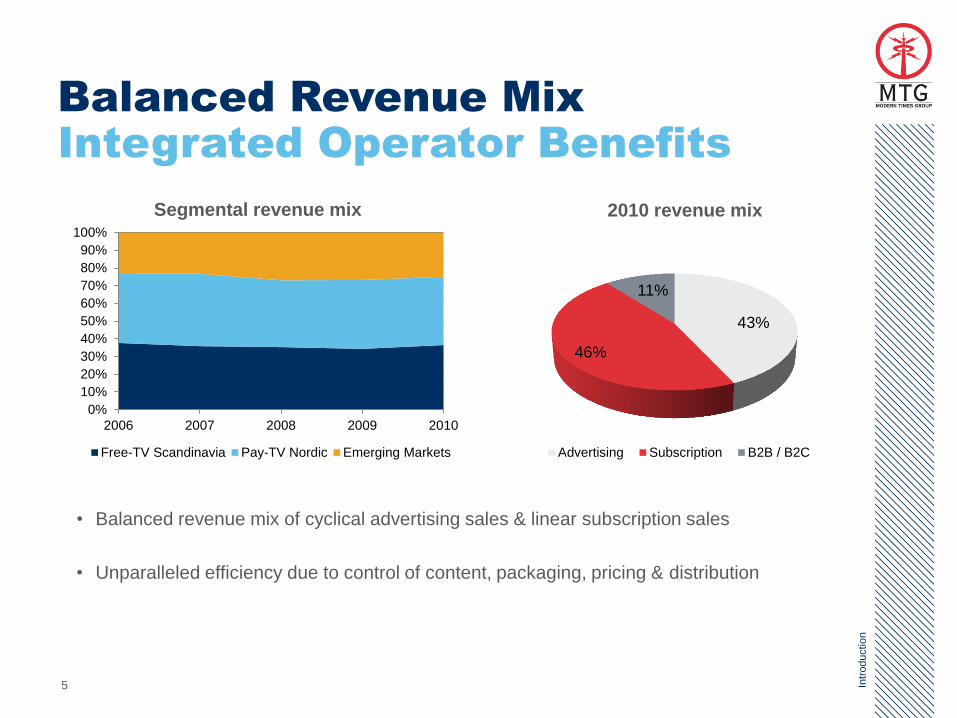

2010 revenue mix Segmental revenue mix

43%

46%

11%

Advertising Subscription B2B / B2C

• Balanced revenue mix of cyclical advertising sales & linear subscription sales

• Unparalleled efficiency due to control of content, packaging, pricing & distribution

Balanced Revenue Mix

Integrated Operator Benefits

Intr

oductio

n

6 Fre

e-T

V S

candin

avia

110

160

210

260

310

360

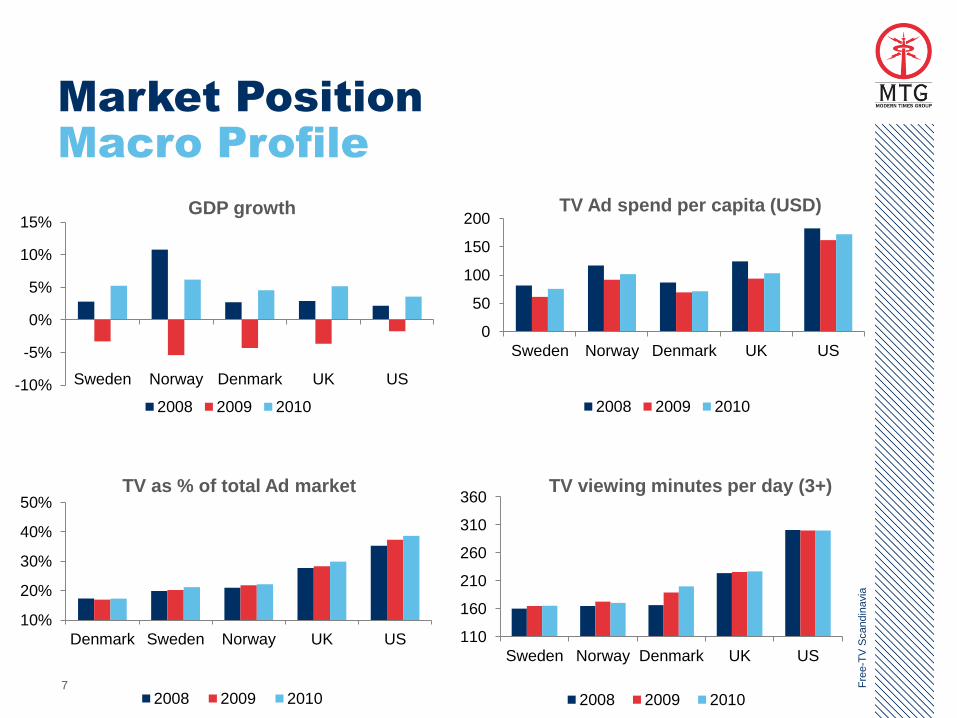

Sweden Norway Denmark UK US

2008 2009 2010

Market Position

Macro Profile

TV as % of total Ad market

10%

20%

30%

40%

50%

Denmark Sweden Norway UK US

2008 2009 2010

TV viewing minutes per day (3+)

0

50

100

150

200

Sweden Norway Denmark UK US

2008 2009 2010

TV Ad spend per capita (USD) GDP growth

-10%

-5%

0%

5%

10%

15%

Sweden Norway Denmark UK US

2008 2009 2010

7 Fre

e-T

V S

candin

avia

8

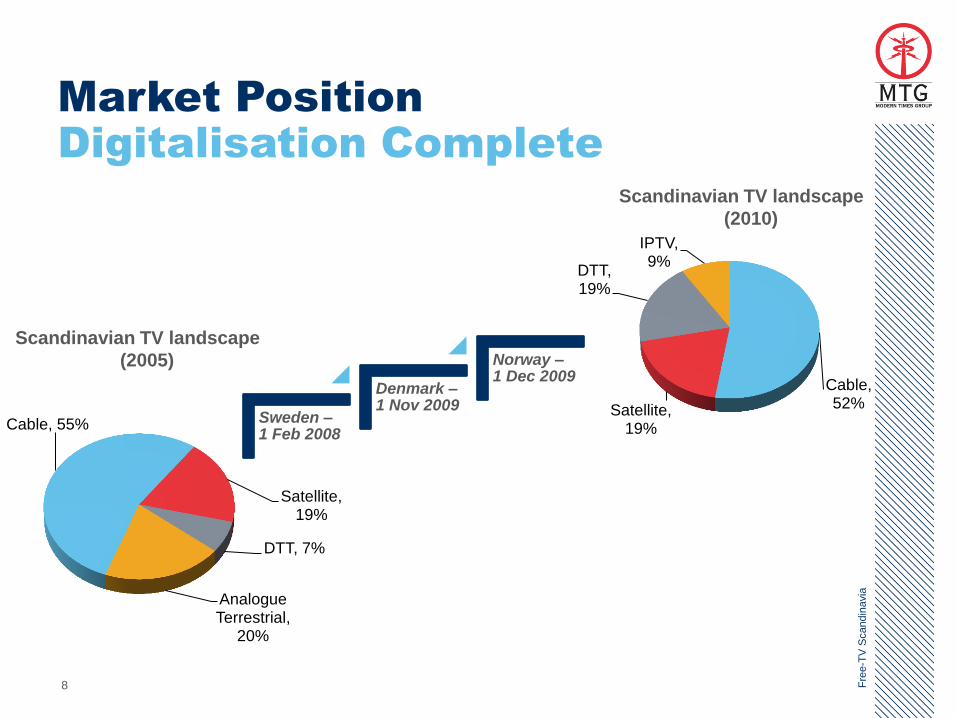

Market Position

Digitalisation Complete

Sweden – 1 Feb 2008

Denmark – 1 Nov 2009

Norway – 1 Dec 2009

Fre

e-T

V S

candin

avia

Scandinavian TV landscape

(2010)

Cable, 52% Satellite,

19%

DTT, 19%

IPTV, 9%

Cable, 55%

Satellite, 19%

DTT, 7%

Analogue Terrestrial,

20%

Scandinavian TV landscape

(2005)

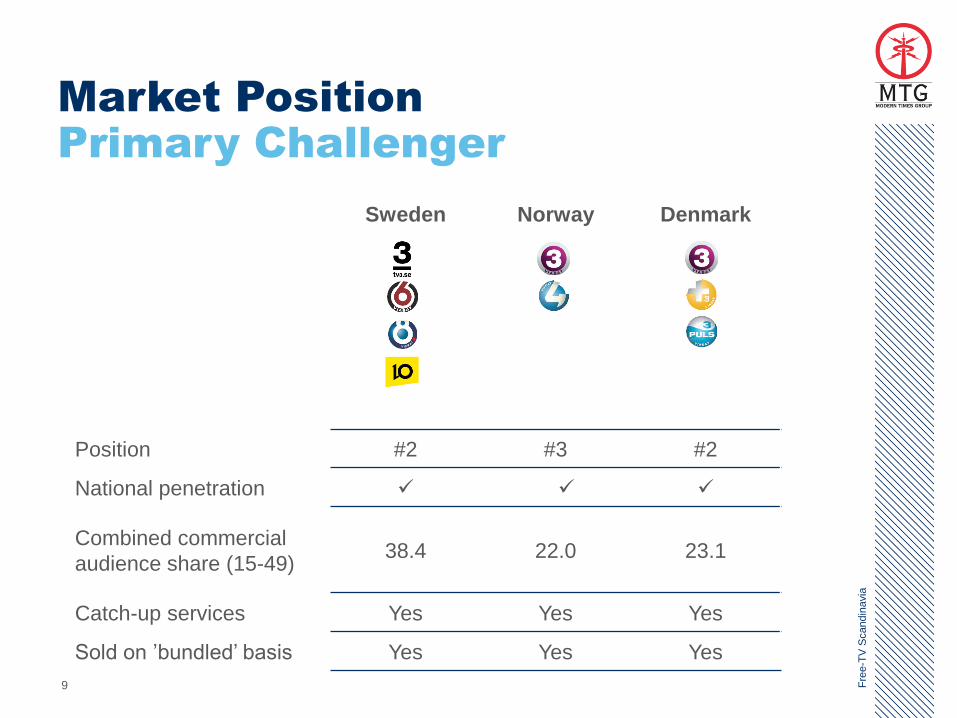

Sweden Norway Denmark

Position #2 #3 #2

National penetration

Combined commercial

audience share (15-49) 38.4 22.0 23.1

Catch-up services Yes Yes Yes

Sold on ’bundled’ basis Yes Yes Yes

9

Market Position

Primary Challenger

Fre

e-T

V S

candin

avia

The Opportunity

Breaking the Monopoly

10 Fre

e-T

V S

candin

avia

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Bonnier MTG ProSiebenSat.1

2003 2010

11

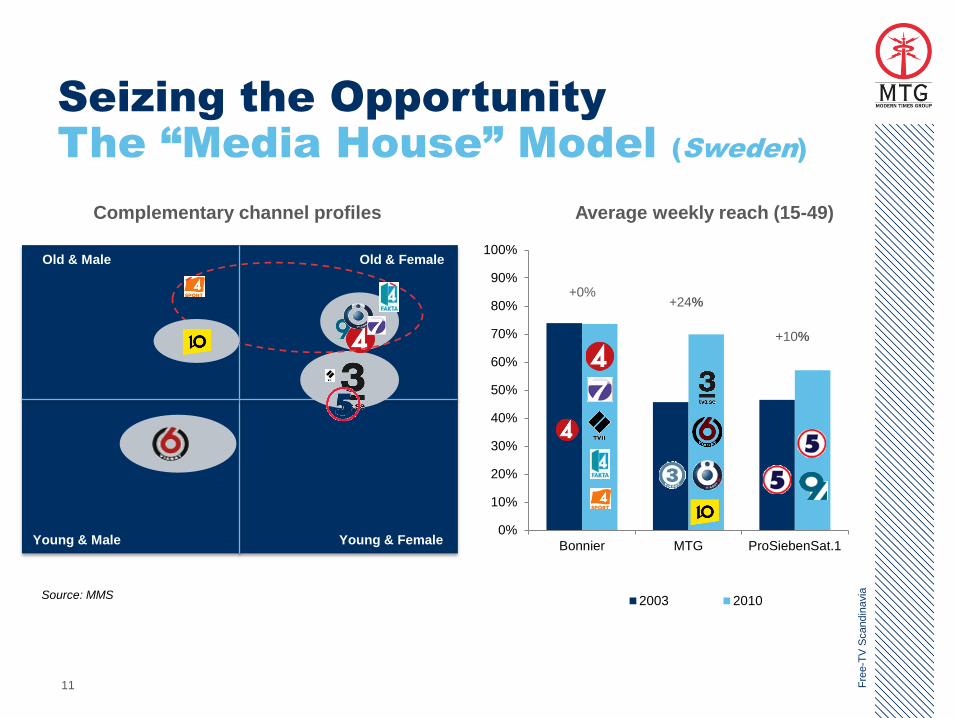

Seizing the Opportunity

The “Media House” Model (Sweden)

Fre

e-T

V S

candin

avia

Source: MMS

Complementary channel profiles Average weekly reach (15-49)

+0% +24%

+10%

Old & Male Old & Female

Young & Male Young & Female

TV4, 87% MTG, 7%

Other, 6%

Print, 63% Direct advertising,

14%

Internet, 14%

Radio, 4% TV, 5%

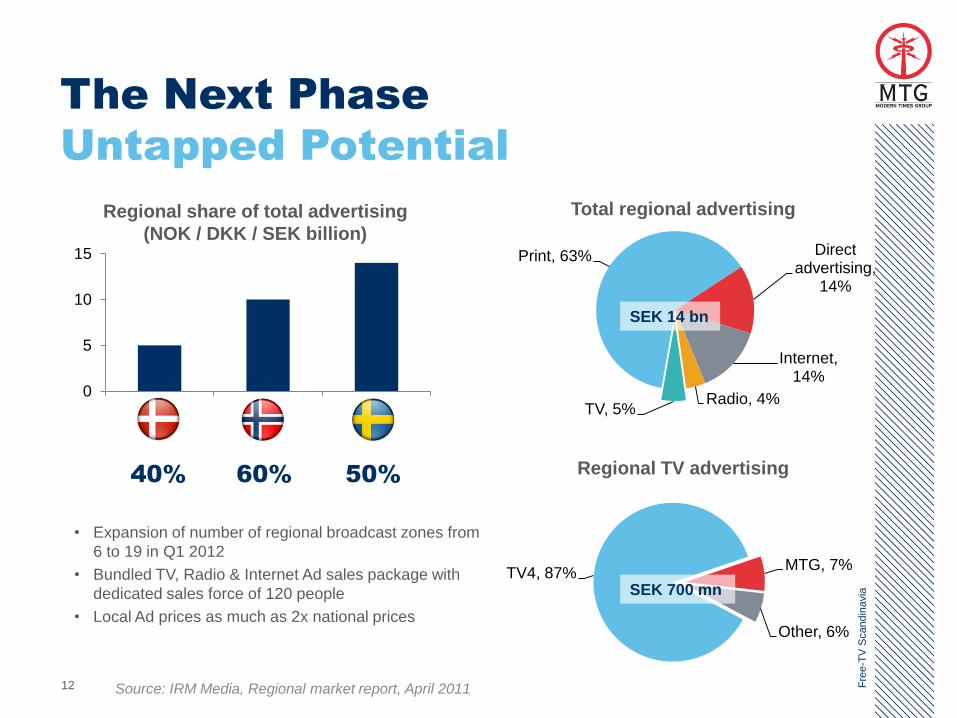

The Next Phase

Untapped Potential

Regional share of total advertising

(NOK / DKK / SEK billion)

50% 40% 60%

Source: IRM Media, Regional market report, April 2011

0

5

10

15

12 Fre

e-T

V S

candin

avia

Total regional advertising

Regional TV advertising

SEK 14 bn

SEK 700 mn

• Expansion of number of regional broadcast zones from

6 to 19 in Q1 2012

• Bundled TV, Radio & Internet Ad sales package with

dedicated sales force of 120 people

• Local Ad prices as much as 2x national prices

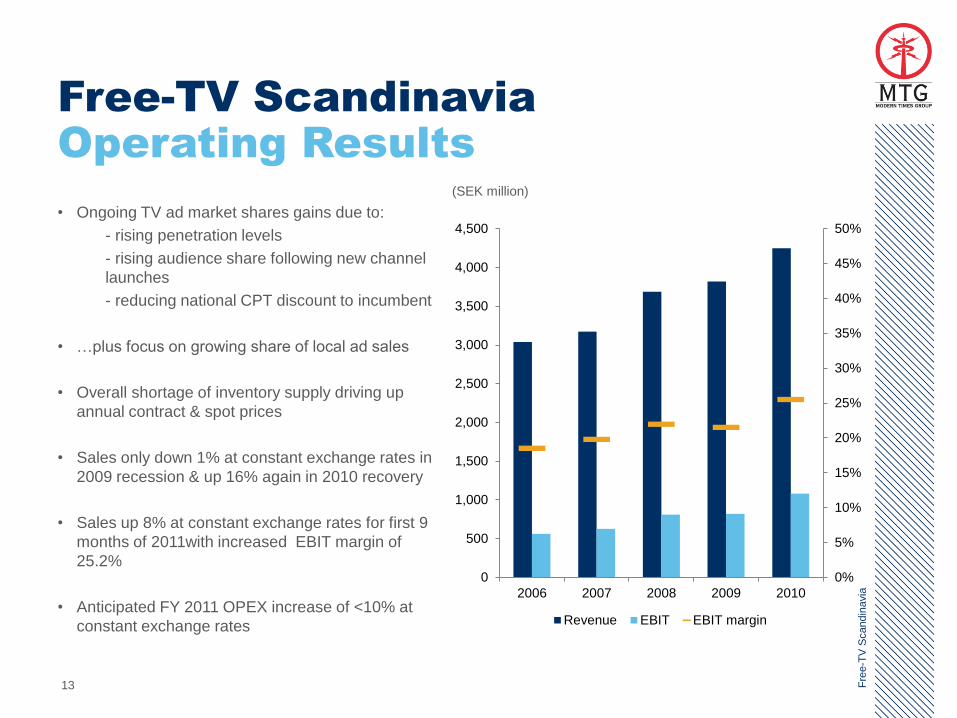

13

Free-TV Scandinavia

Operating Results

• Ongoing TV ad market shares gains due to:

- rising penetration levels

- rising audience share following new channel

launches

- reducing national CPT discount to incumbent

• …plus focus on growing share of local ad sales

• Overall shortage of inventory supply driving up

annual contract & spot prices

• Sales only down 1% at constant exchange rates in

2009 recession & up 16% again in 2010 recovery

• Sales up 8% at constant exchange rates for first 9

months of 2011with increased EBIT margin of

25.2%

• Anticipated FY 2011 OPEX increase of <10% at

constant exchange rates

Fre

e-T

V S

candin

avia

(SEK million)

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

2006 2007 2008 2009 2010

Revenue EBIT EBIT margin

14 Fre

e-T

V E

merg

ing M

ark

ets

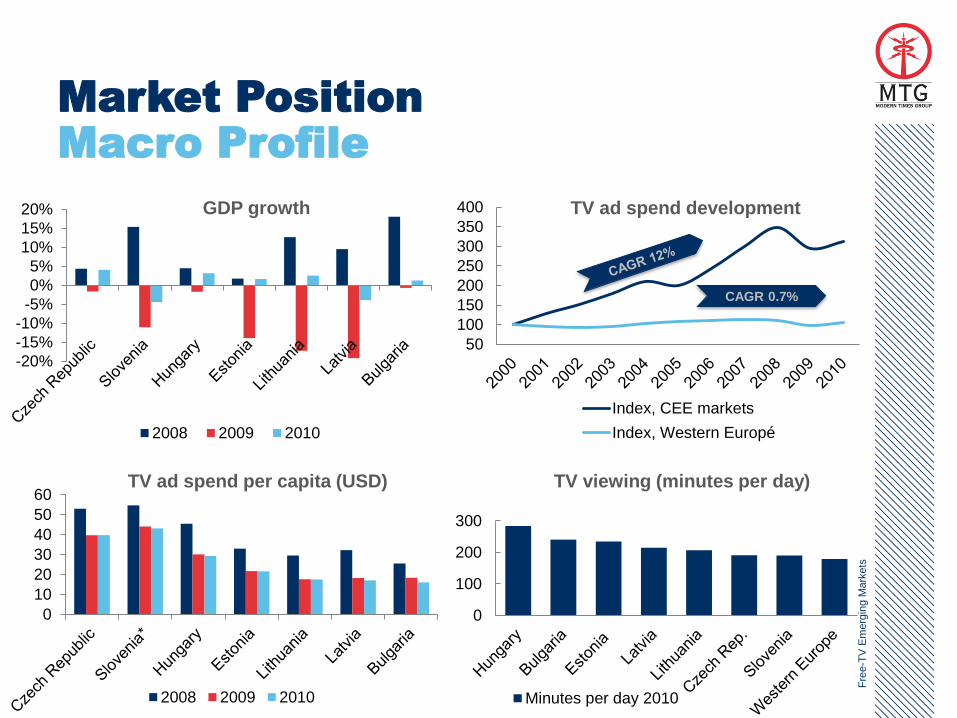

0

10

20

30

40

50

60

2008 2009 2010

0

100

200

300

Minutes per day 2010

Market Position

Macro Profile

TV viewing (minutes per day)

Fre

e-T

V E

merg

ing M

ark

ets

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

2008 2009 2010

GDP growth

TV ad spend per capita (USD)

50

100

150

200

250

300

350

400

Index, CEE markets

Index, Western Europé

TV ad spend development

CAGR 0.7%

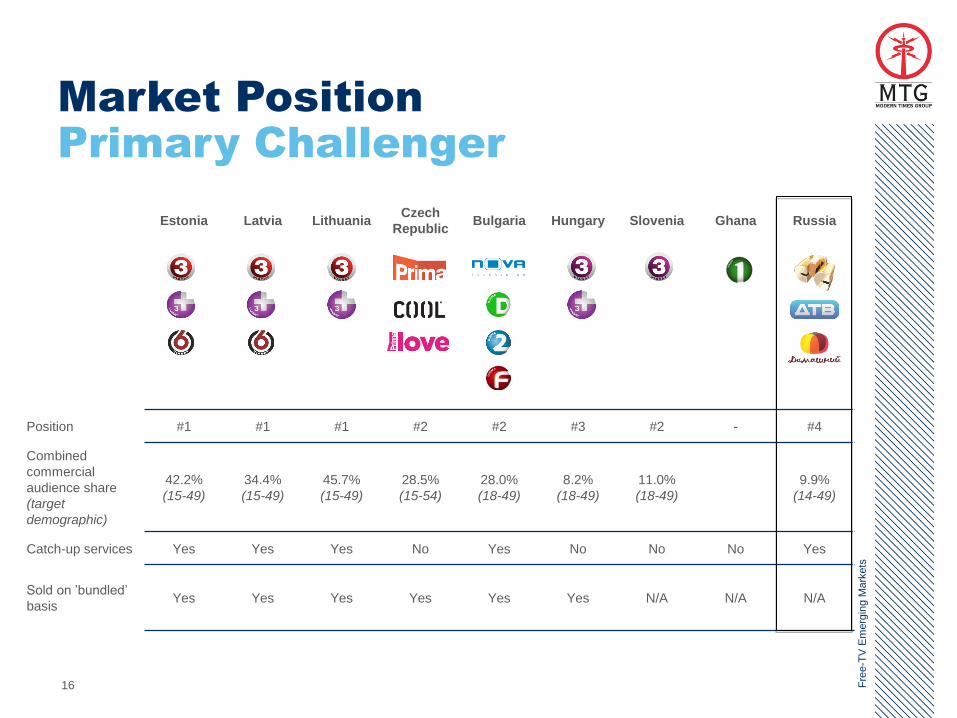

16

Market Position

Primary Challenger

Estonia Latvia Lithuania Czech

Republic Bulgaria Hungary Slovenia Ghana Russia

Position #1 #1 #1 #2 #2 #3 #2 - #4

Combined

commercial

audience share

(target

demographic)

42.2%

(15-49)

34.4%

(15-49)

45.7%

(15-49)

28.5%

(15-54)

28.0%

(18-49)

8.2%

(18-49)

11.0%

(18-49)

9.9%

(14-49)

Catch-up services Yes Yes Yes No Yes No No No Yes

Sold on ’bundled’

basis Yes Yes Yes Yes Yes Yes N/A N/A N/A

Fre

e-T

V E

merg

ing M

ark

ets

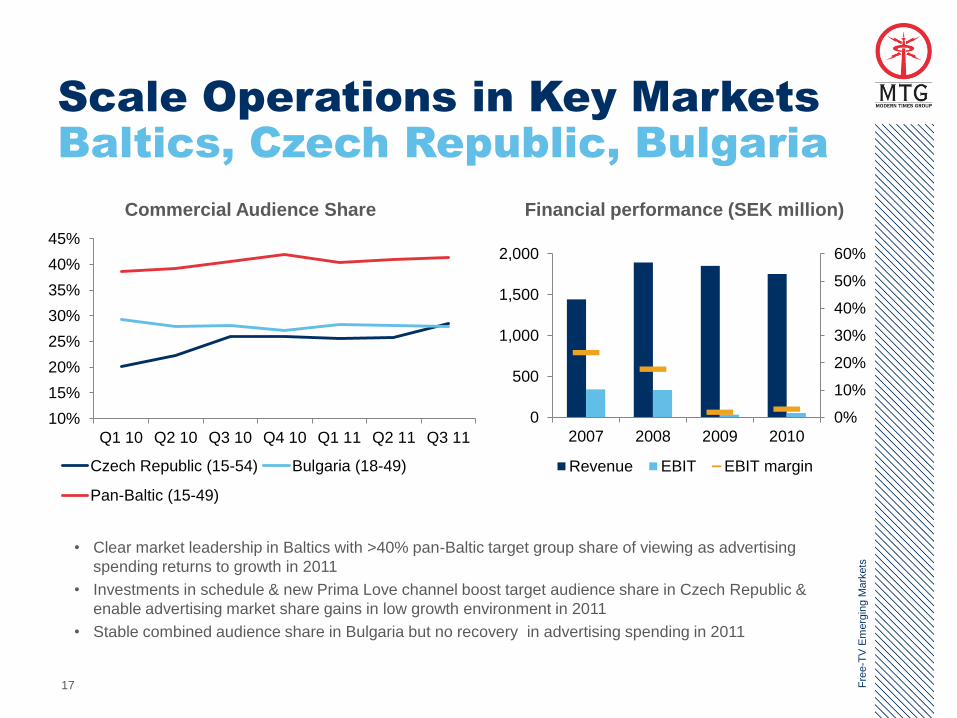

Scale Operations in Key Markets

Baltics, Czech Republic, Bulgaria

17

0%

10%

20%

30%

40%

50%

60%

0

500

1,000

1,500

2,000

2007 2008 2009 2010

Revenue EBIT EBIT margin

Financial performance (SEK million) Commercial Audience Share

• Clear market leadership in Baltics with >40% pan-Baltic target group share of viewing as advertising

spending returns to growth in 2011

• Investments in schedule & new Prima Love channel boost target audience share in Czech Republic &

enable advertising market share gains in low growth environment in 2011

• Stable combined audience share in Bulgaria but no recovery in advertising spending in 2011

Fre

e-T

V E

merg

ing M

ark

ets

10%

15%

20%

25%

30%

35%

40%

45%

Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11

Czech Republic (15-54) Bulgaria (18-49)

Pan-Baltic (15-49)

18

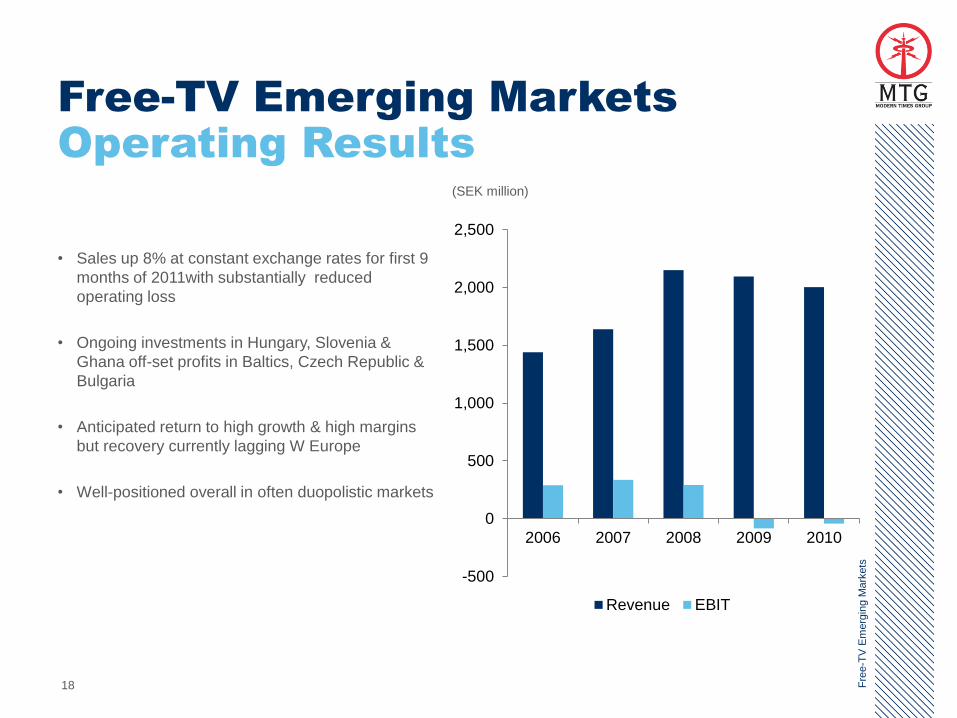

Free-TV Emerging Markets

Operating Results

• Sales up 8% at constant exchange rates for first 9

months of 2011with substantially reduced

operating loss

• Ongoing investments in Hungary, Slovenia &

Ghana off-set profits in Baltics, Czech Republic &

Bulgaria

• Anticipated return to high growth & high margins

but recovery currently lagging W Europe

• Well-positioned overall in often duopolistic markets

Fre

e-T

V E

merg

ing M

ark

ets

-500

0

500

1,000

1,500

2,000

2,500

2006 2007 2008 2009 2010

Revenue EBIT

(SEK million)

0%

5%

10%

15%

20%

25%

0

100 000

200 000

300 000

400 000

500 000

600 000

700 000

2005 2006 2007 2008 2009 2010

Sales EBIT

48%

19%

32%

13%

-3%

2006 2007 2008 2009 201019

Participating in Russian Growth

CTC Media

Operating results (USD millions)

• 38.1% shareholding in Russia’s leading

independent TV broadcaster

• Equity stake acquired for USD 83 million -

equity market value of ~USD 2.2 billion

• Co-Chairmanship & total of 4 Board seats

• 3 national Russian TV networks & 1.5x combined

power ratio = ~19% TV advertising market share

• Sales up 15% y/y in ruble terms to USD 601

million in 2010 with OIBDA margin of 34%

• Cash dividend payments of USD 80 million in

2010 and USD 130 million in 2011

CTC Media Russian Ad sales growth

(RUB)

Audience share (4+)

Fre

e-T

V E

merg

ing M

ark

ets

20 Pay-T

V N

ord

ic

21

Market Position

Premium Content Provider of

Choice

• MTG & 3rd party Free-TV channels

• MTG thematic sports channels – Viasat Football, Viasat Hockey, Viasat Motor,

Viast Golf, Viasat Sport HD

• MTG thematic movie channels – TV1000 Nordic, TV1000 Action, TV1000 Family,

TV1000 Classic, TV1000 Drama

• MTG thematic documentary channels – Viasat History, Viasat Nature,

Viasat Explorer, Viasat Crime

• Leading 3rd party premium channels – music, news, documentaries, kids, nature etc

• MTG & 3rd party HD channels

Pay-T

V N

ord

ic

22

The Evolving Opportunity

Technology Changes Consumer

Behaviour

Owned & Operated

Satellite Platform

Viasat Channels in

3rd Party Networks

Virtual Operator

in 3rd Party B’band Networks

Gatekeeper

Independent

Internet

Environment

Pay-T

V N

ord

ic

0

50

100

150

200

250

2006 2007 2008 2009 2010

HDTV PVR Multi-room

0

1,000

2,000

3,000

4,000

5,000

2006 2007 2008 2009 2010

23

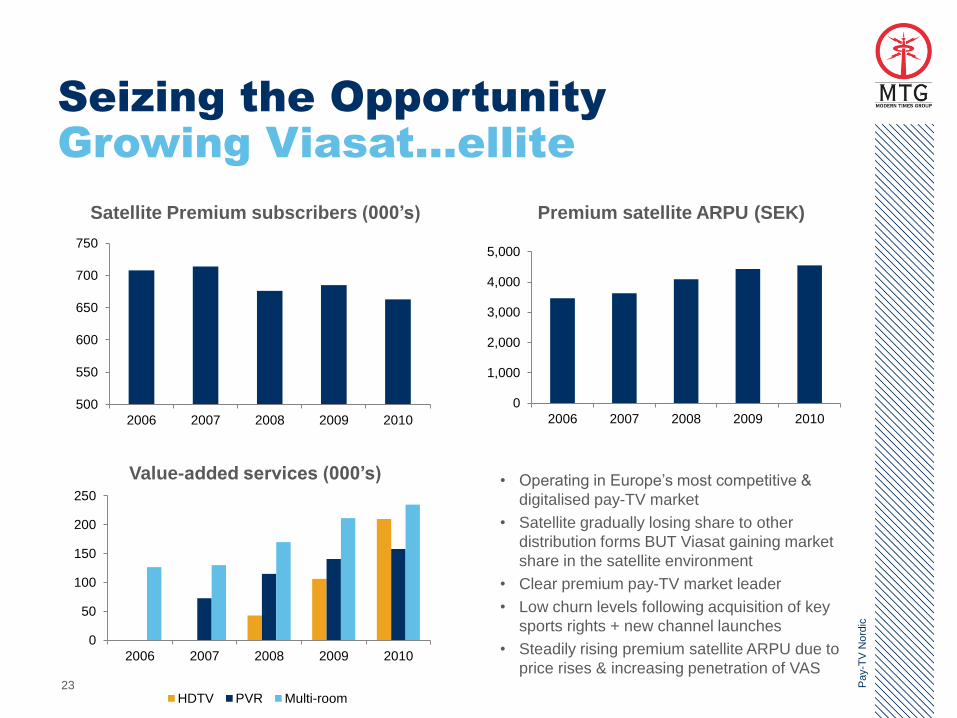

Seizing the Opportunity

Growing Viasat...ellite

Pay-T

V N

ord

ic

500

550

600

650

700

750

2006 2007 2008 2009 2010

Premium satellite ARPU (SEK)

Value-added services (000’s)

Satellite Premium subscribers (000’s)

• Operating in Europe’s most competitive &

digitalised pay-TV market

• Satellite gradually losing share to other

distribution forms BUT Viasat gaining market

share in the satellite environment

• Clear premium pay-TV market leader

• Low churn levels following acquisition of key

sports rights + new channel launches

• Steadily rising premium satellite ARPU due to

price rises & increasing penetration of VAS

24

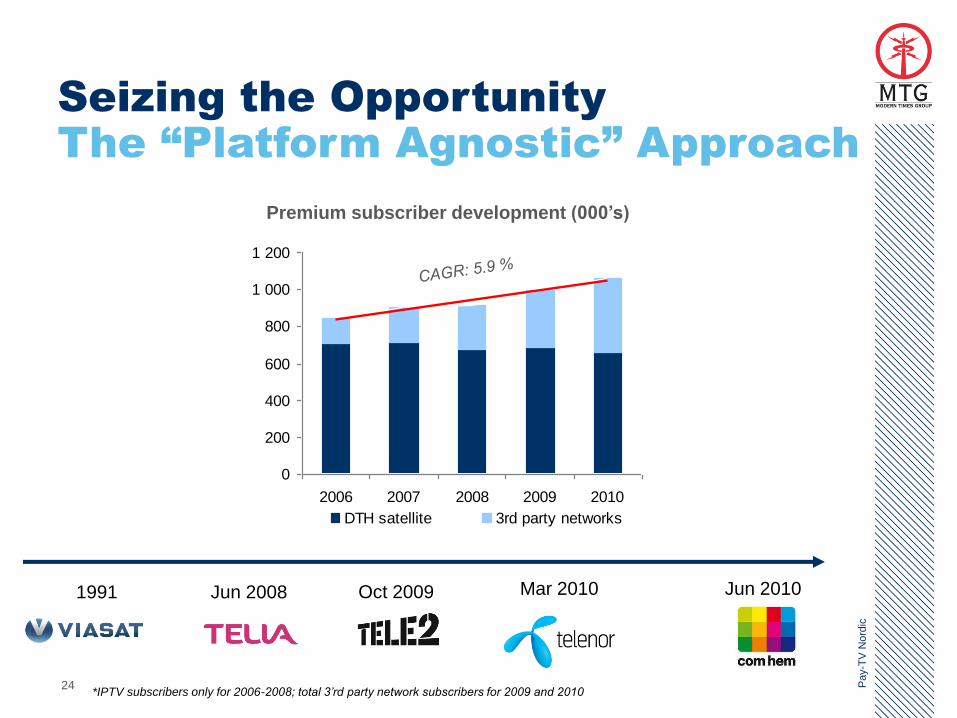

Seizing the Opportunity

The “Platform Agnostic” Approach

Pay-T

V N

ord

ic

Premium subscriber development (000’s)

*IPTV subscribers only for 2006-2008; total 3’rd party network subscribers for 2009 and 2010

Jun 2008 Oct 2009 Mar 2010 Jun 2010

0

200

400

600

800

1 000

1 200

2006 2007 2008 2009 2010

DTH satellite 3rd party networks

1991

25

Seizing the Opportunity

Entertainment “at your Command”

First to Market with Full Service

‘Over-The-Top’ Solution

• Anytime Access all services ‘on demand’

• Anywhere Access subscription online

• Any Device Enjoy subscription on multiple

devices in and out of home

Pay-T

V N

ord

ic

Set -Top Box

PC/Mac

Mobile

Tablet Media

Players

OTT Set-Top box

Game consoles Embedded

TV Set

Applications

26

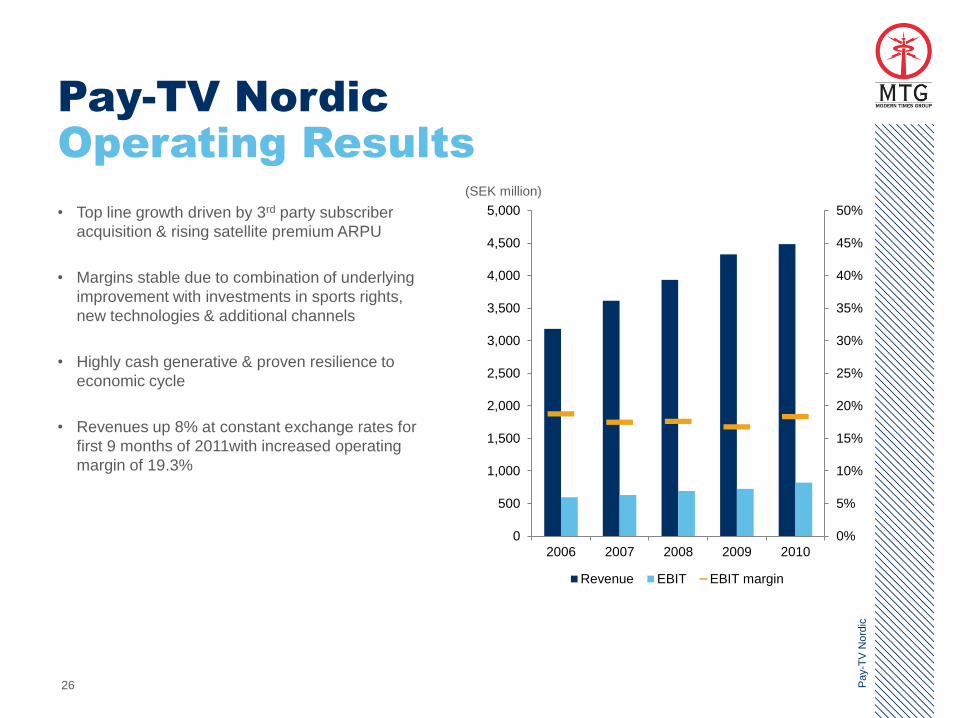

Pay-TV Nordic

Operating Results

• Top line growth driven by 3rd party subscriber

acquisition & rising satellite premium ARPU

• Margins stable due to combination of underlying

improvement with investments in sports rights,

new technologies & additional channels

• Highly cash generative & proven resilience to

economic cycle

• Revenues up 8% at constant exchange rates for

first 9 months of 2011with increased operating

margin of 19.3%

Pay-T

V N

ord

ic

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

2006 2007 2008 2009 2010

Revenue EBIT EBIT margin

(SEK million)

27 Pay-T

V E

merg

ing M

ark

ets

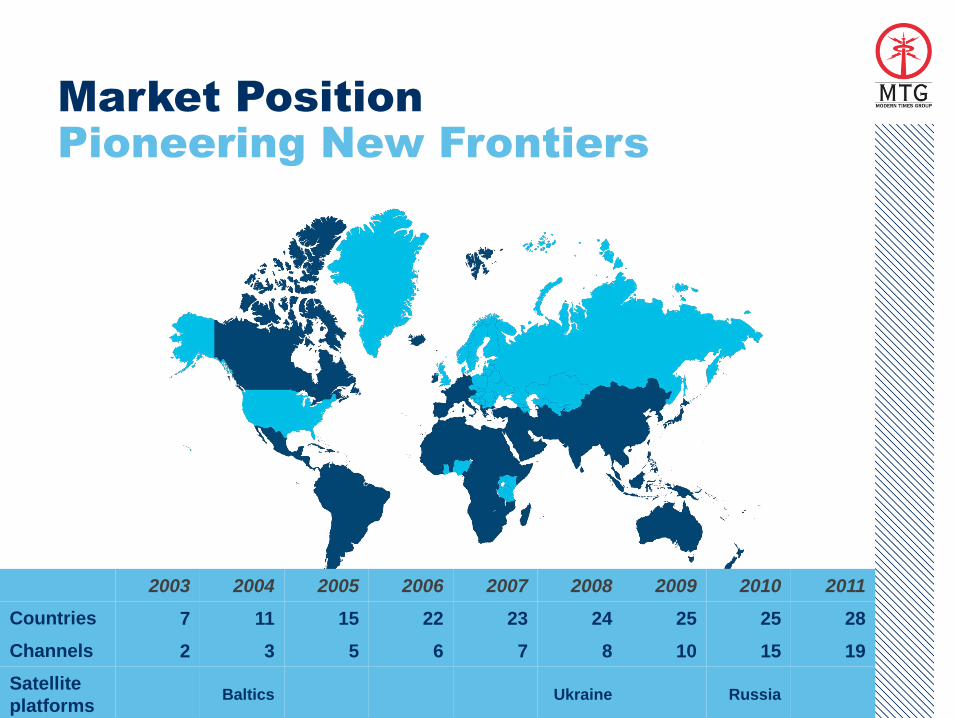

Market Position

Pioneering New Frontiers

28

2003 2004 2005 2006 2007 2008 2009 2010 2011

Countries 7 11 15 22 23 24 25 25 28

Channels 2 3 5 6 7 8 10 15 19

Satellite

platforms Baltics Ukraine Russia

29

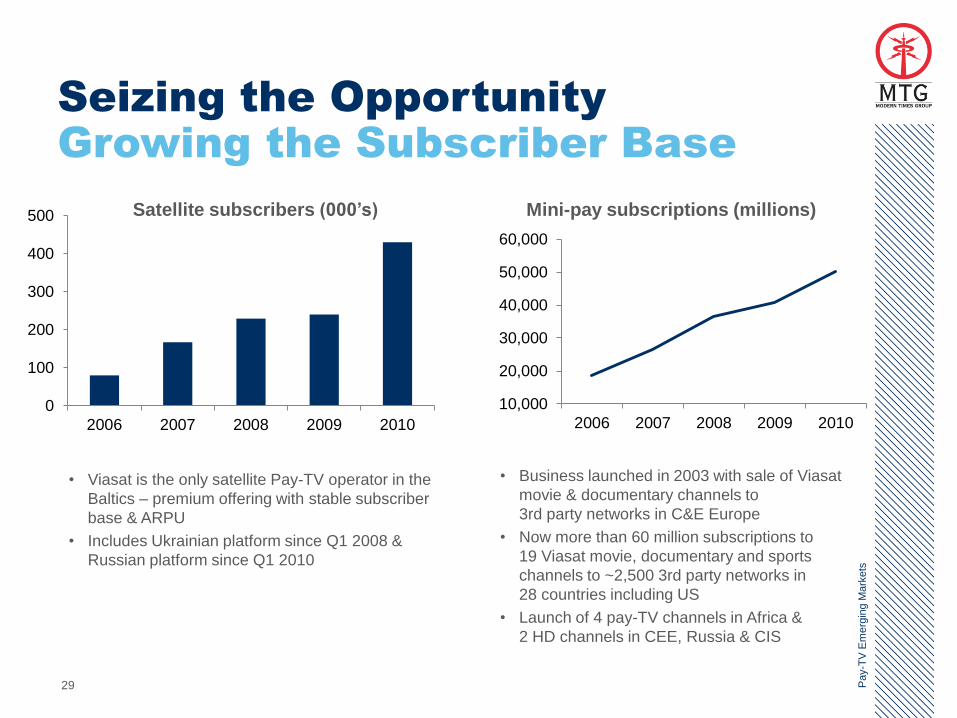

Seizing the Opportunity

Growing the Subscriber Base

• Viasat is the only satellite Pay-TV operator in the

Baltics – premium offering with stable subscriber

base & ARPU

• Includes Ukrainian platform since Q1 2008 &

Russian platform since Q1 2010

Pay-T

V E

merg

ing M

ark

ets

Mini-pay subscriptions (millions) Satellite subscribers (000’s)

• Business launched in 2003 with sale of Viasat

movie & documentary channels to

3rd party networks in C&E Europe

• Now more than 60 million subscriptions to

19 Viasat movie, documentary and sports

channels to ~2,500 3rd party networks in

28 countries including US

• Launch of 4 pay-TV channels in Africa &

2 HD channels in CEE, Russia & CIS

10,000

20,000

30,000

40,000

50,000

60,000

2006 2007 2008 2009 20100

100

200

300

400

500

2006 2007 2008 2009 2010

63%

29%

5% 2% 2%

Viasat NTV + Tricolor Viva Poverhnost' TV30

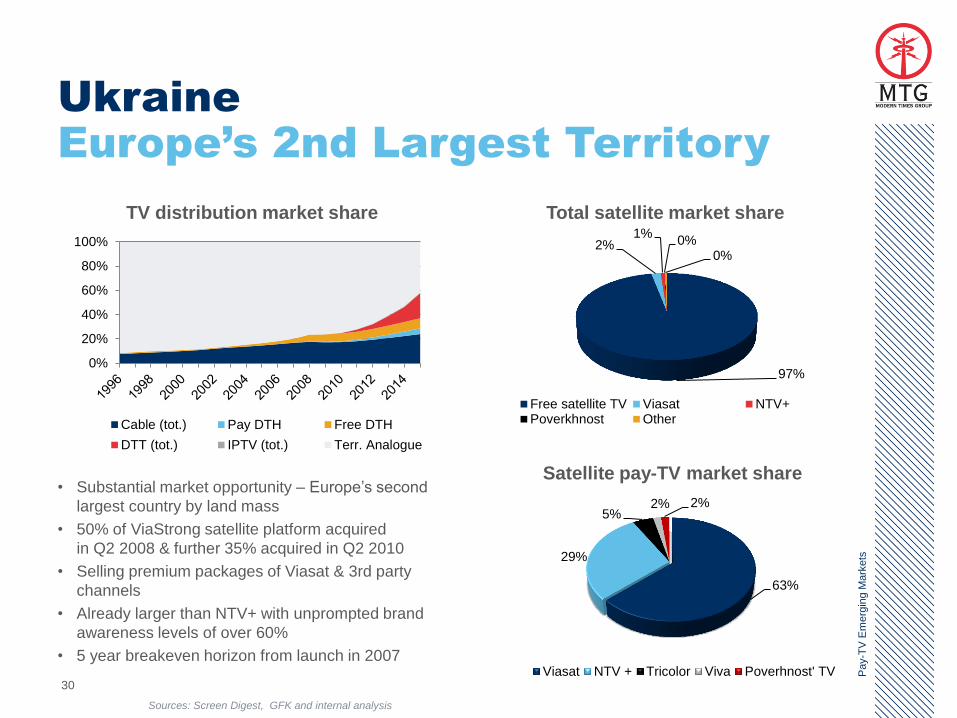

Ukraine

Europe’s 2nd Largest Territory

Pay-T

V E

merg

ing M

ark

ets

Satellite pay-TV market share

Total satellite market share

• Substantial market opportunity – Europe’s second

largest country by land mass

• 50% of ViaStrong satellite platform acquired

in Q2 2008 & further 35% acquired in Q2 2010

• Selling premium packages of Viasat & 3rd party

channels

• Already larger than NTV+ with unprompted brand

awareness levels of over 60%

• 5 year breakeven horizon from launch in 2007

97%

2% 1%

0% 0%

Free satellite TV Viasat NTV+Poverkhnost Other

0%

20%

40%

60%

80%

100%

Cable (tot.) Pay DTH Free DTH

DTT (tot.) IPTV (tot.) Terr. Analogue

TV distribution market share

Sources: Screen Digest, GFK and internal analysis

Tricolor, 83%

NTV+, 10%

Orion-Express,

4%

Raduga TV, 2%

Platform HD, 1%

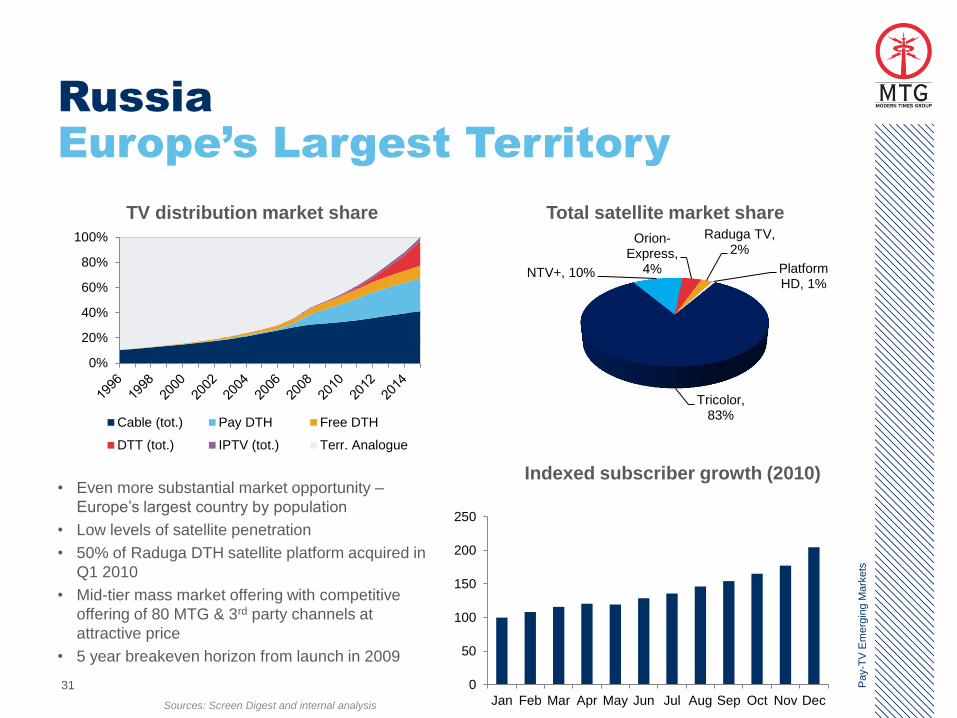

31

Russia

Europe’s Largest Territory

• Even more substantial market opportunity –

Europe’s largest country by population

• Low levels of satellite penetration

• 50% of Raduga DTH satellite platform acquired in

Q1 2010

• Mid-tier mass market offering with competitive

offering of 80 MTG & 3rd party channels at

attractive price

• 5 year breakeven horizon from launch in 2009

Pay-T

V E

merg

ing M

ark

ets

Total satellite market share TV distribution market share

Indexed subscriber growth (2010)

0%

20%

40%

60%

80%

100%

Cable (tot.) Pay DTH Free DTH

DTT (tot.) IPTV (tot.) Terr. Analogue

Sources: Screen Digest and internal analysis

0

50

100

150

200

250

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

32

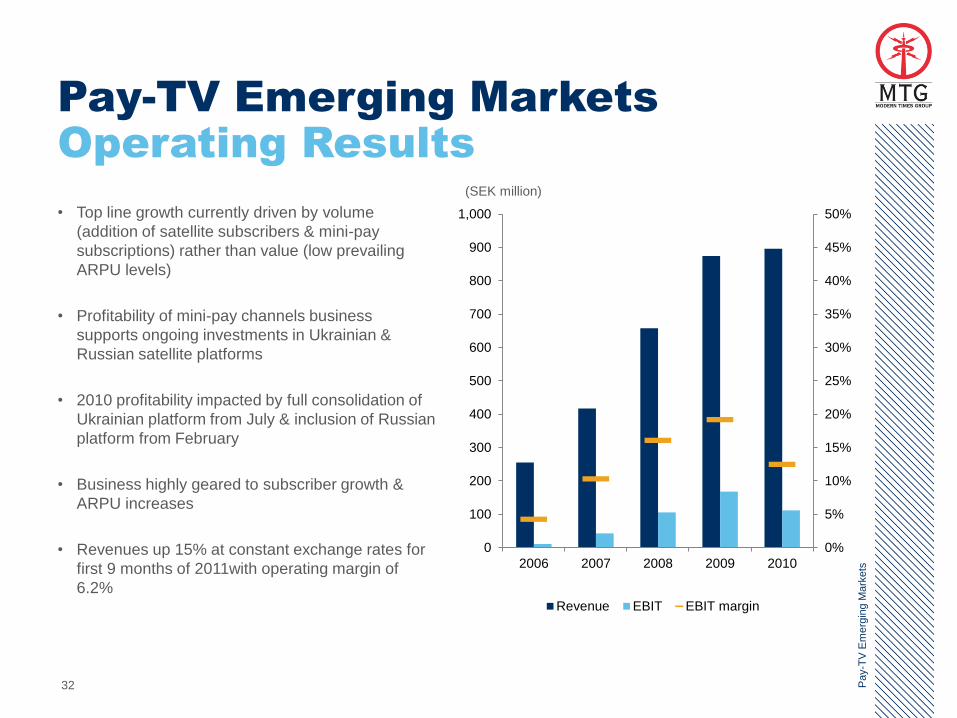

Pay-TV Emerging Markets

Operating Results

• Top line growth currently driven by volume

(addition of satellite subscribers & mini-pay

subscriptions) rather than value (low prevailing

ARPU levels)

• Profitability of mini-pay channels business

supports ongoing investments in Ukrainian &

Russian satellite platforms

• 2010 profitability impacted by full consolidation of

Ukrainian platform from July & inclusion of Russian

platform from February

• Business highly geared to subscriber growth &

ARPU increases

• Revenues up 15% at constant exchange rates for

first 9 months of 2011with operating margin of

6.2%

Pay-T

V E

merg

ing M

ark

ets

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

100

200

300

400

500

600

700

800

900

1,000

2006 2007 2008 2009 2010

Revenue EBIT EBIT margin

(SEK million)

33

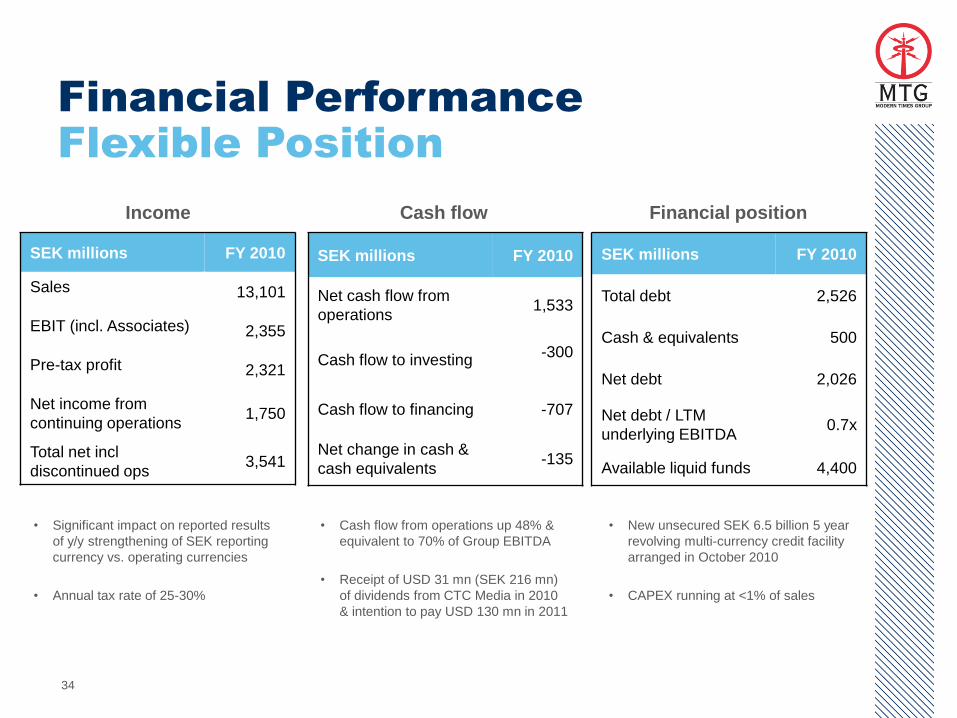

34

Financial Performance

Flexible Position

SEK millions FY 2010

Sales 13,101

EBIT (incl. Associates) 2,355

Pre-tax profit 2,321

Net income from

continuing operations 1,750

Total net incl

discontinued ops 3,541

SEK millions FY 2010

Net cash flow from

operations 1,533

Cash flow to investing -300

Cash flow to financing -707

Net change in cash &

cash equivalents -135

SEK millions FY 2010

Total debt 2,526

Cash & equivalents 500

Net debt 2,026

Net debt / LTM

underlying EBITDA 0.7x

Available liquid funds 4,400

Income Cash flow Financial position

• Significant impact on reported results

of y/y strengthening of SEK reporting

currency vs. operating currencies

• Annual tax rate of 25-30%

• Cash flow from operations up 48% &

equivalent to 70% of Group EBITDA

• Receipt of USD 31 mn (SEK 216 mn)

of dividends from CTC Media in 2010

& intention to pay USD 130 mn in 2011

• New unsecured SEK 6.5 billion 5 year

revolving multi-currency credit facility

arranged in October 2010

• CAPEX running at <1% of sales

35

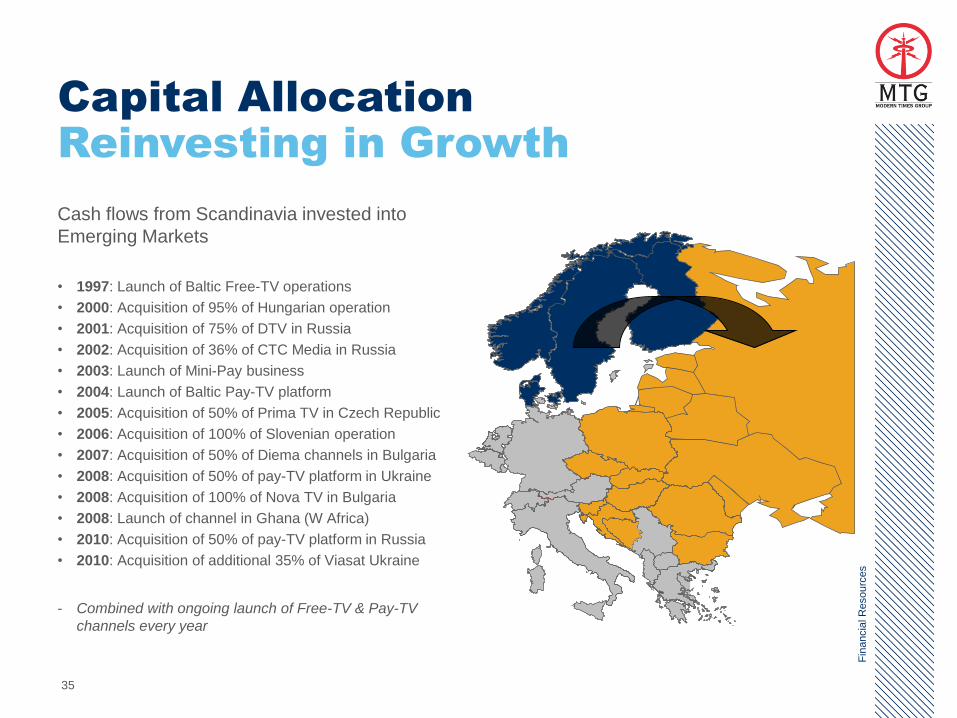

Capital Allocation

Reinvesting in Growth

Cash flows from Scandinavia invested into

Emerging Markets

• 1997: Launch of Baltic Free-TV operations

• 2000: Acquisition of 95% of Hungarian operation

• 2001: Acquisition of 75% of DTV in Russia

• 2002: Acquisition of 36% of CTC Media in Russia

• 2003: Launch of Mini-Pay business

• 2004: Launch of Baltic Pay-TV platform

• 2005: Acquisition of 50% of Prima TV in Czech Republic

• 2006: Acquisition of 100% of Slovenian operation

• 2007: Acquisition of 50% of Diema channels in Bulgaria

• 2008: Acquisition of 50% of pay-TV platform in Ukraine

• 2008: Acquisition of 100% of Nova TV in Bulgaria

• 2008: Launch of channel in Ghana (W Africa)

• 2010: Acquisition of 50% of pay-TV platform in Russia

• 2010: Acquisition of additional 35% of Viasat Ukraine

- Combined with ongoing launch of Free-TV & Pay-TV

channels every year

Fin

ancia

l R

esourc

es

36

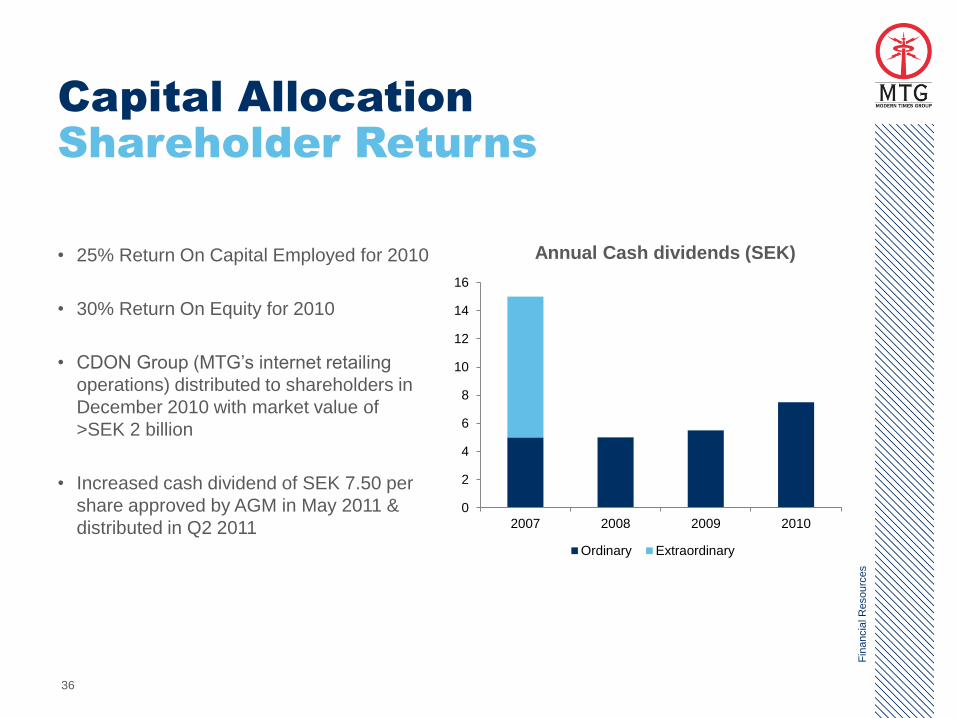

Capital Allocation

Shareholder Returns

• 25% Return On Capital Employed for 2010

• 30% Return On Equity for 2010

• CDON Group (MTG’s internet retailing

operations) distributed to shareholders in

December 2010 with market value of

>SEK 2 billion

• Increased cash dividend of SEK 7.50 per

share approved by AGM in May 2011 &

distributed in Q2 2011

Fin

ancia

l R

esourc

es

Annual Cash dividends (SEK)

0

2

4

6

8

10

12

14

16

2007 2008 2009 2010

Ordinary Extraordinary

37

38

The Lean & Mean

Broadcasting Machine

• Operationally geared growth company with balanced & diversified revenue

mix

• Driving growth primarily through organic expansion & start-ups

• Challenger to incumbents in structurally evolving markets

• Successful multi-channel, multi-platform, multi-territory media house model

• Efficient integrated operating structure yields competitive advantage &

synergies

• Investing healthy cash flows from Nordic region into emerging markets

• Strict cost control, cash management & capital allocation

• Strong & flexible financial position

• Delivering enhanced shareholder returns

Sum

mary

39

For Further Information, please visit www.mtg.se or contact:

MTG Investor Relations

Tel: +44 7768 440 414 / +44 759 009 8188

Email: [email protected]

Nasdaq OMX: ‘MTGA’, ‘MTGB’

Conta

ct

info

rmatio

n