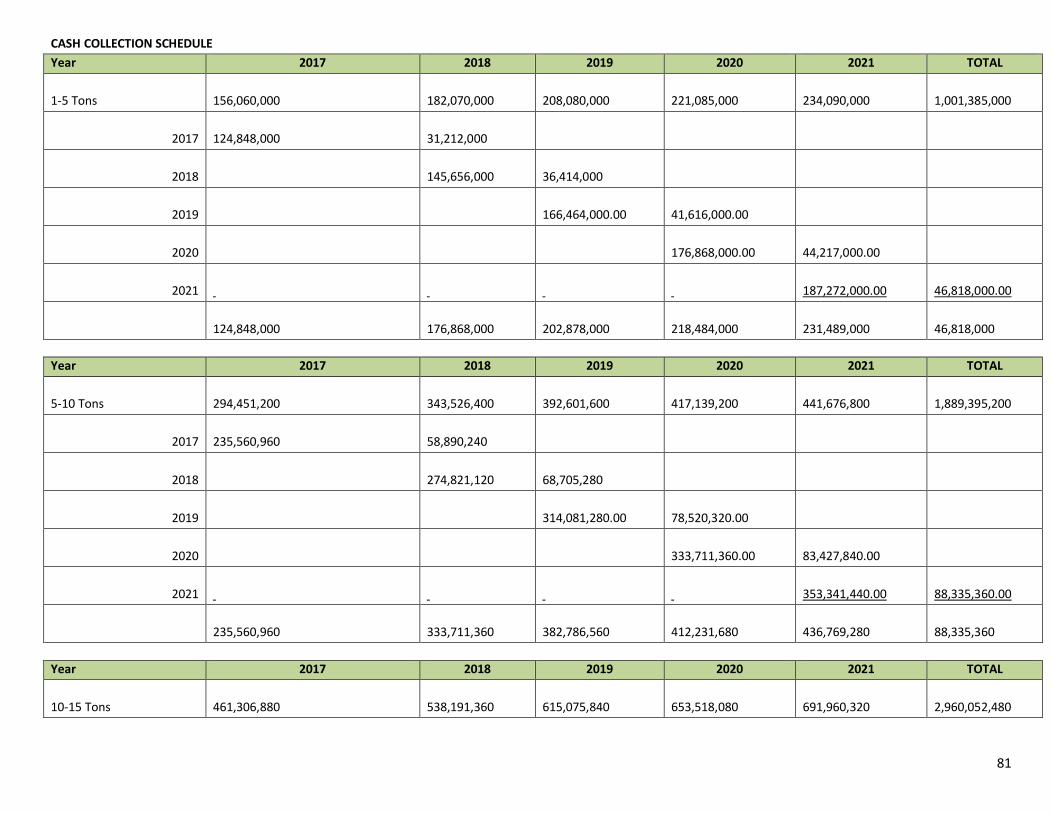

1. - usaid|nigeria expanded trade and transport (nextt) · pdf file · 2017-09-075...

TRANSCRIPT

2

1. INTRODUCTION

1.1 The objectives of the study are as follows:- (a) To prepare a Turnkey Model business plan / Feasibility Study for Cassava Processing to Starch

(Food & Industry Grade).

(b) To enable NEXTT partner with value chain associations and technical teams to produce high level business plans that could enable best practices and attract investors.

(c) To spur investments to improve economic environment of Nigeria and ensure sustainability of

investments. (d) To align with and ensure achievement of objectives of NEXTT.

1.2 On the basis of the foregoing, Agroec Consultants would prepare a Turnkey Feasibility Report

/Business Plan for USAID. Special attention was given to:-

i. The market potential for Starch (Industry and Food Grade) ii. Profitability or otherwise of operations

iii. Technical operations iv. Organization and personnel requirements.

The subsequent pages of this report contains the observations, findings and recommendations of the Consultants.

2. OVERALL ECONOMIC & INDUSTRY SURVEY

2.1 Overall Economic Environment 2.1.1 Nigeria became independent in 1960 and from then the political and economical leadership and

management of the country was transferred to Nigerians.

Since independence, the country has had 15 Governments, 4 Development Plans and several other rolling Plans (the first 1962 – 1968 to the fourth 1975 – 1981 which are all geared towards bringing about a general improvement in the living standard of the population. Despite various

government policies and well articulated development and rolling plans, Nigerians are yet to experience any appreciable improvement in their living condition. while billions of Naira have been budgeted and spent over various Development Plans, the country is yet to find answers to

its basic social and economic problems, which include amongst others:-

A dilapidated and scanty infrastructure; An agricultural system that can neither feed the growing population nor supply the essential

inputs to her industries;

An exogenous demand profile that far outstrips our production capacity;

Declining industrial output and productivity; Massive unemployment and under – employment;

Soaring prices and inflation; A dysfunctional bureaucracy which is allegedly corrupt and inept and yet exercises supreme

control over the economy;

Inadequate and unreliable data for national planning;

High leadership turnover; and A high level of external dependence

2.1.2 In the early days of Nigeria’s independence, agriculture accounted for nearly 60% of Gross

Domestic Product (GDP) and 80% of export earnings (Shaib, Aliyu, Bakshi 1997). Today, agriculture accounts for a third of GDP and less than 1% of export earnings, oil and gas accounting for the rest.

A desirable outcome for the Nigerian population and current government is a strong diversified economy able to:- i. Generate employment

ii. Sustain incomes for its citizens iii. Increase the productivity of agriculture iv. Increase utilization of industrial capacity

3

v. Improve export earnings

2.1.3 The Government has just launched the Economic Recovering and Growth Plan Policy (2017). The highlight of the policy designed to achieve above are as follows:-

i. Review ban on 41 items, free forex market ii. Sell National Assets:- Selected public enterprises/assets will be privatized to optimize their

efficiency and reduce fiscal burden on the government. iii. Create 15 Million Jobs by 2020:- One major strategy is to accelerate implementation of

the National Industrial Revolution Plan (NIRP) through Special Economic Zones (SEZs). The focus will be on priority sectors to generate jobs, promote exports, boost growth and upgrade skills.

iv. Don’t Import a Drop of Petrol by 2020:- Boost local refining for self-sufficiency. Reduce petroleum product imports by 60 per cent by 2018, become a net exporter by 2020, save foreign exchange and prevent reversion to the fuel subsidy regime.

v. Hit 10,000 Megawatts by 2020 – But no selling TCN:- With regards to the power value chain, efforts will be concentrated on overcoming the current challenges which relate to governance, funding, legal, regulatory, an pricing issues across the three main power

segments of generation, transmission and distribution, and ensuring stricter contract and regulatory compliance. “The Plan also aims to increase power generation by optimizing operational capacity to improve the energy mix including through greater use of renewable

energy, encouraging small-scale projects, and building more capacity over the long term. Government will also invest in transmission infrastructure”.

vi. Raise VAT to 15% - Only on Luxury Items:- The plan is to increase the tax base by

raising the VAT rate for luxury items from 5 to 15 per cent from 2018, while improving CIT and VAT compliance to raise 350 billion annually.

vii. Raise Oil Production to 2.5MBPD

viii. Take Inflation Back to Single Digit:- The recovery plan seeks to cut inflation from 15.7 percent in 2017, and down to 9.9 percent by 2020, based on sound macro-economic policies.

ix. Achieve Tomato, Rice, Wheat Self-sufficiency:- Nigeria is projected to become a net

exporter of key agricultural products, such as rice, cashew nuts, groundnuts, cassava and vegetable oil. The government also plan to “open up a minimum of 100,000 hectares of irrigable land through the 12 River Basin Development Authorities by 2020”, and “expand the

use of dams for commercial farming and aquaculture”. x. Provide Two Million Houses by 2020:- Improve access to finance for the construction

industry, e.g. by fast-tracking implementation of the proposed Family Homes Fund, to build

2 million housing units by 2020. “Reposition of the Federal Mortgage Bank of Nigeria by recapitalizing it from N2.5 billion to N5000 billion to meet the housing needs across Nigeria.

The Cassava value chain represents a unique opportunity for the diversification of the Economy

for employment Generation and value added activities.

3. BACKGROUND INFORMATION Cassava – Farm Production, Processing Trends (Global & Nigeria), Opportunities and

Economic Potentials

3.1 Production – Commodity Context

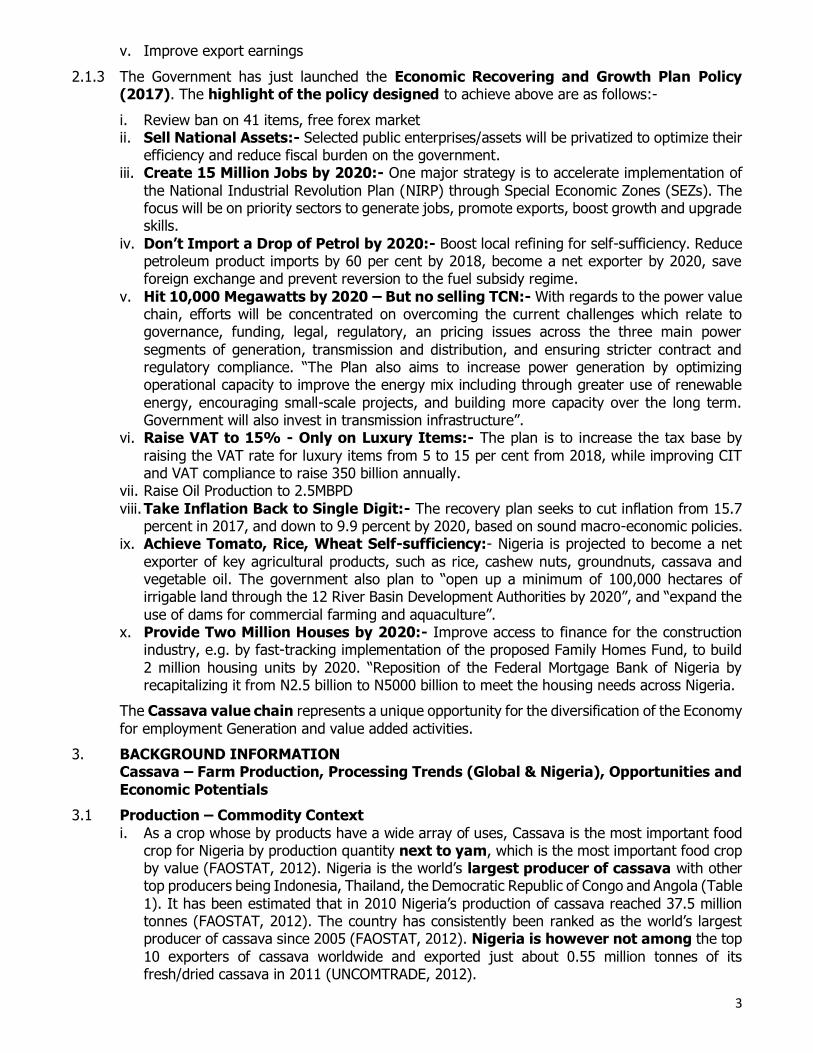

i. As a crop whose by products have a wide array of uses, Cassava is the most important food crop for Nigeria by production quantity next to yam, which is the most important food crop by value (FAOSTAT, 2012). Nigeria is the world’s largest producer of cassava with other top producers being Indonesia, Thailand, the Democratic Republic of Congo and Angola (Table

1). It has been estimated that in 2010 Nigeria’s production of cassava reached 37.5 million tonnes (FAOSTAT, 2012). The country has consistently been ranked as the world’s largest producer of cassava since 2005 (FAOSTAT, 2012). Nigeria is however not among the top

10 exporters of cassava worldwide and exported just about 0.55 million tonnes of its fresh/dried cassava in 2011 (UNCOMTRADE, 2012).

4

Source: FAOSTAT 2012 Table I – Top ten cassava producing countries in 2010 (USD, tonne)

Cassava is also seen to have a high poverty-reduction potential for Nigeria due to its

low production cost (Nweke 2004, FAO 2005). Egesi et al (2006), argue that cassava has been transformed from a reserve commodity for support in times of famine into a rural staple, and subsequently a cash crop. A prior study conducted by Nweke et al (1997) shows that

cassava accounts for 21 percent of the income of cassava producing households.

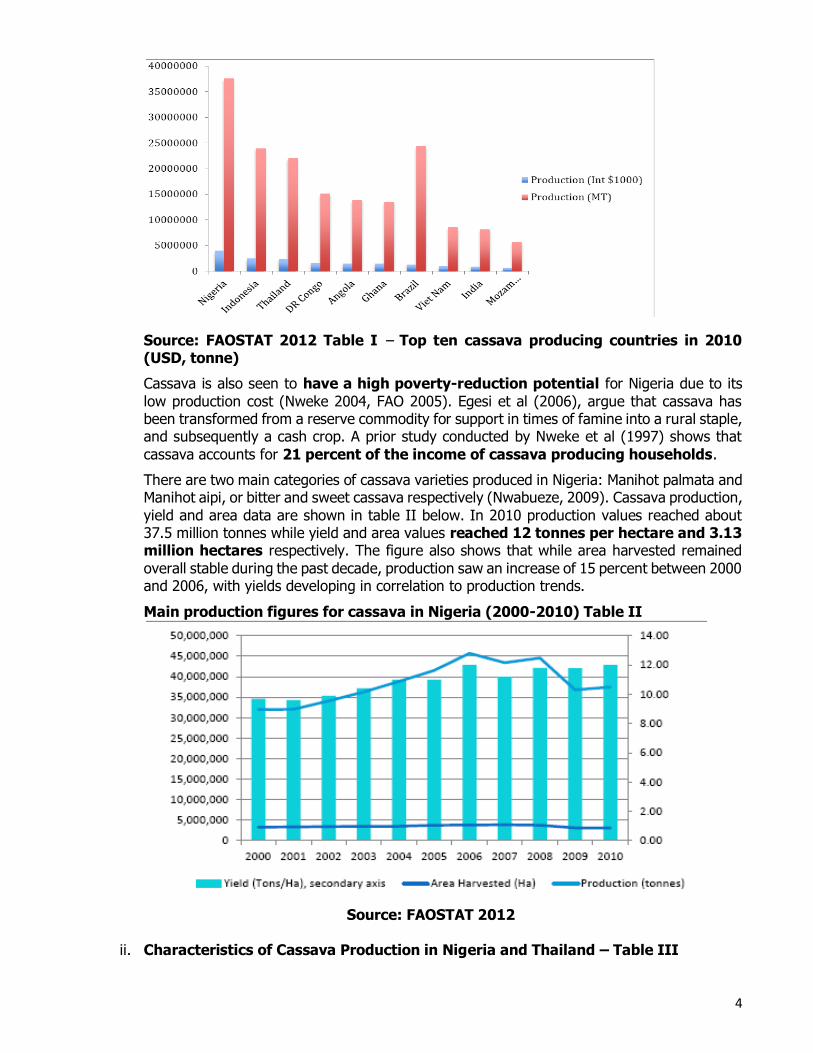

There are two main categories of cassava varieties produced in Nigeria: Manihot palmata and Manihot aipi, or bitter and sweet cassava respectively (Nwabueze, 2009). Cassava production,

yield and area data are shown in table II below. In 2010 production values reached about 37.5 million tonnes while yield and area values reached 12 tonnes per hectare and 3.13 million hectares respectively. The figure also shows that while area harvested remained

overall stable during the past decade, production saw an increase of 15 percent between 2000 and 2006, with yields developing in correlation to production trends.

Main production figures for cassava in Nigeria (2000-2010) Table II

Source: FAOSTAT 2012

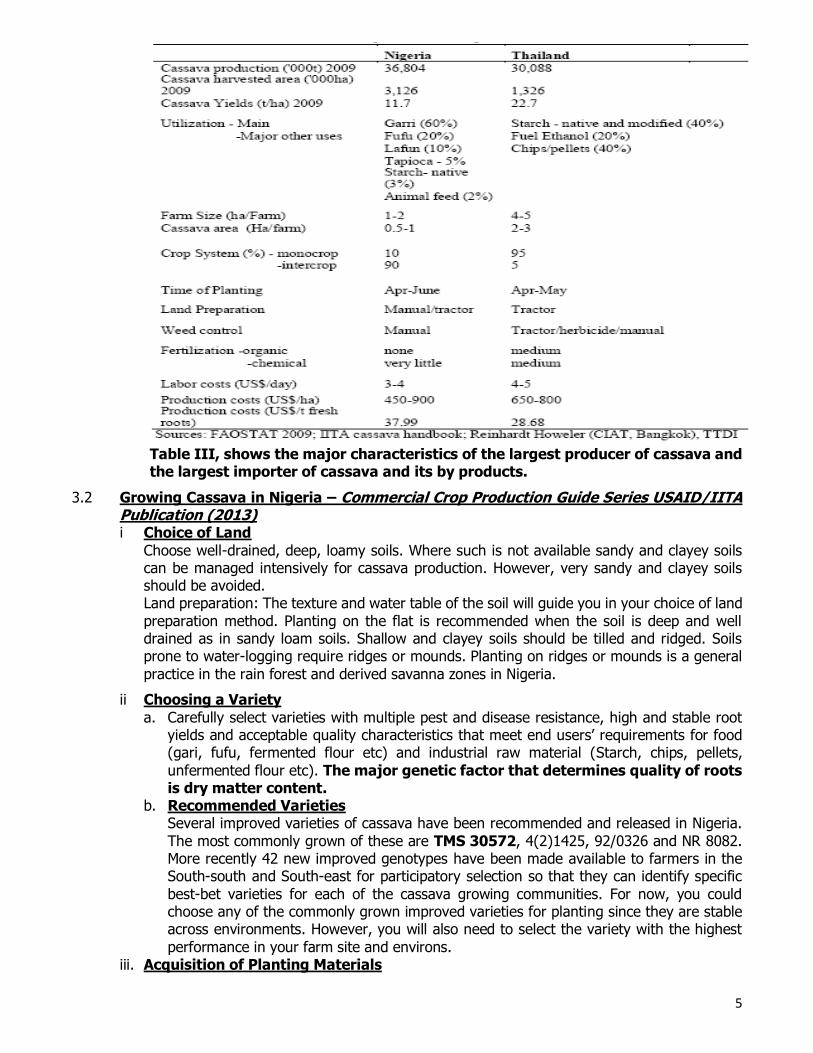

ii. Characteristics of Cassava Production in Nigeria and Thailand – Table III

5

Table III, shows the major characteristics of the largest producer of cassava and the largest importer of cassava and its by products.

3.2 Growing Cassava in Nigeria – Commercial Crop Production Guide Series USAID/IITA Publication (2013) i Choice of Land

Choose well-drained, deep, loamy soils. Where such is not available sandy and clayey soils can be managed intensively for cassava production. However, very sandy and clayey soils should be avoided. Land preparation: The texture and water table of the soil will guide you in your choice of land

preparation method. Planting on the flat is recommended when the soil is deep and well drained as in sandy loam soils. Shallow and clayey soils should be tilled and ridged. Soils prone to water-logging require ridges or mounds. Planting on ridges or mounds is a general

practice in the rain forest and derived savanna zones in Nigeria.

ii Choosing a Variety

a. Carefully select varieties with multiple pest and disease resistance, high and stable root yields and acceptable quality characteristics that meet end users’ requirements for food (gari, fufu, fermented flour etc) and industrial raw material (Starch, chips, pellets,

unfermented flour etc). The major genetic factor that determines quality of roots is dry matter content.

b. Recommended Varieties Several improved varieties of cassava have been recommended and released in Nigeria.

The most commonly grown of these are TMS 30572, 4(2)1425, 92/0326 and NR 8082. More recently 42 new improved genotypes have been made available to farmers in the South-south and South-east for participatory selection so that they can identify specific

best-bet varieties for each of the cassava growing communities. For now, you could choose any of the commonly grown improved varieties for planting since they are stable across environments. However, you will also need to select the variety with the highest

performance in your farm site and environs. iii. Acquisition of Planting Materials

6

Stems of improved varieties can be obtained from National Seed Service (NSS), state offices

of Agricultural Development Programs (ADP), the Cassava Growers Association (CGA) and several out-growers who produce quality stems for sale. Stems are usually tied in bundles each having 50 stems that are 1metre long. Fifty of such bundles are needed to plant 1

hectare of land.

Keep bundles of stems stacked vertically on the soil under a shade. The distal end of the stem should touch the soil. Moisten the soil regularly and keep the

surrounding weed free. This way you can store your stems for more than 3 months. Under low relative humidity and heat stress store your stems in pits under shade.

(a) Stem Quality

Cassava stakes (cuttings) for planting should be taken from plants 8 – 18 months old. Stakes taken from older plants are lignified and they perform poorly due to delayed sprouting and rooting. A mature cassava stem has 3 sections – hardwood, semi-hardwood

and shoot-tip. The hard and semi-hardwood sections are the best for planting. Shoot tips are very fragile and have high mortality rate especially if they are subjected to moisture stress during the first month after planting. If you must source planting materials from an

old field (over 18 months) the semi-hardwood section gives the best quality.

Use sharp tools preferably a secateurs or cutlass to cut stems into stakes for planting. Avoid bruising the stems. Smooth cuts enhance root yields through rapid and uniform root

development from the cut surface. The recommended length of stakes is 20-25 cm with 5 or more nodes. Mini-stakes (10cm) are required for multiplication while micro-stakes (3-5 cm) are used for rapid multiplication.

(b) Handling of Stakes Stakes should be planted soon after they are cut otherwise they get dehydrated and perform poorly. If stakes must be stored for a few days (3-5 days) before planting put

them into transparent polyethylene bags. You can also gather the stakes together under shade and cover with a plastic bag. The high relative humidity and temperature within the bag usually induce rapid sprouting and rooting of stakes. Plant vigour, survival rate and

yields are better if stakes are pre-sprouted before planting.

iv. Plant Population

The optimum plant population for high root yield is 10,000 plants per hectare obtainable when plants are spaced at 1 x 1 m. This population is seldom achieved at harvest due to losses caused by genetic and environmental factors. In other to harvest a plant population near the optimum an initial plant population/ha of 12300 at 0.9 x 0.9m is recommended. Plant spacing

and population will vary depending on if cassava is planted sole or in association with other crops.

Cassava is compatible with many crops when intercropped. The best intercrops of cassava in Nigeria include maize, melon, groundnut, cowpea and vegetables. Other less important intercrops particularly in the South-south and Southeastern Nigeria include yam,

cocoyam, sweet potato, plantain and banana. Non or high branching varieties of cassava are best for intercropping. Profuse and low branching varieties will shade light off the intercrops. In medium and large-scale farms maize is the best intercrop.

a. Weed Control This is one of the major limiting factors to production accounting for more than 25% of the total cost and time of production. Integrated weed control (cultural, mechanical and

chemical) is recommended. The ideal combination will depend on the agro ecology, weed spectrum and level of infestation, soil type and cropping system.

Cassava should be planted early before weeds emerge after land preparation. Adopt

improved fallow practices using live mulch to suppress weeds. Under monocropping, plant varieties with potentials for early canopy closure to reduce weed infestation. Such varieties

7

should be vigorous and resistant to major pests and diseases in addition to having multiple

branching at a medium height. b. Mechanical

Do double or triple harrowing before planting. Weed with hoes or adapted cutlasses 3 or

more times depending on agro ecology and type of weed. More weeding times are required in the forest than in the savanna. Weeds with stolon, rhizome, tubers or deep taproot require more frequent weeding. On a large scale you will require tractor-operated

weeders. c. Chemical

Several pre and post emergence herbicides exist but only few of them are available in Nigeria for controlling weeds in a cassava farm. In the forest zone, apply pre-emergence

herbicides like premextra or dual while in the savanna zone you can apply primextra, dual or cotoran multi immediately after planting to keep your farm weed free for periods ranging from 4-8 weeks. Apply post-emergence herbicides (paraquat or

gramozone) as soon as weeds begin to emerge after the pre-emergence herbicide treatment. They are basically non-selective, localized contact herbicides and should be sprayed with a guard to ensure that only the weeds receive the chemical. If

your field is infested with difficult-to-control weeds like Spear grass (Imperata cylindrica) carefully apply systemic herbicides like Glyphosate, Fusilade or Sarosate. Weather conditions affect herbicide performance. Do not apply herbicides soon after a heavy

rainfall or when it is likely to rain to avoid diluting the chemical and reducing its effectiveness. For best results gramozone should be sprayed only when you are sure of having at least 3 hours of sunshine after spraying. For cost effectiveness and results use

skilled staff for chemical weeds control. Organic herbicides are available. These include Weed Pharm (20% acetic acid), C-Cide (5% citric acid), GreenMatch (55% d-limonene), Matratec (50% clove oil), WeedZap (45% clove oil + 45%

cinnamon oil) and GreenMatch EX (50% lemongrass oil).

v. Fertilizer rate and time of application Ideally, fertilizer recommendations should be based on soil analysis but when this is not

done then use the land history and vegetation as a guide. Lands naturally inundated with Chromolaena odorata (Akintola taku) as weed can support a good cassava crop without fertilizer while the presence of Spear grass or poorly established

vegetation is a signal for fertilization. Under continuous cultivation in the forest zone apply a first dose of 200kg (4 bags) of N: P: K 15:15:15 per hectare or a full small matchbox per plant at 4-6 weeks after planting (June-July). A second dose of 100kg of muriate of potash or a half-

full small matchbox per plant at 14-16 weeks after planting (September) should also be applied. In the savanna zone, apply 200kg (4 bags) of N: P: K 15:15:15 per hectare or a full small matchbox per plant at 4-6 weeks after planting and a second dose of 50kg of muriate of potash

per hectare. Apply fertilizer in holes 5 cm deep and 10 cm radius from the plant. Do not apply fertilizer if the soil is dry.

3.3 Trends – Global and Nigeria

3.3.1 Cassava is one of the world’s most important food crops, with annual global production at approximately 276 million metric tons (MT) in 2013. The Top producing countries globally in 2013 were: Nigeria (accounting for ~19% of the total), Thailand (~11%), Indonesia (~9%), Brazil

(~8%) and Democratic Republic of Congo (~6%).

Global demand for the commodity has been growing significantly between 2004 and

2013 because of its appeal as a food security crop for growing populations in emerging markets, and the growing demand for industrially processed cassava products. Africa accounts for less than 1% of total exports and the cassava production space is dominated by smallholder farmers (25% women). The root crop is a source of livelihood for at least 300 million

people. Virtually all cassava (90%) produced in Africa is used as a staple food for human

8

consumption, providing calories for ~500 million people and constituting ~37% of the

population’s dietary energy requirements.

However, in several African countries, cassava is perceived, not only as a food security crop, but also as a raw material for various types of industries. In some countries, there

are concerted efforts being initiated, sometimes with strong political support at the highest level to make cassava an engine of economic growth. The Global Cassava Development Strategy study commissioned by IFAD and FAO and the Vision 2020 study on Root and Tuber crops stressed the

great potential of cassava to spur rural industrial development, raise rural incomes, and contribute to food security.

3.3.2 The New Partnership for African Development (NEPAD) has also recognized Cassava as a

powerful poverty fighter in Africa and recommended a Pan-African Cassava Initiative based on a transformation strategy which emphasizes better markets, better organization of producers for collective action, and better participation by the private sector.

3.3.3 However, for cassava to be a contributor to development, the demand must grow more rapidly. This can only be made possible by the introduction and promotion of new uses for cassava.

Despite widespread subsistence cultivation of cassava, especially in Africa, the crop’s derivatives have enormous potential for use in industrial processing.

In terms of national policy objectives for the Cassava sector, both the National Investment Plan

(NAIP) and the Presidential Agricultural Transformation Agenda (ATA) include cassava within their main focus crops. The NAIP (2011-2014), provides for increased input supply and distribution, by monitoring the quality standard of fertilizers in the country. The use of organic fertilizers is

encouraged as a complement to inorganic fertilizers.

The NAIP also promotes the export of cassava products by adopting measures including the US African Growth and Opportunity Act (AGOA) and the adoption of appropriate Sanitary and

Phytosanitary Standards, in compliance with the Technical Barriers to Trade agreements of the World Trade Organization.

The country’s Presidential Agricultural Transformation Agenda (2011-15), intends to create 3.5 million jobs along key agricultural product value chains. Furthermore, the Agenda provides for improved mechanisms for the supply of quality inputs, such as subsidized fertilizers and seeds to farmers, as well as guaranteed farm-gate minimum prices for many crops. The Presidential

council, which is in charge of implementing the Agenda, also intends to increase Cassava production up to 50 million tonnes by 2015, while supporting its export.

3.3.4 Lessons can be drawn from success stories of agricultural transformation in other countries such as Thailand and Vietnam. The Federal Government of Nigeria launched the Agricultural Transformation Agenda (ATA) in 2012, as a private sector-driven, agri-business

based, development of commodity value chains to create wealth, attain industrialization and sustain livelihood. This program which was built on commodity value chains drove Nigeria’s cassava production to 54 million tons in 2015. Based on the impressive

food production, Nigeria met the Millennium Development Goal of halving the number of hungry people (MDG 1 - poverty reduction) in 2013, two years ahead of 2015 target.

3.4. Opportunities (By Products)

3.4.1 The huge and untapped market opportunities of cassava in Africa can be effectively exploited for transforming Africa’s agriculture. The challenge today is to increase productivity, marketing opportunities and profitability through effective and efficient cassava value chain development.

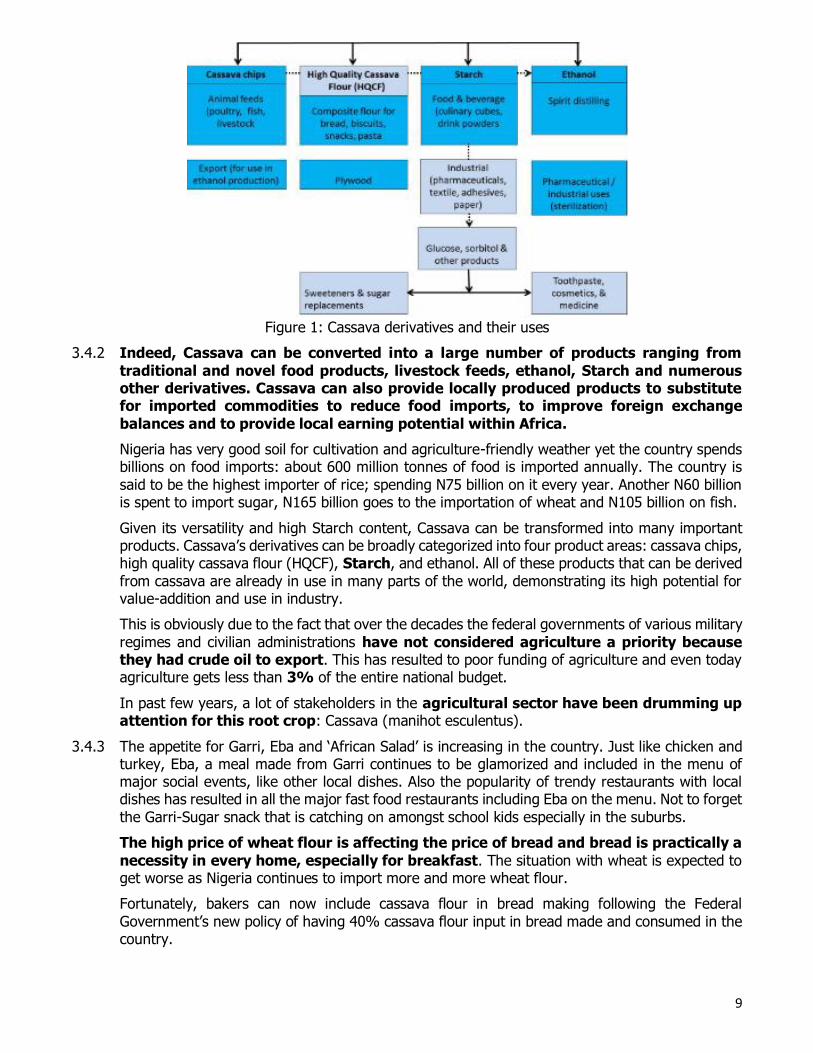

Cassava has diverse end-uses (Figure 1) despite its widespread subsistence cultivation in Africa for mainly food. Given its versatility and high Starch content, it can be transformed into many important products/derivatives (cassava chips, high quality cassava flour (HQCF), Starch, and

ethanol).

9

Figure 1: Cassava derivatives and their uses

3.4.2 Indeed, Cassava can be converted into a large number of products ranging from

traditional and novel food products, livestock feeds, ethanol, Starch and numerous other derivatives. Cassava can also provide locally produced products to substitute for imported commodities to reduce food imports, to improve foreign exchange

balances and to provide local earning potential within Africa.

Nigeria has very good soil for cultivation and agriculture-friendly weather yet the country spends billions on food imports: about 600 million tonnes of food is imported annually. The country is

said to be the highest importer of rice; spending N75 billion on it every year. Another N60 billion is spent to import sugar, N165 billion goes to the importation of wheat and N105 billion on fish.

Given its versatility and high Starch content, Cassava can be transformed into many important products. Cassava’s derivatives can be broadly categorized into four product areas: cassava chips, high quality cassava flour (HQCF), Starch, and ethanol. All of these products that can be derived

from cassava are already in use in many parts of the world, demonstrating its high potential for value-addition and use in industry.

This is obviously due to the fact that over the decades the federal governments of various military

regimes and civilian administrations have not considered agriculture a priority because they had crude oil to export. This has resulted to poor funding of agriculture and even today agriculture gets less than 3% of the entire national budget.

In past few years, a lot of stakeholders in the agricultural sector have been drumming up attention for this root crop: Cassava (manihot esculentus).

3.4.3 The appetite for Garri, Eba and ‘African Salad’ is increasing in the country. Just like chicken and turkey, Eba, a meal made from Garri continues to be glamorized and included in the menu of major social events, like other local dishes. Also the popularity of trendy restaurants with local dishes has resulted in all the major fast food restaurants including Eba on the menu. Not to forget

the Garri-Sugar snack that is catching on amongst school kids especially in the suburbs.

The high price of wheat flour is affecting the price of bread and bread is practically a

necessity in every home, especially for breakfast. The situation with wheat is expected to get worse as Nigeria continues to import more and more wheat flour.

Fortunately, bakers can now include cassava flour in bread making following the Federal

Government’s new policy of having 40% cassava flour input in bread made and consumed in the country.

10

The new policy, expected to come into operation on July 1, 2012, proposes that bread made in

the country will comprise 60% wheat and 40% processed cassava flour. Brazil is usually cited as the country where cassava content in bread is highest at 30%.

In the meantime, while stakeholders in the bakery and confectionery sector have expressed

doubts as regards the success of the policy because of the plethora of logistic and operational challenges that are yet to be solved, some say 100% cassava bread stands a chance of becoming a delicacy someday, just like corn bread. Also some noodle makers are quietly using cassava to

supplement wheat flour that is more expensive. The chances are that bread consumers may not even know their bakeries have switched to cassava flour. But there is more to Cassava than all of this.

Over 800 million people worldwide depend on cassava for food. The consumption in West Africa is more than 120kg per annum/per capita while that of Central Africa Republic is more than 300kg per annum/per capita.

3.5 Challenges, Risks and Contribution to addressing challenges 3.5.1 The major challenges to the development of the cassava subsector in Africa include the following:-

(i) Low yields: The yields of African cassava producers are 37 - 64% below the global value. In 2013, Nigeria reached 14.1 tons/ha, similar to Brazil but ~37% less than Indonesia (22.5 tons/ha) and Thailand (21.8 tons/ha) (FAOSTATS accessed 2015). The yields of the other top African producers are also low. Cameroon’s cassava yield in 2013 was at 14.7 MT/Ha, while

Angola achieved yields similar to those of Nigeria at 14.1 tons/ha. DRC’s 2013 yield was 8.0 tons/ha, less than 60% of Nigeria’s yield. Yields are low by global standards, mainly due to the prevalence of traditional subsistence farming techniques with little or no use of inputs.

(ii) Variety improvement: Improved crop varieties remain the engine of agriculture. Successful value-added chains of cassava in Thailand and Brazil take advantage of the increased productivity, and profits for actors along the chain, that improved varieties of

cassava brings. Under the cassava transformation emphasis will be placed on the development of new varieties that respond well to inputs, the use of biotechnology approaches to accelerate breeding, expanding the genetic base with novel traits, and capacity

building of a new generation of cassava breeders. (iii) Identification of cassava varieties that respond to increased use of inputs

especially fertilizer: Cassava breeding in Nigeria test materials across agro-ecologies under

zero input conditions typical of how farmers have always grown cassava. But the emphasis is now to grow cassava under best production practices; there is a need to improve cassava for these conditions. In the first instance, 60 advanced breeding lines in the IITA and NRCRI

breeding programs will be tested across the cassava belt of Nigeria under optimum production conditions. This activity is expected to result in the identification of genetically improved cultivars that respond to fertilizer best suited in each agro-ecological zone. In addition, an

emphasis will be placed traits important to the value-added chains, especially high Starch yields.

To ensure quick adoption by farmers and processors, lines already at an advanced stage in

the breeding pipeline will be evaluated for performance and quality traits in collaboration with farmers and processors involved in the five value-added chains to determine those that best meet commercial quality requirements. It is important that farmers include seed producers

in the respective SCPZ clusters. They can contribute to quick dissemination of new selected materials.

(iv) Fragmented, Smaller-Holder Farms: In Africa, cassava production is carried out in

predominantly smaller-holder and fragmented farms with rudimentary technologies, low use of inputs limited economy of scale. Six million small-scale farmers account for 90% of the production in Nigeria.

(v) Limited Adoption of Improved Seeds: Small-scale farmers rarely use improved planting materials (clean, healthy seeds), and the sub-sector is dominated by disease-prone local

11

varieties with long maturation periods and low yield potential. IITA and African NARS (National

Agricultural Research System) have played leading roles in the development of improved cassava varieties that are multiple disease and pest resistant, early maturing, and high yielding. These varieties have the potential to raise productivity by up to 30-40 tons/ha.

Thirty-two African countries have released an estimated 384 high yielding varieties between 1970 and 2014. These varieties are high yielding with good levels of multiple disease and pest resistance as well as of acceptable quality for food, feed and industrial uses in Africa. While

the combination of these new varieties and better agronomic practices could increase yields per unit area by at least 40%, the rate of adoption by smallholder farmers has been low.

The dissemination of these varieties has often suffered from the lack of a reliable planting

material distribution system from National Agricultural Research Systems (NARS) because of weak extension systems, insufficient quantities of planting material, and delays in distributing the approved planting materials.

This compels farmers to continue to grow local, low yielding, varieties. This is exacerbated by inadequate location specific knowledge on fertilizer use, and other cultural practices such as

weed and pest and disease management for cassava systems and late planting specifically in southern Africa region where maize comes first. Private companies are also not involved in distribution because cassava is propagated vegetatively, and it takes one year to produce cassava stems material compared to three to five months for grain seeds.

(vi) Low use of Herbicides: Low use of herbicides and pesticides presents another obstacle. In the case of south-eastern Nigeria, only 3% of farmers use herbicides because they do not

know about them, lack the technical skills to use them, are not able to afford them or are under pressure from local NGOs to avoid them. When they do use them, most use insufficient amounts of herbicides to save cost. Instead increasing herbicide use would reduce the need

for weeding and free up labor for other activities.

(vii) Limited use of Fertilizers and Irrigation: Fertilizers are used infrequently, and even when used, the amounts are below the recommended levels because of the high cost. Use

of irrigation techniques is also a constraint in almost all cassava farms in Africa as the system of cultivation is predominantly rain-fed.

(viii) High labor use: Cassava farming is highly labor-intensive and related costs can account

for up to 90% of total production costs. For example, the cost of developing and preparing land is quite high. In Oyo and Benue states of Nigeria, 98% of the average cassava production cost of USD 700 per hectare is labor (ridging, planting, weeding, etc.) and 2%

is inputs (fertilizers, seeds).

(ix) Low use of mechanization: A low level of mechanization characterizes small-scale

cultivation. For example, tractors are used in just 10% of Nigeria’s cassava cultivation. Harvesting is done manually and is therefore time-consuming and expensive. In both small-scale and commercial farming, 8-12% of cassava roots are lost due to sub-

optimal harvesting methods. A survey conducted by the African Agricultural Technology Foundation (AATF) during the 2004 Triennial Symposium of the International Society for Tropical Root Crops – Africa Branch revealed a consensus among African cassava experts that the most important intervention to increase the competitiveness of the cassava industry

was the adoption of mechanization in cassava production. Such mechanization will enable a reduction of labor costs, thus bringing down the cost of cassava as a raw material and stimulating reliance on local cassava as a competitive raw material for various industries.

(x) High Prices of Cassava Roots: Cassava prices vary greatly from country to country as there is no global commodity market and production costs differ vastly due to varying levels

of input use. For example, in 2012, the average price for cassava was USD 161/ton in Nigeria (10% mechanized), and USD 67/ton in Thailand (highly mechanized).

12

Cassava derived products must be price-competitive with their substitute products like corn

Starch and ethanol made from other sources.

(xi) Limited access to finance: Both commercial and smallholder farmers have limited access to finance. In Nigeria the agricultural sector accounts for 42% of GDP but has 2% of all

formal credit flows. Reasons for this include:- - Conditions to access a bank loan are stringent; - Interest rates are high (17-25%);

- And commercial banks do not offer conducive payment terms for agro- based activities (e.g., fixed repayment periods that may not match annual cropping, especially when loan release is not coordinated with growing cycles). As a result, commercial farmers

may produce lower volumes.

(xii) Trade and Transport: Smallholder cassava producers have weak and limited access to markets. The high transportation costs and the need to process cassava within 48 hours of

harvesting because of its perish ability, makes small producers to sell most of their product at local markets. The high fragmentation (scattered farms) and poor infrastructure make it difficult to develop commercial-scale aggregation. Poor roads and inadequate storage

facilities drive up prices and increase postharvest losses.

(xiii) Weak Access to Markets: Agricultural markets world-wide are characterized by market structures, both quantitative – aggregation, storage, and processing facilities, and

qualitative – quality standards, information services, logistics for distribution of agricultural products. Many of these structures do not exist in many African countries for cassava distribution.

(xiv) 3 year Cassava Burst Cycle: Nigerian cassava farmers produce for an inelastic food market. This leads to wide swings of prices every other harvest, in the absence of a

minimum price guarantee schemes by government. For example, the price of a ton of cassava in 2007 was N5,000-N6,000 in central Nigeria due to overproduction, partly in response to an appeal to farmers by the last Presidential cassava initiative to increase

cassava production for new markets of high quality cassava flour, Starch, and chips, markets that were only partly achieved. Because of the depressed prices, many farmers switched to other crops and production output fell. By March and August 2009 cassava sold at farm

gate in most of central Nigeria for N12,000 – N15,000 per metric ton; given the good prices many farmers went back to cassava production, leading to an overproduction. In 2011 cassava roots are selling for between N5,000 – N8,000 a ton; and N16,000 in 2016: essentially completing the burst-boom cycle of cassava that occurs every three years;

cassava in Nigeria is a 15-18 months harvest and two crop cycles is 3 years.

3.5.2 Contributions Towards Addressing the Challenges:-

i. IITA has pioneered since the 1970s and will continue to propel the Cassava research improvement in Africa to increase and sustain cassava production and utilization in sub-Saharan Africa. The Institute, working with national partners, has been actively involved in

the development of Value chains of the cassava subsector in Africa since the 2000s.

Examples include the Rural Sector Enhancement Program, Pre-emptive management of Cassava Mosaic disease in Nigeria, and the Cassava Transformation Agenda all in Nigeria.

Under the Nigeria Cassava Presidential Initiative on Cassava (1999 – 2007), IITA research efforts increased cassava production by 10 million tons, making Nigeria global top producer. Similar efforts in Cameroon also helped the country to double cassava production. Other

projects such as the Support for Agricultural Research for Development of Strategic Crops which is funded by the Africa Development Bank, and the Cassava Enterprise Development Project are also driving the production and productivity of Cassava. In 2004, the New

Partnership for Africa’s Development (NEPAD) launched the NEPAD Pan African Cassava Initiative (NPACI) as a means to tap on the enormous potential of cassava in Africa for food security and income generation.

13

The project made significant contributions towards cassava production, commercialization and

social marketing in Southern Africa with specific emphasis in Malawi, Zimbabwe and Mozambique. These efforts have contributed to food security and incomes in those countries. Other projects such as Great Lakes Cassava Initiative and Cassava Weed Management Project

are also having an impact.

ii. What should be done in the short-term, medium term: To address the challenges currently constraining the full realization of cassava subsector for the agricultural

transformation of African economies, there are number of recommendations that stakeholders across the cassava value chain should act upon:- Develop a market-oriented strategy with emphasis on value-addition and productivity

enhancement along the whole value-chain. Launch a roadmap for the cassava sub-sector reform setting out clear implementation

plans focusing on the integration of food production, storage, food processing and

industrial manufacturing by value chains (‘farm to fork’) where countries have comparative advantages to resolve the challenges of the subsector, and setting the path for its improvement in the short (1-5 years) and medium (5-10 years) terms. This should be a

deliberate, strategic, sustained set of actions for a private-sector-led agricultural transformation as there are no “quick fixes” for sustained economic growth and poverty alleviation (Short term).

Deploy integrated pest/pathogen management (IPM) programs backed with clean seed production, and effective surveillance to prevent geographic expansion of cassava brown streak disease (CBSD) and also to control endemic diseases like cassava mosaic and

cassava bacterial blight, and control emerging insect pests on cassava, such as spiralling whitefly and papaya mealy bug (short to medium term).

Change mindset of small and medium farmers to treat agriculture as a business and create

incentives and efficient input delivery systems including private-sector enabled Agricultural Equipment and Mechanization: Leasing Services to make cassava production financially attractive to end-users (Short term).

Increase awareness of potential to produce and use cassava substitutes through targeted and frequent advocacy efforts for cassava value chains (short term).

Develop infrastructure to reduce the costs of aggregation and transport that currently

make many locally made products non-competitive (Medium term). Continue funding R & D on: (i) using advance breeding technologies to rapidly produce

varieties more suited for production and processing, and pilot efforts to demonstrate

feasibility of substituting cassava products for imported goods; (ii) climate-smart agriculture that promote sustainable agricultural management systems, and (iii) Research and development that enhance efficiency of production along the value chain as well as strengthening of the national agricultural systems. (Short to medium term).

Build strong farmer groups and linkages with appropriate financing that level the playing field so that they are able to effectively access inputs and markets and receive fairer product and input prices, and promote backward integration into commercial farming to

buttress supply (short term). Provide access to expertise and know-how through Technical Assistance to increase

productivity and competitiveness of the commercial cassava farming sector (Short to

medium term). Create output markets links for farmers, primary and secondary processors, aggregators,

farmer cooperatives, small and large traders by improving regional and global market links

for increased value chain efficiency and to access to regional and global agricultural trade (short to medium term).

Facilitate public-private partnerships (PPPs) to encourage cross-sector collaboration and

knowledge sharing especially in research and development, and initiatives along the

14

agricultural value chain to develop infrastructure and/or build stronger farmer linkages,

e.g. Agricultural Enterprise Processing Zones (medium term). Develop new policies, institutions and financing structures to drive sector growth (Short

to medium term): Deregulation of seed and fertilizer sectors; marketing reforms to

structure markets; innovative financing for agriculture for farmers inputs and credit guarantees and low interest rate, long-term debt products for construction of new processing facilities; new agricultural investment framework.

Improve the legal framework in land acquisition and transfer to ensure ownership and right of use, and facilitate development of a system for making available unutilized government and communal lands for agricultural use in order to facilitate contiguous farming for farmers’ groups/organizations and industries (Short to medium term).

Develop sustainable market information, e.g. private-led; develop warehousing system (Bonded system for easy access to finance); develop bulking system for primary product, e.g. fresh tubers; and upgrading of informal markets, especially for primary commodities

(short term). Capacity building for all actors of the value chain including farmer education and

commercialization through public and private extension (short to medium term).

Create specific women and youth in cassava agribusiness programs (short term)

3.5.3 Vision for Sustainability:-

i. African cassava industrialization will create wealth, jobs and promote sector-wide efficiency and productivity growth. It will enhance and meet the demand of emerging industrial needs, traditional products and global demand by reducing production costs and increasing the output of high quality industrial products to strengthen the continent’s position in the global

context for competition.

Five major cassava value chains are proposed for industrialization based on the demand and

supply side targets for various African countries and elsewhere as estimated from the FAOSTATS database:- High Quality Cassava Flour (HQCF),

Starch, Chips, High Fructose Cassava Syrup (HFCS) and

Ethanol

These value chains offer tremendous potential to fuel the economic growth in the continent as this will create jobs for women and youth, improve food security and

generate wealth. Production should be expanded to:- Meet domestic, industrial demand and export markets through promotion of industrial

applications of key value chains (HQCF, livestock feed, Starch, ethanol, etc.);

Encourage the involvement of large scale farming as a driving force for industrialization; and encourage private sector investment and engagement. Each country can develop its industry according to its available resources and market opportunities within a globally

competitive framework.

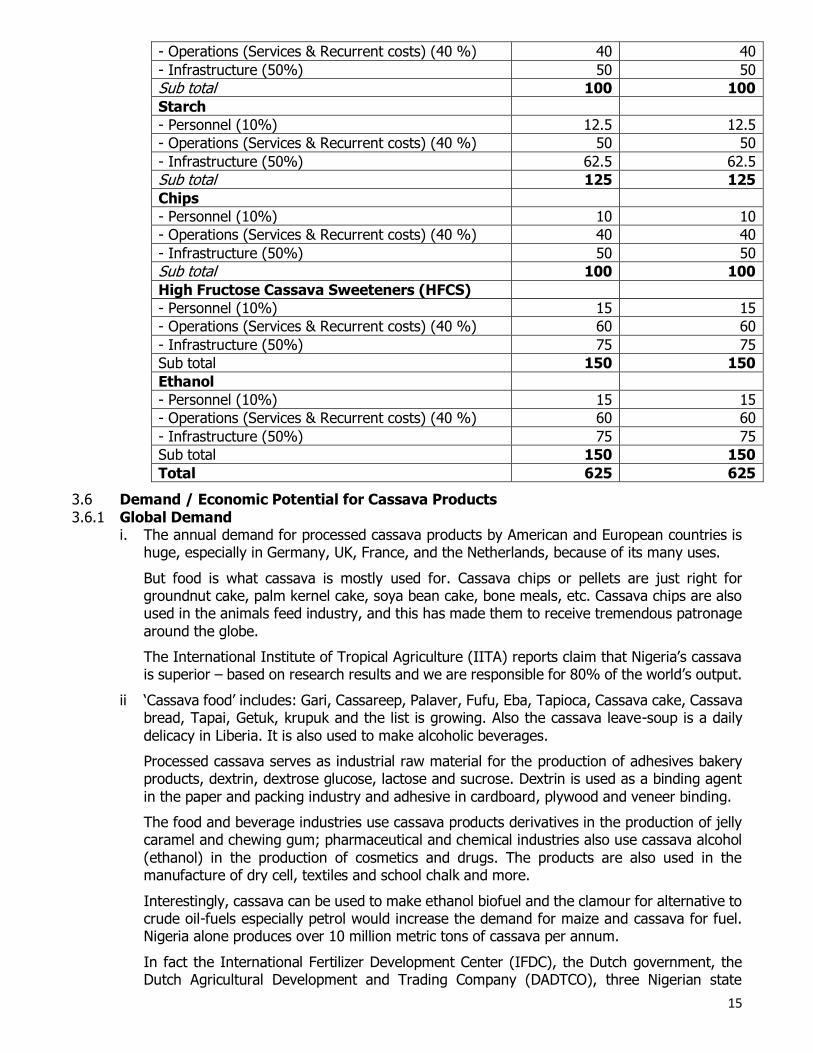

ii. Estimated Costs – Sustainability Issues The proposal is for individual African governments of the top 20 producing countries to commit

at least US$625 million over 5 years and US$625 million for outscaling in the subsequent 5 years to fully implement the specified value chains. This can be done through PPP arrangements.

Table IV:- Estimated Costs

Value Chain Indicative funding (million US$)

2016-2020 2020-2024

High Quality Cassava Flour (HQCF)

- Personnel (10%) 10 10

15

- Operations (Services & Recurrent costs) (40 %) 40 40

- Infrastructure (50%) 50 50

Sub total 100 100

Starch

- Personnel (10%) 12.5 12.5

- Operations (Services & Recurrent costs) (40 %) 50 50

- Infrastructure (50%) 62.5 62.5

Sub total 125 125

Chips

- Personnel (10%) 10 10

- Operations (Services & Recurrent costs) (40 %) 40 40

- Infrastructure (50%) 50 50

Sub total 100 100

High Fructose Cassava Sweeteners (HFCS)

- Personnel (10%) 15 15

- Operations (Services & Recurrent costs) (40 %) 60 60

- Infrastructure (50%) 75 75

Sub total 150 150

Ethanol

- Personnel (10%) 15 15

- Operations (Services & Recurrent costs) (40 %) 60 60

- Infrastructure (50%) 75 75

Sub total 150 150

Total 625 625

3.6 Demand / Economic Potential for Cassava Products

3.6.1 Global Demand i. The annual demand for processed cassava products by American and European countries is

huge, especially in Germany, UK, France, and the Netherlands, because of its many uses.

But food is what cassava is mostly used for. Cassava chips or pellets are just right for groundnut cake, palm kernel cake, soya bean cake, bone meals, etc. Cassava chips are also used in the animals feed industry, and this has made them to receive tremendous patronage

around the globe.

The International Institute of Tropical Agriculture (IITA) reports claim that Nigeria’s cassava is superior – based on research results and we are responsible for 80% of the world’s output.

ii ‘Cassava food’ includes: Gari, Cassareep, Palaver, Fufu, Eba, Tapioca, Cassava cake, Cassava bread, Tapai, Getuk, krupuk and the list is growing. Also the cassava leave-soup is a daily

delicacy in Liberia. It is also used to make alcoholic beverages.

Processed cassava serves as industrial raw material for the production of adhesives bakery products, dextrin, dextrose glucose, lactose and sucrose. Dextrin is used as a binding agent

in the paper and packing industry and adhesive in cardboard, plywood and veneer binding.

The food and beverage industries use cassava products derivatives in the production of jelly caramel and chewing gum; pharmaceutical and chemical industries also use cassava alcohol

(ethanol) in the production of cosmetics and drugs. The products are also used in the manufacture of dry cell, textiles and school chalk and more.

Interestingly, cassava can be used to make ethanol biofuel and the clamour for alternative to crude oil-fuels especially petrol would increase the demand for maize and cassava for fuel. Nigeria alone produces over 10 million metric tons of cassava per annum.

In fact the International Fertilizer Development Center (IFDC), the Dutch government, the Dutch Agricultural Development and Trading Company (DADTCO), three Nigerian state

16

governments: Rivers, Taraba and Osun, and a non-governmental organization,

Communicating For Change (CFC) have begun the ‘Cassava Revolution’.

iii. More companies are going into the processing of Garri. Local makers predominantly produced it back in the day. Things have changed now and farmers are very delighted to sell off

hundreds of tons of the cassava roots in one transaction to a company.

In April 2005 Nigeria began exporting cassava chips to the People's Republic of China under the Presidential Initiative on cassava. The first export was 40 metric tonnes of cassava chips

in two batches of 20 metric tonnes.

iv. HarvestPlus (2015) is at this point striving to achieve its goal of having more than 150,000

Nigerian households eating vitamin A fortified yellow cassava by the year 2014. HarvestPlus, an international agricultural organisation, is partnering with the IITA which is leading a global effort to breed and disseminate micro-nutrient-rich staple food crops to reduce hunger in

malnourished populations. This means that more of the Garri consumed in the country would be processed by cassava processing companies.

In June 2011 Roberts Ungwaga Orya, Managing Director/Chief Executive Officer of the Nigeria

Export-Import Bank said that the bank had “provided funding windows of N500 million” for the export of cassava and provided about N1.1 billion to five companies for value added processing of cassava to flour, chips and glucose syrup.

3.6.2 Regional Market There are export opportunities for Nigerian cassava products (e.g. gari) from and to countries in the West African sub-region (such as Niger and Mali). In these cases, Nigerian cassava products

will compete with cassava products from neighboring countries. (Ghana and Benin). Coastal West African (Cote d’Ivoire, Ghana, Togo, Benin) countries are both competitors and the potential markets for Nigerian products. The determining factor is the price of the raw material.

There are some indications that prices in Ghana are similar to those in Nigeria, while the prices of cassava products in the Republic of Benin are generally lower. The latter observation explains the periodic presence of Benin gari on the Lagos, Nigeria market. Gari prices fluctuate in all West

African coastal countries, and not necessarily at the same time. Recent market surveys by the West Africa Trade Network (www.wa-agritrade.net) and MISTOWA (www.mistowa.org) confirm that Nigeria cassava products do not yet enjoy a significant price advantage over those in

competing West Africa countries. Nevertheless, a cross-border trade study (Ezedinma et al, 2005d) in Northern Nigeria showed a substantial cassava export to Niger (mostly gari, but also chips), especially during the “hungry season” (February through April) when the new grain crops

in Niger are not yet harvested (see: www.cassavabiz.org).

3.6.3 Economic Potentials / Domestic Demand i. As the main food staple for urban and rural people in the south and the central States of the

country, Cassava already makes a major contribution to the Nigerian economy. Additionally,

the market for industrially processed cassava is growing - Estimates indicate the potential short-term demand for industrial cassava at about 8.8 million MT of fresh cassava annually. This domestic shortfall in demand provides Nigerian cassava farmers an increase in

demand of more than 20%. Assuming a well-managed cassava farm that yields 20 MT/hectare, this untapped domestic demand implies an increase in acreage of over 440,000 hectares.

Sector

Current Domestic Demand

Substitution

Potentials

(MT/Product)

Fresh Root

Starch 230,000 MT 50 % 115,000 MT 1,150,000 MT

Flour 330,000 MT 10 % 330,000 MT 1,320,000 MT

17

Ethanol E10 1.1 billion L 50 % 550,000 MT 4,400,000 MT

Ethanol Industrial /Beverage

160,000,000 L 10.0 % 160,000 MT 1.040,000 MT

Animal Feed 1,200,000 MT 20 % 240,000 MT 960,000 MT

Total required 8,870,000 MT

Table V: Potential Market for Cassava-derived Products in Nigeria – ATA (2015)

From the domestic demand analysis presented in Tables V and VI, the necessary economic inputs can be estimated.

Based on the capacity figures (small to medium scale), and the cost estimates, the number of processing plants, and the associated investments can also be estimated. The analysis shows that the domestic demand has the potential to motivate investments in nearly 500

small to medium scale plants in the foreseeable future, with at least 100 such plants in the short run – If supporting policy measures are in place.

ii. Assuming an average investment of about N20 million per plant, the associated investment

would amount to about N10 billion in the foreseeable future (or N2 billion in the short run). This value of investment excludes the associated investments at the farm level and the multiplier effects that would be created through other activities and services along the value

chain.

Sector

Fresh Root

(Million)

Plants

Short Term

1 -2 yrs

Medium Term

2 -5 yrs

Long Term

5 yrs

Starch 0.6 MT 17 plants (24T/daily) 20% 40% 40%

Flour 1.2 MT Turnkey: 50 plants Batch: 100 plants

20% 60%

40% 40%

40%

Ethanol E10 3.6 MT 214 plants 100%

Ethanol Industrial /Beverage

1.0 MT 60 plants 60% 40%

Animal Feed 10 MT 52 plant (10%

cassava)

33% 33% 34%

Total required 493 126 108 259

Table VI: Expected Fresh Roots Demands and Processing Plants to be established – (ATA 2015)

3.7 Getting Involved 3.7.1 To become an exporter and investor of cassava and cassava products information is key. The

Nigerian Export Promotion Council (NEPC) can provide this information while consultations from practitioners in the sector will go a long way to educate potential investors. However, prospective

investors need to identify which of the cassava products they intend to focus on.

The opportunities that cassava based businesses have are vast but Nigeria has not harnessed it

even though stakeholders have been creating the awareness in their own capacities for several years.

The farmers still battle with poor technology, poor transportation, poor infrastructure and pests

(cassava mites).

3.7.2 The information on how to get started is available (even on the internet) and this includes:-

- Addresses of local makers, - Fabricators of the cassava processing machines, information on the - Cassava production technology, - Appropriate packaging to meet the export standard,

- Processing cassava and its derivatives, - Export procedures, documentation and marketing in the international market,

18

- Procedures for collecting 30% rebate on export of agricultural products, and

- Contact data of foreign companies seeking to buy cassava products.

As for the cassava root itself, an investor would also need to know:- - How to keep their tubers fresh for months,

- Which varieties of cassava are of the highest/most sort after quality for the product the investor is focusing on as well as

- High yielding varieties, and details on

- How to order for supplies of cassava chips.

3.7.3 This information is also available online and on request from the various stakeholders, including their respective unions. Information on how to actually process cassava is also available and

this includes the making of cassava flour which food processing companies purchase more than 1,000 tonnes daily. One could also seek information on funding, as cassava is one of the ‘new brides’ of the ministry of agriculture.

Once an investor has decided what point of the equation he or she would want to come in, the next stage is to learn the processes and the details. The information is available on request.

Meeting with some of the players in the ‘line of choice’ is a very good idea; prospective suppliers of your raw materials and consumers of your products.

Then the issue of funding comes up. It is believed that it is easier to get funding with the help of

any of the government schemes for cassava processing so as to enjoy the incentives. An investor can also team up with existing companies and thus ride on their backs to make huge profits.

3.8 Governments Latest Efforts

3.8.1 In the current Government’s “The Agriculture Promotion Policy” (2016-2020) launched recently, the Government has enunciated the under listed policy framework:- i. Building on the successes and lessons from the ATA, the vision of the Buhari Administration

for Agriculture is to work with key stakeholders to Agriculture Transformation Agenda build an agribusiness economy capable of delivering sustained prosperity by meeting domestic food security goals, generating exports, and supporting sustainable income and job growth. In

this regard, a number of specific objectives for the period 2016 – 2020 emerge:

Grow the integrated agriculture sector at 1x to 2x the average Nigerian GDP for 2016 – 2020; sector’s historical growth was between 3% - 6% per annum in 2011 – 2015, hence

the need to raise performance. Assuming GDP growth of 6% in 2017, agriculture would aim to achieve 6% - 12% , allowing agricultural household income to double in 6–12 years, holding all else equal

Agriculture’s Share of GDP: 23% (Q1 2016)

Agriculture’s Share of the Labor Force: 70% Agricultural Activity Mix: Crop Production: 85%; Livestock and other non-crop: 15%

Integrate agricultural commodity value chains into the broader supply chain of Nigerian

and global industry, driving job growth, increasing the contribution of agriculture to wealth creation, and enhancing the capacity of the country to earn foreign exchange from agricultural exports;

Agriculture’s Share of Non-Oil Exports Earnings: 75% Promote the responsible use of land, water and other natural resources to create a vibrant

agricultural sector offering employment and livelihood for a growing population; Facilitate the government’s capacity to meet its obligations to Nigerians on food security,

food safety and quality nutrition

Agriculture’s Share of Federal Budget: ~2.0% Create a mechanism for improved governance of agriculture by the supervising

institutions, and improving quality of engagement between the Federal and State

Governments.

19

ii. Unlocking Nigeria’s full agricultural potential requires that Nigeria solve the underlying

challenges in its agricultural system, which includes the following:- Policy Framework: Nigeria suffers from policy instability driven by high rate of turnover of

programmes and personnel, which in turn has made the application of policy instruments

unstable. The outcome is an uneven development pathway for agriculture; lack of policy accountability, transparency and due process of law, relating to willful violation of the constitution and subsidiary legislations governing the agriculture sector. That in turn has

made the business environment unpredictable and discourages investors. To address this challenge, Nigeria needs to create a policy structure that matches evidence-driven coordination among decision-making authorities with common and public goals for an agricultural transformation of the country. Building that evidence base requires that

Nigeria adopt a consistent fact base to drive decision making, as well as build on prior successes e.g. the Jonathan Administration’s pioneering Agricultural Transformation Agenda (ATA).

Political Commitment: This pertains to the non-implementation of international protocols or conventions agreed to with other members of the comity of nations. For example, Nigeria has failed to achieve the targets in the Maputo Declaration that prescribes a

minimum of 10% budgetary allocation to the agricultural sector. Political commitment at both the Federal and State levels will be required to enforce reforms.

Agricultural Technology: Persistent shortcomings of the National Agricultural Research

System (NARS) to generate and commercialize new agricultural technologies that meet local market needs. NARS’s challenges have been relatively severe particularly around improved varieties of seed or other planting materials and breeds of livestock and aquatic

species. The failure to also deliver already proven technologies available on the shelf to farmers’ fields where they are needed is a challenge. Addressing these will require better coordination among extension delivery system, the national agricultural research system,

as well as public and private sector suppliers of agricultural inputs. Infrastructure Deficit: Nigeria’s agricultural sector suffers from an infrastructure challenge.

Infrastructure such as motor roads, railroads or irrigation dams are either insufficient, or

when available, not cost competitive. They are thus unable to operate to support scale-driven agriculture. That imposes an added cost (up to 50% - 100%) on the delivered price of agricultural produce in Nigeria, making it uncompetitive compared to global peers.

In order to boost farm productivity, raise the level of marketable surplus and expand value chain participants’ access to low cost infrastructure, Nigeria will need to rethink the business and operating model for agricultural infrastructure.

Finance and Risk Management: Nigeria’s agriculture sector continues to have poor access to financial services that enable farmers and other agricultural producers to adopt new technologies, improve market linkages, and increase their resilience to economic shocks. Poor access to financial services that enable input suppliers, processors, traders and

others in agribusiness to address liquidity and encourage targeted private sector engagement in agriculture remains a challenge. Lending rates still routinely range from 10% to 30% subject to whether the borrower is considered prime, has access to low cost,

government-provided financing (BoA, CBN, BOI), or is offered a NIRSAL Plc. -financed interest rate subsidy and credit guarantee. To improve financing options and de-risk value chains further, Nigeria will need to intensify innovation in financing ecosystems.

Institutional Reform and Realignment: Today, many federal and state agricultural institutions only exist on paper. In fact, the system even ignores local government areas which is actually where a majority of activity takes place. There is a need to streamline,

clarify mandates and ensure continued accountability for results. Unless these issues are tackled, Nigeria will continue to struggle with the capacity of its agricultural institutions to deliver on their public mandates. A turnaround will mean, for example, adding more

resources such as adding up to 15,000 extension workers, setting up more operational

20

coordination mechanisms between the Federal Government and States in between the

National Council of Agriculture, and linking rewards to performance.

iii. In addressing these constraints, the government will apply prudent, market based policy measures to grow the sector, with a clear recognition that widespread poverty

reduction through the transformation of the agriculture sector is integral to the country’s long run economic growth trajectory and prosperity. Accordingly, this policy statement is anchored on three main pillars in line with the constitutional provision for

the role of Federal Government in agricultural development:- Promotion of agricultural investment; Financing agricultural development programmes and

Research for agricultural innovation and productivity.

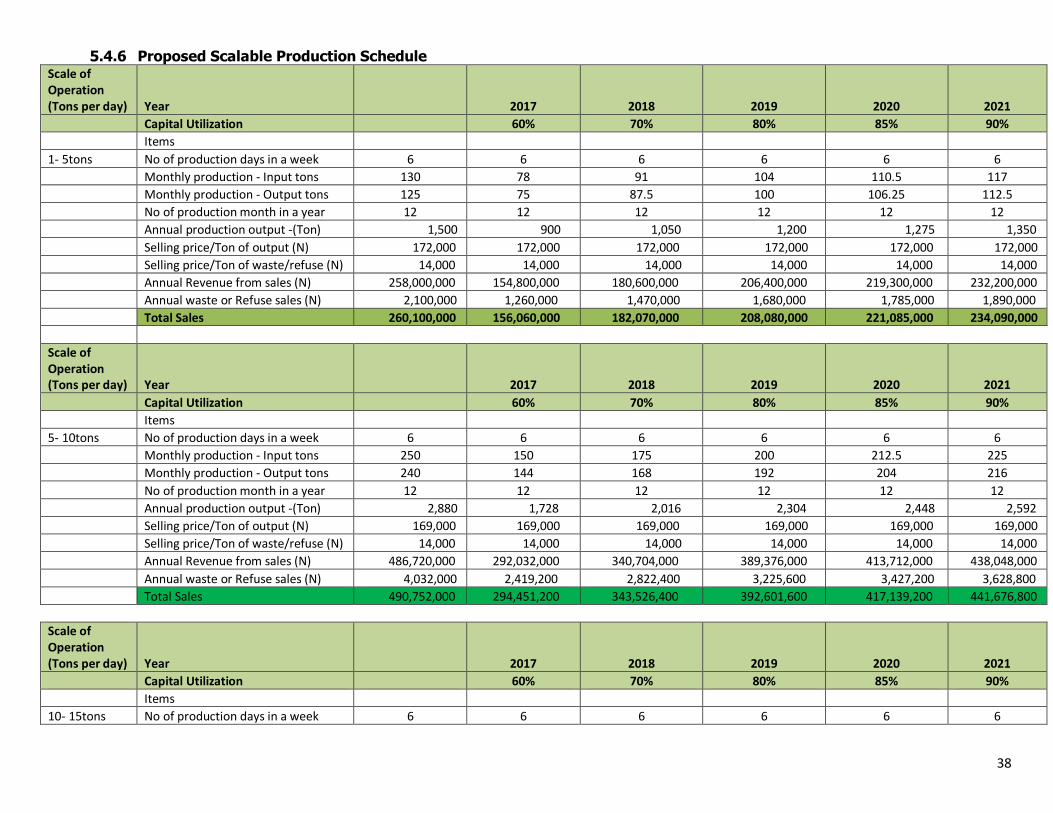

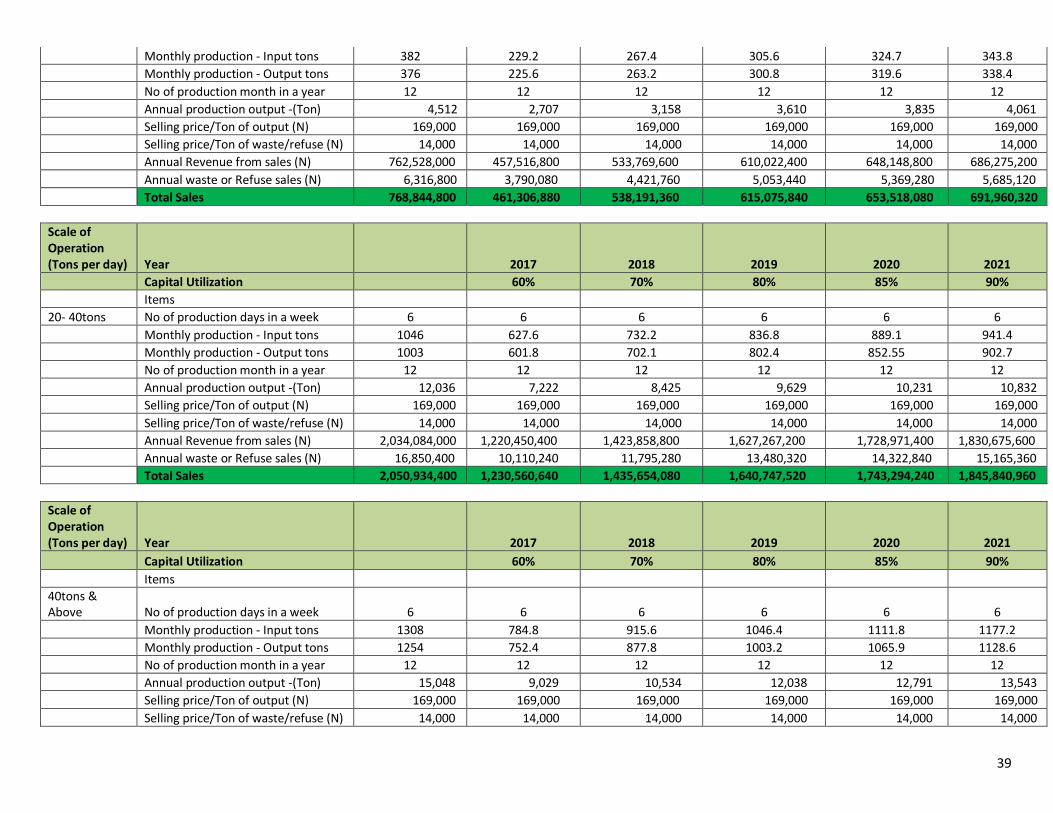

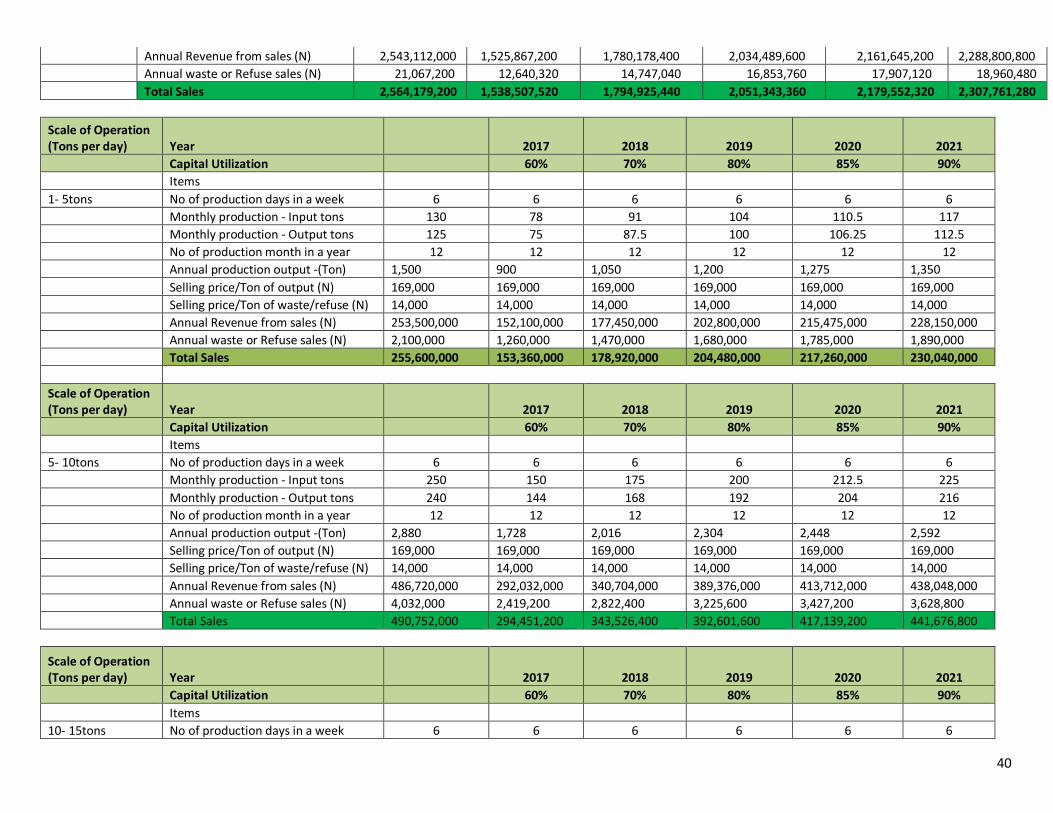

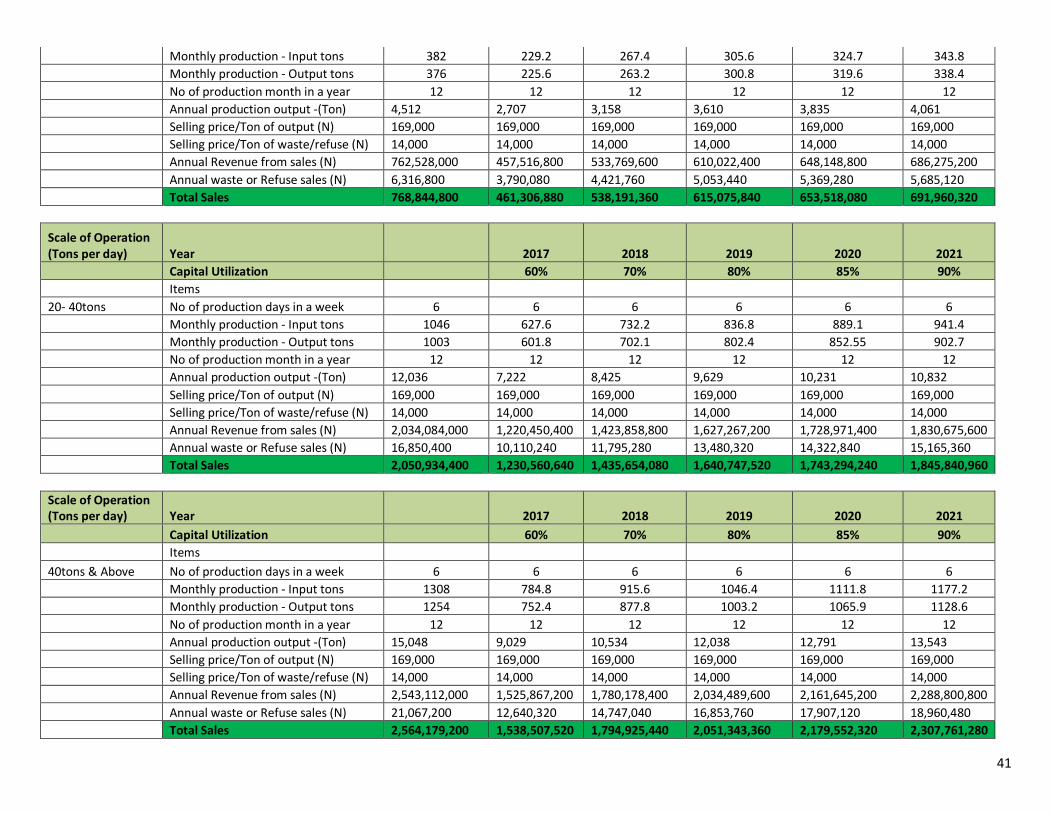

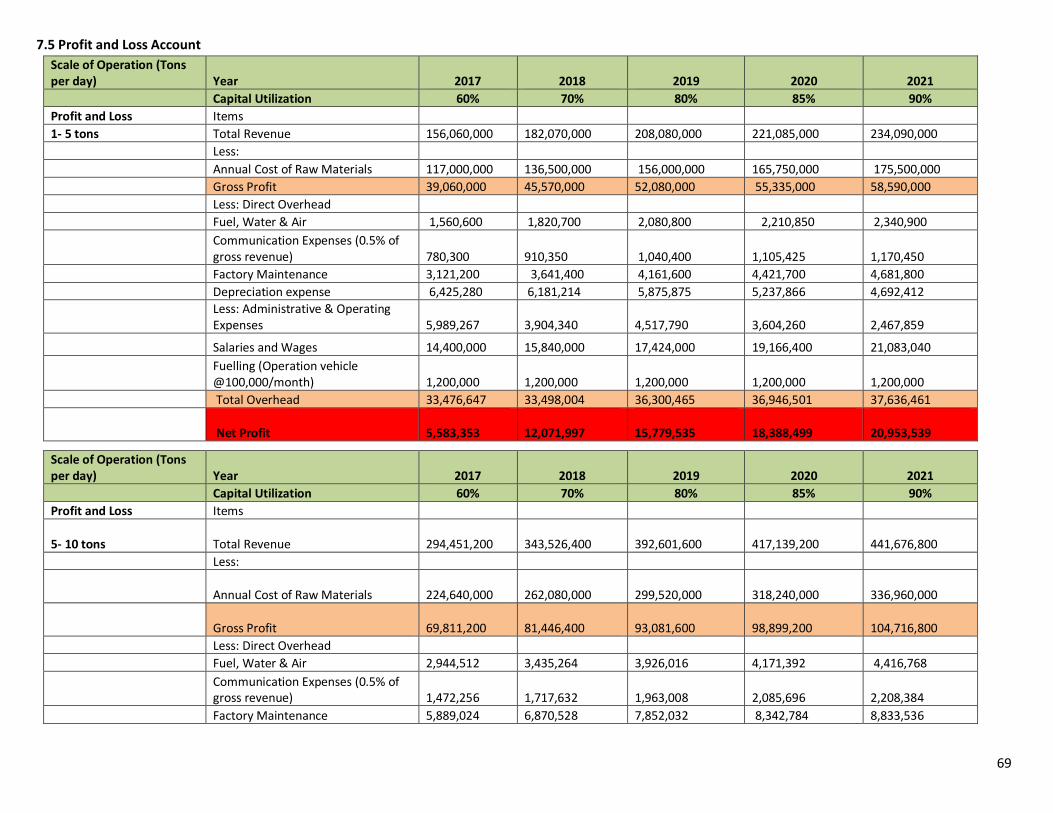

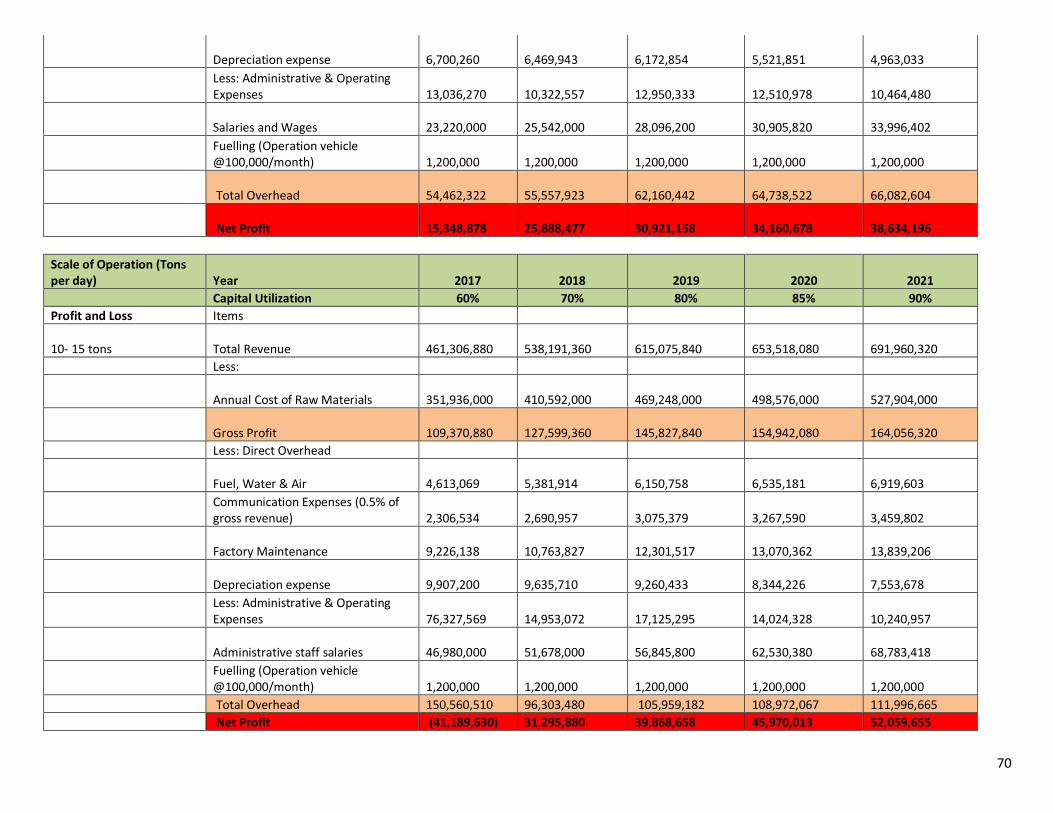

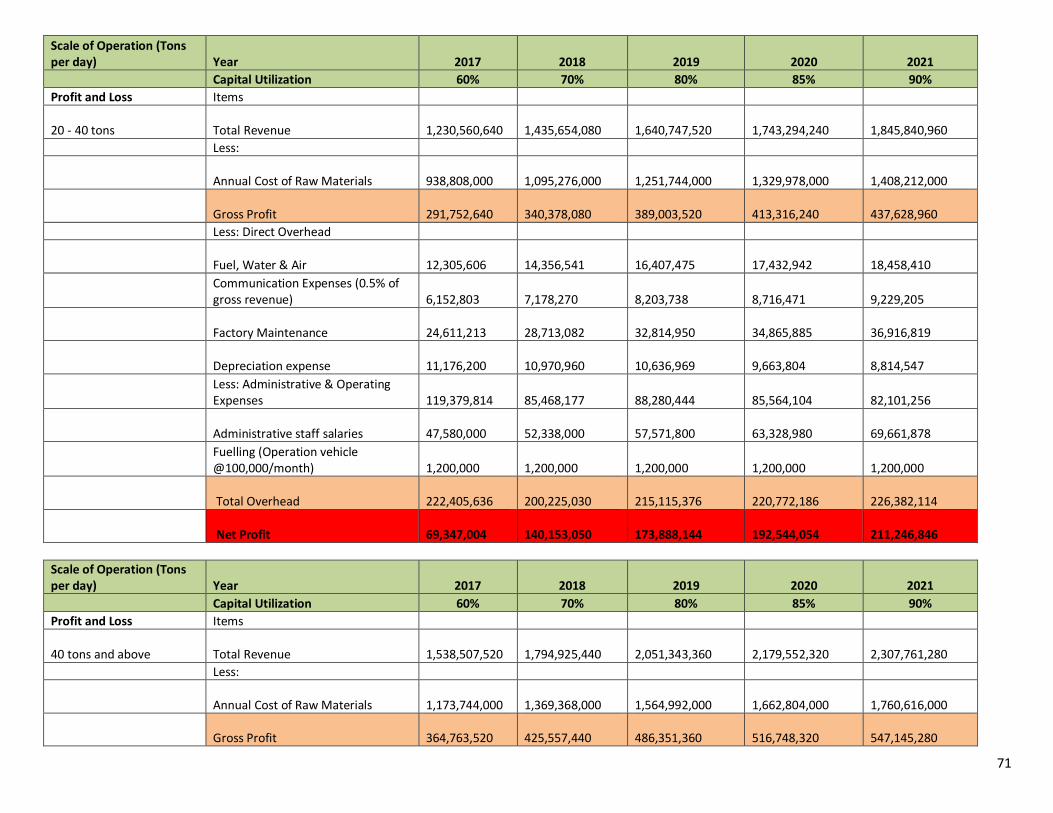

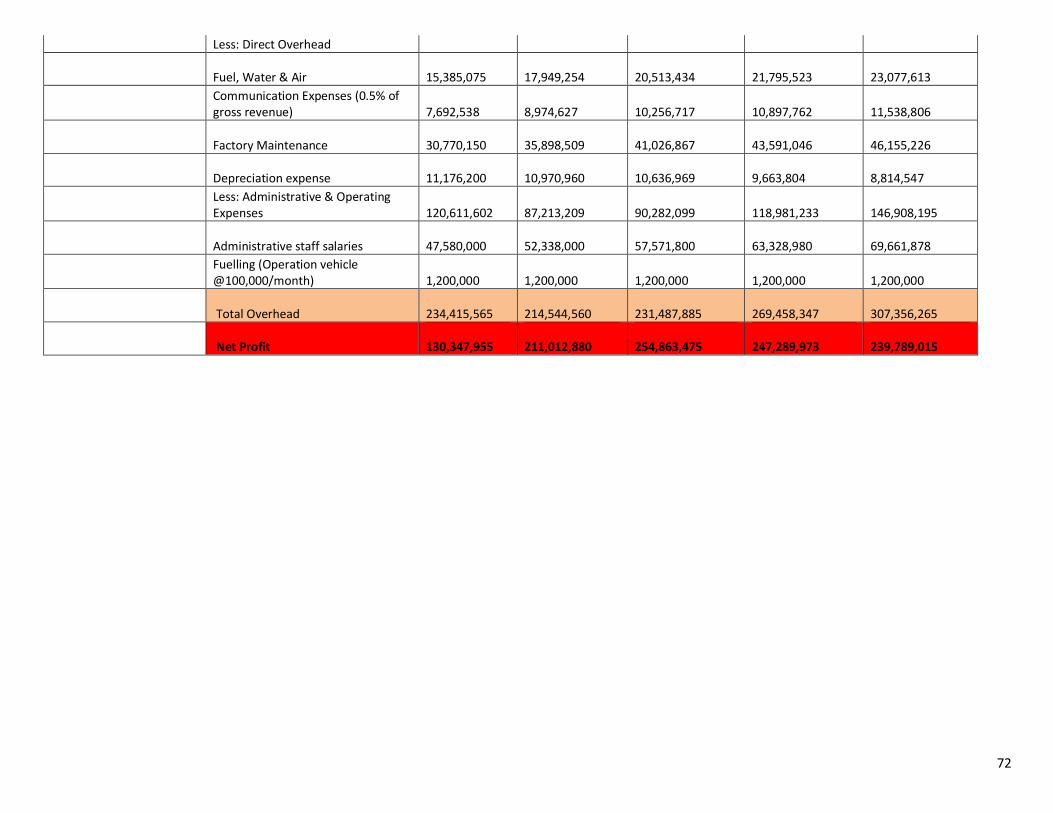

One of the most important by products of Cassava – Starch – Industry & Food Grade is the object of this study.

21

CASSAVA STARCH INDUSTRY

Problems and Prospects

22

4. CASSAVA STARCH INDUSTRY – Problems & Prospects

4.1 The Product Starch is a soft, white, tasteless powder that is insoluble in cold water, alcohol or other solvents. Starch can be cassava based but also cereal based Starch. Over 90% of Starch produced in

Nigeria have a production capacity of less than 10tons per day.

Starch uses are varied and are diversifying further with continued global economic development. Starch is produced from local production of grain or root crop. Starches from different raw

materials i.e. maize or cassava can be substitutable in end-use.

4.2 Types of Starches 4.2.1 Starch can be classified into two types: native and modified. Native Starches are produced

through the separation of naturally occurring Starch from either grain or root crops, such as cassava, maize, and sweet potato, and can be used directly in producing certain foods, such as noodles. The raw Starches produced still retain the original structure and characteristics and are

called “native Starches”. Native Starch is the basic Starch product that is marketed in the dry powder form under different grades for food, and as pharmaceutical, human, and industrial raw material. Native Starch has different functional properties depending on the crop source, and

specific types of Starch are preferred for certain applications. Native Starch can be considered a primary resource that can be processed into a range of Starch products.

Native Starches have limited usage, mainly in the food industry, because they lack certain desired

functional properties. The native Starch granules hydrate easily when heated in water, they swell and gelatinize; the viscosity increases to a peak value, followed by a rapid decrease, yielding weak-boiled, stringy, and cohesive pastes of poor stability and poor tolerance to acidity, with low

resistance to shear pressure, as commonly employed in modern food processing. However, food, metallurgic, mining, fermentation, construction, cosmetics, pharmaceutical, paper and cardboard, and textiles industries among others use native Starch in its traditional form.

4.2.2 Modified Starches For those characteristics, which are unattainable with native Starch, modified Starch can be used

for other industrial applications through a series of techniques, chemical, physical, and enzymatic modification. Thus, modified Starch is native Starch that has been changed in its physical and/or chemical properties.

Modifications may involve altering the form of the granule or changing the shape and composition of the constituent amylose and amylopectin molecules. Modifications are therefore carried out on

the native Starch to confer it with properties needed for specific uses. Some of these modified Starches, their methods of modification and desirable properties are shown in Table 6. When a Starch is modified chemically or physically, the properties of the native Starch is altered. Various

modifications give the Starch properties that make it useful in many industries such as food, pharmaceutical, textile, petroleum, and paper pulp industries.

The different ways of modifying native Starch consist in altering one or more of the following

properties: paste temperature, solids/viscosity ratio, Starch paste resistance to reduction of viscosity by acids, heat and or mechanical agitation (shear), retro gradation tendencies, ionic and hydrophilic nature.

Modifying Starch is important to provide the following properties: thickening, gelatinization, adhesiveness and/or film-formation, to improve water retention, enhance palatability and sheen and to remove or add opacity.

The reasons why native Starch is modified are: To modify cooking characteristics (gelatinization).

To reduce retro gradation. To reduce paste’s tendency to gelatinize. To increase paste’s stability when cooled or frozen. To increase transparency of pastes and gels.

23

To improve texture of pastes and gels.

To improve adhesiveness between different surfaces, such as in paper applications.

4.2.3 Advantages of Cassava Starch Cassava has many advantages for Starch production.

High level of purity. Excellent thickening characteristics. A neutral (bland) taste.

Desirable textural characteristics. A relatively cheap source of raw material containing a high concentration of Starch (dry-

matter basis) that can equal or surpass the properties offered by other Starches

(maize, wheat, sweet-potato, and rice).

Cassava Starch:-

Is easy to extract using a simple process (when compared to other Starches) that can be

carried out on a small-scale with limited capital. Is often preferred in adhesive production as the adhesives are more viscous, work more

smoothly, and provide stable glues of neutral pH has clear paste.

The development of both the food and non-food uses of cassava Starch has made much progress and continues to have a bright future. Both old and important new

products, such as modified Starches, Starch sugars, Starch-based plastics and fuel alcohol, are reviewed briefly.

4.2.4 Cassava Starch is an important domestic and industrial raw material used in the manufacture of

various products including food, adhesives, thickening agents, paper, and pharmaceuticals. It has many remarkable characteristics including high paste viscosity, high paste clarity and high freeze-thaw stability, which are advantageous to many industries.

4.3 Cassava Starch – Global and Nigeria Trends 4.3.1 The world Starch production is about 60 million tonnes and its consumption trend is expected to

be 70 million tonnes by 2012 (Vilpoux, 2005). The largest producer is United States with 25.2

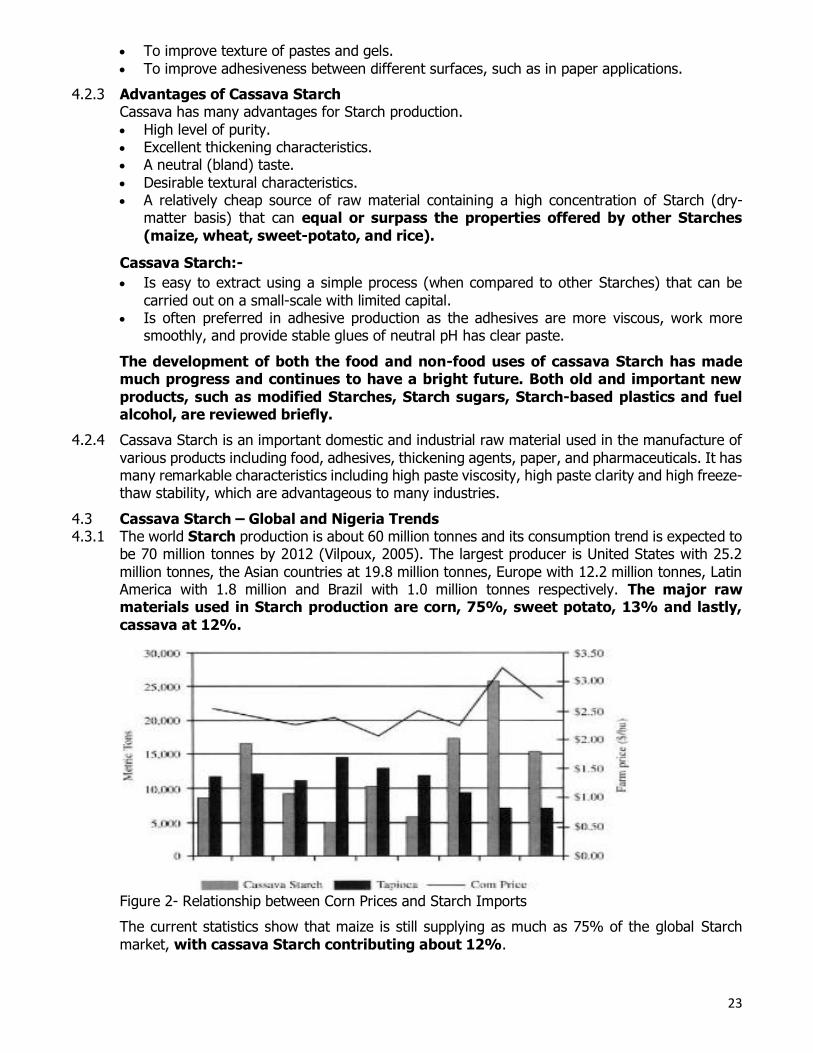

million tonnes, the Asian countries at 19.8 million tonnes, Europe with 12.2 million tonnes, Latin America with 1.8 million and Brazil with 1.0 million tonnes respectively. The major raw materials used in Starch production are corn, 75%, sweet potato, 13% and lastly,

cassava at 12%.

Figure 2- Relationship between Corn Prices and Starch Imports

The current statistics show that maize is still supplying as much as 75% of the global Starch

market, with cassava Starch contributing about 12%.

24

4.3.2 On the international market, Cassava Starch is able to compete against corn, wheat and potatoes

Starches. Cassava Starch is especially competitive outside the two main markets, US and EU (i.e. in South East Asia). The overall world demand for all Starch products grows at an annual rate of 4%. It is expected that this significant growth in demand will continue in the

next decade.

4.3.3 A high level of protection characterizes the Starch market, as many users protect their local Starch industries. Tariffs on Cassava Starch in the main importer countries range from 0%

in Canada, Malaysia, Indonesia and the United States to 480% in the Republic of Korea. In the main markets, Starch is imported under preferential access conditions. Japan for instance, has established an overall 200,000 tonnes tariff quota on native Starch from maize, potato and

cassava, beginning with a 25% duty and reducing it to 15% in 2000.

4.4 Cassava Starch Industry in Nigeria 4.4.1 In a paper presented by Chief Executive Officer (CEO) of Union Dicon Salt (UDS) Plc Mr. Chuka

Mordi in August 2016, he said inter alia:-

Nigeria’s Cassava Starch industry generates over $240 million about N76.9 billion yearly, 90

per cent of which is from importation. But the industry has the potential to grow as population and income per capita increase.

According to Mordi, Nigeria currently has four major functional Starch processing plants with a

combined capacity of 27,000 tons. He said the Nation’s Annual Starch demand of over 250,000 tons with a market size of $240m is met by importation of corn Starch, and this provides an opportunity for import substitution, which is in line with UDS’s strategy.

UDS Plc is a company operating in the Nigerian consumer goods sector. It has been diversifying into the agro industrial sector, with an initial concentration on Cassava and Starch processing. The firm has already finalized agreement with GEA Westphalia of Germany to build the largest

Industrial Starch processing facility in Nigeria.

Mordi said the potential for Nigeria’s Starch market is huge, as Nigeria is the largest cassava

growing country in the world, with an estimated annual output of 45m tons, which continues to grow annually.

He, however, said over $600m worth of cassava products (flour, Starch, glucose and animal feed)

are imported, largely as a result of uncoordinated harvest and transport of high grade cassava in commercial quantities.

Cassava Starch, a food grade product refined from cassava roots, the major component of the

cassava plant. It has thickening and binding qualities and is used as binder and thickener in convenience foods. But Mordi said Nigeria processes very little of its current output Starch compared with other countries.

According to him, all the major Starch processing factories in Nigeria operate at less than 20 per cent of their installed capacity, producing about 27,000 tons of Starch per annum. The 20 per cent domestic production capacity, he said, fall short of the nation’s current demand for

Starch, put in excess of 250,000 tons per annum.

To meet local supply, the CEO said Starch end-users resort to importation of Starch, which

presents a clear opportunity for investment in Starch processing for import substitution. He said the company’s investment in Cassava processing involved the installation of a 10,000 Metric Tons Per Annum (MT PA) Starch processing plant for the conversion of cassava to Starch.

4.5 Characteristics of the Starch Industry 4.5.1 First, the share of the cassava crop going to Starch is very little (2%) but has been growing over

time. The number of participants involved in Starch production has increased, including both rural

households and large firms. Field survey results show that at least 5% of total cassava production is now used for Starch.

25

4.5.2 Second, many Starch processors cannot buy enough cassava to run at full capacity. In particular,

there is a sizable gap between potential and utilized capacities, a gap that grows with firm size. Capacity utilization for micro firms is 66%, for small firms it is 41%, for medium firms 36%, and for large firms 25%.

The Starch value-chain is characterized by difficulty in securing sufficient fresh roots to run the large mill at full capacity; both NSM and MATNA run at 40 and 60% capacity respectively. Currently, the MATNA mill works a single shift and sources cassava from 1,200 hectares of small

holder farms located 650km from the mill. The plan going forward is to improve this supply by clustering 2,500-3,000 hectares of farms within 300km of the mill for a two shift operation. In the long term, the mill will operate three shifts using fresh roots from 4500-5000 hectares of

cassava of which at least 2/3 is from within 300km. NSM on the other hand has a nucleus farm of 500Ha that meets roughly 20% of its raw material needs. The rest of its raw material comes from white Zimbabwean out grower farmers, some 700 km away in Shonga, Kwara state.

Sourcing cassava from such a long distance adds N7,000 to each ton of fresh cassava roots.

A study of USAID MARKETS revealed commercial Starch processors of Cassava need consistent volumes to be profitable. Solutions include The Cassava Supply Management System

(CSMS), a database for managing supplier relationship, it includes: a system for planning harvest; a record of deliveries for accounting; manages complex supplier network; efficient allocation of transport fleet; Standard Operating Procedures Developed: Harvest, Transport and

Delivery.

4.5.3 Third, high Cassava Root costs contribute to lowering the competitiveness of the industry, particularly of the larger firms. Survey results show that large firms pay the highest prices

for raw materials procured from farmers, where as the smallest firms pay the lowest prices. Moreover, small and medium firms travel shorter distances to procure cassava than do large processors. High costs are also related to the low productivity of cassava farming. Current yields

only average 15tons/ha in Nigeria, where as in China and Thailand yields are nearly double that.

4.5.4 Fourth, most of the Starch firms are micro or small. Micro firms (with a production capacity of

less than one ton per day) comprise almost 50%, with small firms (between 1and 5tons per day) making up about 26%, medium firms (between 5 and 10tons per day) about 24%, and large firms (over 10tons per day) only 10%. The largest enterprise, MSN, has a capacity of 10,000ton/yr

(ATA 2015).

Small firms also have poorer quality equipment. Most small processors manufacture Starch with a bare minimum of equipment, using only graters and pumps in their operations. By contrast,

large firms have access to sedimentation tanks, dryers, and complete Starch systems. The majority of participants (both small and large) in the Starch industry use locally manufactured equipment, which is often of low quality and in appropriate for producing high

quality Starch.

Field Survey indicates small firms-and even some large firms-face credit constraints that make it quite difficult for them to increase the quantity and quality of their equipment. The

survey revealed a higher incidence of borrowing by medium and large processors (68% and 76%, respectively) than micro and small processors (44% and 22%, respectively). While large firms have better access to bank credit, the survey reports a larger gap between obtained credit and

credit requirements for these firms. Problems with securing sufficient collateral and difficulties with banks were stated by firms in the survey as the main reasons for not being able to obtain additional credit.

4.5.5 Fifth, as firm size increases, the capital/labor ratio increases. Nearly all of the firms in the survey are labor-intensive, with capital use increasing only after an enterprise has reached a scale of at least three tons per day. Survey results show that the average value of equipment for micro,

small, and large firms was respectively N1m, N12m, N240m (using the 2017 exchange rate of U.S.$1 to N305.6)

26