1 security analysis financial statements balance sheet

Post on 22-Dec-2015

220 views

TRANSCRIPT

1

Security Analysis

Financial StatementsBalance Sheet

2

Income Statement Revenues -Cost of Goods Gross Income -Operating Expenses Operating Income -Financing Expenses -Taxes Net Income Before Extraordinary Items +/- Extraordinary Profits/(Losses) Preferred Dividends Net Common Income to Shareholders

3

Principles

Accrual Accounting Categorization of Expenses into 1. Operating Expenses 2. Financing Expenses 3. Capital Expenditures

4

Warning Signs EPS Growing Faster than Revenue

Year after Year Frequent Acquisitions or One Time

Charges Rapid Growth in Working Capital Changes in Inventory/Depreciation

Methods Change in Auditors

5

Balance Sheet

What is it and What can Investors Use it For?

6

Statement of Financial Position as of a Specific DateAssets Liabilities and Equity Cash Accounts Payable Accts Receivable Accrued Expenses Inventory Current Debt Prepaid Expenses Taxes Payable Current Assets Current Liabilities

Other Assets Long Term Debt

Fixed Assets Retained Earnings Net Fixed Assets Shareholders Equity

Total Assets Total Liabilities & Equity==================================

7

Uses of the Balance Sheet

Assess Risk

Identify Value

Understand Competitive Advantage

8

Info in the Balance Sheet

Division of Capital Between Senior Obligations and Common Equity

Strength or Weakness of Working Capital Position

Reconciliation of Earnings reported in income statement

9

Info on the Balance Sheet

Data for Analyzing Relationship between Earnings Power and Asset Values. (Fixed/Variable Costs)

Data to Test True Business Success (ROIC)

10

Impact of Debt

Magnifies Returns (Positive AND Negative)

Adds Fixed Costs

Adds Uncertainty

11

How Much Debt is Enough?

Versus Business Model

Versus Peers

Working Capital

12

Historic Value of Book Value Originally Represented Value of

Private Business (Tangible Assets) Today Little Relation to Market

Value Intangibles as Valuable as Plant Useful to Corroborate Income

Statement Still Relevant in Energy, Financials,

Distressed

13

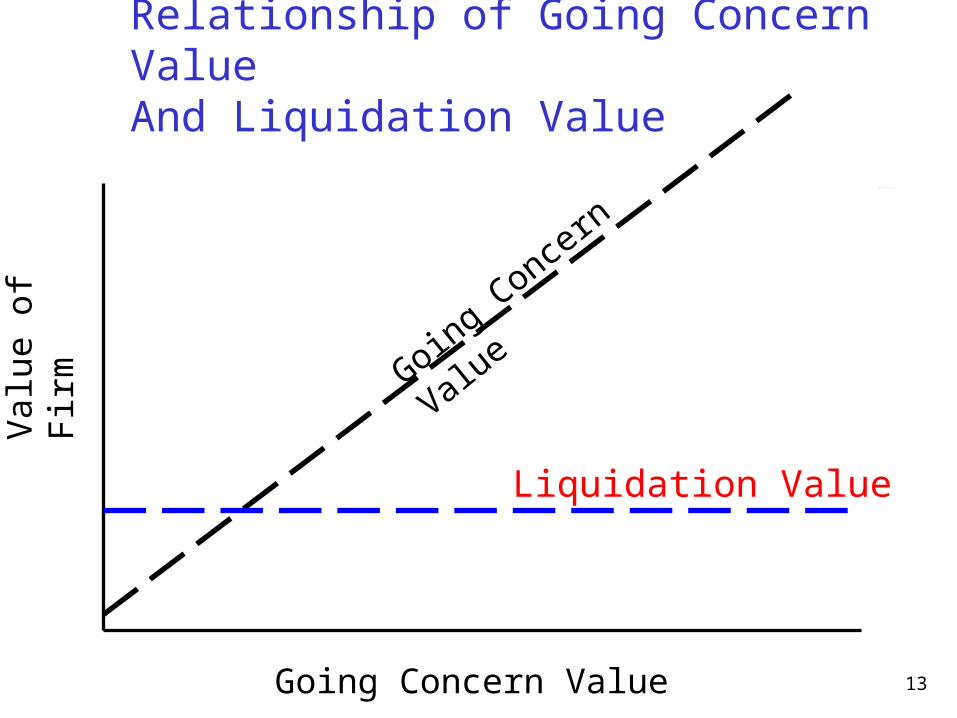

Relationship of Going Concern ValueAnd Liquidation Value

Valu

e o

f Fi

rm

Going Concern Value

Liquidation Value

Going C

once

rn

Value

14

Relationship of Going Concern ValueAnd Liquidation Value

Valu

e o

f Fi

rm

Going Concern Value

Liquidation Value

Going C

once

rn

Value

15

Business Model and Profitability Drive BV Multiples

Price9/7/04

Price to Book Value

Return on Assets

EBAY $89.28 10.18x 8.88%

International Paper

$41.08 2.4x 0.87%

16

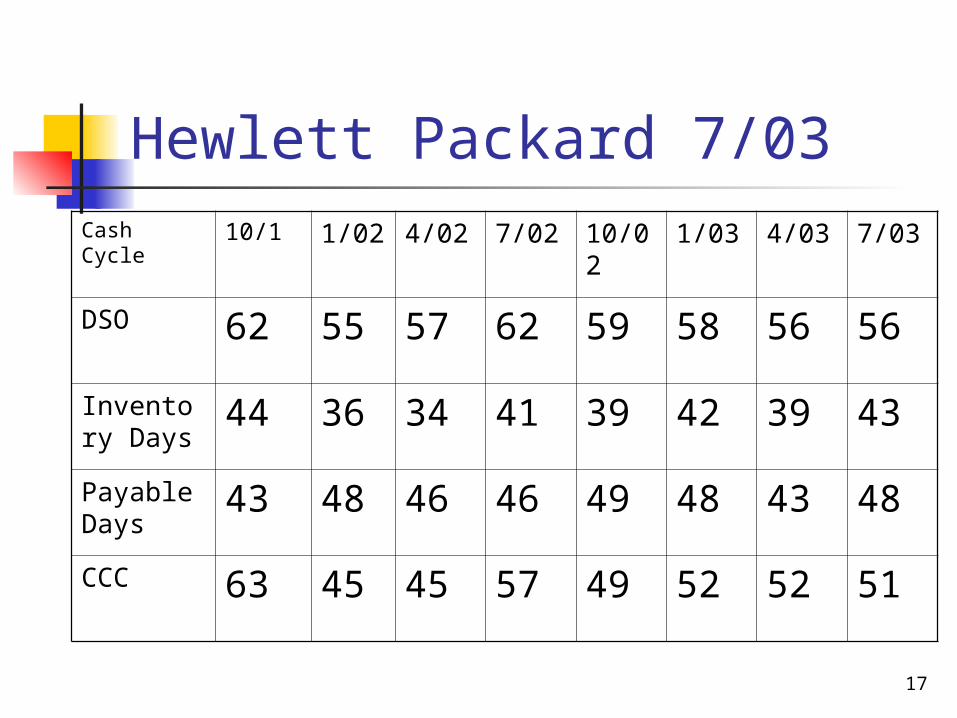

Balance Sheet Can Discern Efficiency Trends

Cash Cycle: Time it Takes to Turn Raw Materials into Cash

Day in Inventory+Days Receivable-Days Payable

Fast is Good!

17

Hewlett Packard 7/03Cash Cycle 10/1 1/02 4/02 7/02 10/0

21/03 4/03 7/03

DSO 62 55 57 62 59 58 56 56

Inventory Days

44 36 34 41 39 42 39 43

Payable Days

43 48 46 46 49 48 43 48

CCC 63 45 45 57 49 52 52 51

18

Dell 7/03Cash Cycle 10/1 1/02 4/02 7/02 10/0

21/03 4/03 7/03

DSO 32 25 26 28 26 24 25 27

Inventory Days

4 4 4 4 4 3 3 4

Payable Days

70 66 68 73 71 68 70 72

CCC (34) (37) (38)

(41)

(41)

(41)

(42)

(41)

19

Relative Profitability Dell/HPQ

Profit metrics

1/02

4/02

7/02 10/02 1/03 4/03

7/03

DellROA%

13 13 13 14 15 15 15

HPQ ROA%

4 3.3 2.4 4.2 4.9 4.9 3.9

DELL ROE%

35 36 39 42 46 48 48

HPQ ROE%

4.7 4.8 4.7 6.5 7.1 8.3 8.8

20

Update on Dell/HPQ

Earnings 3,043 3,497

Interest Exp 0 225

Assets 23,215 76,138

Shareholders’ Equity 6,485 37,564

ROA 13.1% 4.9%

ROE 46.9% 9.3%

Dell 1/05 HPQ 10/04

21

Accounting Ratios/Stock Price: Dell/HPQ

ROE 59.1% 8.08%

P/B 15.53 2.15

“Return on Mkt Cap” 3.81% 3.77%

P/E 26.4 25.5P/B = Price/Equity

ROE = NI/Equity

ROE x 1/(P/B) = return on market cap

= (NI/Equity x (1/(price/equity)Figures are per Yahoo Finance 9-05-05

Dell HPQ

22

Balance Sheet Manipulation

Leases: Operating versus Capital

Pension Assets

Special Purpose entities

23

Ratio Analysis: Combining IS and BS

Liquidity: Current Ratio, Working Capital to Sales Ratio

Asset Management: Inventory Turns, Asset Turns, Days Receivable

Profitability: Gross Margin, Operating Margin, ROA, ROE

Leverage Ratios: Debt to Capitalization

24

Assignment for Tuesday

Calculate Liquidity, Asset, Profitability, and Leverage Ratios for your selected company and its comparable companies over each of the 5 years

LOOK at them. THINK about them Identify likely areas of required

accounting adjustments

25

Ratios Current Ratio= Current Assets/Current Liabilities Working Capital Ratio= Working Capital/Sales Inventory Turns=Cost of Goods Sold/Inventory Asset Turns=Sales/Assets Receivable Days=Receivables/Sales x 365 Return on Assets=Net Income*/Total Assets Return on Equity=Net Inc/Shareholders Equity Return on Sales=Net Inc/Net Sales Gross Margin= (Sales-Cost of Gds Sold)/Sales Operating Margin=Operating Income/Sales Debt/Capital=Long Term Debt/Long Term

Debt+Shrhldrs Equity

*Some add back interest on debt

26

What is in the 10k and What can We Learn?Item 1: Business Model and Strategy Industry Trends/ Comparisons2. Properties: Sources of Capacity and Revenues.

Exposure to currency and variation in cost levels

3. Legal Proceedings: Potential Liquidity issues4. Matters Requiring Shareholder Vote. Potential

material change in business (M&A)5. Stock Performance, Listings, Float, Dividend6. Selected Financial Data: Snapshot of

data deemed important by management. One time items

27

What is in the 10k and What can We Learn?7. Management Discussion. Analysis of past

financial performance and future outlook. Strength and weakness in business operations and funding issues. Supplement to data in notes.

7a. Market Risk: Laundry list of risks and competition

8. Financial Statements and Supplementary Data (notes). Indications for future sustainability and quality of earnings/Profitability

9. Changes and Disagreements w/Accountants. Potential red flags regarding quality of disclosure and financial performance.

28

What is in the 10k and What can We Learn?

10. Directors/Officers and Conflicts11. Executive Compensation12. Ownership of Stock. Executives and

certain beneficial owners13. Related Party Transactions/Conflicts14. Exhibits, Statement Schedules.

More info providing insight (subjective accruals). New contracts. Off balance sheet entities. Changes in Bank covenants.