1 private equity investing mehmet i. budak. 2 what is private equity? investment strategy that...

Post on 22-Dec-2015

234 views

TRANSCRIPT

1

Private Equity InvestingPrivate Equity Investing

Mehmet I. BudakMehmet I. Budak

2

What is Private Equity?What is Private Equity?

Investment strategy that involves the Investment strategy that involves the purchase of equity or equity linked securities purchase of equity or equity linked securities in a companyin a company

Investment is made through a negotiated Investment is made through a negotiated processprocess

By sophisticated investors with financial and By sophisticated investors with financial and operating expertiseoperating expertise

The goal is to acquire undervalued or The goal is to acquire undervalued or “promising” assets and realize profits in 3-5 “promising” assets and realize profits in 3-5 years after the acquisitionyears after the acquisition

Information asymmetry and inefficiencies are Information asymmetry and inefficiencies are important factorsimportant factors

3

Alternative InvestmentsAlternative Investments

4

Private Equity Investment Private Equity Investment StrategiesStrategies

Leveraged BuyoutsLeveraged Buyouts Venture Capital (early vs. late Venture Capital (early vs. late

stage)stage) Special Situations (i.e. distressed)Special Situations (i.e. distressed) MezzanineMezzanine Secondary PurchasesSecondary Purchases Fund of FundsFund of Funds

5

Leveraged BuyoutsLeveraged Buyouts

Established firms with track records, Established firms with track records, stable cash flows and stable growth stable cash flows and stable growth ratesrates

Annual revenues of $25 - $500 millionAnnual revenues of $25 - $500 million Typically in basic retail, transportation Typically in basic retail, transportation

and manufacturing industriesand manufacturing industries Typically have assets to borrow against Typically have assets to borrow against

and access to bank loansand access to bank loans Seek private equity to effect a change Seek private equity to effect a change

in ownership, finance an expansion or in ownership, finance an expansion or restructurerestructure

6

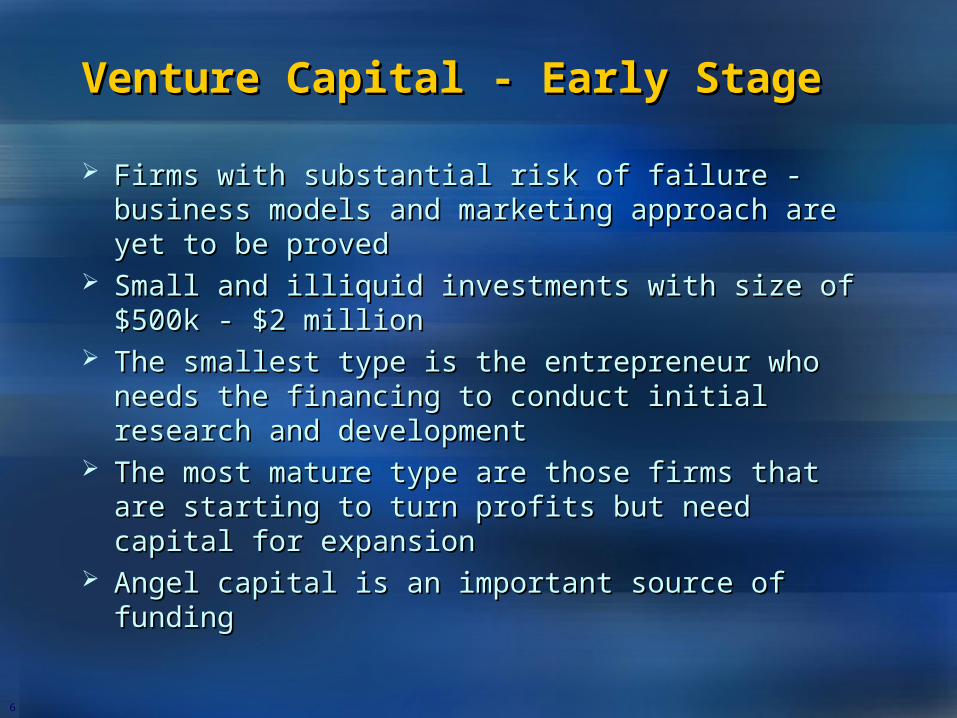

Venture Capital - Early Stage Venture Capital - Early Stage

Firms with substantial risk of failure - business Firms with substantial risk of failure - business models and marketing approach are yet to be models and marketing approach are yet to be provedproved

Small and illiquid investments with size of Small and illiquid investments with size of $500k - $2 million$500k - $2 million

The smallest type is the entrepreneur who The smallest type is the entrepreneur who needs the financing to conduct initial research needs the financing to conduct initial research and developmentand development

The most mature type are those firms that are The most mature type are those firms that are starting to turn profits but need capital for starting to turn profits but need capital for expansionexpansion

Angel capital is an important source of fundingAngel capital is an important source of funding

7

Venture Capital - Late Stage Venture Capital - Late Stage

Firms with more certain business modelsFirms with more certain business models Proven technology and marketProven technology and market Profitable and need expansion capitalProfitable and need expansion capital

General size of $2 - $15 millionGeneral size of $2 - $15 million IPO or Sale expected/feasible in near termIPO or Sale expected/feasible in near term Original investors may achieve some Original investors may achieve some

liquidityliquidity Because the risk is generally lower and Because the risk is generally lower and

the liquidity higher, later-stage the liquidity higher, later-stage investments require lower returns than investments require lower returns than early-stage investmentsearly-stage investments

8

Leveraged Buyouts vs. Venture Leveraged Buyouts vs. Venture CapitalCapital

Buyouts focus on mature companies Buyouts focus on mature companies with stable or sustainable growth profilewith stable or sustainable growth profile

Buyouts rely heavily on debt financing Buyouts rely heavily on debt financing to finance most of the purchase priceto finance most of the purchase price

Venture Capital focus on high growth Venture Capital focus on high growth industries with riskier investment profile industries with riskier investment profile than buyoutsthan buyouts

Venture Capital relies heavily on equity Venture Capital relies heavily on equity financing and has higher return targets financing and has higher return targets than buyoutsthan buyouts

9

Special SituationsSpecial Situations

Investment is supplied by specialized Investment is supplied by specialized Turnaround Funds (TF) for target firms that Turnaround Funds (TF) for target firms that have defaulted on their outstanding loanshave defaulted on their outstanding loans

TFs receive controlling interests, with TFs receive controlling interests, with former owners making up the minority former owners making up the minority interestinterest

TFs renegotiates terms with existing TFs renegotiates terms with existing lenders, offering to restructure or pay off lenders, offering to restructure or pay off loans at a discountloans at a discount

TFs also deliver expertise to find new TFs also deliver expertise to find new markets or partners for the firm’s products, markets or partners for the firm’s products, cut costs, change or improve the current cut costs, change or improve the current managementmanagement

10

Fund of FundsFund of Funds

Investing directly in PE funds can be Investing directly in PE funds can be difficult for individual investors and small difficult for individual investors and small institutionsinstitutions

Relatively high investment minimums may Relatively high investment minimums may disqualify some of the small investorsdisqualify some of the small investors

Information on PE managers is difficult to Information on PE managers is difficult to locatelocate

Gaining access to top PE funds can be Gaining access to top PE funds can be difficult due to high investor demanddifficult due to high investor demand

Fund of Funds co-mingles the investments Fund of Funds co-mingles the investments of small investors into a single pool and of small investors into a single pool and then assembles a portfolio of PE fundsthen assembles a portfolio of PE funds

11

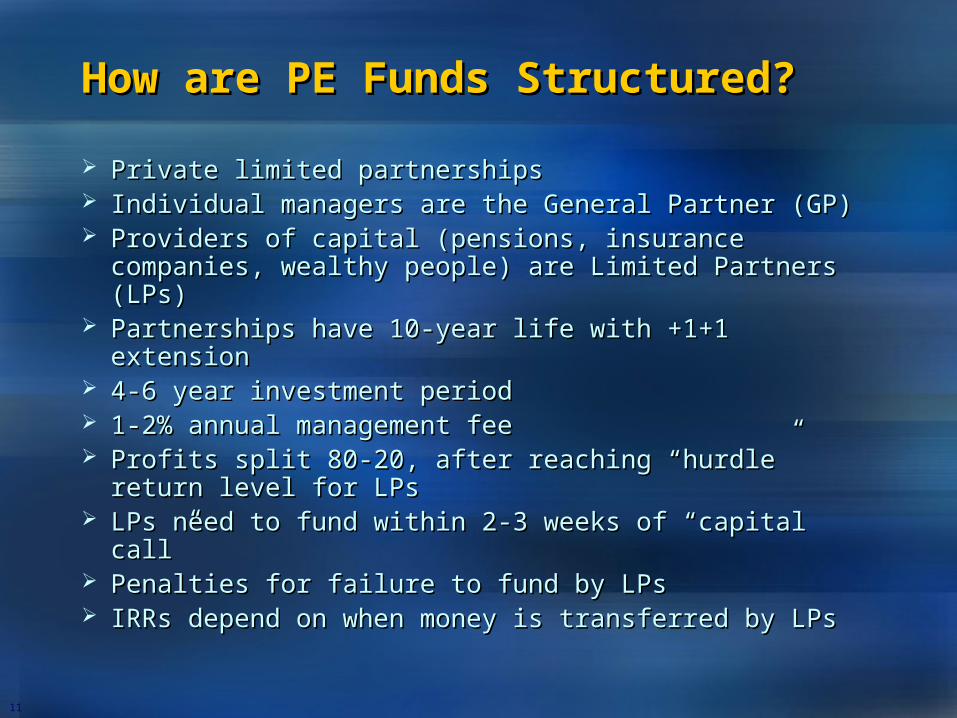

How are PE Funds Structured?How are PE Funds Structured?

Private limited partnershipsPrivate limited partnerships Individual managers are the General Partner (GP)Individual managers are the General Partner (GP) Providers of capital (pensions, insurance Providers of capital (pensions, insurance

companies, wealthy people) are Limited Partners companies, wealthy people) are Limited Partners (LPs)(LPs)

Partnerships have 10-year life with +1+1 extensionPartnerships have 10-year life with +1+1 extension 4-6 year investment period4-6 year investment period 1-2% annual management fee1-2% annual management fee Profits split 80-20, after reaching “hurdle” return Profits split 80-20, after reaching “hurdle” return

level for LPslevel for LPs LPs need to fund within 2-3 weeks of “capital call” LPs need to fund within 2-3 weeks of “capital call” Penalties for failure to fund by LPsPenalties for failure to fund by LPs IRRs depend on when money is transferred by LPsIRRs depend on when money is transferred by LPs

12

General Partner’s Key ActivitiesGeneral Partner’s Key Activities

Selecting investmentsSelecting investments Obtaining access to high quality deal flowObtaining access to high quality deal flow Sorting and evaluating large amount of Sorting and evaluating large amount of

informationinformation Structuring investmentsStructuring investments

Designing transactionsDesigning transactions Monitoring investmentsMonitoring investments

Providing strategic, operational and Providing strategic, operational and financial assistance to portfolio companiesfinancial assistance to portfolio companies

Exiting investmentsExiting investments IPO, Sale or RecapitalizationIPO, Sale or Recapitalization

13

Private Equity Partnerships and Private Equity Partnerships and FundraisingFundraising

14

Private Equity Market - Private Equity Market - InvestorsInvestors

Public and corporate pension funds, Public and corporate pension funds, endowments, foundations, wealthy endowments, foundations, wealthy families, insurance companies, foreign families, insurance companies, foreign investors and othersinvestors and others

Investors expect to receive higher risk-Investors expect to receive higher risk-adjusted returns on private equity than adjusted returns on private equity than other investmentsother investments

Potential benefits of diversificationPotential benefits of diversification Advantage of economies of scope Advantage of economies of scope

between private equity investing and between private equity investing and investors’ other activitiesinvestors’ other activities

15

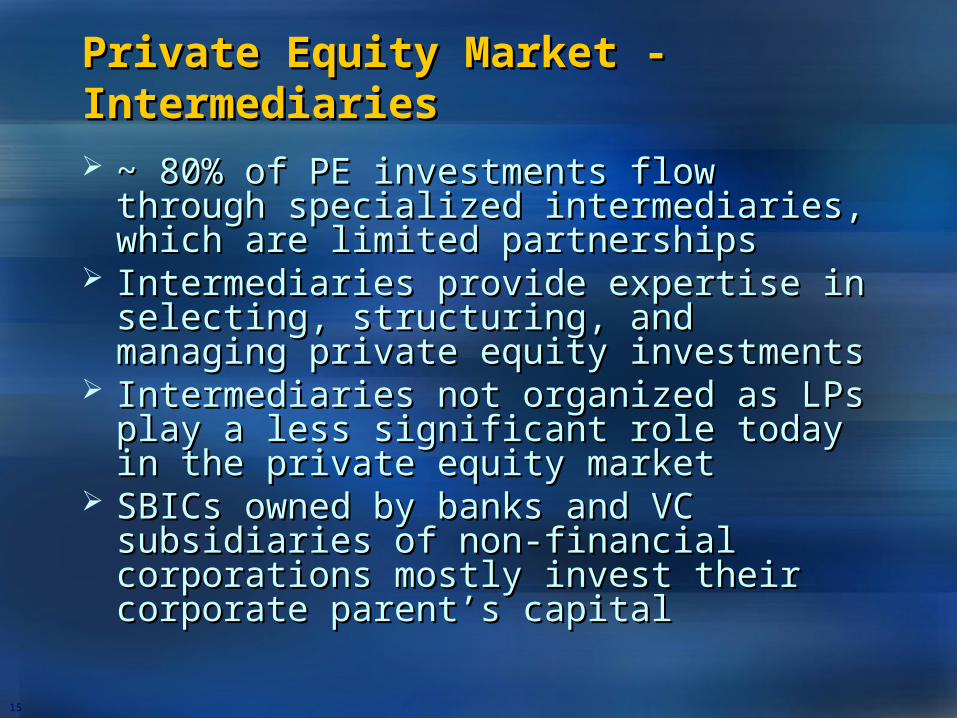

Private Equity Market - Private Equity Market - IntermediariesIntermediaries ~ 80% of PE investments flow through ~ 80% of PE investments flow through

specialized intermediaries, which are specialized intermediaries, which are limited partnershipslimited partnerships

Intermediaries provide expertise in Intermediaries provide expertise in selecting, structuring, and managing selecting, structuring, and managing private equity investmentsprivate equity investments

Intermediaries not organized as LPs Intermediaries not organized as LPs play a less significant role today in the play a less significant role today in the private equity marketprivate equity market

SBICs owned by banks and VC SBICs owned by banks and VC subsidiaries of non-financial subsidiaries of non-financial corporations mostly invest their corporations mostly invest their corporate parent’s capitalcorporate parent’s capital

16

Private Equity Market - IssuersPrivate Equity Market - Issuers

Vary in size and their reasons for raising Vary in size and their reasons for raising capitalcapital Young firms that are developing innovative Young firms that are developing innovative

technologiestechnologies Middle market companies that are stable, Middle market companies that are stable,

profitable and need private equity to expand or profitable and need private equity to expand or restructurerestructure

Going private transactions for public Going private transactions for public companiescompanies

PIPE (Private Investment in Public Equity) PIPE (Private Investment in Public Equity) provides financing without registration provides financing without registration costs/ disclosures associated with public costs/ disclosures associated with public offeringsofferings

17

How are PE Funds Structured?How are PE Funds Structured?

Limited Partners – Investors with moneyLimited Partners – Investors with money Insurance companies, pension funds, banks, Insurance companies, pension funds, banks,

and high net worth individualsand high net worth individuals Investors commit a certain amount to the fundInvestors commit a certain amount to the fund They have no other active role in the fund and They have no other active role in the fund and

no liability beyond their commitmentsno liability beyond their commitments

One General Partner – Managers of moneyOne General Partner – Managers of money Manages the investments via a management Manages the investments via a management

companycompany Receives management fee (typically 2%) on Receives management fee (typically 2%) on

commitmentscommitments Receives “carried interest” in the profitsReceives “carried interest” in the profits

18

How are PE Funds Structured?How are PE Funds Structured?

Contractually fixed lifetime (10-12 years)Contractually fixed lifetime (10-12 years)

Capital is invested during the first 4-6 yearsCapital is invested during the first 4-6 years

Thereafter, investments are managed and Thereafter, investments are managed and liquidatedliquidated

Distributions are made to the limited partners in Distributions are made to the limited partners in the forms of cash or securitiesthe forms of cash or securities

General Partner typically raises a new fund when General Partner typically raises a new fund when the investment phase for the existing fund has the investment phase for the existing fund has been completed (=> 80%)been completed (=> 80%)

Each fund partnership is legally separate and is Each fund partnership is legally separate and is managed independently of other fund partnerships managed independently of other fund partnerships (i.e KKR I vs. KKR II)(i.e KKR I vs. KKR II)

19

Partnership Terms - ExamplePartnership Terms - Example

Target Fund SizeTarget Fund Size $1 billion$1 billion Minimum CommitmentMinimum Commitment $10 $10

millionmillion Gross Target ReturnGross Target Return 25%25% Management FeeManagement Fee 2%2% Carried InterestCarried Interest 80% - 20%80% - 20% Commitment PeriodCommitment Period 5 years5 years Fund TermFund Term 10 years 10 years

+1+1+1+1

20

Relationship Between LPs and Relationship Between LPs and GPsGPs

LPs delegate significant responsibilities to LPs delegate significant responsibilities to GPsGPs

Resolution of potential conflict of Resolution of potential conflict of interests lies in the structure of the interests lies in the structure of the partnership agreementpartnership agreement

Partnerships have finite livesPartnerships have finite lives To remain in business, GPs regularly raise To remain in business, GPs regularly raise

new funds - easier for reputable firms new funds - easier for reputable firms with good recordwith good record

GP compensation is closely linked to the GP compensation is closely linked to the fund returnsfund returns

21

Partnership CovenantsPartnership Covenants

The objective is to limit excessive risk taking by The objective is to limit excessive risk taking by GPsGPs

Covenants usually set limits on the % of the Covenants usually set limits on the % of the partnership’s capital that may be invested in a partnership’s capital that may be invested in a single firmsingle firm

Covenants may preclude investments in publicly Covenants may preclude investments in publicly traded and foreign securities, derivatives and traded and foreign securities, derivatives and other private equity funds, etcother private equity funds, etc

Covenants usually require that cash from sale of Covenants usually require that cash from sale of portfolio assets be immediately distributed to LPsportfolio assets be immediately distributed to LPs

LPs usually limit such deal fees or require that LPs usually limit such deal fees or require that deal fees be offset against management feesdeal fees be offset against management fees

Return hurdle rates for LPsReturn hurdle rates for LPs

22

Evaluating General PartnersEvaluating General Partners

Track record, relevancy of past experienceTrack record, relevancy of past experience Generation of adequate deal flowGeneration of adequate deal flow Sound investment decision-making processesSound investment decision-making processes Ability to achieve successful exits / liquidityAbility to achieve successful exits / liquidity Advantages vs. similarly focused fundsAdvantages vs. similarly focused funds Sufficiency of resourcesSufficiency of resources Meaningful commitment of timeMeaningful commitment of time Cohesiveness and sustainability of teamCohesiveness and sustainability of team Succession planningSuccession planning

23

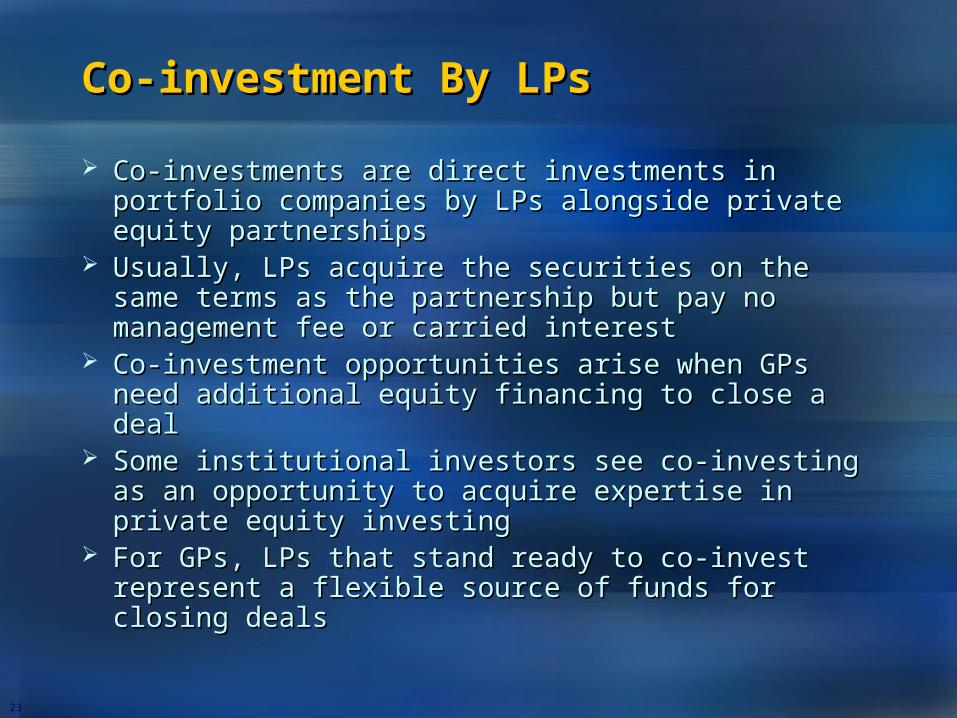

Co-investment By LPsCo-investment By LPs

Co-investments are direct investments in portfolio Co-investments are direct investments in portfolio companies by LPs alongside private equity companies by LPs alongside private equity partnershipspartnerships

Usually, LPs acquire the securities on the same Usually, LPs acquire the securities on the same terms as the partnership but pay no management terms as the partnership but pay no management fee or carried interestfee or carried interest

Co-investment opportunities arise when GPs need Co-investment opportunities arise when GPs need additional equity financing to close a dealadditional equity financing to close a deal

Some institutional investors see co-investing as an Some institutional investors see co-investing as an opportunity to acquire expertise in private equity opportunity to acquire expertise in private equity investinginvesting

For GPs, LPs that stand ready to co-invest For GPs, LPs that stand ready to co-invest represent a flexible source of funds for closing represent a flexible source of funds for closing dealsdeals

24

Transaction OriginationTransaction Origination

25

Deal FlowDeal Flow

Deal flow, access to high quality investment Deal flow, access to high quality investment opportunities, is absolutely crucialopportunities, is absolutely crucial

GPs rely on relationships with third parties and GPs rely on relationships with third parties and industry contacts for deal flow generationindustry contacts for deal flow generation

The greater the deal flow, the higher the The greater the deal flow, the higher the likelihood of identifying an attractive likelihood of identifying an attractive opportunityopportunity

““Proprietary” deals are more attractive than Proprietary” deals are more attractive than deals brought by agents or intermediariesdeals brought by agents or intermediaries Less competition means lower purchase priceLess competition means lower purchase price Lower purchase price means higher IRRsLower purchase price means higher IRRs

26

OriginationOrigination

Investment banks, consultants, lawyers and Investment banks, consultants, lawyers and industry contacts introduce potential industry contacts introduce potential opportunitiesopportunities

Preliminary opportunity analysis will be Preliminary opportunity analysis will be performed relatively quicklyperformed relatively quickly

Initial decision is quickly made whether a PE Initial decision is quickly made whether a PE firm would be interested in the opportunityfirm would be interested in the opportunity PE firms have different investment strategies and PE firms have different investment strategies and

views of the worldviews of the world If interested, PE firms would sign If interested, PE firms would sign

Confidentiality Agreement to begin evaluating Confidentiality Agreement to begin evaluating the opportunitythe opportunity

27

Screening of DealsScreening of Deals

Deal screening is art and scienceDeal screening is art and science PE firms receive many investment proposals in a yearPE firms receive many investment proposals in a year Proposals are first screened to eliminate those that Proposals are first screened to eliminate those that

are clearly fail to meet investment criteriaare clearly fail to meet investment criteria Specialization on a specific industry or geography Specialization on a specific industry or geography

reduces the number of investment opportunities reduces the number of investment opportunities consideredconsidered

Initial review takes a 1 – 2 days and results in the Initial review takes a 1 – 2 days and results in the rejection of ~ 90% of proposals received by a PE firmrejection of ~ 90% of proposals received by a PE firm

““Surviving” proposals then become subject to a Surviving” proposals then become subject to a secondary review after the signing of a secondary review after the signing of a Confidentiality AgreementConfidentiality Agreement

Proposals that survive the preliminary and secondary Proposals that survive the preliminary and secondary reviews become the subject of a comprehensive due reviews become the subject of a comprehensive due diligence processdiligence process

28

Non-Binding Indications of Non-Binding Indications of InterestInterest

Commonly referred to as “1st round bid”Commonly referred to as “1st round bid” Give sellers a perspective on the level of Give sellers a perspective on the level of

buyer interest and the valuation buyer interest and the valuation parameters buyers are likely to assumeparameters buyers are likely to assume

Indication of interest subject to:Indication of interest subject to: Completion of business, legal, accounting Completion of business, legal, accounting

and environmental due diligenceand environmental due diligence Negotiation and execution of documentsNegotiation and execution of documents Receipt of necessary approvalsReceipt of necessary approvals Negotiation of employment agreements with Negotiation of employment agreements with

key managementkey management

29

Leveraged BuyoutsLeveraged Buyouts

30

What is an LBO?What is an LBO?

Acquisition of a company where a PE firm uses cash Acquisition of a company where a PE firm uses cash equity and debt to fund the purchase priceequity and debt to fund the purchase price

PE firm injects equity into a new shell company PE firm injects equity into a new shell company (“NewCo”), which borrows debt and simultaneously (“NewCo”), which borrows debt and simultaneously acquires the targetacquires the target

PE firm contributes capital, operating and financial PE firm contributes capital, operating and financial expertise, strategic insight, contacts and expertise, strategic insight, contacts and management talentmanagement talent

Management ownership increases, creating higher Management ownership increases, creating higher incentives to improve operations and deliver resultsincentives to improve operations and deliver results

Debt is repaid by the operating cash flows or by the Debt is repaid by the operating cash flows or by the sale of non-core assets of the acquired businesssale of non-core assets of the acquired business

LBO is similar to buying and renting out a house - LBO is similar to buying and renting out a house - the rent cash flows to pay down the mortgage debtthe rent cash flows to pay down the mortgage debt

31

Typical LBO StructureTypical LBO Structure

Ownership

Purchase price Equity investment

Bonds Bank loan

NewCo acquires Target

Acquiror (LBO firm)

Banks

Current Owners

Bond Holders

NewCo

Target

32

Typical LBO StructureTypical LBO Structure

Varies over time with market Varies over time with market conditionsconditions

Sources of financingSources of financing 40 – 50% senior bank debt (5-7 years)40 – 50% senior bank debt (5-7 years) 20 – 30% subordinated debt (8-12 20 – 30% subordinated debt (8-12

years)years) 20 – 40% common equity20 – 40% common equity

Bank debt is secured from Bank debt is secured from receivables, inventory and PP&Ereceivables, inventory and PP&E

33

Good LBO CandidatesGood LBO Candidates

History of consistent profitabilityHistory of consistent profitability Predictable cash flows to service debtPredictable cash flows to service debt Availability of excess cashAvailability of excess cash Easily separable assets or businessesEasily separable assets or businesses Strong management teamStrong management team Strong brands and market positionStrong brands and market position Industry with barriers to entryIndustry with barriers to entry Little danger from disruptive changes Little danger from disruptive changes

(technology, regulatory, etc.)(technology, regulatory, etc.) Visible/feasible exit strategy (IPO or M&A)Visible/feasible exit strategy (IPO or M&A)

34

Value CreationValue Creation

StrategicStrategic Vision, growth initiatives, add-on acquisitions, Vision, growth initiatives, add-on acquisitions,

exitexit OperationalOperational

Sales, costs, assetsSales, costs, assets OrganizationalOrganizational

Processes, structure, systems, skillsProcesses, structure, systems, skills FinancialFinancial

Balance sheet, tax structure, capitalizationBalance sheet, tax structure, capitalization Expansion in valuation multiplesExpansion in valuation multiples Advantages of being privateAdvantages of being private

35

How Do PE Firms Create Value?How Do PE Firms Create Value?

Minimize purchase priceMinimize purchase price Maximize leverageMaximize leverage Minimize liabilities purchasedMinimize liabilities purchased Manage transaction costsManage transaction costs Improve business operationsImprove business operations Maximize tax efficiencyMaximize tax efficiency Optimize exitOptimize exit

36

Minimize Purchase PriceMinimize Purchase Price

Avoid competitionAvoid competition Auction process vs. proprietary dealAuction process vs. proprietary deal

Maintain price disciplineMaintain price discipline Avoid “deal fever”Avoid “deal fever”

Maximize deductions from Maximize deductions from headline priceheadline price Earn outsEarn outs Liabilities – pension, legal, otherLiabilities – pension, legal, other

37

Maximize LeverageMaximize Leverage

Maintain competitive process among Maintain competitive process among banks willing to fund the transactionbanks willing to fund the transaction

Choose right financing structureChoose right financing structure Balance of risk, flexibility and interest Balance of risk, flexibility and interest

costcost Seller notes and staple financingSeller notes and staple financing

Deeply subordinate and at attractive Deeply subordinate and at attractive termsterms

Partner with co-investorsPartner with co-investors

38

Minimize Liabilities PurchasedMinimize Liabilities Purchased

Detailed due diligenceDetailed due diligence LegalLegal FinancialFinancial AccountingAccounting EnvironmentalEnvironmental

Tough negotiationsTough negotiations Reps and WarrantiesReps and Warranties

39

Transaction Costs and TaxationTransaction Costs and Taxation

Minimize transaction costsMinimize transaction costs Internal costsInternal costs Aborted deal costsAborted deal costs

Maximize tax efficiencyMaximize tax efficiency Increase interest tax shieldIncrease interest tax shield Increase depreciationIncrease depreciation Increase tax deductible amortizationIncrease tax deductible amortization

40

Improve Business OperationsImprove Business Operations

Top line growthTop line growth New markets, partnersNew markets, partners ProductsProducts

Margin improvementMargin improvement COGSCOGS SG&ASG&A

41

ExitExit

Difficult to predict future business cycles and Difficult to predict future business cycles and market conditionsmarket conditions

Prepare an exit strategy and groom the Prepare an exit strategy and groom the business for that exitbusiness for that exit

Trade sale or M&A – “clean” cash exitTrade sale or M&A – “clean” cash exit IPO – long process, company needs to be IPO – long process, company needs to be

above a certain size, lock-up restrictionsabove a certain size, lock-up restrictions Leveraged recapitalization – allows sponsor to Leveraged recapitalization – allows sponsor to

remove invested capital prior to ultimate exit, remove invested capital prior to ultimate exit, increases IRR and hedges against poor exitincreases IRR and hedges against poor exit

Secondary buyout – selling to another sponsorSecondary buyout – selling to another sponsor

42

Sources and Uses of FundsSources and Uses of Funds

SOURCES USES

New Revolver (L + 275 bps) $ 25.0 Purchase Price of Equity $ 250.0

New Term Loan A (L + 275 bps) 150.0 Refinance Existing Debt 630.0

New Term Loan B (L + 325 bps) 200.0 Assume Capital Leases 25.0

Assume Capital Leases 25.0 Transaction Costs 20.0

Total Senior Debt 400.0

New Senior Subordinated Notes (12%) 250.0

Total Debt 650.0

New PIK Preferred / Seller Paper (14%) 75.0

Acquiror’s Equity / Strategic Cash 200.0

Total Sources $925.0 Total Uses $925.0

43

Sources of FundsSources of Funds

EquityEquity New equity injection from LBO sponsorNew equity injection from LBO sponsor Potential equity contribution from existing Potential equity contribution from existing

managementmanagement Potential continuing equity investment by existing Potential continuing equity investment by existing

shareholders (“rollover”)shareholders (“rollover”) Equity from a strategic partnerEquity from a strategic partner

DebtDebt Bank debt (“senior” debt)Bank debt (“senior” debt) High yield debt (“subordinated” debt)High yield debt (“subordinated” debt)

Mezzanine securitiesMezzanine securities Can be structured to be more “debt-like” or more Can be structured to be more “debt-like” or more

“equity-like” depending on the situation“equity-like” depending on the situation

44

Bank DebtBank Debt

Senior secured (most senior debt)Senior secured (most senior debt) Flexible, interest rate is floatingFlexible, interest rate is floating Matures before other debt classes, Matures before other debt classes,

amortizingamortizing Typically callable/prepayable at parTypically callable/prepayable at par Quarterly interest paymentsQuarterly interest payments Maintenance covenantsMaintenance covenants Structured at the operating company levelStructured at the operating company level Underwritten via syndicationUnderwritten via syndication Diligence, commitment, launch, syndicate, Diligence, commitment, launch, syndicate,

fundfund

45

Bank DebtBank Debt

Revolving Credit Facilities vs. Term loansRevolving Credit Facilities vs. Term loans Revolvers allow multiple drawings for working capital Revolvers allow multiple drawings for working capital

and general corporate needsand general corporate needs Term loans funded at closingTerm loans funded at closing

Pro Rata facilitiesPro Rata facilities Revolver and Term Loan A – held by commercial banksRevolver and Term Loan A – held by commercial banks Buy and hold mentality, shrinking segmentBuy and hold mentality, shrinking segment

Institutional tranchesInstitutional tranches Consist of Term Loans “B”, “C” or “D”- held by Consist of Term Loans “B”, “C” or “D”- held by

insurance companies, CLOs and CDOs, growing insurance companies, CLOs and CDOs, growing segmentsegment

Purely transactional, liquidity in the secondary marketPurely transactional, liquidity in the secondary market Minimal front-end amortizationMinimal front-end amortization

46

High Yield Bond DebtHigh Yield Bond Debt

Usually subordinated and/or unsecuredUsually subordinated and/or unsecured Interest rate is fixed, maturity of 8-10 yearsInterest rate is fixed, maturity of 8-10 years ““Bullet” maturity after full bank debt Bullet” maturity after full bank debt

amortizationamortization Usually not callable at par in early years, Usually not callable at par in early years,

typically 1-5 yearstypically 1-5 years Structured at the operating company levelStructured at the operating company level Publicly quoted securityPublicly quoted security Incurrence covenantsIncurrence covenants Diligence, document, roadshow, price and Diligence, document, roadshow, price and

fundfund

47

Mezzanine DebtMezzanine Debt

Subordinated to bank debt and high Subordinated to bank debt and high yield bondsyield bonds

Flexible, typically floating interest rateFlexible, typically floating interest rate Non-amortizing, “bullet” maturity Non-amortizing, “bullet” maturity

typically after 10 yearstypically after 10 years Cash & PIK coupon payment further Cash & PIK coupon payment further

enhanced with equity warrantsenhanced with equity warrants PIK component can “eat” into equityPIK component can “eat” into equity Structurally subordinated at the holding Structurally subordinated at the holding

company levelcompany level Incurrence covenantsIncurrence covenants

48

Due DiligenceDue Diligence

49

Due DiligenceDue Diligence

ObjectiveObjective Validate business conceptValidate business concept Verify marketVerify market Appraise managementAppraise management Validate forecastsValidate forecasts

ValuationValuation Diligence establishes basis for valuation, price and Diligence establishes basis for valuation, price and

negotiationnegotiation Diligence is expensive and time consumingDiligence is expensive and time consuming

Diligence strategyDiligence strategy Preliminary evaluation to identify “deal-breakers” Preliminary evaluation to identify “deal-breakers”

before spending time and money on detailed due before spending time and money on detailed due diligencediligence

50

Key Topics for Due DiligenceKey Topics for Due Diligence

Business concept, opportunityBusiness concept, opportunity MarketMarket CompetitionCompetition CustomersCustomers ProductsProducts ManagementManagement FinancialsFinancials ReturnsReturns

51

Business Concept, OpportunityBusiness Concept, Opportunity

What is the concept/opportunity?What is the concept/opportunity? Is the opportunity sustainable?Is the opportunity sustainable? Potential size of the opportunity?Potential size of the opportunity? How can the target company How can the target company

capitalize on the opportunity?capitalize on the opportunity? Is the proposed plan/strategy Is the proposed plan/strategy

realistic?realistic? How does the target business fit to its How does the target business fit to its

markets and region?markets and region? Why are we so smart or lucky?Why are we so smart or lucky?

52

MarketMarket

Market characteristics, segments, size, Market characteristics, segments, size, growth, cyclicality, key metrics, growth, cyclicality, key metrics, demographics?demographics?

Projected market share and sales Projected market share and sales volume?volume?

Low barriers to entry into the market?Low barriers to entry into the market? Is target’s business model sustainable?Is target’s business model sustainable? How will the business be perceived by How will the business be perceived by

customers?customers? Regulatory issues?Regulatory issues?

53

CompetitionCompetition

Who are the direct competitors? Who are the direct competitors? Relative size, scope, cost basis, brands and Relative size, scope, cost basis, brands and

market share?market share? What are the key factors/levers of What are the key factors/levers of

competition in the industry?competition in the industry? How is target’s business strategy different How is target’s business strategy different

than competitors’?than competitors’? What are target’s competitive advantages?What are target’s competitive advantages? What are the target’s competitive What are the target’s competitive

disadvantages?disadvantages? Threat from potential new entrants?Threat from potential new entrants?

54

CustomersCustomers

Who are the customers?Who are the customers? Current and future customer base?Current and future customer base? What specific market and customer needs What specific market and customer needs

does the target business serve?does the target business serve? How do customers make their purchase How do customers make their purchase

decisions? Key criteria?decisions? Key criteria? Customer satisfaction and retention?Customer satisfaction and retention? Does the projected number of customers Does the projected number of customers

or sales make sense? Realistic?or sales make sense? Realistic? How will the target acquire new How will the target acquire new

customers?customers?

55

ProductsProducts

Product life cycle, penetration trends?Product life cycle, penetration trends? Product pricing?Product pricing? Product profitability? Product profitability? Productivity versus competition?Productivity versus competition? Maintain or “jettison” certain products?Maintain or “jettison” certain products? Plant consolidation?Plant consolidation? Inventory optimization?Inventory optimization? CAPEX requirements?CAPEX requirements? Development plans?Development plans?

56

ManagementManagement

Competent?Competent? Experienced?Experienced? Cohesive?Cohesive? Strategic?Strategic? Flexible?Flexible? Incentivized?Incentivized? Proactive?Proactive? Realistic?Realistic?

57

FinancialsFinancials

What is the optimal capital structure?What is the optimal capital structure? Are revenue and cost projections Are revenue and cost projections

comprehensive, realistic, reasonable?comprehensive, realistic, reasonable? What are the underlying business What are the underlying business

assumptions of the projections?assumptions of the projections? Impact of various business case Impact of various business case

scenarios?scenarios? How does cash flow in this business?How does cash flow in this business? How much capital investment needed? How much capital investment needed?

When?When? Correct accounting treatment?Correct accounting treatment? What are the key sensitivities?What are the key sensitivities?

58

Confirming ValueConfirming Value

Financial and accounting diligence Financial and accounting diligence is primarily focused on drilling into is primarily focused on drilling into the basic components of valuationthe basic components of valuation

Recurring EBITDA (adjust for Recurring EBITDA (adjust for extraordinary items)extraordinary items)

CAPEXCAPEX Working CapitalWorking Capital Cash FlowCash Flow MultipleMultiple

59

Recurring EBITDARecurring EBITDA

General issues – exclusions, accounting changes, General issues – exclusions, accounting changes, pro forma adjustmentspro forma adjustments

Revenue – components, method of recognition, Revenue – components, method of recognition, customers, customer arrangements, customers, customer arrangements, pricing/volumepricing/volume

Margins – components of cost of sales, gross Margins – components of cost of sales, gross margin trendsmargin trends

Reserves – under/over statement of profitsReserves – under/over statement of profits Compensation – benefits, headcount needs, Compensation – benefits, headcount needs,

transition issues, bonustransition issues, bonus SG&A – components, trends, discretionary costs, SG&A – components, trends, discretionary costs,

fixed vs. variable, cost savingsfixed vs. variable, cost savings Other – restructurings, acquisitions, contingenciesOther – restructurings, acquisitions, contingencies

60

CAPEXCAPEX

Determine normalized annual CAPEXDetermine normalized annual CAPEX Maintenance or mandatory CAPEXMaintenance or mandatory CAPEX

Determine expansion CAPEXDetermine expansion CAPEX Discretionary CAPEXDiscretionary CAPEX

CAPEX between signing and closing of CAPEX between signing and closing of transaction reduce net cash positiontransaction reduce net cash position

Important to have correct CAPEX Important to have correct CAPEX assumptions in calculating exit valueassumptions in calculating exit value

61

Working CapitalWorking Capital

Analyze working capital cycleAnalyze working capital cycle Components of B/S accountsComponents of B/S accounts Needs and trendsNeeds and trends Savings opportunitiesSavings opportunities Potential closing balance sheet Potential closing balance sheet

issuesissues Important to have correct working Important to have correct working

capital assumptions in calculating capital assumptions in calculating exit valueexit value

62

Legal Due DiligenceLegal Due Diligence

Conducted in tandem with business, Conducted in tandem with business, financial and accounting due diligencefinancial and accounting due diligence

Structure the transaction in the most Structure the transaction in the most tax efficient mannertax efficient manner

Understand the legal aspects of Understand the legal aspects of target’s business and assets being target’s business and assets being acquiredacquired

Identify and evaluate liabilitiesIdentify and evaluate liabilities Materials are typically made available Materials are typically made available

for review in a data roomfor review in a data room

63

What Is a Bad Deal?What Is a Bad Deal?

No real competitive advantage of PE firmNo real competitive advantage of PE firm Long list of things that have to go right to Long list of things that have to go right to

make the deal workmake the deal work ““Build it and they will come” is not a good Build it and they will come” is not a good

business strategybusiness strategy Aggressive estimates of future growthAggressive estimates of future growth Employing the wrong management teamEmploying the wrong management team True downside case is not adequately True downside case is not adequately

evaluatedevaluated

64

Transaction Structuring and Transaction Structuring and DocumentationDocumentation

65

Term SheetsTerm Sheets

Preliminary documents designed to provide a framework Preliminary documents designed to provide a framework for negotiations between investors and the target for negotiations between investors and the target companycompany

Provides collective understanding of the proposed Provides collective understanding of the proposed transaction, basic terms and conditionstransaction, basic terms and conditions

Generally focuses on the target’s valuation and the Generally focuses on the target’s valuation and the conditions under which investors agree to provide conditions under which investors agree to provide financingfinancing

Term sheet eventually transforms into a formal Term sheet eventually transforms into a formal agreement known as the Purchase Agreement, which is a agreement known as the Purchase Agreement, which is a legal document that detailslegal document that details who is buying whatwho is buying what from whomfrom whom at what priceat what price whenwhen

66

Key Sections of Term SheetsKey Sections of Term Sheets

AcquirerAcquirer TargetTarget ValuationValuation Structure of acquisitionStructure of acquisition Management compensationManagement compensation Debt financingDebt financing Board of directorsBoard of directors RightsRights Transaction feesTransaction fees Management feesManagement fees

67

Purchase AgreementPurchase Agreement

Transaction terms and structureTransaction terms and structure Description of asset soldDescription of asset sold Calculation of purchase priceCalculation of purchase price Closing dateClosing date Reps and Warranties – buyer and Reps and Warranties – buyer and

sellerseller Conditions to closing – sellerConditions to closing – seller Conditions to closing – buyerConditions to closing – buyer Conditions for terminationConditions for termination

68

Purchase AgreementPurchase Agreement

Clarity regarding key financial and deal termsClarity regarding key financial and deal terms Business/assets being acquired and the Business/assets being acquired and the

liabilities being assumedliabilities being assumed Arrangements for asset sharing going forwardArrangements for asset sharing going forward Protecting the acquirer from contingent or Protecting the acquirer from contingent or

undisclosed liabilitiesundisclosed liabilities Locking up the target, no “shopping” of the dealLocking up the target, no “shopping” of the deal Representations and Warranties – verification of Representations and Warranties – verification of

factual matters covered during the due factual matters covered during the due diligencediligence

Pre-closing operationsPre-closing operations Closing conditions – fiduciary outs, break up feeClosing conditions – fiduciary outs, break up fee Purchase price adjustments – post closing Purchase price adjustments – post closing

adjustmentadjustment

69

Representations and WarrantiesRepresentations and Warranties

Statement of fact at a particular point in timeStatement of fact at a particular point in time PurposePurpose

Provides basis for refusal to close the transaction if Provides basis for refusal to close the transaction if untrue (pre-close)untrue (pre-close)

Provides basis for post-closing indemnification for Provides basis for post-closing indemnification for damages if untrue (post-close)damages if untrue (post-close)

Mainly refers to areas covered in due diligenceMainly refers to areas covered in due diligence Financial statements, liabilities, contracts, real estate, Financial statements, liabilities, contracts, real estate,

litigation, taxeslitigation, taxes Both buyer and seller gives Reps & WarrantiesBoth buyer and seller gives Reps & Warranties Buyer’s objective – understand what I am Buyer’s objective – understand what I am

buyingbuying Seller’s objective – increase certainty of closingSeller’s objective – increase certainty of closing

70

CovenantsCovenants

Agreements to act or refrain from acting in the Agreements to act or refrain from acting in the futurefuture

Positive vs. Negative covenantsPositive vs. Negative covenants Necessary because signing and closing are not Necessary because signing and closing are not

simultaneoussimultaneous Pre-closing covenantsPre-closing covenants

Largely to the benefit of buyerLargely to the benefit of buyer Objective is to preserve the asset to be purchased and Objective is to preserve the asset to be purchased and

ensure closing occursensure closing occurs Post-closing covenantsPost-closing covenants

To the benefit of sellerTo the benefit of seller Objective is to protect certain interests once seller no Objective is to protect certain interests once seller no

longer owns the businesslonger owns the business

71

CovenantsCovenants

Pre-closingPre-closing Operations in the ordinary course of businessOperations in the ordinary course of business No solicitation of proposals from competing No solicitation of proposals from competing

buyersbuyers No dividends and distributionsNo dividends and distributions No issuance of equity or incurrence of debtNo issuance of equity or incurrence of debt No acquisitions and divestituresNo acquisitions and divestitures No execution of significant contractsNo execution of significant contracts No change in accounting practicesNo change in accounting practices

Post-closingPost-closing No changes to compensationNo changes to compensation No hiring or firing of key management No hiring or firing of key management

employeesemployees

72

Closing ConditionsClosing Conditions

Transaction will not close until all conditions are satisfiedTransaction will not close until all conditions are satisfied Representations and warranties are trueRepresentations and warranties are true Absence of material adverse change in the businessAbsence of material adverse change in the business

Excludes general economic or industry conditions, stock price Excludes general economic or industry conditions, stock price movements, failure to meet forecasts, matters known to buyermovements, failure to meet forecasts, matters known to buyer

Receipt of required government approvals and major third Receipt of required government approvals and major third party consentsparty consents

Debt financing available on terms and conditions set forth in Debt financing available on terms and conditions set forth in commitment letterscommitment letters

Termination is cessation of both parties’ obligationsTermination is cessation of both parties’ obligations ““Drop dead” date – financing and regulatoryDrop dead” date – financing and regulatory Breaches - break up fee ~5%Breaches - break up fee ~5% Fiduciary outFiduciary out

Buyer’s objective – to be able to walk away if anything major Buyer’s objective – to be able to walk away if anything major is wrongis wrong

Seller’s objective – to have some certainty that transaction will Seller’s objective – to have some certainty that transaction will close if things are in reasonable orderclose if things are in reasonable order

73

Deal Process Inside the PE FirmDeal Process Inside the PE Firm

Initial screening of dealsInitial screening of deals ““Heads up” memorandumHeads up” memorandum Non-binding indications / term Non-binding indications / term

sheetssheets Detailed due diligence and Detailed due diligence and

evaluationevaluation Formal and detailed presentation to Formal and detailed presentation to

the investment committeethe investment committee Final approval and fundingFinal approval and funding

74

Heads Up MemoHeads Up Memo

Why is the company being sold?Why is the company being sold? What is the investment thesis?What is the investment thesis? How does the opportunity fit with the PE How does the opportunity fit with the PE

firm’s investment strategy and skill base?firm’s investment strategy and skill base? What are the size, structure and timing of What are the size, structure and timing of

the investment?the investment? What is the PE firm’s “edge” in the What is the PE firm’s “edge” in the

process?process? What is the due diligence road map?What is the due diligence road map? How will the PE firm exit the investment?How will the PE firm exit the investment? What are the expected returns and key What are the expected returns and key

assumptions driving the projections?assumptions driving the projections?

75

Formal Investment Committee Formal Investment Committee MemoMemo Analysis of the deal opportunity, the business, Analysis of the deal opportunity, the business,

the transaction, the process, industry trends, the transaction, the process, industry trends, due diligence resultsdue diligence results

Detailed discussion of risks and opportunitiesDetailed discussion of risks and opportunities Detailed analysis of operating and financial Detailed analysis of operating and financial

projectionsprojections Detailed scenario analysis and projected returnsDetailed scenario analysis and projected returns Key questions to answer:Key questions to answer:

Why do we want to do this deal?Why do we want to do this deal? What is our edge?What is our edge? What value do we bring to this deal?What value do we bring to this deal? Who is the competition?Who is the competition? How and when will we exit?How and when will we exit? Impact of this deal on the rest of the portfolio?Impact of this deal on the rest of the portfolio?

76

Portfolio Company MonitoringPortfolio Company Monitoring

77

Portfolio Company LifePortfolio Company Life

Year 1 – Figure out what you just boughtYear 1 – Figure out what you just bought Fix problems, focus on 2-3 key areas to Fix problems, focus on 2-3 key areas to

improveimprove Assess and change out managementAssess and change out management

Years 2-3 – Strategic Plan and ExecutionYears 2-3 – Strategic Plan and Execution Develop strategic business planDevelop strategic business plan Make investments, pursue acquisitionsMake investments, pursue acquisitions Execute planExecute plan Pay down debtPay down debt

Year 4-5 – Prepare for ExitYear 4-5 – Prepare for Exit Windows dressing, clean upWindows dressing, clean up Sell on good performanceSell on good performance

78

Portfolio MonitoringPortfolio Monitoring

Takes place at least quarterlyTakes place at least quarterly Candid and open discussion on the Candid and open discussion on the

status of each investmentstatus of each investment Progress of investment thesisProgress of investment thesis Value already createdValue already created Problems experiencedProblems experienced Changes needed to the “game plan”Changes needed to the “game plan” Basis for valuationBasis for valuation Exit planning and timingExit planning and timing

79

Portfolio MonitoringPortfolio Monitoring

Information gathering is crucialInformation gathering is crucial Board seats provide meaningful accessBoard seats provide meaningful access Monthly financial and operational Monthly financial and operational

statistics are provided to PE investorsstatistics are provided to PE investors Regular interaction (weekly/monthly Regular interaction (weekly/monthly

conference calls) with managementconference calls) with management Weekly PE firmwide meetingsWeekly PE firmwide meetings Quarterly MD&A write-ups from portfolio Quarterly MD&A write-ups from portfolio

companiescompanies Annual audit reportsAnnual audit reports

80

Portfolio Company AssistancePortfolio Company Assistance

Strategic and operational adviceStrategic and operational advice Financial engineering expertiseFinancial engineering expertise Recruitment of top management and board membersRecruitment of top management and board members Leveraging industry contacts for identifying future Leveraging industry contacts for identifying future

partners, marketspartners, markets Revenue growthRevenue growth Gross margin improvementGross margin improvement Operating expense reductionOperating expense reduction Cash flow improvementCash flow improvement Crisis managementCrisis management Corporate governanceCorporate governance Exit preparationExit preparation Degree of involvement varies with type of investmentDegree of involvement varies with type of investment

81

Mechanisms of ControlMechanisms of Control

Board RepresentationBoard Representation GPs are extremely influential and effective outside directorsGPs are extremely influential and effective outside directors GPs have the resources and staff to monitor portfolio GPs have the resources and staff to monitor portfolio

companiescompanies Allocation of Voting RightsAllocation of Voting Rights

GP investment is large enough to achieve majority ownershipGP investment is large enough to achieve majority ownership In some situations, GPs may obtain voting control even if they In some situations, GPs may obtain voting control even if they

are not majority shareholdersare not majority shareholders In general, a GP’s voting rights do not depend on the type of In general, a GP’s voting rights do not depend on the type of

stock issued. For example, holders of convertible preferred stock issued. For example, holders of convertible preferred stock may be allowed to vote their shares on an as converted stock may be allowed to vote their shares on an as converted basisbasis

Control of Access to Additional FinancingControl of Access to Additional Financing Venture Capital is provided in several roundsVenture Capital is provided in several rounds Influence of original investor is high on new GPs’ willingness to Influence of original investor is high on new GPs’ willingness to

participate in subsequent roundsparticipate in subsequent rounds

82

Best PracticesBest Practices

Interact regularly with the management Interact regularly with the management and gather timely informationand gather timely information

Focus on top 2-3 priorities and deliver Focus on top 2-3 priorities and deliver strategic and operational assistancestrategic and operational assistance

Evaluate progress made vs. planEvaluate progress made vs. plan Identify problems earlyIdentify problems early Adjust “game plan” as neededAdjust “game plan” as needed Value portfolio companies conservativelyValue portfolio companies conservatively Prepare for exit at least one year in Prepare for exit at least one year in

advanceadvance

83

ExitExit

84

ExitExit

Limited partnerships must be dissolved Limited partnerships must be dissolved within a certain time as they need to within a certain time as they need to return capital to LPsreturn capital to LPs

Exit = Monetization and realization of Exit = Monetization and realization of “paper” profits“paper” profits

Exit requires advanced planning and Exit requires advanced planning and preparationpreparation

SaleSale IPOIPO RecapitalizationRecapitalization

85

Exit PlanningExit Planning

Need to forecast the evolution of the Need to forecast the evolution of the businessbusiness

Closely follow macro trends in the industryClosely follow macro trends in the industry Who are the likely buyers?Who are the likely buyers?

Strategics vs. financial buyersStrategics vs. financial buyers Foreigners vs. local buyersForeigners vs. local buyers

Exit preparation takes timeExit preparation takes time Execute strategy and hit the budget forecastsExecute strategy and hit the budget forecasts Develop and prepare the management team Develop and prepare the management team Establish a “clean” track record (audits)Establish a “clean” track record (audits) Establish a reputable and competent boardEstablish a reputable and competent board

86

M&A ExitM&A Exit

AdvantagesAdvantages Buyers usually pay a premiumBuyers usually pay a premium ““Clean” exit with greater certaintyClean” exit with greater certainty Cheaper than IPOCheaper than IPO Faster and simpler than IPOFaster and simpler than IPO Convince one buyer vs. the whole marketConvince one buyer vs. the whole market

DisadvantagesDisadvantages May not be welcomed by the management – May not be welcomed by the management –

sale or merger imply reduced independencesale or merger imply reduced independence Buyer appetite can be unpredictableBuyer appetite can be unpredictable

87

M&A Sellside ProcessM&A Sellside Process

Investment bank (target advisor) due diligenceInvestment bank (target advisor) due diligence Investment bank (target advisor) writes selling memoInvestment bank (target advisor) writes selling memo Narrow the universe of potential buyers and place initial calls Narrow the universe of potential buyers and place initial calls

into buyersinto buyers Send and negotiate confidentiality agreementsSend and negotiate confidentiality agreements Send preliminary bid lettersSend preliminary bid letters Analyze preliminary bidsAnalyze preliminary bids Create management presentationsCreate management presentations Assemble data roomAssemble data room Buyer due diligenceBuyer due diligence Send final bid letterSend final bid letter Analyze final bidsAnalyze final bids Negotiate key termsNegotiate key terms Contract negotiations and documentationContract negotiations and documentation Transaction announcementTransaction announcement

88

IPO ExitIPO Exit

AdvantagesAdvantages Prestige of becoming a publicly traded companyPrestige of becoming a publicly traded company Currency for future M&A activityCurrency for future M&A activity Increased visibility for the companyIncreased visibility for the company Preservers a company’s independence and provides Preservers a company’s independence and provides

continued access to capitalcontinued access to capital DisadvantagesDisadvantages

Not an immediate, “clean” liquidity event for Not an immediate, “clean” liquidity event for investorsinvestors

Long and time-consumingLong and time-consuming Distraction for managementDistraction for management Expensive processExpensive process Information disclosure requirementsInformation disclosure requirements Lock upsLock ups

89

IPO ProcessIPO Process

1.1. Due Diligence and DraftingDue Diligence and Drafting Meetings with senior management, iterative drafting of registration Meetings with senior management, iterative drafting of registration

statement (Business Overview, Risk Factors, Financials, MD&A)statement (Business Overview, Risk Factors, Financials, MD&A)

2.2. Initial Filing with SECInitial Filing with SEC Generally accessible to the public and does not include the expected Generally accessible to the public and does not include the expected

share price range for the offeringshare price range for the offering

3.3. Structuring and ValuationStructuring and Valuation Selecting co-managers, setting the initial filing range that serves as a Selecting co-managers, setting the initial filing range that serves as a

valuation guideline for investors during the marketing processvaluation guideline for investors during the marketing process

4.4. Prospectus DistributionProspectus Distribution SEC gives comments on each draft of registration statement, the SEC gives comments on each draft of registration statement, the

preliminary Prospectus is mailed broadly to potential investorspreliminary Prospectus is mailed broadly to potential investors

5.5. Salesforce EducationSalesforce Education On the company’s story before marketing to potential investing clients, On the company’s story before marketing to potential investing clients,

management dry runsmanagement dry runs

6.6. Targeting InvestorsTargeting Investors Identification of best potential buyers, determine “anchor” buyers based Identification of best potential buyers, determine “anchor” buyers based

on their current holdings of stock, one-on-one meetingson their current holdings of stock, one-on-one meetings

90

IPO ProcessIPO Process

7.7. SyndicationSyndication The lead underwriter takes the primary responsibility for this, syndicate The lead underwriter takes the primary responsibility for this, syndicate

members underwrite a fixed amount of stock and may be given additional members underwrite a fixed amount of stock and may be given additional allotmentsallotments

8.8. Roadshow and BookbuildingRoadshow and Bookbuilding Schedule of meetings with investors in key cities around the world, lasts 2-3 Schedule of meetings with investors in key cities around the world, lasts 2-3

weeks, roadshow team makes formal presentations to investors at these weeks, roadshow team makes formal presentations to investors at these meetings, key investors are met in a one-on-one format, smaller investors are meetings, key investors are met in a one-on-one format, smaller investors are accommodated in a groupaccommodated in a group

In tandem with the marketing effort, the bookbuilding process begins, investors In tandem with the marketing effort, the bookbuilding process begins, investors submit indications of interest for shares in the IPO, the lead managers collect submit indications of interest for shares in the IPO, the lead managers collect these orders and build a book of demand over the course of the marketing these orders and build a book of demand over the course of the marketing period, a critical component is the collection of qualitative feedback on the period, a critical component is the collection of qualitative feedback on the orders in the bookorders in the book

9.9. Pricing and AllocationPricing and Allocation The quality of the book and aftermarket intentions of investors are critical, The quality of the book and aftermarket intentions of investors are critical,

share performance in the aftermarket is important, allocations to institutional share performance in the aftermarket is important, allocations to institutional and retail investorsand retail investors

10.10. AftermarketAftermarket Balance supply and demand in the aftermarket, over-allotment option, on-Balance supply and demand in the aftermarket, over-allotment option, on-

going research coverage (after 25 days) and trading supportgoing research coverage (after 25 days) and trading support

91

RecapitalizationRecapitalization

Usually, the acquired company is highly Usually, the acquired company is highly levered at the beginninglevered at the beginning

Over time, the company pays off debt with Over time, the company pays off debt with cash flows from its operationscash flows from its operations

This creates additional capacity to add This creates additional capacity to add more debt 1-3 years after the acquisitionmore debt 1-3 years after the acquisition

When additional debt is issued, excess When additional debt is issued, excess cash is dividended out to the equity cash is dividended out to the equity investorsinvestors

Investors achieve “partial” monetizationInvestors achieve “partial” monetization Refinancing a mortgage is effectively a Refinancing a mortgage is effectively a

recapitalizationrecapitalization

92

Capital Distribution to LPsCapital Distribution to LPs

Once an investment is “monetized”, the Once an investment is “monetized”, the profits will be divided between LPs and GPs profits will be divided between LPs and GPs according to the partnership agreementaccording to the partnership agreement

80% / 20% is usually the norm80% / 20% is usually the norm 80% to the LPs80% to the LPs 20% to the GPs20% to the GPs

A minimum return hurdle % for LPs may have A minimum return hurdle % for LPs may have to be cleared before GPs can claim their to be cleared before GPs can claim their share of profits (I.e. 8%)share of profits (I.e. 8%)

Clawback provisionClawback provision High returns make a strong track record High returns make a strong track record

which in turn makes future fundraising easierwhich in turn makes future fundraising easier

93

Other TopicsOther Topics

94

Business PlanBusiness Plan

Identify a business need or niche and Identify a business need or niche and demonstrate its feasibilitydemonstrate its feasibility

Analyze a product within the context of Analyze a product within the context of market and customermarket and customer

Evaluate the viability of a technologyEvaluate the viability of a technology Describe major goals, objectives, and Describe major goals, objectives, and

vision for 1 year, 3 years and 5 yearsvision for 1 year, 3 years and 5 years Assess ability of management to Assess ability of management to

executeexecute Provide detailed financial projectionsProvide detailed financial projections

95

Business Plan – Key SectionsBusiness Plan – Key Sections

Concept/OpportunityConcept/Opportunity StrategyStrategy OperationsOperations MarketsMarkets CustomersCustomers ProductsProducts CompetitionCompetition RisksRisks ImplementationImplementation

96

Concept/OpportunityConcept/Opportunity

Always stated within the context of an existing Always stated within the context of an existing or projected marketor projected market

Translate concept into terms that investors Translate concept into terms that investors can understandcan understand

Clearly highlight which market needs will be Clearly highlight which market needs will be filled or issues will be addressedfilled or issues will be addressed

Have comprehensive knowledge of the Have comprehensive knowledge of the competitive environment and the potential competitive environment and the potential reactions from competitorsreactions from competitors

Analyze the current and future customer base Analyze the current and future customer base in detail in detail

97

Raising MoneyRaising Money

The process of raising money may have The process of raising money may have significant costssignificant costs TimeTime Opportunity cost of distractionOpportunity cost of distraction Significant amount of questions and Significant amount of questions and

information requestsinformation requests Impact on the organization (I.e. uncertainty)Impact on the organization (I.e. uncertainty) Direct expenses – travel, legal and Direct expenses – travel, legal and

accountingaccounting May be beneficial to hire reputable May be beneficial to hire reputable

advisors with relevant past fundraising advisors with relevant past fundraising experience and track recordexperience and track record

98

Presenting to Private Equity Presenting to Private Equity FirmsFirms

Identify relevant PE firmsIdentify relevant PE firms May make sense to use advisorsMay make sense to use advisors Most effective if someone credible Most effective if someone credible

refers you to the PE firmrefers you to the PE firm Do your research in advanceDo your research in advance At the initial meeting, impress them and At the initial meeting, impress them and

capture their interestcapture their interest PE firms’ time is the biggest assetPE firms’ time is the biggest asset

99

Questions in PE MindsQuestions in PE Minds

Who are these people?Who are these people? Do they fit the way we do business?Do they fit the way we do business? What is the value and appeal of this business?What is the value and appeal of this business? Will there be enough customer demand for its products?Will there be enough customer demand for its products? What can go wrong with this company?What can go wrong with this company? What needs to be accomplished to justify this valuation?What needs to be accomplished to justify this valuation? What are the key trends in the industry and sector?What are the key trends in the industry and sector? How dependent is the value of this company on the overall How dependent is the value of this company on the overall

performance of the sector or industry?performance of the sector or industry? What is the likely response from competition?What is the likely response from competition? Do they have the right experience and skills to deliver?Do they have the right experience and skills to deliver? Do they have a realistic, relevant and flexible strategy?Do they have a realistic, relevant and flexible strategy? What are the exit implications?What are the exit implications? IPO and M&A market trends?IPO and M&A market trends? Can we/they win?Can we/they win?

100

Developing Economies Need…Developing Economies Need…

CapitalCapital Strategic visionStrategic vision GrowthGrowth CredibilityCredibility Global best practicesGlobal best practices Investor contactsInvestor contacts Management talentManagement talent

101

Private Equity Provides….Private Equity Provides….

Access to long-term financingAccess to long-term financing GPs and LPs with significant investing GPs and LPs with significant investing

experience around the globeexperience around the globe Valuable strategic insights and Valuable strategic insights and

operational expertiseoperational expertise Significant financial disciplineSignificant financial discipline Substantial credibility and visibility to Substantial credibility and visibility to

target company and the countrytarget company and the country Best practices to pursue profitable Best practices to pursue profitable

growthgrowth

102

Positive Impact of Private EquityPositive Impact of Private Equity

A long-term support to those companies A long-term support to those companies with the potential of success and with the potential of success and sustainabilitysustainability

Builds and grows business faster than they Builds and grows business faster than they otherwise wouldotherwise would

Encourages entrepreneurial spirit, Encourages entrepreneurial spirit, technological advancement and job creationtechnological advancement and job creation

Crucial to the existence, feasibility and Crucial to the existence, feasibility and success of businesses in the seed/start-up success of businesses in the seed/start-up and expansion stagesand expansion stages

Teaches discipline of the “buyside”Teaches discipline of the “buyside”

103

Priorities for Private EquityPriorities for Private Equity

Promote entrepreneurial environment Promote entrepreneurial environment and increase incentives for and increase incentives for entrepreneurial investmentsentrepreneurial investments

Facilitate private equity fund Facilitate private equity fund formationformation

Develop long-term capital sourcesDevelop long-term capital sources Incorporate private equity needs and Incorporate private equity needs and

perspectives into policy-makingperspectives into policy-making

104

Entrepreneurial EnvironmentEntrepreneurial Environment

Minimum regulation and bureaucracyMinimum regulation and bureaucracy Simplified requirements of company Simplified requirements of company

formationformation Support for private equity and Support for private equity and

entrepreneurial educationentrepreneurial education Favorable tax regime – capital gainsFavorable tax regime – capital gains Equity and options ownershipEquity and options ownership Awareness of private equity as engine Awareness of private equity as engine

of growth and value creationof growth and value creation

105

Long-Term Capital SourcesLong-Term Capital Sources

Access to long-term funding is essential Access to long-term funding is essential for PE firmsfor PE firms

Development of pension funds and Development of pension funds and relevant regulatory regime is a critical relevant regulatory regime is a critical stepstep

U.S. exampleU.S. example Pension funds should be allowed to Pension funds should be allowed to

invest in private equityinvest in private equity Unrestricted movement of capital is a Unrestricted movement of capital is a

must-have for private equity industrymust-have for private equity industry

106

Rules for Private Equity Rules for Private Equity InvestingInvesting

1.1. Develop your own idea of what a business is worthDevelop your own idea of what a business is worth

2.2. Avoid auctionsAvoid auctions

3.3. Pick your spotsPick your spots

4.4. Approach each potential transaction with Approach each potential transaction with overwhelming forceoverwhelming force

5.5. Follow the cashFollow the cash

6.6. Get timely help from experts, advisorsGet timely help from experts, advisors

7.7. Keep your emotions in check (“deal fever”)Keep your emotions in check (“deal fever”)

8.8. Develop trust with your team and managersDevelop trust with your team and managers

9.9. Make sure acquired company managers concentrate Make sure acquired company managers concentrate on the few vital objectiveson the few vital objectives

10.10. When management team is not working, change them When management team is not working, change them as soon as possibleas soon as possible