1 financial issues discussions may 30, 2002 payments & securities clearance and settlement...

TRANSCRIPT

1

Financial Issues DiscussionsMay 30, 2002

Payments & Securities Clearance and Settlement Systems

Compliance with International Principles

Robert H. Keppler Financial Sector Development Department

2

The role of the World Bank in the transformation process in payment systems

Developing the Core Principles for Systemically Important Payment Systems

Applying the Core Principles International Standards for SSS

Compliance with International Principles

3

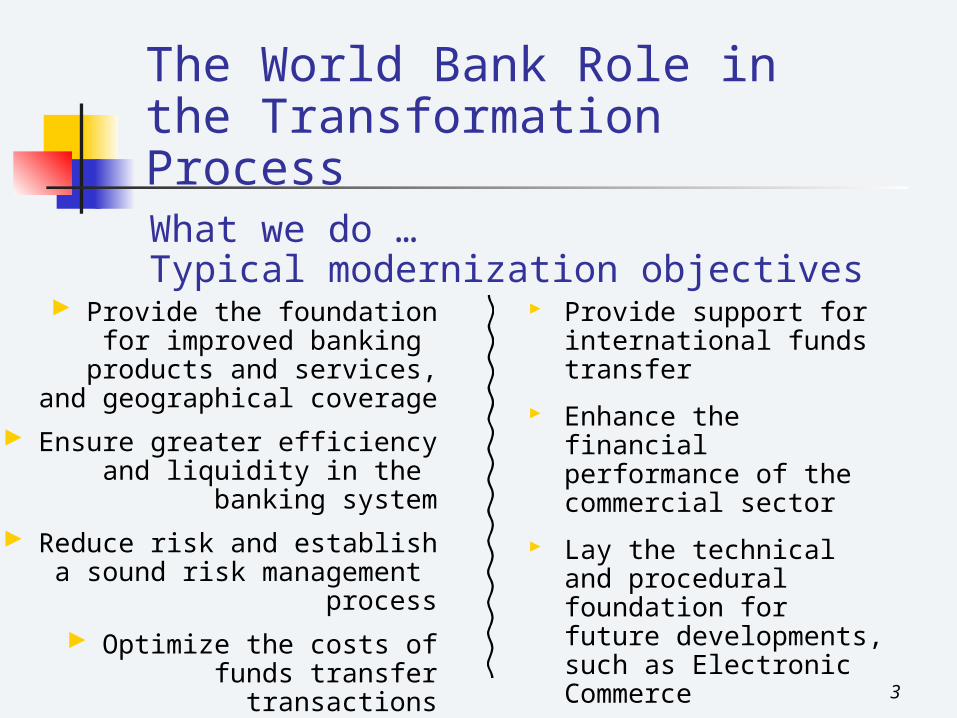

Provide the foundation for improved banking products

and services, and geographical coverage

Ensure greater efficiency and liquidity in the banking

system

Reduce risk and establish a sound risk management

process

Optimize the costs of funds transfer transactions

Provide support for international funds transfer

Enhance the financial performance of the commercial sector

Lay the technical and procedural foundation for future developments, such as Electronic Commerce

The World Bank Role in the Transformation ProcessWhat we do …Typical modernization objectives

4

Comprehensive initiatives: China, Vietnam, Algeria, Angola, Azerbaijan, BCEAO,

BEAC, Libya, etc.

Undertaking initial diagnostics and developing reform strategies: Costa Rica, Ecuador, Haiti, India, Indonesia,

Madagascar, Morocco, Poland, Thailand, Tunisia, Venezuela, etc.

Providing specific technical advice: Estonia, Hong Kong, Russia, Ukraine, Iran, Moldova,

Barbados, etc.

The World Bank Role in the Transformation Process

5

The World Bank Role in the Transformation Process Coordinating and managing regional

initiatives BCEAO, Central Bank of West Africa and

BEAC Southern African Development Community

(SADC) Western Hemisphere Initiative

Commercial bank operational procedural improvements - MIS, Decision Support, and Products & Services Modernization (India, Vietnam)

6

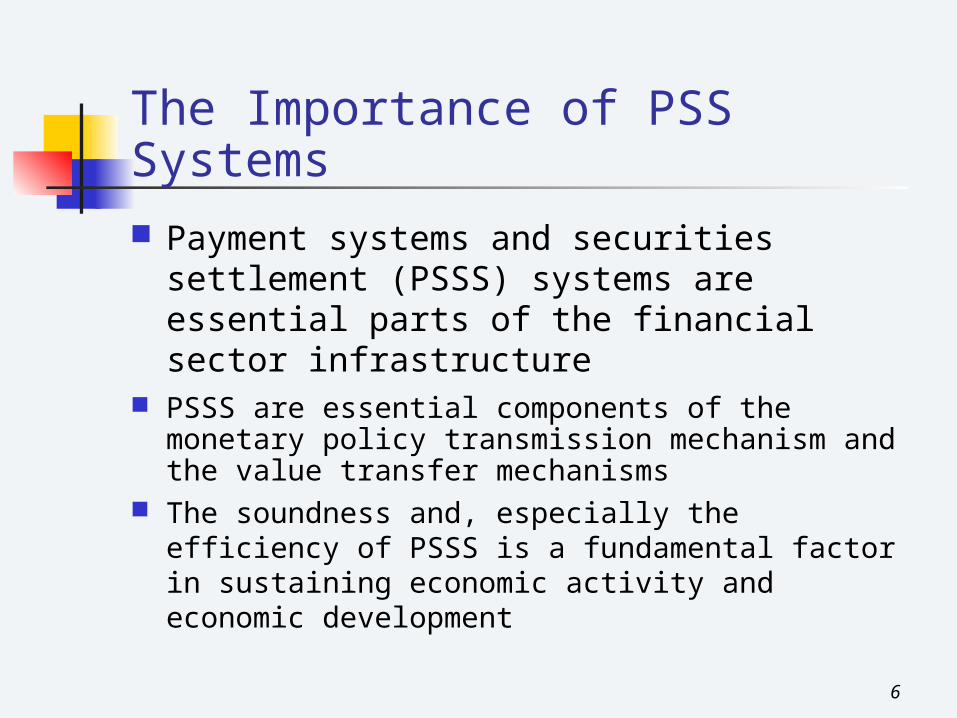

The Importance of PSS Systems Payment systems and securities

settlement (PSSS) systems are essential parts of the financial sector infrastructure

PSSS are essential components of the monetary policy transmission mechanism and the value transfer mechanisms

The soundness and, especially the efficiency of PSSS is a fundamental factor in sustaining economic activity and economic development

7

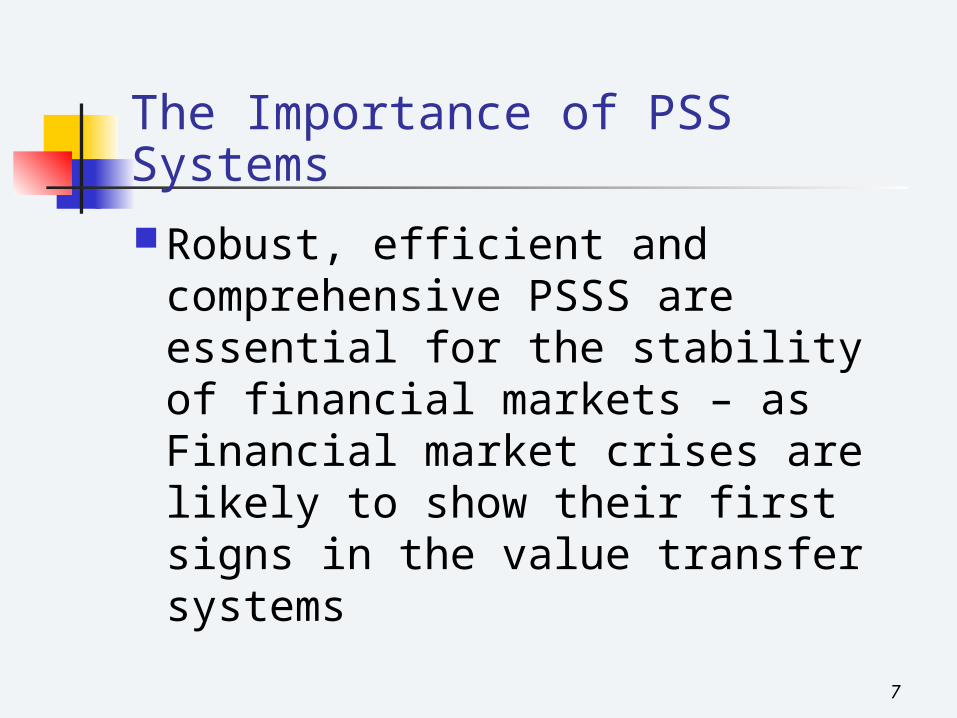

The Importance of PSS Systems

Robust, efficient and comprehensive PSSS are essential for the stability of financial markets – as Financial market crises are likely to show their first signs in the value transfer systems

8

Internationally Accepted Principles & Standards Recognizing this Importance the

Financial Stability Forum, the Standard Setters (E.G. BIS and IOSCO) and the International Financial Institutions (including the IMF and the WB) have pushed for the update and/or release of common international principles, standards and best practices for payments and securities settlement systems - for use in the development and the assessment of such systems

9

Developing the Core Principles The Committee on Payment and

Settlement Systems (CPSS, Bank for International Settlements) has traditionally been the forum to discuss and develop international standards and best practices in the payments arena

In May 1998, the CPSS established a Task Force on Payment System Principles and Practices

10

Developing the Core Principles The TF comprised representatives not

only from G10 CBs and the ECB but also from 11 other CBs of countries in different stages of development, the IMF and the WB

The BIS published a draft of Part I of the report in December 1999 and a draft of Part II in July 2000, for public comments. Final publication of the entire Report occurred in January 2001

11

Developing the Core Principles The TF identified:

Two Public Policy objectives (safety and efficiency) in systemically important payment systems (SIPS)

Ten core principles for SIPS Four central bank’s responsibilities

in applying the core principles

12

Developing the Core Principles A PS is Systemically Important if disruption within

it could trigger or transmit further disruptions amongst participants and ultimately in the entire financial arena

It is likely that a system is a SIPS if at least one of the following is true: It is the only or the main system in the country It handles payments of high individual value It is used for settlement of financial market

transactions or of other important interbank payment systems

13

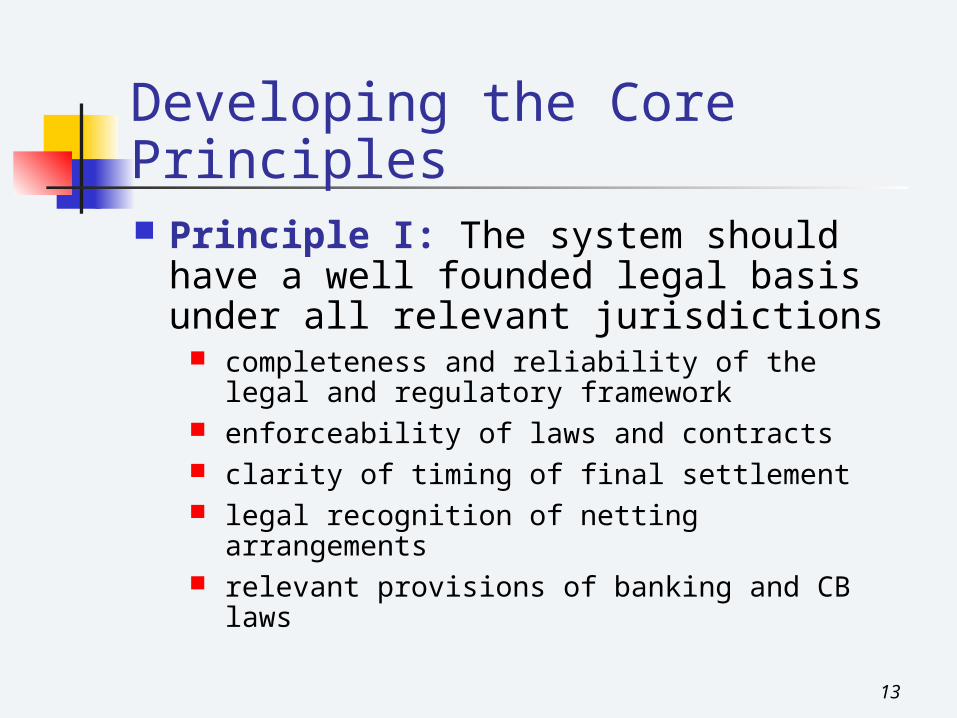

Developing the Core Principles Principle I: The system should

have a well founded legal basis under all relevant jurisdictions

completeness and reliability of the legal and regulatory framework

enforceability of laws and contracts clarity of timing of final settlement legal recognition of netting arrangements relevant provisions of banking and CB

laws

14

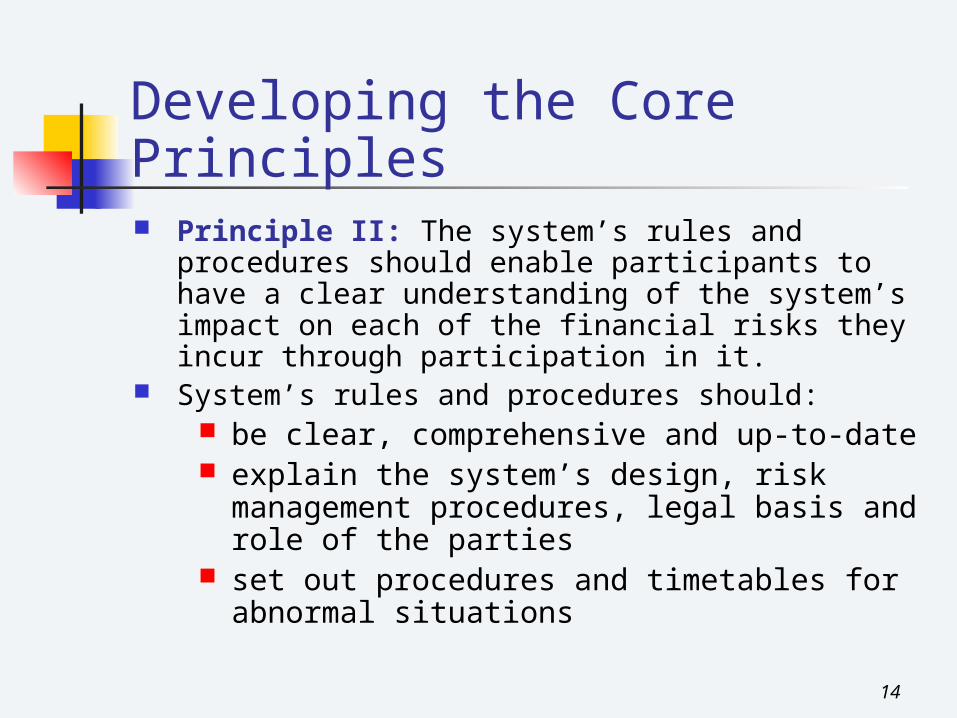

Developing the Core Principles Principle II: The system’s rules and

procedures should enable participants to have a clear understanding of the system’s impact on each of the financial risks they incur through participation in it.

System’s rules and procedures should: be clear, comprehensive and up-to-date explain the system’s design, risk

management procedures, legal basis and role of the parties

set out procedures and timetables for abnormal situations

15

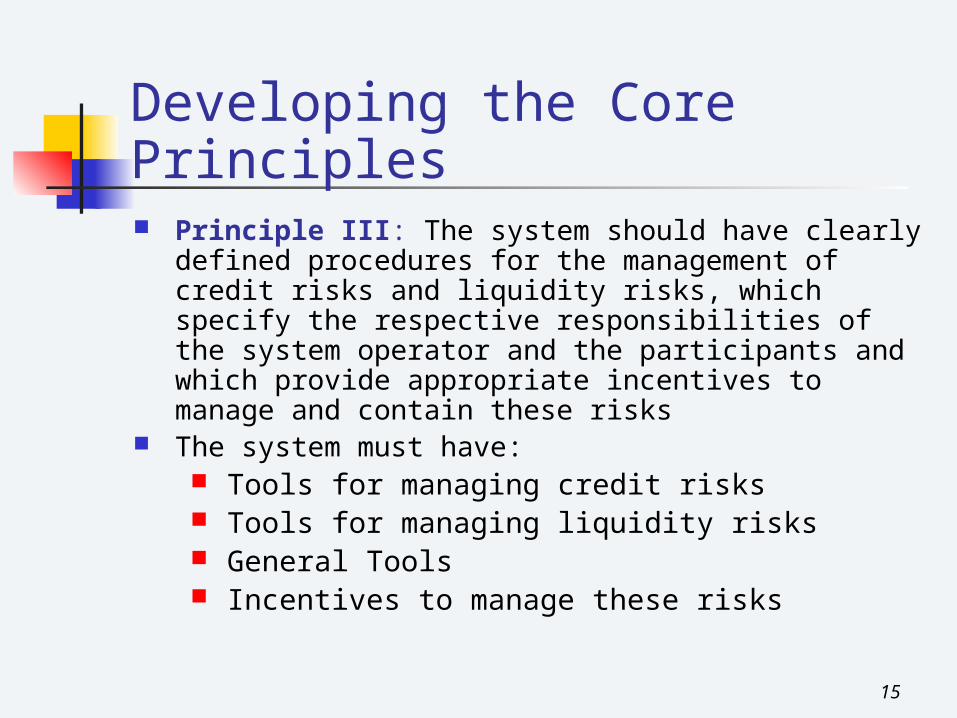

Developing the Core Principles Principle III: The system should have clearly

defined procedures for the management of credit risks and liquidity risks, which specify the respective responsibilities of the system operator and the participants and which provide appropriate incentives to manage and contain these risks

The system must have: Tools for managing credit risks Tools for managing liquidity risks General Tools Incentives to manage these risks

16

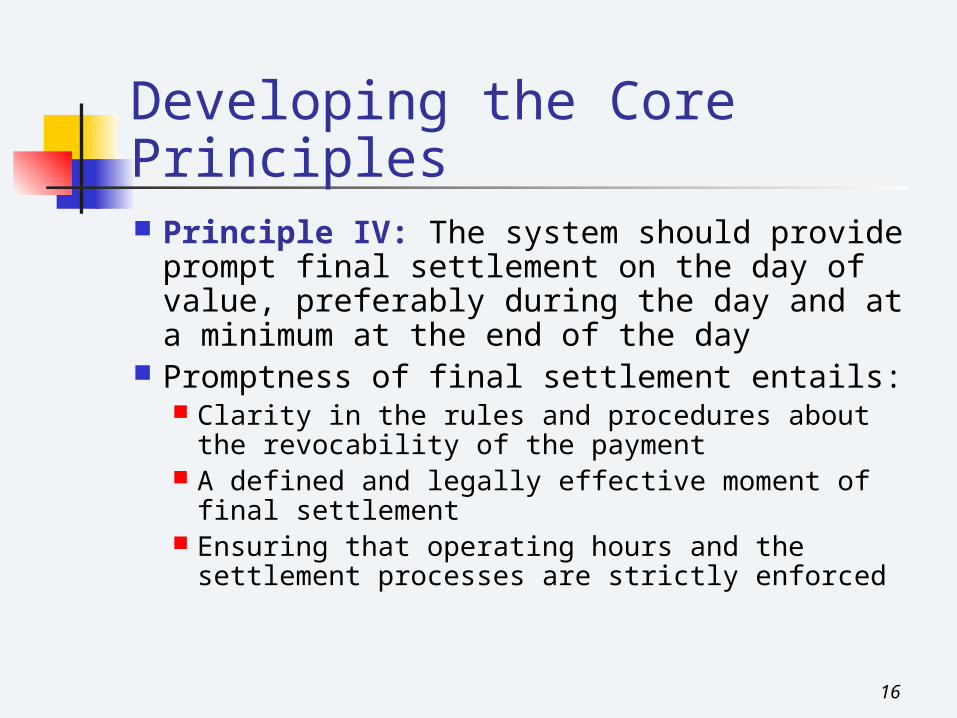

Developing the Core Principles Principle IV: The system should provide

prompt final settlement on the day of value, preferably during the day and at a minimum at the end of the day

Promptness of final settlement entails: Clarity in the rules and procedures about the

revocability of the payment A defined and legally effective moment of final

settlement Ensuring that operating hours and the

settlement processes are strictly enforced

17

Developing the Core Principles Principle V: A system in which multilateral

netting takes place should, at a minimum,be capable of ensuring the timely completion of daily settlements in the event of an inability to settle by the participant with the largest single settlement obligation Additional financial resources must be

available to meet this contingency The amount of these resources must be

determined appropriately Alternatively, other system designs (e.g.

RTGS) must be explored

18

Developing the Core Principles Principle VI: Assets used for settlement should

preferably be a claim on the central bank; where other assets are used, they should carry little or no credit risk and little or no liquidity risk

If assets other than a CB’s claim are used, it should be checked: the creditworthiness of the issuer how readily the asset can be transferred

into others size and duration of exposures of the issuer risk controls, if any

19

Developing the Core Principles Principle VII: The system should

ensure a high degree of security and operational reliability and should have contingency arrangements for timely completion of daily processing

The following issues should be considered: Security Operational reliability Business continuity

20

Developing the Core Principles Principle VIII: The system should provide a

means of making payments which is practical for its users and efficient for the economy

The following issues should be considered: General: Define objectives; Identify user

needs and constraints; Identify system choices and benefits; Determine social and private costs; Develop decision choices

Analytical Framework: Identify efficiency and safety requirements; Evaluate costs; Identify resources; Determine practical and safety constraints

21

Developing the Core Principles Principle VIII: The system should

provide a means of making payments which is practical for its users and efficient for the economy

The following issues should be considered: Methods: Cost-Benefits or other structured

analysis; involvement of participants and/or users in discussions; Methodology for data collection and analysis; Identify data sources

22

Developing the Core Principles Principle IX: The system should have

objective and publicly disclosed criteria for participation, which permit fair and open access

The following issues should be considered: Access criteria should be justified in terms

of both safety and efficiency Exit criteria

23

Developing the Core Principles Principle X: The system’s governance

arrangements should be effective, accountable and transparent Major decisions should be made after

consultation with interested parties The systems consistently attains projected

financial results The system delivers payment services that

satisfy customer needs The system complies with the other 9

principles

24

Developing the Core Principles The Central Bank’s Responsibilities

in Applying the Core principles: A: The Central Bank should define clearly its

payment system objectives and should disclose publicly its role and major policies with respect to systemically important payment systems

B: The Central Bank should ensure that the systems it operates comply with the core principles

25

Developing the Core Principles The Central Bank’s Responsibilities in

Applying the Core principles: C: The Central Bank should oversee compliance

with the Core Principles by systems it does not operate and it should have the ability to carry out this oversight

D: The Central Bank, in promoting payment system safety and efficiency through the Core Principles, should cooperate with other central banks and with any other relevant domestic and foreign authorities

26

The World Bank Role in the Implementation of the Core Principles

We have always used international standards and best practices (e.g., Lamfalussy, other BIS reports, G-30 recommendations) in our assessments and payments system design activities

We consistently supported the need for internationally recognized principles for payment systems

The Importance of International Standards and Best Practices

27

The World Bank Role in the Implementation of the Core Principles

We were pleased with the methodology used to develop the CPSS core principles, namely the involvement of the IMF/WB and of representatives from emerging markets

We participated enthusiastically in the works of the Task Force

The Importance of International Standards and Best Practices

28

The World Bank Role in the Implementation of the Core Principles

In the payment system component of the Financial Sector Assessment Program (FSAP): The IMF/WB joint effort to assess the

vulnerability of the financial sector. The FSAP normally includes a formal

assessment of the standards and codes indicated by the Financial Stability Forum (ROSC).

Applying the core principles

29

The World Bank Role in the Implementation of the Core Principles

We have teamed up with Fund Colleagues and consulted the CPSS to prepare a uniform approach in assessing the CPSIPS in the context of the FSAP.

The Guidance Note, Questionnaire and Assessment Templates are now available and are being used since August 2001.

Applying the core principles

30

The World Bank Role in the Implementation of the Core Principles

We conducted a comprehensive evaluation of past FSAP experience to draw lessons for the future and improve the process (Paris Outreach in November 2001 and possible joint Outreach with the CPSS in late 2002).

Applying the core principles

31

The World Bank Role in the Implementation of the Core Principles

In our technical assistance missions

In our technical loans (we encourage our borrowers to use the principles)

In Regional Initiatives

Applying the core principles

32

Definition of SSS The SSS include the full set of

institutional arrangements for confirmation, clearance and settlement of securities trades and safekeeping of securities

Weaknesses in SSSs can be a source of inefficiency: Impede capital formation due to

higher costs

33

Definition of SSS Weaknesses in SSSs can be a

source of systemic disturbances due to:

Creation of liquidity pressures Potential relevant credit losses Potential spillover effects to

payment systems Uncertainty on who bears risks

34

International Standards for SSS

1989: G30 Recommendations 1990: IOSCO C&S Blueprint 1991: OECD Systemic Risks in Sec. Mkts 1992: BIS - CPSS DVP Report 1992: IOSCO Blueprint for Emerging Mkts 1995: BIS Cross Border Sec. Settlements 1996: FIBV Best Practices 1996: COSRA Principles 1997: CPSS/IOSCO Disclosure Framework

Evolution of Standards for SSS

35

International Standards for SSS

1997: IOSCO Legal Framework for SSS 1998: IOSCO Principles of Securities

Regulation 1999: FIBV Best Practices 2000: ISSA Recommendations 2000: ACSDA Identification of Risks 2001: CPSS/IOSCO Recommendations 2001-02: New G-30 Projects

Evolution of Standards for SSS

36

International Standards for SSS

1998-99: ESCB requisites for the use of securities as collateral in TARGET

2001: World Bank Guide to Best Practices

2001: Evolution of Securities Markets and Infrastructure in Europe (Committee of Wise Men, Giovannini Group, etc.)

Evolution of Standards for SSS (other references)

37

International Standards for SSS In December 1999 CPSS and

IOSCO established a Joint Task Force to set up recommendations for sound and efficient securities settlement systems.

The recommendations were released for public comments in January 2001 and in their final version in November 2001

38

International Standards for SSS The CPSS and IOSCO have

directed the Task Force to complete by the end of 2002 a methodology for assessing the implementation of the recommendations

The World Bank and the IMF are participating actively in this work

39

International Standards for SSS Key Public Policy Objectives for SSS

Reduction of Systemic Risks Protection of Investor Assets Efficiency To Guarantee Well Functioning Financial

Markets and Efficient Capital Formation

40

International Standards for SSS

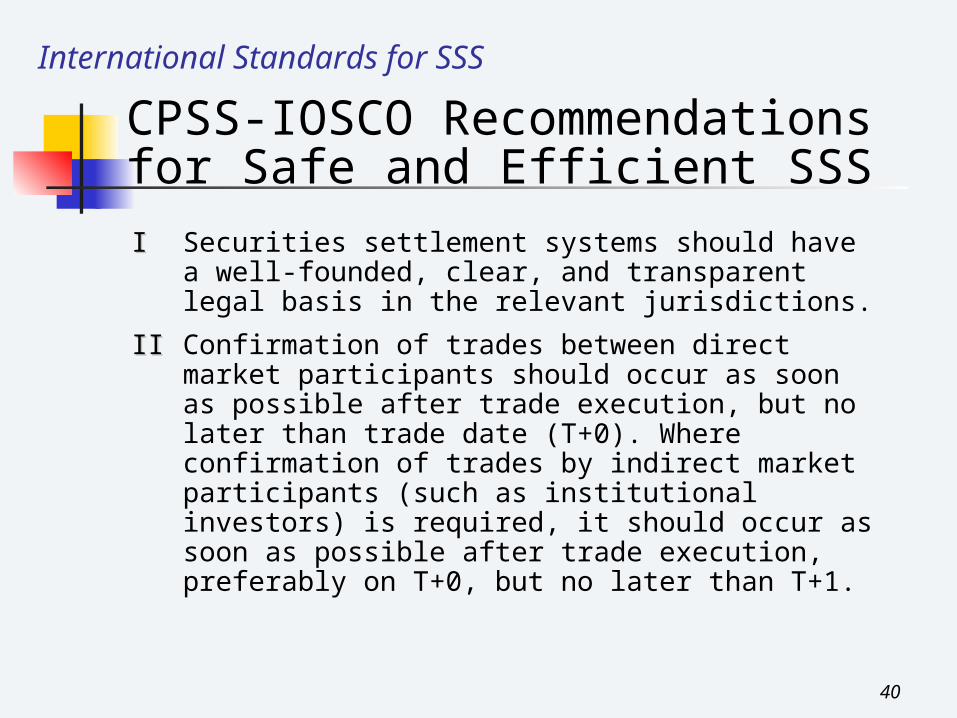

I I Securities settlement systems should have a well-founded, clear, and transparent legal basis in the relevant jurisdictions.

II II Confirmation of trades between direct market participants should occur as soon as possible after trade execution, but no later than trade date (T+0). Where confirmation of trades by indirect market participants (such as institutional investors) is required, it should occur as soon as possible after trade execution, preferably on T+0, but no later than T+1.

CPSS-IOSCO Recommendations for Safe and Efficient SSS

41

International Standards for SSS

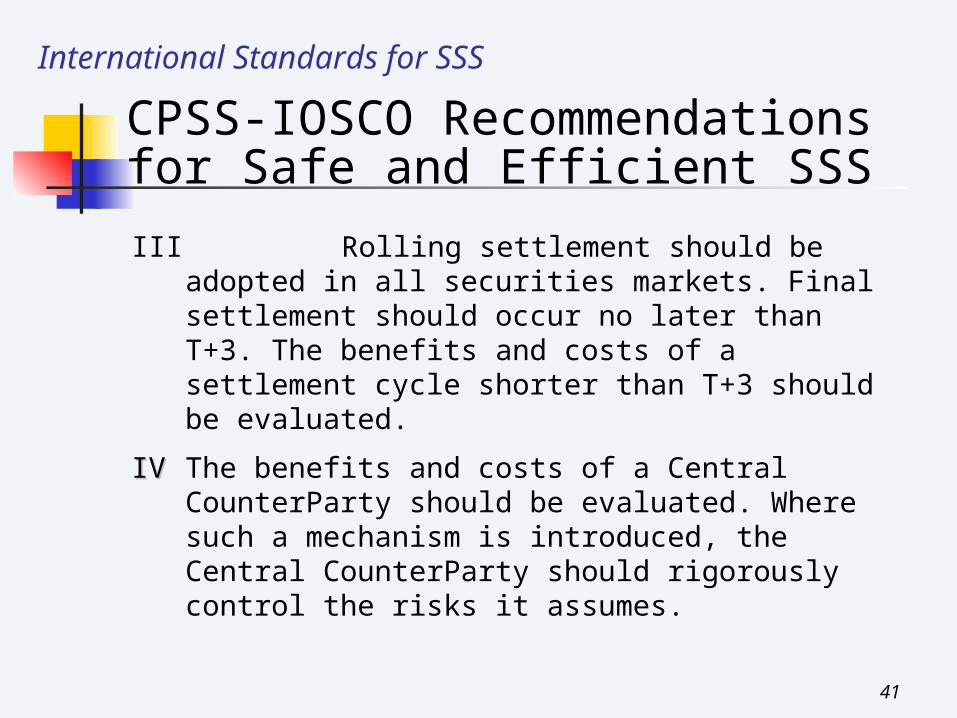

III Rolling settlement should be adopted in all securities markets. Final settlement should occur no later than T+3. The benefits and costs of a settlement cycle shorter than T+3 should be evaluated.

IV IV The benefits and costs of a Central CounterParty should be evaluated. Where such a mechanism is introduced, the Central CounterParty should rigorously control the risks it assumes.

CPSS-IOSCO Recommendations for Safe and Efficient SSS

42

International Standards for SSS

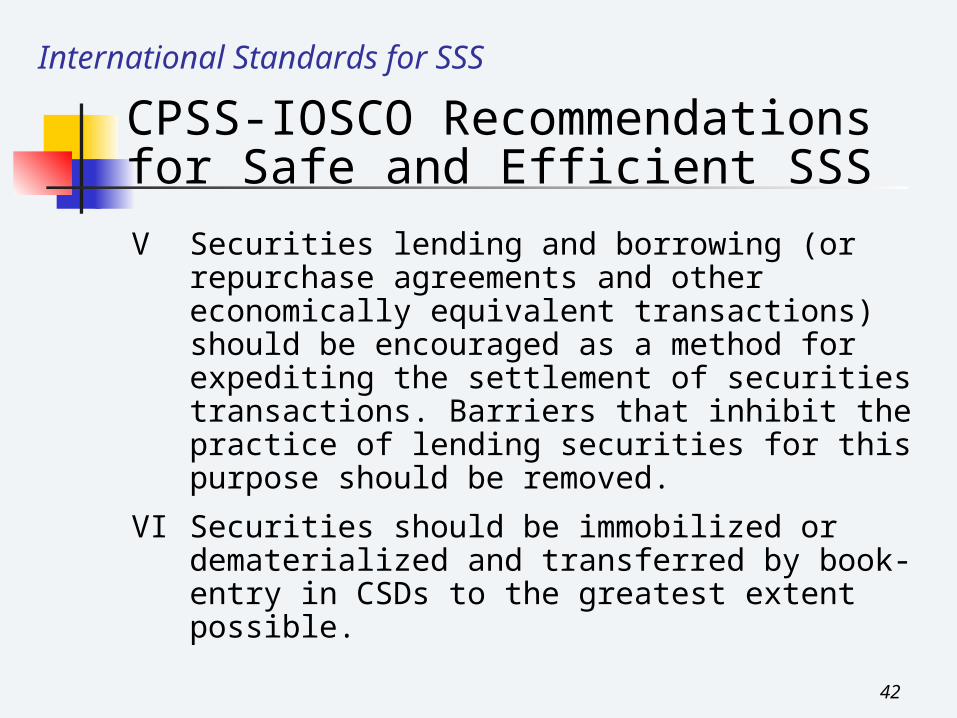

V Securities lending and borrowing (or repurchase agreements and other economically equivalent transactions) should be encouraged as a method for expediting the settlement of securities transactions. Barriers that inhibit the practice of lending securities for this purpose should be removed.

VI Securities should be immobilized or dematerialized and transferred by book-entry in CSDs to the greatest extent possible.

CPSS-IOSCO Recommendations for Safe and Efficient SSS

43

International Standards for SSS

VIIVII CSDs should eliminate principal risk by linking securities transfers to funds transfers in a way that achieves delivery-versus-payment (DvP).

VIII Final settlement should occur no later than the end of the settlement day. Intraday or real-time finality should be provided where necessary to reduce risks.

CPSS-IOSCO Recommendations for Safe and Efficient SSS

44

International Standards for SSS

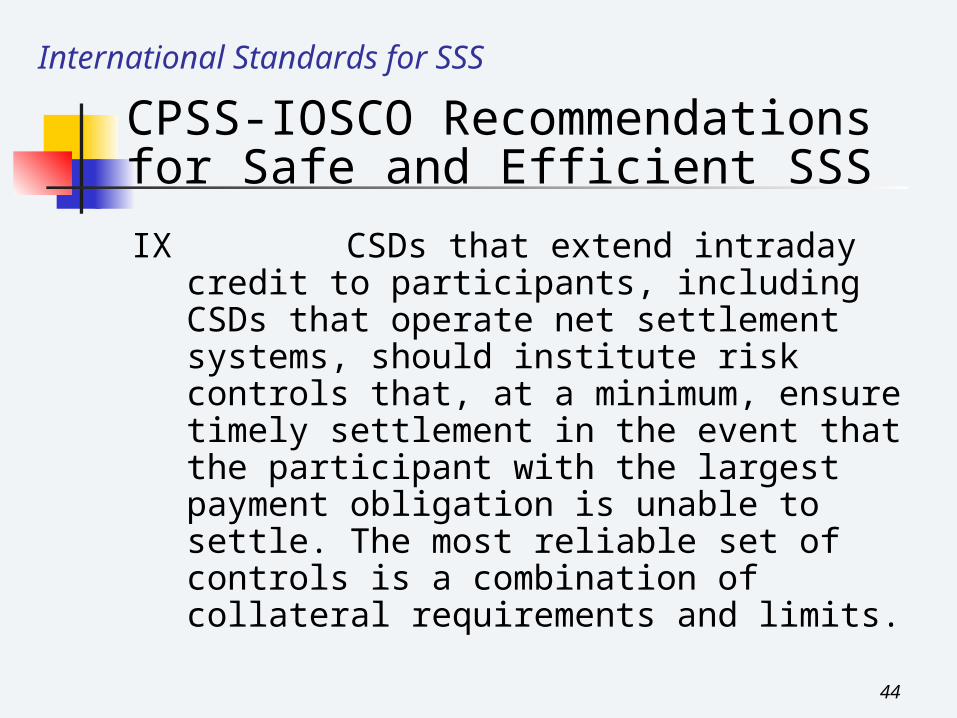

IX CSDs that extend intraday credit to participants, including CSDs that operate net settlement systems, should institute risk controls that, at a minimum, ensure timely settlement in the event that the participant with the largest payment obligation is unable to settle. The most reliable set of controls is a combination of collateral requirements and limits.

CPSS-IOSCO Recommendations for Safe and Efficient SSS

45

International Standards for SSS

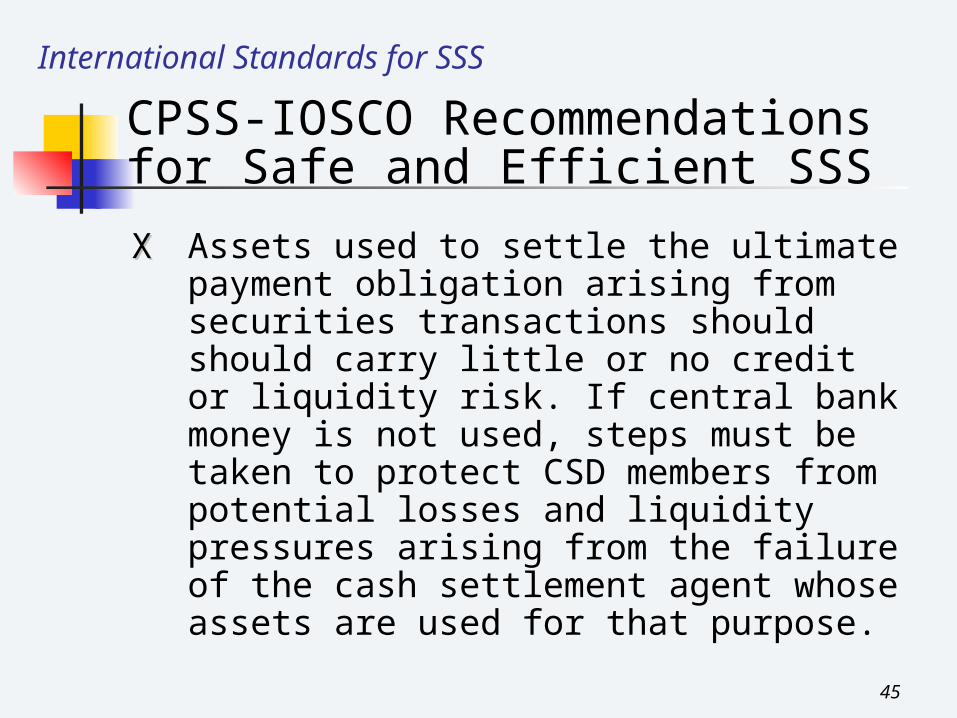

X X Assets used to settle the ultimate payment obligation arising from securities transactions should should carry little or no credit or liquidity risk. If central bank money is not used, steps must be taken to protect CSD members from potential losses and liquidity pressures arising from the failure of the cash settlement agent whose assets are used for that purpose.

CPSS-IOSCO Recommendations for Safe and Efficient SSS

46

International Standards for SSS

XI Sources of operational risk arising in the clearing and settlement process should be identified and minimized through the development of appropriate systems, controls, and procedures. Systems should be reliable and secure, and have adequate, scaleable capacity. Contingency plans and backup facilities should be established to allow for timely recovery of operations and completion of the settlement process.

CPSS-IOSCO Recommendations for Safe and Efficient SSS

47

International Standards for SSS

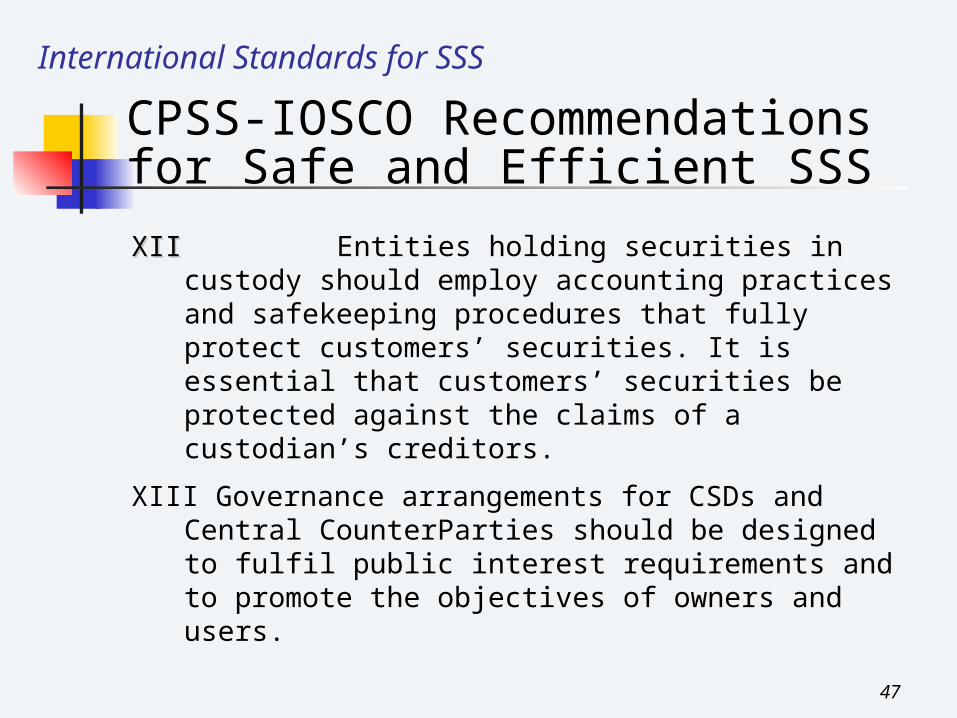

XII XII Entities holding securities in custody should employ accounting practices and safekeeping procedures that fully protect customers’ securities. It is essential that customers’ securities be protected against the claims of a custodian’s creditors.

XIII Governance arrangements for CSDs and Central CounterParties should be designed to fulfil public interest requirements and to promote the objectives of owners and users.

CPSS-IOSCO Recommendations for Safe and Efficient SSS

48

International Standards for SSS

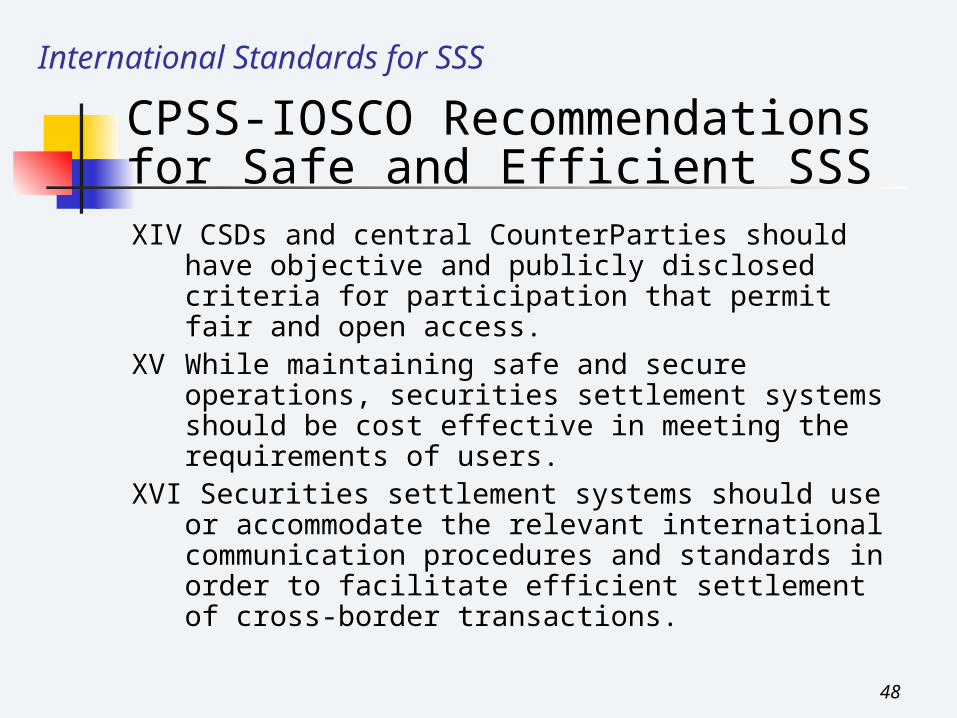

XIV CSDs and central CounterParties should have objective and publicly disclosed criteria for participation that permit fair and open access.

XV While maintaining safe and secure operations, securities settlement systems should be cost effective in meeting the requirements of users.

XVI Securities settlement systems should use or accommodate the relevant international communication procedures and standards in order to facilitate efficient settlement of cross-border transactions.

CPSS-IOSCO Recommendations for Safe and Efficient SSS

49

International Standards for SSS

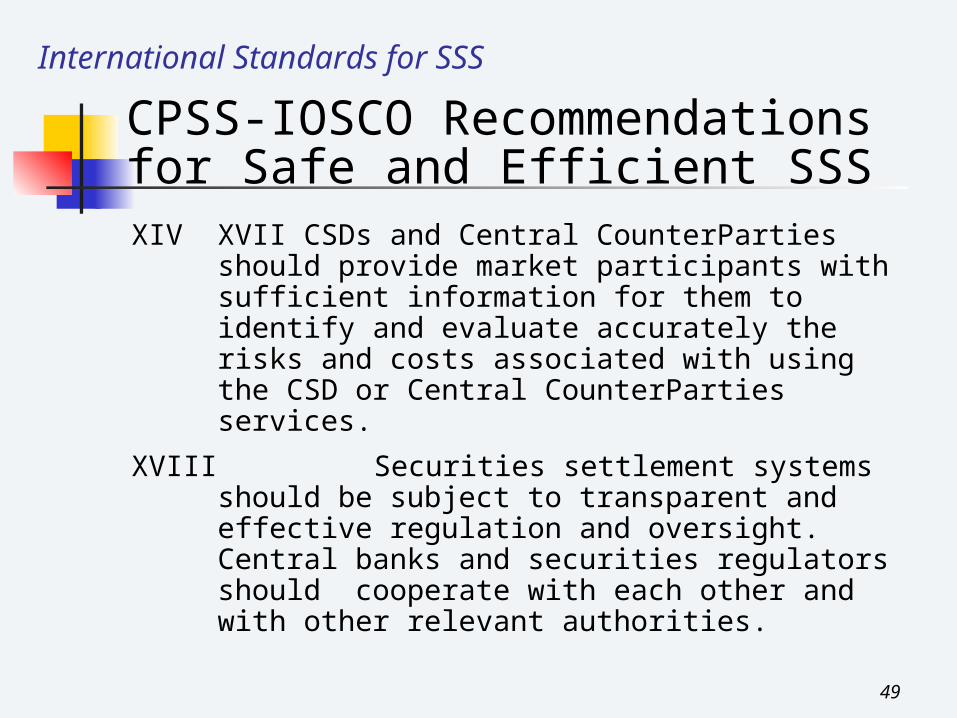

XIV XVII CSDs and Central CounterParties should provide market participants with sufficient information for them to identify and evaluate accurately the risks and costs associated with using the CSD or Central CounterParties services.

XVIII Securities settlement systems should be subject to transparent and effective regulation and oversight. Central banks and securities regulators should cooperate with each other and with other relevant authorities.

CPSS-IOSCO Recommendations for Safe and Efficient SSS

50

International Standards for SSS

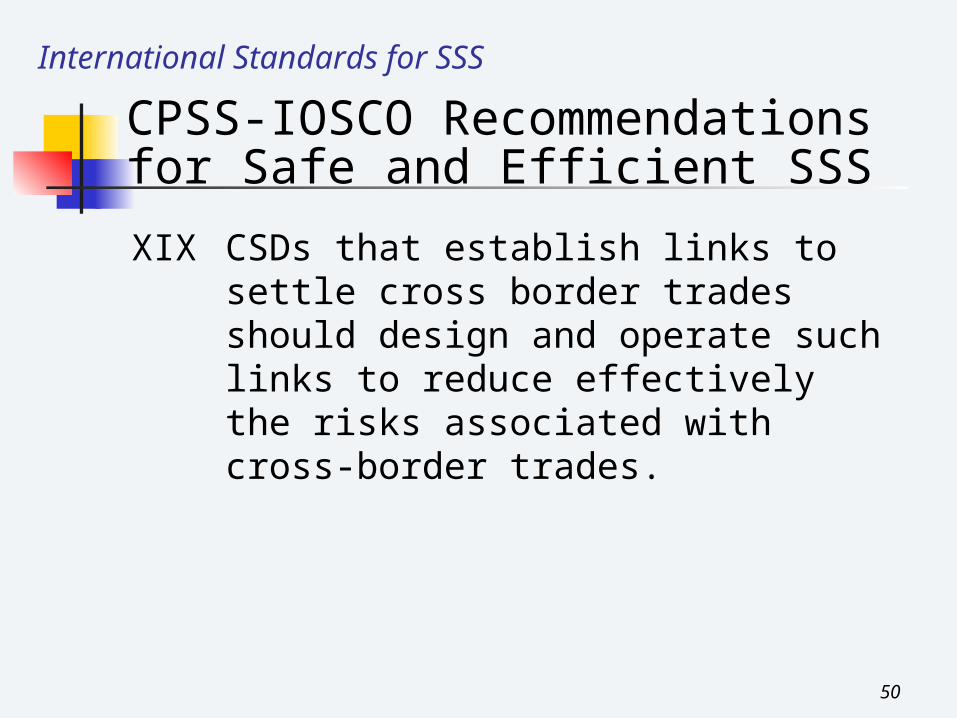

XIX CSDs that establish links to settle cross border trades should design and operate such links to reduce effectively the risks associated with cross-border trades.

CPSS-IOSCO Recommendations for Safe and Efficient SSS

51

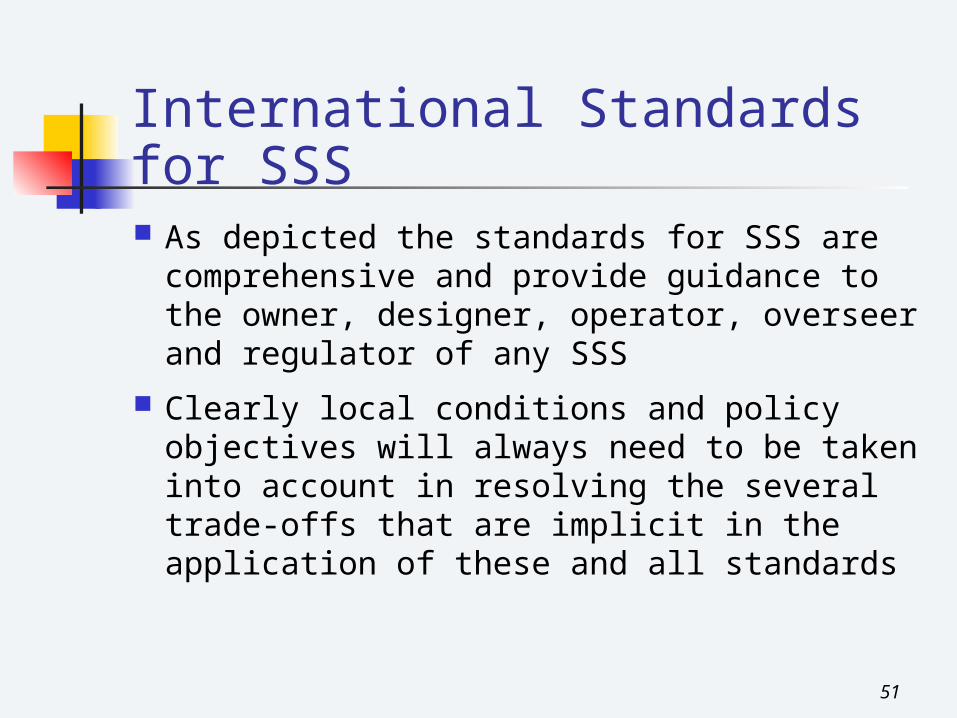

International Standards for SSS As depicted the standards for SSS are

comprehensive and provide guidance to the owner, designer, operator, overseer and regulator of any SSS

Clearly local conditions and policy objectives will always need to be taken into account in resolving the several trade-offs that are implicit in the application of these and all standards

52

The World Bank Role in the Implementation of the SSS

Recommendations: We will continue to participate in the work of

the Task Force in producing the assessment methodology

We, as an institution, have confirmed our belief that the SSS recommendations should be included in the international list of standards and codes

We also support the emerging belief that payments and securities settlement systems should be viewed as parts of a common integrated value transfer system and assessed together in the context of FSAPs and other ESW.

53

WWW.IPHO-WHPI.ORG

CASE STUDYThe Western Hemisphere Payments & Securities Clearance and Settlement Initiative

54

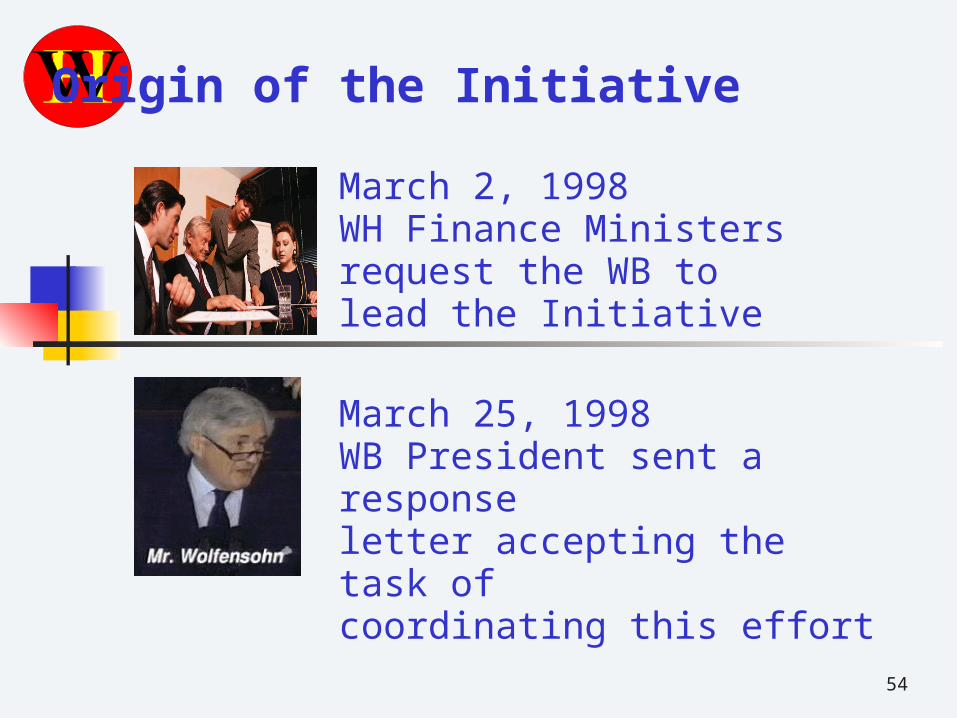

Origin of the Initiative

March 2, 1998WH Finance Ministersrequest the WB to lead the Initiative

March 25, 1998WB President sent a responseletter accepting the task of coordinating this effort

55

OBJECTIVE: Assessing and recommending improvements to

payments and securities settlement systems in the Hemisphere

Pillars of the Strategy

Integration ofIntegration ofsecurities andsecurities and

paymentspayments

Integration ofIntegration ofsecurities andsecurities and

paymentspayments

Cooperation Cooperation withwith

internationalinternationalorganizationsorganizations

Cooperation Cooperation withwith

internationalinternationalorganizationsorganizations

CountryCountryOwnershipOwnershipCountryCountry

OwnershipOwnership

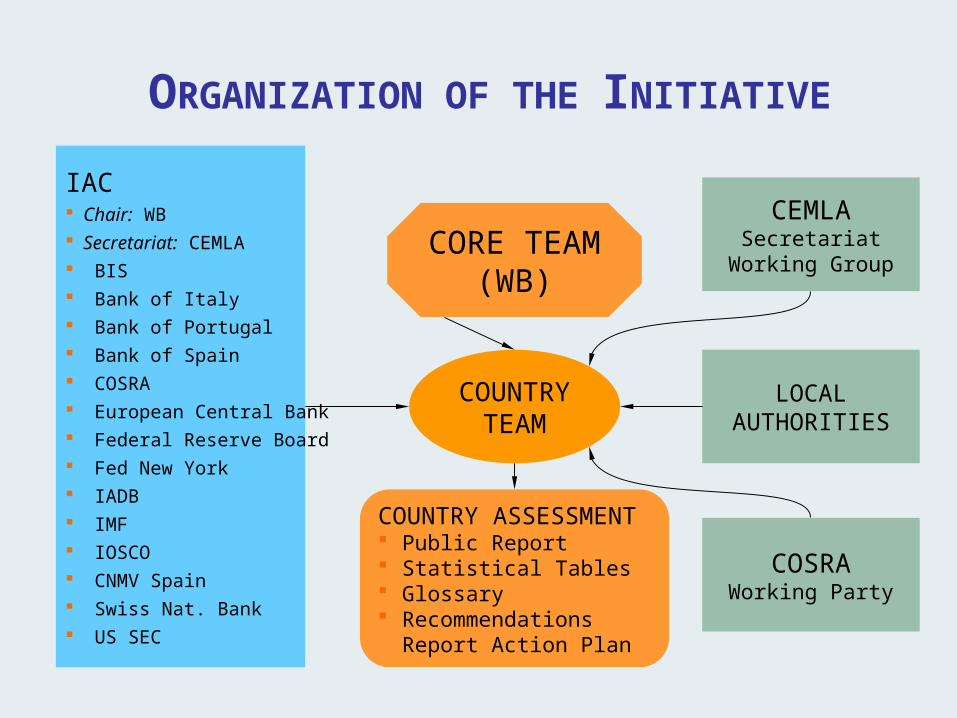

ORGANIZATION OF THE INITIATIVE

IAC Chair: WB Secretariat: CEMLA BIS Bank of Italy Bank of Portugal Bank of Spain COSRA European Central Bank Federal Reserve Board Fed New York IADB IMF IOSCO CNMV Spain Swiss Nat. Bank US SEC

CEMLASecretariat

Working Group

COUNTRYTEAM

COUNTRY ASSESSMENT Public Report Statistical Tables Glossary Recommendations

Report Action Plan

LOCALAUTHORITIES

COSRAWorking Party

CORE TEAM(WB)

57

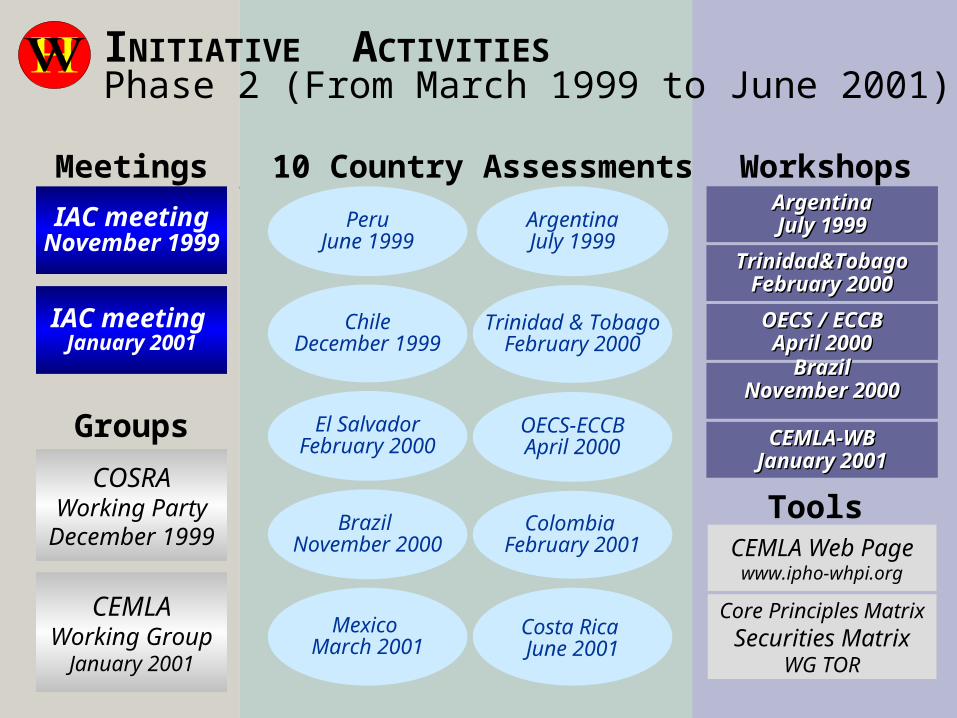

CEMLA-WBCEMLA-WBJanuary 2001January 2001

Phase 2 (From March 1999 to June 2001)

ChileDecember 1999

ArgentinaJuly 1999

PeruJune 1999

Trinidad & TobagoFebruary 2000

10 Country AssessmentsArgentinaArgentinaJuly 1999July 1999

INITIATIVE ACTIVITIES

El SalvadorFebruary 2000

Costa Rica June 2001

OECS-ECCBApril 2000

Colombia February 2001

Brazil November 2000

Mexico March 2001

IAC meetingNovember 1999

Meetings Workshops

IAC meeting January 2001

Groups

COSRAWorking Party

December 1999

CEMLAWorking Group

January 2001

CEMLA Web Pagewww.ipho-whpi.org

Tools

Core Principles MatrixSecurities Matrix

WG TOR

Trinidad&TobagoTrinidad&TobagoFebruary 2000February 2000

OECS / ECCBOECS / ECCBApril 2000April 2000

BrazilBrazilNovember 2000November 2000

58

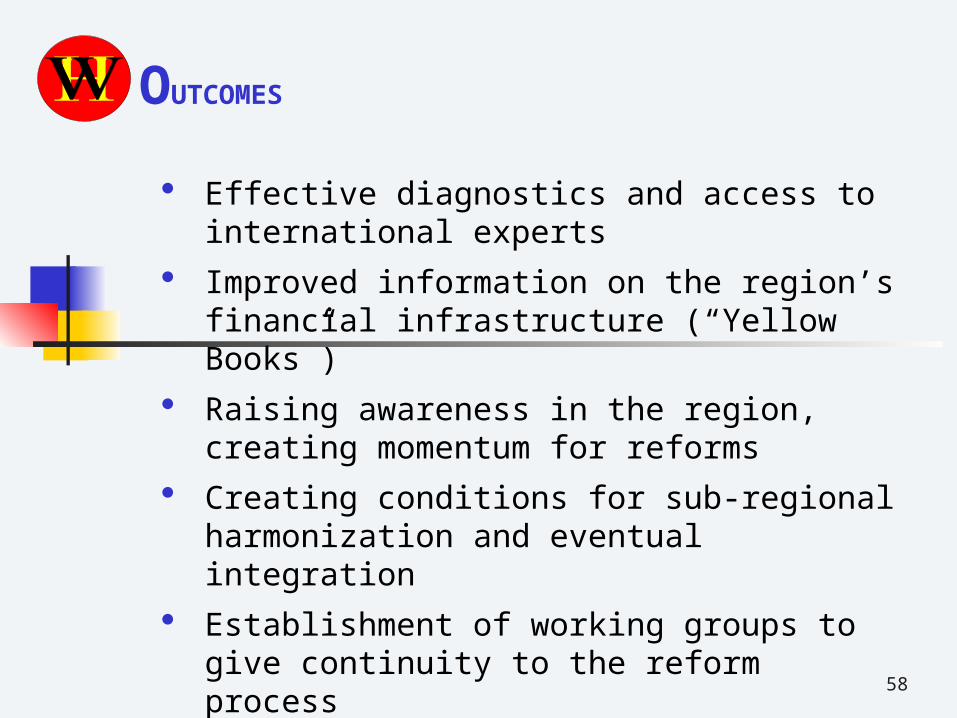

OUTCOMES

Effective diagnostics and access to international experts

Improved information on the region’s financial infrastructure (“Yellow Books”)

Raising awareness in the region, creating momentum for reforms

Creating conditions for sub-regional harmonization and eventual integration

Establishment of working groups to give continuity to the reform process

59

OOUTCOMESUTCOMES

Effective diagnostics and access to international experts

Strengthening of CEMLA’s in-house expertise

Development of specific country-studies tools based on international standards.

Demand from additional countries for assessment.