1 1 privatization update: gencos and transco january 2005 presentation to ledac

TRANSCRIPT

1111

Privatization Update:Privatization Update:

GENCOS and TRANSCOGENCOS and TRANSCO

January 2005

Presentation to LEDAC

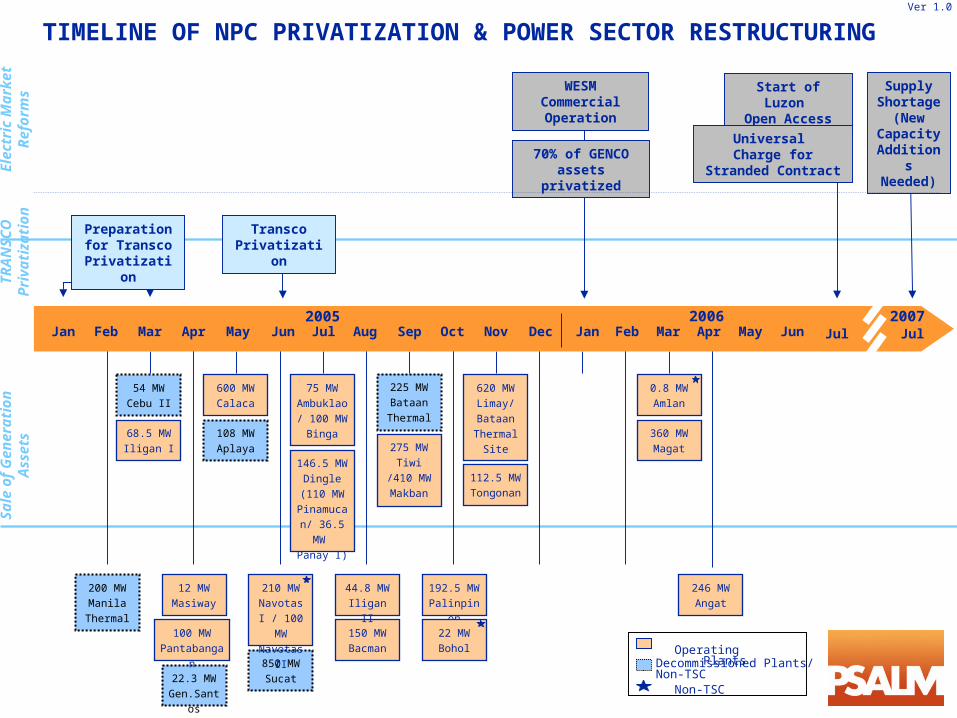

Feb OctJul Aug Sep Nov DecJan Mar Apr May Jun

12 MW Masiway

150 MW Bacman

192.5 MW Palinpinon

75 MW Ambuklao / 100 MW

Binga

112.5 MW Tongonan

275 MW Tiwi /410

MW Makban

600 MW Calaca

44.8 MW Iligan II

146.5 MW Dingle

(110 MW Pinamuca

n/ 36.5 MW

Panay I)

2005

850 MW Sucat

620 MW Limay/ Bataan Thermal

Site

210 MW Navotas I / 100

MW Navotas II

108 MW Aplaya

22.3 MW Gen.Santo

s

54 MW Cebu II

225 MW Bataan Thermal

200 MW Manila

Thermal22 MW Bohol

FebJan Mar Apr

360 MW Magat

0.8 MW Amlan

2006

246 MW Angat

100 MW Pantabanga

n

68.5 MW Iligan I

Operating Plants

Non-TSC

Decommissioned Plants/Non-TSC

Preparation for Transco Privatizatio

n

70% of GENCO assets

privatized

WESM Commercial Operation

Start of Luzon Open Access

Universal Charge for

Stranded Contract

Jul Jul

Supply Shortage (New Capacit

y Addition

s Needed)

2007May Jun

Transco Privatizatio

n

Sale

of

Gen

era

tion

A

ssets

TR

AN

SC

OP

rivati

zati

on

Ele

ctr

ic M

ark

et

Refo

rms

TIMELINE OF NPC PRIVATIZATION & POWER SECTOR RESTRUCTURING Ver 1.0

3333

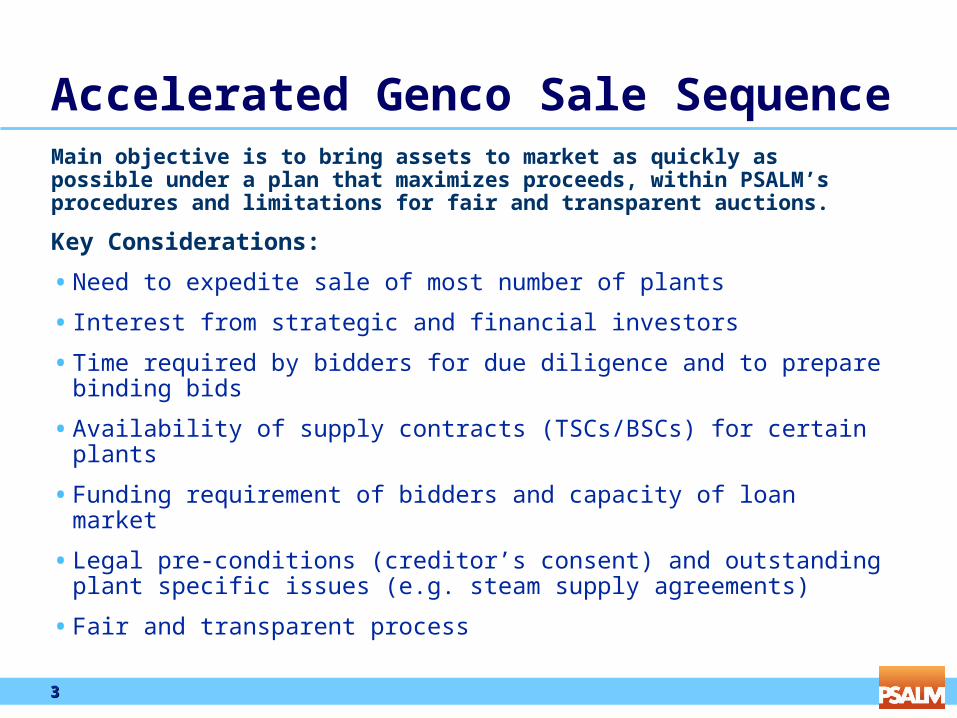

Accelerated Genco Sale Sequence Main objective is to bring assets to market as quickly as possible under a plan that maximizes proceeds, within PSALM’s procedures and limitations for fair and transparent auctions.

Key Considerations:

• Need to expedite sale of most number of plants

• Interest from strategic and financial investors

• Time required by bidders for due diligence and to prepare binding bids

• Availability of supply contracts (TSCs/BSCs) for certain plants

• Funding requirement of bidders and capacity of loan market

• Legal pre-conditions (creditor’s consent) and outstanding plant specific issues (e.g. steam supply agreements)

• Fair and transparent process

4444

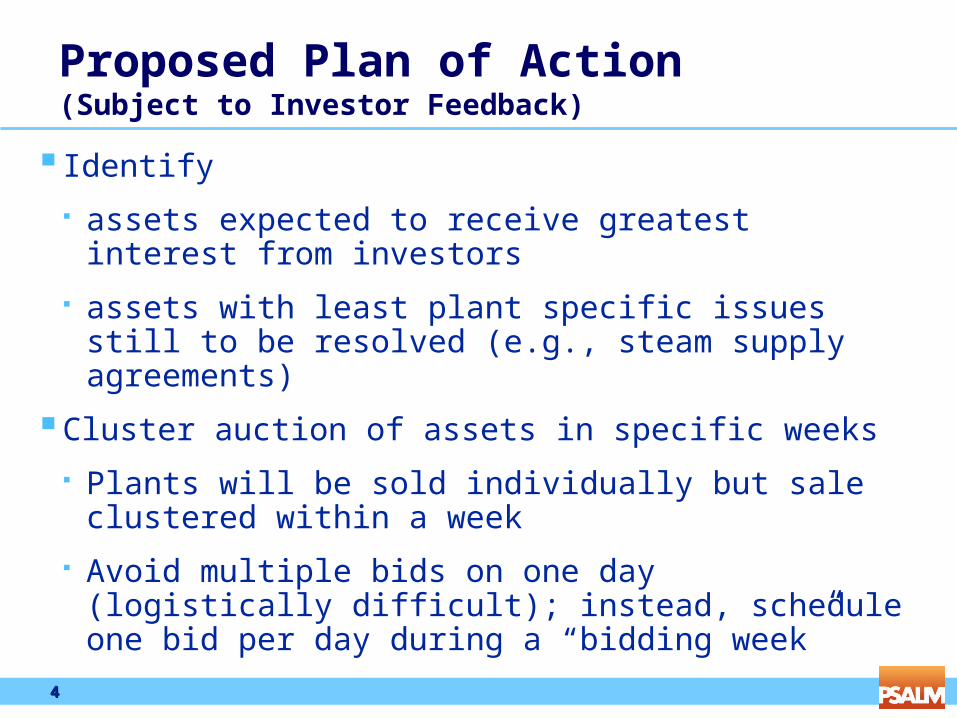

Proposed Plan of Action(Subject to Investor Feedback)

Identify

assets expected to receive greatest interest from investors

assets with least plant specific issues still to be resolved (e.g., steam supply agreements)

Cluster auction of assets in specific weeks

Plants will be sold individually but sale clustered within a week

Avoid multiple bids on one day (logistically difficult); instead, schedule one bid per day during a “bidding week”

5555

Proposed Plan of Action(Subject to Investor Feedback)

Fast-track negotiations of supply contracts (TSCs/BSCs) with distributors (especially Meralco). Assignment of TSCs to certain plants will make it easier for investors to finance acquisition of such assets

Offer bid financing (deferred payments with interest) for certain large plants to make them more affordable to investors, and maximize proceeds to government

6666

Bid Financing (Deferred payments)

• Allows for an accelerated sale process which would not be possible if bidders need to obtain financing (can take months to arrange particularly given the limited capacity of the Philippine lending market)

• Further, the closing process can take considerable time due to lender requirements - the deferred payment mechanism could significantly reduce the closing period

Deferred Payment Structure & Terms

• Allows refinancing.

• Equal semi-annual payments to encourage refinancing.

• Capture greater cash proceeds upfront by increasing down payment from 40% upfront to 50%.

• Bidders will retain the flexibility to prepay if they are able to source cheaper external financing at a later date

7777

Bid Financing (Deferred payments)

Factors Considered in Determining Deferred Payment Terms for each Asset

Size (MW)

• Offer financing for large plants (threshold set at > 150MW)

Remaining Life

• Tenor stepped up according to remaining life of plants.

TSCs

• Preference for financing given to plants to be sold without TSCs - also consider offering financing for non-TSC plants in the <150 MW category

Masinloc Case StudyMasinloc Case Study

9999

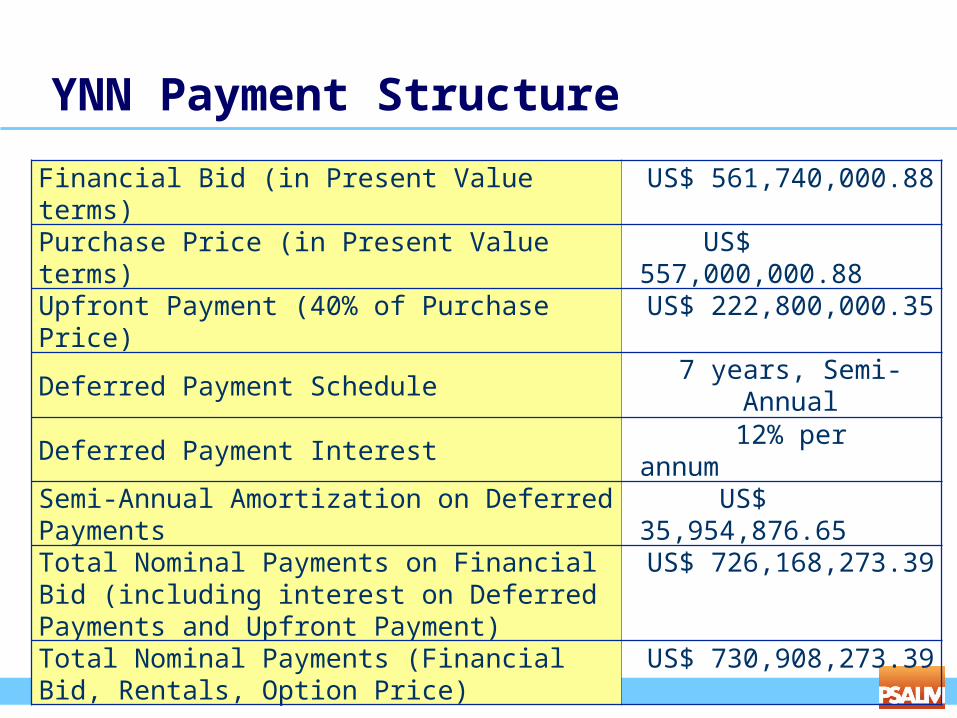

YNN Payment Structure

Financial Bid (in Present Value terms) US$ 561,740,000.88

Purchase Price (in Present Value terms) US$ 557,000,000.88

Upfront Payment (40% of Purchase Price) US$ 222,800,000.35

Deferred Payment Schedule7 years, Semi-Annual

Deferred Payment Interest 12% per annum

Semi-Annual Amortization on Deferred Payments US$ 35,954,876.65

Total Nominal Payments on Financial Bid (including interest on Deferred Payments and Upfront Payment)

US$ 726,168,273.39

Total Nominal Payments (Financial Bid, Rentals, Option Price)

US$ 730,908,273.39

10101010

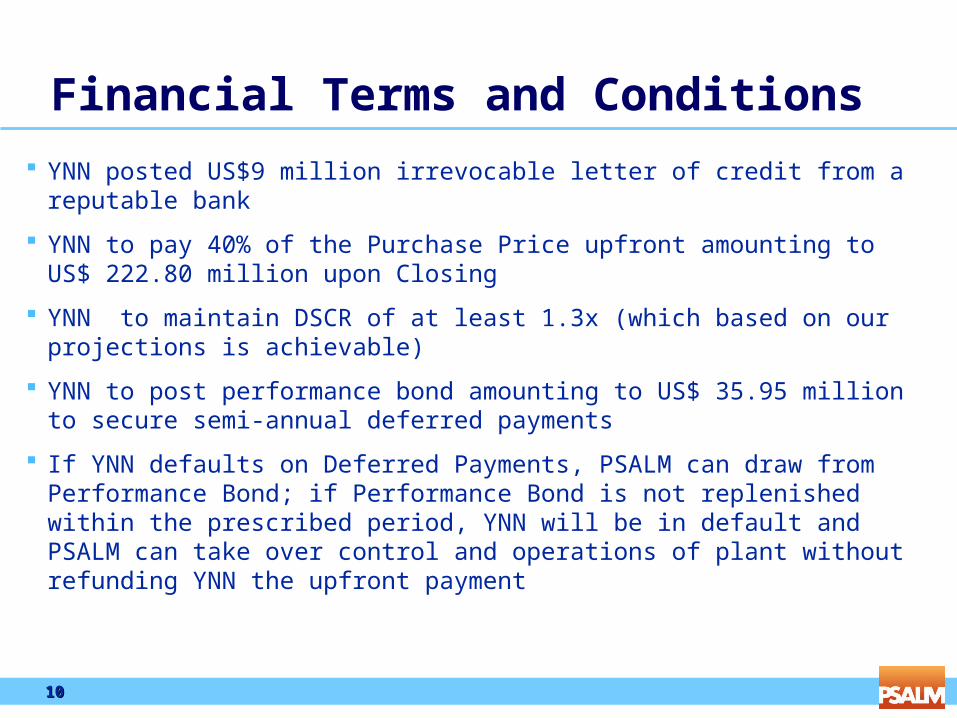

Financial Terms and Conditions

YNN posted US$9 million irrevocable letter of credit from a reputable bank

YNN to pay 40% of the Purchase Price upfront amounting to US$ 222.80 million upon Closing

YNN to maintain DSCR of at least 1.3x (which based on our projections is achievable)

YNN to post performance bond amounting to US$ 35.95 million to secure semi-annual deferred payments

If YNN defaults on Deferred Payments, PSALM can draw from Performance Bond; if Performance Bond is not replenished within the prescribed period, YNN will be in default and PSALM can take over control and operations of plant without refunding YNN the upfront payment

11111111

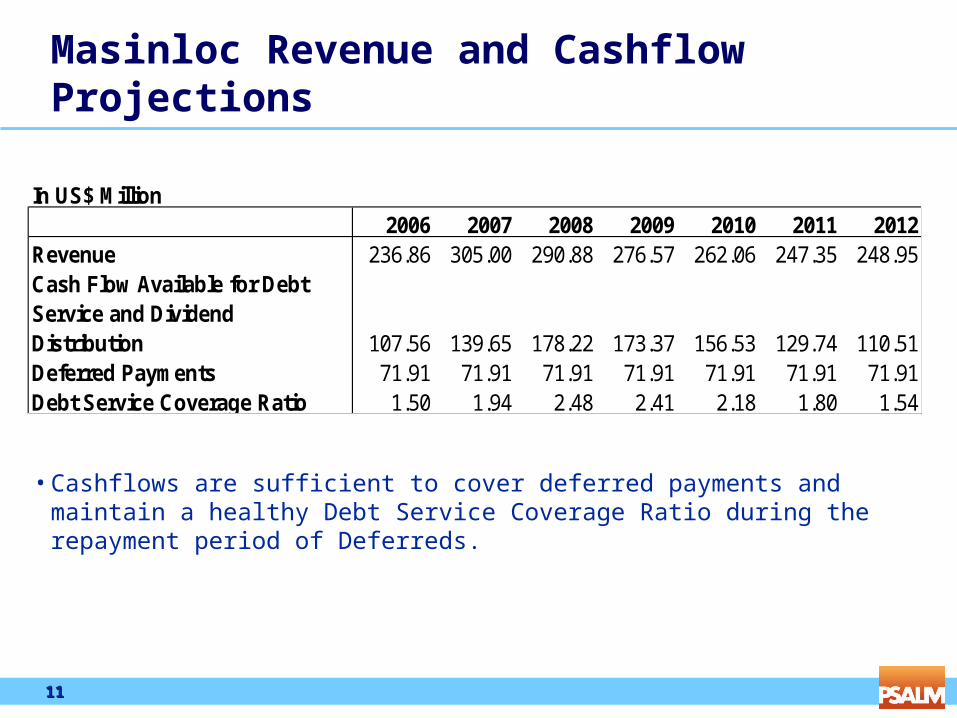

Masinloc Revenue and Cashflow Projections

• Cashflows are sufficient to cover deferred payments and maintain a healthy Debt Service Coverage Ratio during the repayment period of Deferreds.

In US$ Million 2006 2007 2008 2009 2010 2011 2012

Revenue 236.86 305.00 290.88 276.57 262.06 247.35 248.95Cash Flow Available for Debt Service and Dividend Distribution 107.56 139.65 178.22 173.37 156.53 129.74 110.51Deferred Payments 71.91 71.91 71.91 71.91 71.91 71.91 71.91Debt Service Coverage Ratio 1.50 1.94 2.48 2.41 2.18 1.80 1.54

12121212

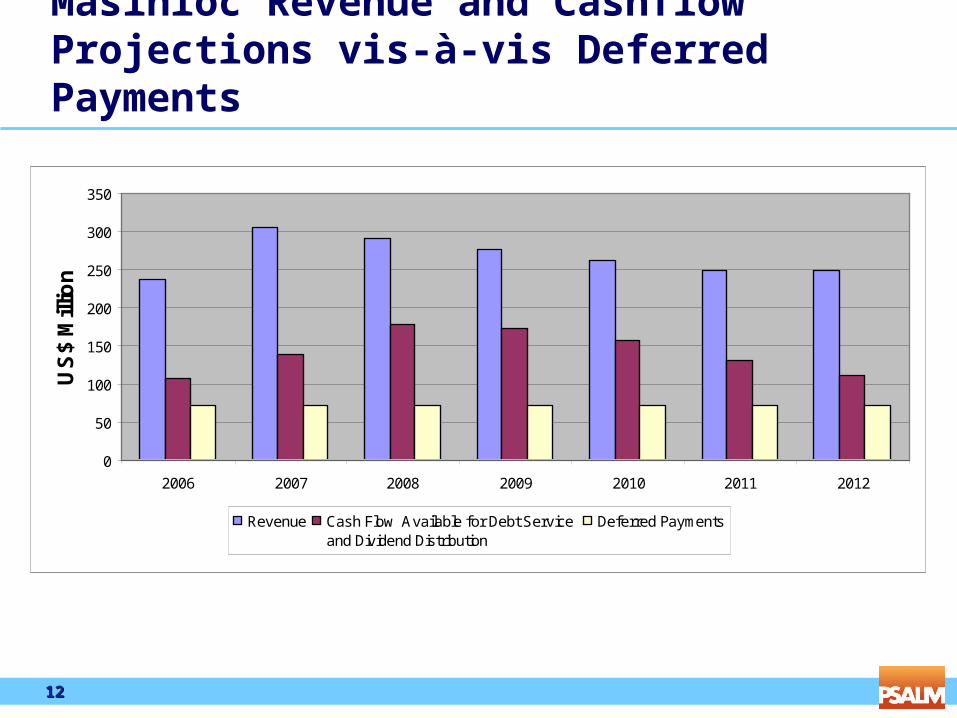

Masinloc Revenue and Cashflow Projections vis-à-vis Deferred Payments

0

50

100

150

200

250

300

350

2006 2007 2008 2009 2010 2011 2012

US

$ M

illio

n

Revenue Cash Flow Available for Debt Service and Dividend Distribution

Deferred Payments

13131313

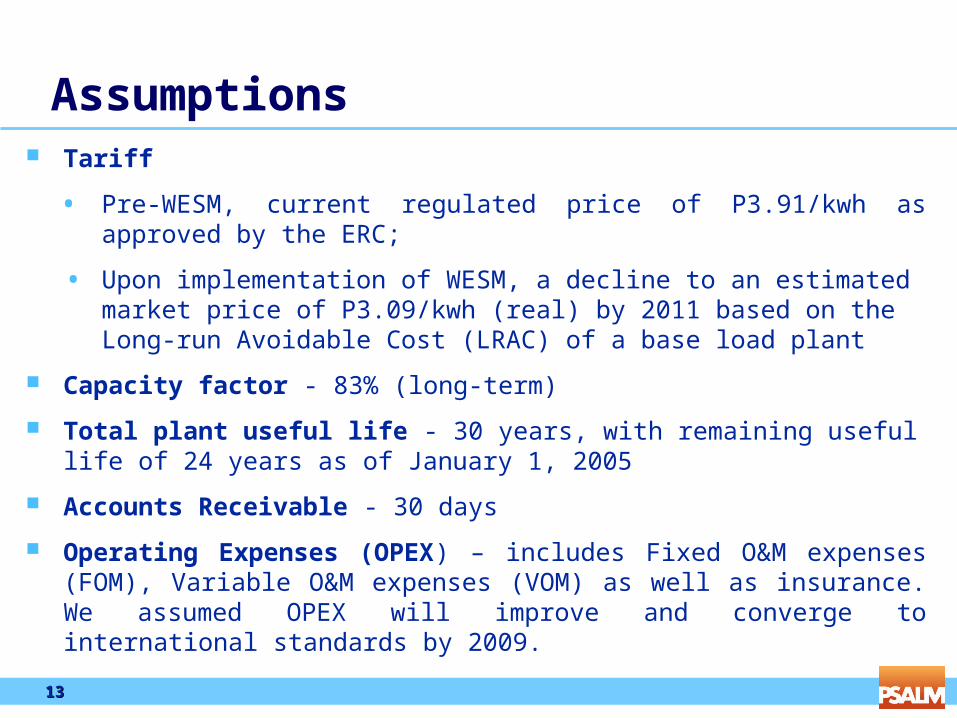

Assumptions Tariff

• Pre-WESM, current regulated price of P3.91/kwh as approved by the ERC;

• Upon implementation of WESM, a decline to an estimated market price of P3.09/kwh (real) by 2011 based on the Long-run Avoidable Cost (LRAC) of a base load plant

Capacity factor - 83% (long-term)

Total plant useful life - 30 years, with remaining useful life of 24 years as of January 1, 2005

Accounts Receivable - 30 days

Operating Expenses (OPEX) – includes Fixed O&M expenses (FOM), Variable O&M expenses (VOM) as well as insurance. We assumed OPEX will improve and converge to international standards by 2009.

Masinloc Next Steps and TimetableMasinloc Next Steps and Timetable

15151515

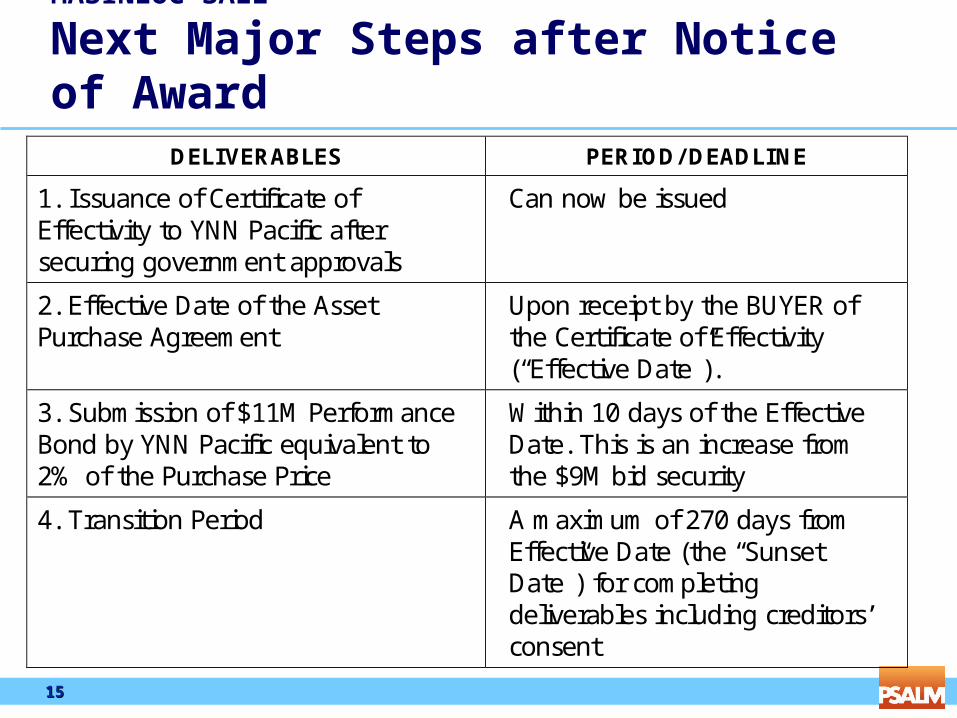

MASINLOC SALE

Next Major Steps after Notice of Award ̀ DELIVERABLES PERIOD/ DEADLINE

1. Issuance of Certificate of Effectivity to YNN Pacific after securing government approvals

Can now be issued

2. Effective Date of the Asset Purchase Agreement

Upon receipt by the BUYER of the Certificate of Effectivity (“Effective Date”).

3. Submission of $11M Performance Bond by YNN Pacific equivalent to 2% of the Purchase Price

Within 10 days of the Effective Date. This is an increase from the $9M bid security

4. Transition Period A maximum of 270 days from Effective Date (the “Sunset Date”) for completing deliverables including creditors’ consent

16161616

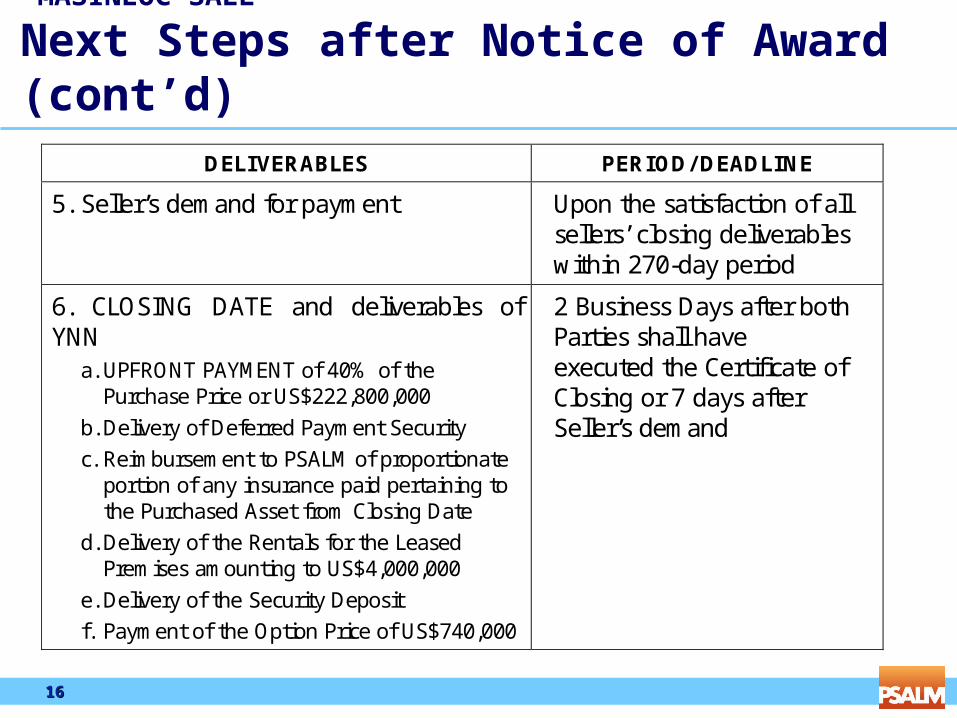

MASINLOC SALE

Next Steps after Notice of Award (cont’d) DELIVERABLES PERIOD/ DEADLINE

5. Seller’s demand for payment Upon the satisfaction of all sellers’ closing deliverables within 270-day period

6. CLOSING DATE and deliverables of YNN

a. UPFRONT PAYMENT of 40% of the Purchase Price or US$222,800,000

b. Delivery of Deferred Payment Security c. Reimbursement to PSALM of proportionate

portion of any insurance paid pertaining to the Purchased Asset from Closing Date

d. Delivery of the Rentals for the Leased Premises amounting to US$4,000,000

e. Delivery of the Security Deposit f. Payment of the Option Price of US$740,000

2 Business Days after both Parties shall have executed the Certificate of Closing or 7 days after Seller’s demand

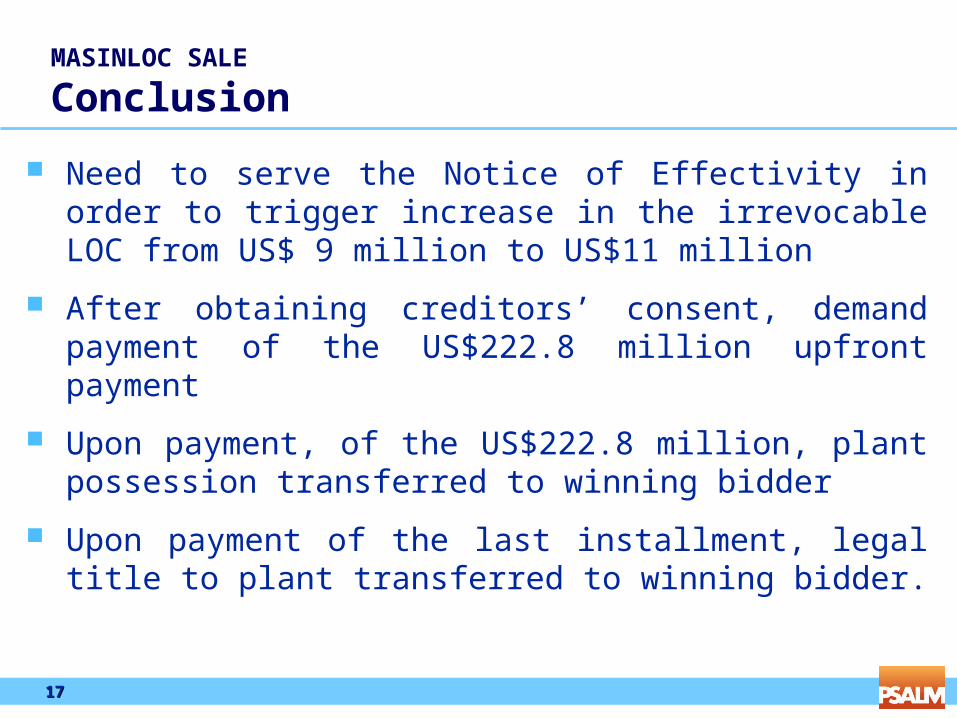

17171717

MASINLOC SALE

Conclusion

Need to serve the Notice of Effectivity in order to trigger increase in the irrevocable LOC from US$ 9 million to US$11 million

After obtaining creditors’ consent, demand payment of the US$222.8 million upfront payment

Upon payment, of the US$222.8 million, plant possession transferred to winning bidder

Upon payment of the last installment, legal title to plant transferred to winning bidder.

TRANSCOTRANSCO

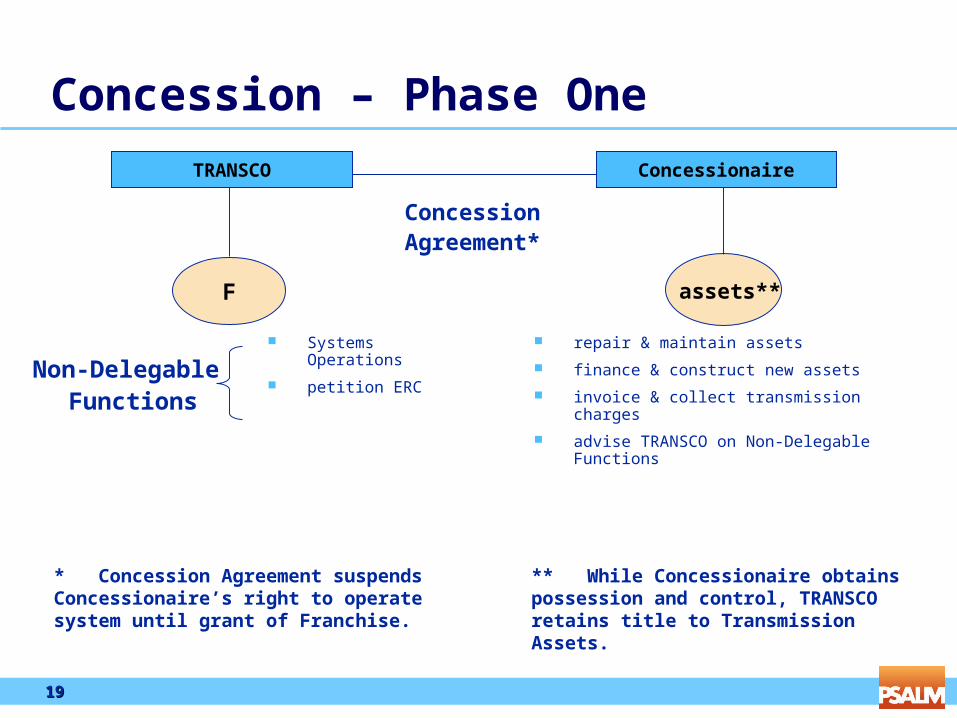

19191919

Concession – Phase One

Systems Operations

petition ERC

repair & maintain assets

finance & construct new assets

invoice & collect transmission charges

advise TRANSCO on Non-Delegable Functions

Non-Delegable Functions

Concession Agreement*

assets**F

ConcessionaireTRANSCO

* Concession Agreement suspends Concessionaire’s right to operate system until grant of Franchise.

** While Concessionaire obtains possession and control, TRANSCO retains title to Transmission Assets.

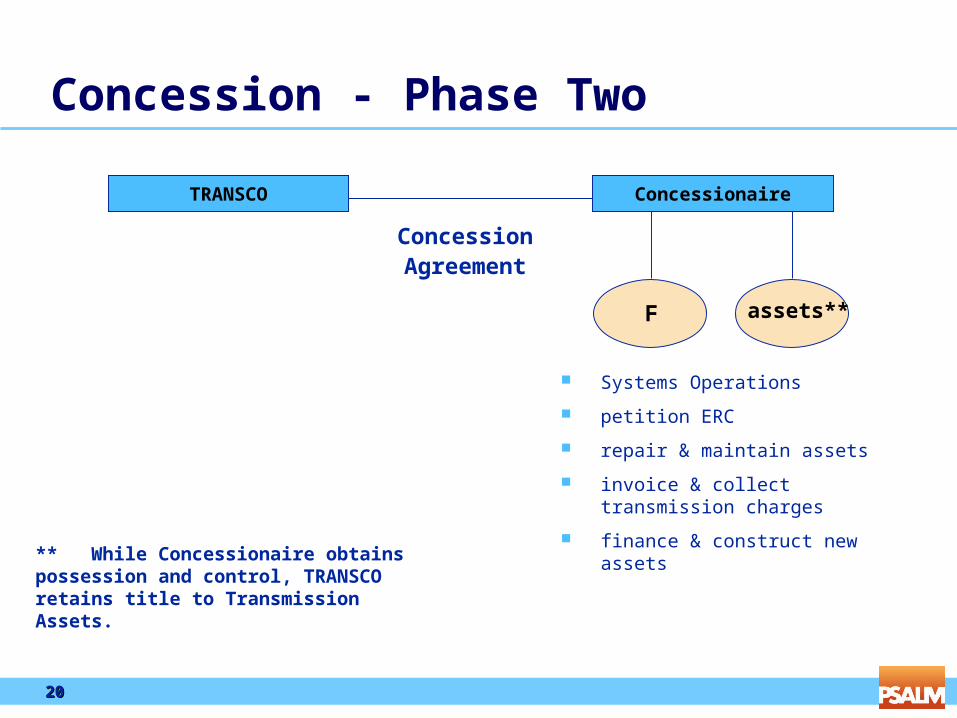

20202020

Concession - Phase Two

Systems Operations

petition ERC

repair & maintain assets

invoice & collect transmission charges

finance & construct new assets

Concession Agreement

assets**F

ConcessionaireTRANSCO

** While Concessionaire obtains possession and control, TRANSCO retains title to Transmission Assets.

21212121

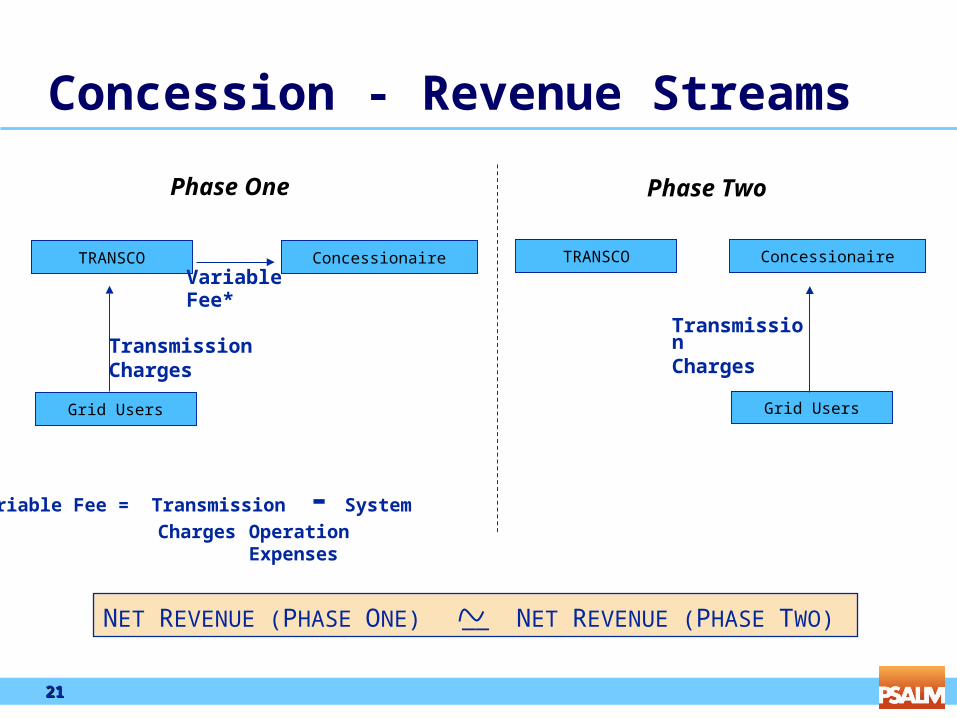

Concession - Revenue Streams

ConcessionaireTRANSCO

Transmission Charges

*Variable Fee = Transmission - System

Charges OperationExpenses

Phase One Phase Two

ConcessionaireTRANSCOVariable Fee*

Grid Users Grid Users

Transmission Charges

NET REVENUE (PHASE ONE) __ NET REVENUE (PHASE TWO)

22222222

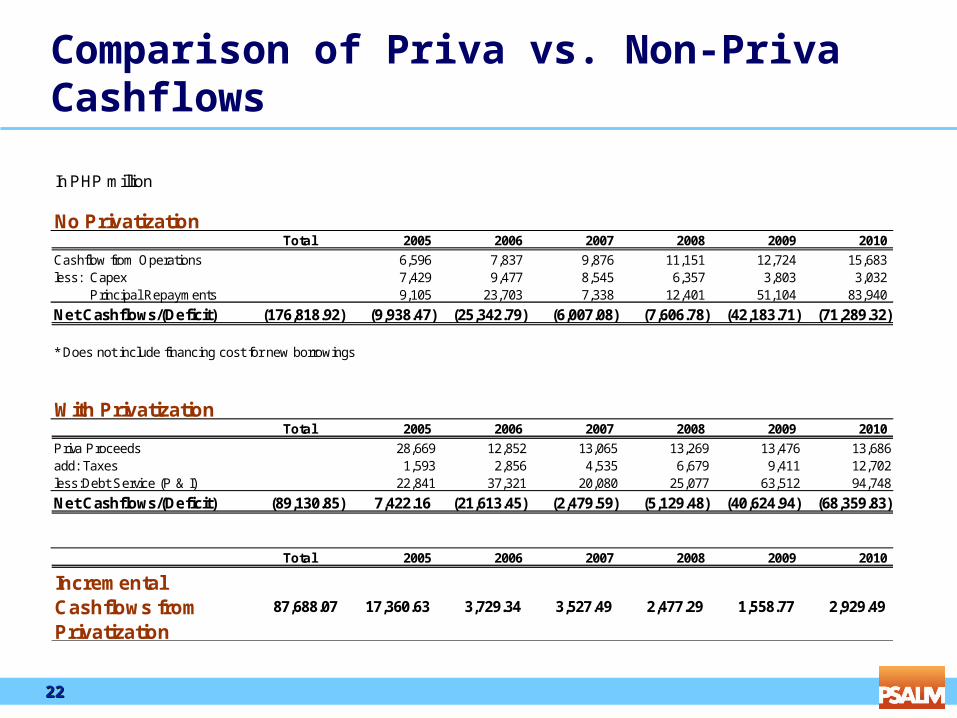

Comparison of Priva vs. Non-Priva Cashflows

In PHP million

No PrivatizationTotal 2005 2006 2007 2008 2009 2010

Cashflow from Operations 6,596 7,837 9,876 11,151 12,724 15,683 less: Capex 7,429 9,477 8,545 6,357 3,803 3,032 Principal Repayments 9,105 23,703 7,338 12,401 51,104 83,940

Net Cashflows/(Deficit) (176,818.92) (9,938.47) (25,342.79) (6,007.08) (7,606.78) (42,183.71) (71,289.32)

* Does not include financing cost for new borrowings

With PrivatizationTotal 2005 2006 2007 2008 2009 2010

Priva Proceeds 28,669 12,852 13,065 13,269 13,476 13,686add: Taxes 1,593 2,856 4,535 6,679 9,411 12,702less:Debt Service (P & I) 22,841 37,321 20,080 25,077 63,512 94,748

Net Cashflows/(Deficit) (89,130.85) 7,422.16 (21,613.45) (2,479.59) (5,129.48) (40,624.94) (68,359.83)

Total 2005 2006 2007 2008 2009 2010

Incremental Cashflows from Privatization

87,688.07 17,360.63 3,729.34 3,527.49 2,477.29 1,558.77 2,929.49

23232323

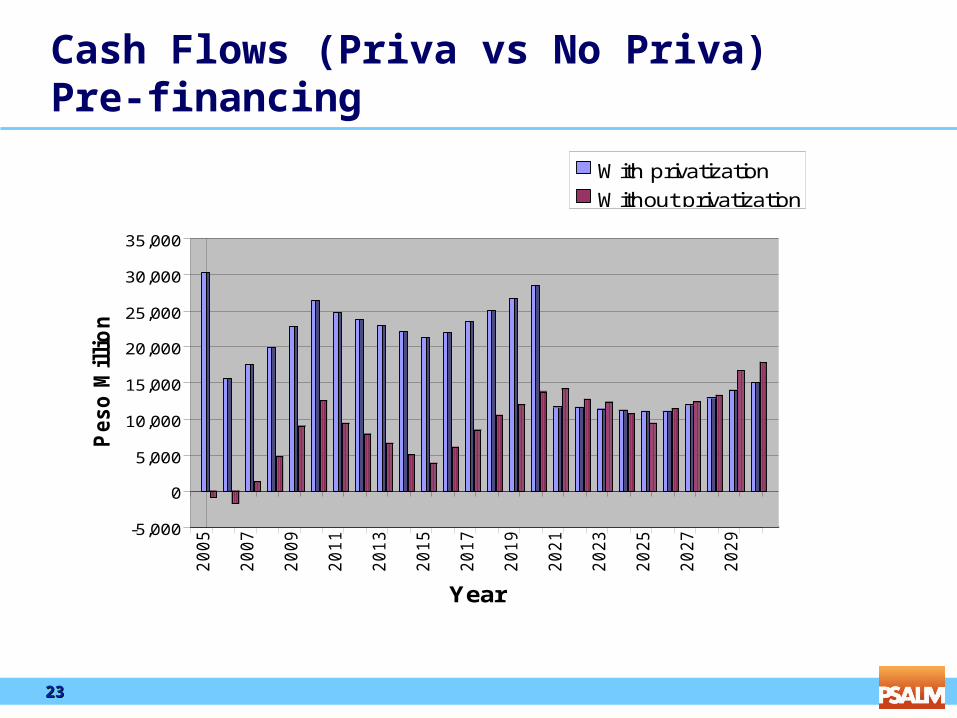

Cash Flows (Priva vs No Priva)Pre-financing

20

05

20

07

20

09

20

11

20

13

20

15

20

17

20

19

20

21

20

23

20

25

20

27

20

29-5,000

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Peso

Mil

lio

ns

Year

With privatization

Without privatization

24242424

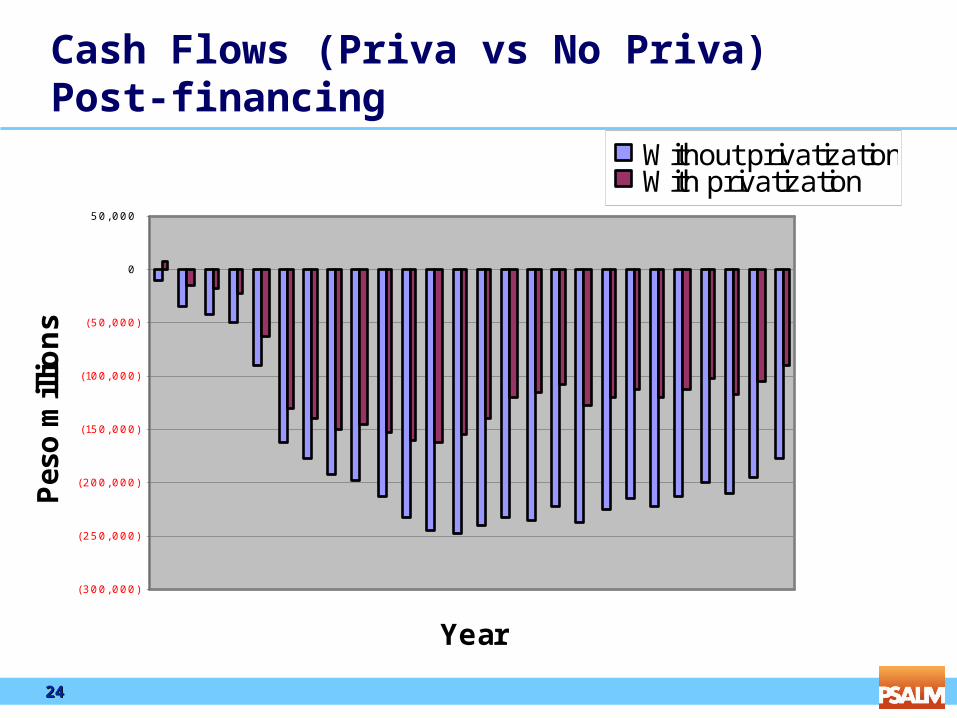

Cash Flows (Priva vs No Priva)Post-financing

(300, 000)

(250, 000)

(200, 000)

(150, 000)

(100, 000)

(50, 000)

0

50, 000

Year

Pes

o m

illio

ns

Without privatizationWith privatization

25252525