© service des relations industrielles (sri)© epfl quelques réalités des start-ups (académiques)...

TRANSCRIPT

© Service des relations industrielles (SRI)© EPFL

Quelques Réalitésdes Start-ups

(académiques)

ventureideas @ EPFL24 novembre 2005

Hervé Lebret

© Service des relations industrielles (SRI)© EPFL

EPFL spin-offs

© Service des relations industrielles (SRI)© EPFL

US University VC backed spin-offs

Source: " A STUDY OF ACADEMIC ENTREPRENEURS USING VENTURE CAPITAL DATA“ Junfu Zhang, PUBLIC POLICY INSTITUTE OF CALIFORNIA (2005)

Range: 1992-2001

These are VC backed startups

EPFL is in the 6-10 range- Snaketech- Cytion- Endoart- IR Microsystems- Dartfish- BeamExpress- Covalys- Innovative SIlicon

Number of Entrepreneurs and Spin-offs from Universities (1992-2001)

Institution Entrepreneurs Spin-offs Institution Entrepreneurs Spin-offs

Stanford 96 91 U Colorado 10 7

MIT 85 76 UIUC 10 6

Harvard 58 53 Brown 9 6

UC Berkeley 38 37 UW-Madison 9 6

CMU 24 19 U Minnesota 8 8

UCSF 20 17 Washington U 8 5

UC San Diego 17 17 Cornell 7 8

Duke 17 14 Northwestern 7 8

U Washington 16 13 Johns Hopkins 7 6

CalTech 15 15 U Arizona 7 6

Columbia 14 12 UCSB 7 6

Michigan 13 13 Princeton 6 5

Yale 13 12 U Penn 6 5

Chicago 13 10 U Pittsburgh 6 4

UT-Austin 12 14 UC Davis 5 6

Boston U 12 10 Purdue 5 5

NYU 12 10 Maryland 5 5

Georgia Tech 11 9 Wake Forest 5 5

USC 11 8 U New Mexico 5 4

UCLA 10 11 Emory 5 3

NC State 10 10

© Service des relations industrielles (SRI)© EPFL

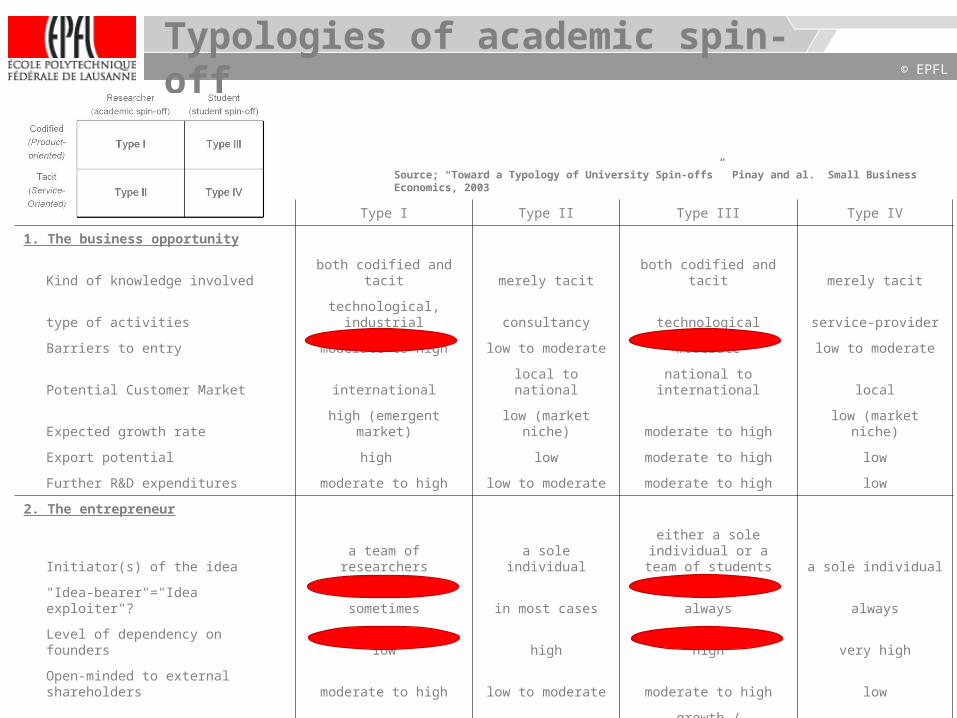

“an academic spin-off is a new firm created to exploit commercially some knowledge, technology or research results developed within a university”from “Toward a Typology of University Spin-offs” Pinay and al. Small Business Economics, 2003

e.g.

Google is a Stanford spin-off, - basic patent belongs to Stanford - technology developed by founders during their work

Yahoo is not a Stanford spin-off: - no IP generated - founders developed it on their spare time

What is an academic spin-off?

© Service des relations industrielles (SRI)© EPFL

Source: “Toward a Typology of University Spin-offs” Pinay and al. Small Business Economics, 2003

Typologies of academic spin-offs

Individual Status

Researcher

(academic spin-off)

Student

(student spin-off)

Nature of knowledge transferred

Codified

(Product-

oriented)Type I Type III

Tacit

(Service-

Oriented)Type II Type IV

© Service des relations industrielles (SRI)© EPFL

Typologies of academic spin-off

Type I Type II Type III Type IV

1. The business opportunity

Kind of knowledge involved both codified and tacit merely tacit both codified and tacit merely tacit

type of activities technological, industrial consultancy technological service-provider

Barriers to entry moderate to high low to moderate moderate low to moderate

Potential Customer Market international local to national national to international local

Expected growth rate high (emergent market) low (market niche) moderate to high low (market niche)

Export potential high low moderate to high low

Further R&D expenditures moderate to high low to moderate moderate to high low

2. The entrepreneur

Initiator(s) of the idea a team of researchers a sole individualeither a sole individual or a

team of students a sole individual

"Idea-bearer"="Idea exploiter"? sometimes in most cases always always

Level of dependency on founders low high high very high

Open-minded to external shareholders moderate to high low to moderate moderate to high low

Goal pursued growth profitability growth / profitability profitability

3. The required resources

Financial needs (seed funding,…) high low to moderate moderate to high low to moderate

Material needs (equipment, …) moderate to high low moderate low

Intangible needs (networking, …) high low to moderate moderate to high low to moderate

Source; “Toward a Typology of University Spin-offs” Pinay and al. Small Business Economics, 2003

© Service des relations industrielles (SRI)© EPFL

Venture backed entrepreneurs by industry

Industry Nb of entrepreneurs Nb of academic entrepreneurs

Percentage of

academic

entrepreneurs

Materials/chemicals 39 11 28%

Biopharma 618 252 41%

Communication 1441 95 6%

Consumer / business products 71 9 13%

Consumer / business services 2470 76 3%

Electronics 280 23 8%

Energy 12 1 8%

Medical devices 346 51 15%

Semiconductor 442 44 10%

Software 2963 226 8%

Total 10530 903 8%

Industry distribution of start-ups

Source: " A STUDY OF ACADEMIC ENTREPRENEURS USING VENTURE CAPITAL DATA“ Junfu Zhang, PUBLIC POLICY INSTITUTE OF CALIFORNIA (2005)

© Service des relations industrielles (SRI)© EPFL

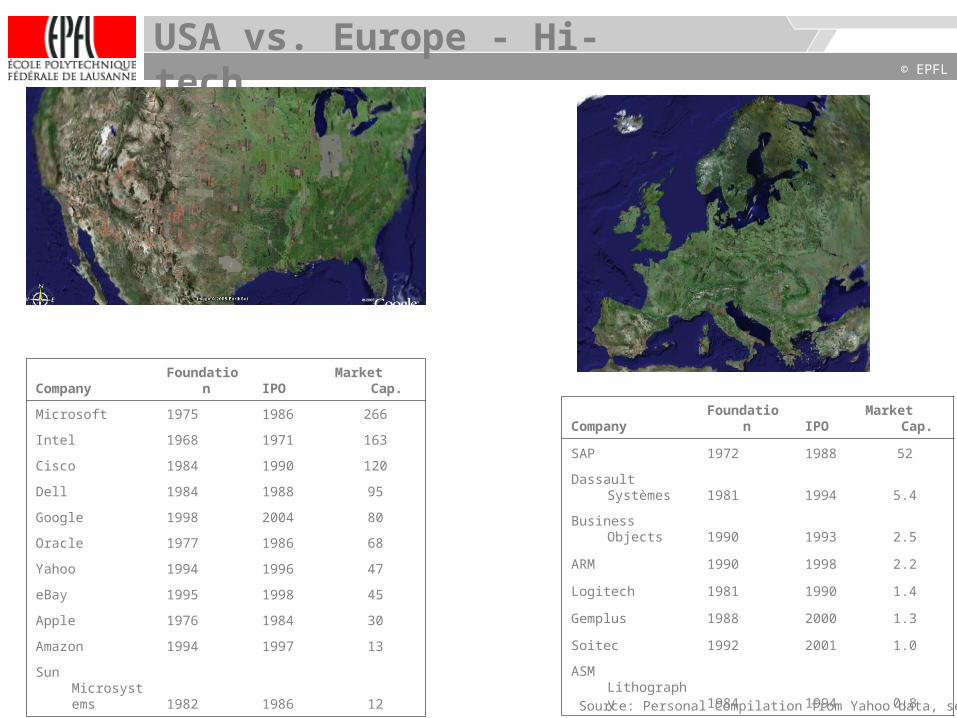

Company Foundation IPO Market Cap.

Microsoft 1975 1986 266

Intel 1968 1971 163

Cisco 1984 1990 120

Dell 1984 1988 95

Google 1998 2004 80

Oracle 1977 1986 68

Yahoo 1994 1996 47

eBay 1995 1998 45

Apple 1976 1984 30

Amazon 1994 1997 13

Sun Microsystems 1982 1986 12

Company Foundation IPO Market Cap.

SAP 1972 1988 52

Dassault Systèmes 1981 1994 5.4

Business Objects 1990 1993 2.5

ARM 1990 1998 2.2

Logitech 1981 1990 1.4

Gemplus 1988 2000 1.3

Soitec 1992 2001 1.0

ASM Lithography 1984 1994 0.8

USA vs. Europe - Hi-tech

Source: Personal Compilation from Yahoo data, sept05

© Service des relations industrielles (SRI)© EPFL

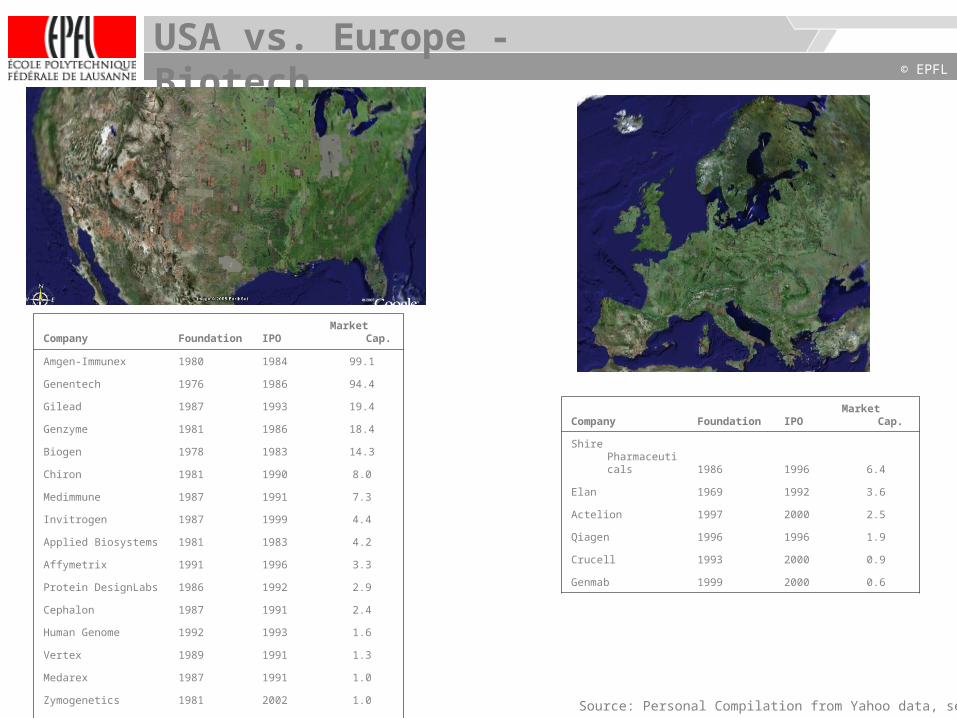

USA vs. Europe - Biotech

Company Foundation IPO Market Cap.

Amgen-Immunex 1980 1984 99.1

Genentech 1976 1986 94.4

Gilead 1987 1993 19.4

Genzyme 1981 1986 18.4

Biogen 1978 1983 14.3

Chiron 1981 1990 8.0

Medimmune 1987 1991 7.3

Invitrogen 1987 1999 4.4

Applied Biosystems 1981 1983 4.2

Affymetrix 1991 1996 3.3

Protein DesignLabs 1986 1992 2.9

Cephalon 1987 1991 2.4

Human Genome 1992 1993 1.6

Vertex 1989 1991 1.3

Medarex 1987 1991 1.0

Zymogenetics 1981 2002 1.0

Celera 1998 1998 0.9

Company Foundation IPO Market Cap.

Shire Pharmaceuticals 1986 1996 6.4

Elan 1969 1992 3.6

Actelion 1997 2000 2.5

Qiagen 1996 1996 1.9

Crucell 1993 2000 0.9

Genmab 1999 2000 0.6

Source: Personal Compilation from Yahoo data, sept05

© Service des relations industrielles (SRI)© EPFL

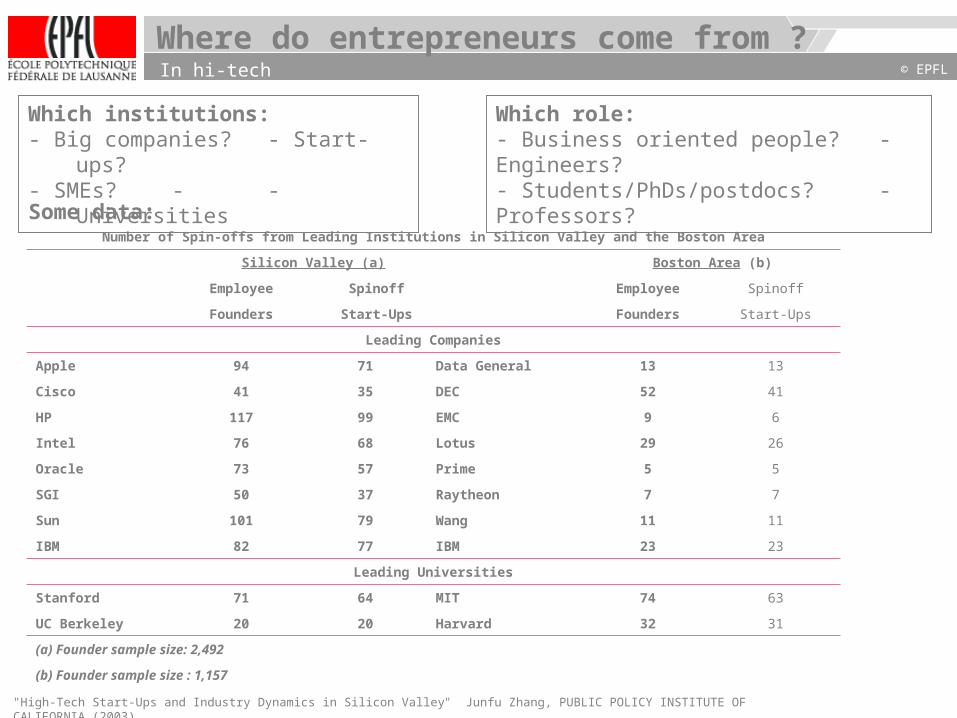

Where do entrepreneurs come from ?

Which institutions:- Big companies? - Start-ups?- SMEs? - - Universities

Which role:- Business oriented people? - Engineers?- Students/PhDs/postdocs? - Professors?

Some data:

"High-Tech Start-Ups and Industry Dynamics in Silicon Valley" Junfu Zhang, PUBLIC POLICY INSTITUTE OF CALIFORNIA (2003)

In hi-tech

Number of Spin-offs from Leading Institutions in Silicon Valley and the Boston Area

Silicon Valley (a) Boston Area (b)

Employee Spinoff Employee Spinoff

Founders Start-Ups Founders Start-Ups

Leading Companies

Apple 94 71 Data General 13 13

Cisco 41 35 DEC 52 41

HP 117 99 EMC 9 6

Intel 76 68 Lotus 29 26

Oracle 73 57 Prime 5 5

SGI 50 37 Raytheon 7 7

Sun 101 79 Wang 11 11

IBM 82 77 IBM 23 23

Leading Universities

Stanford 71 64 MIT 74 63

UC Berkeley 20 20 Harvard 32 31

(a) Founder sample size: 2,492

(b) Founder sample size : 1,157

© Service des relations industrielles (SRI)© EPFL

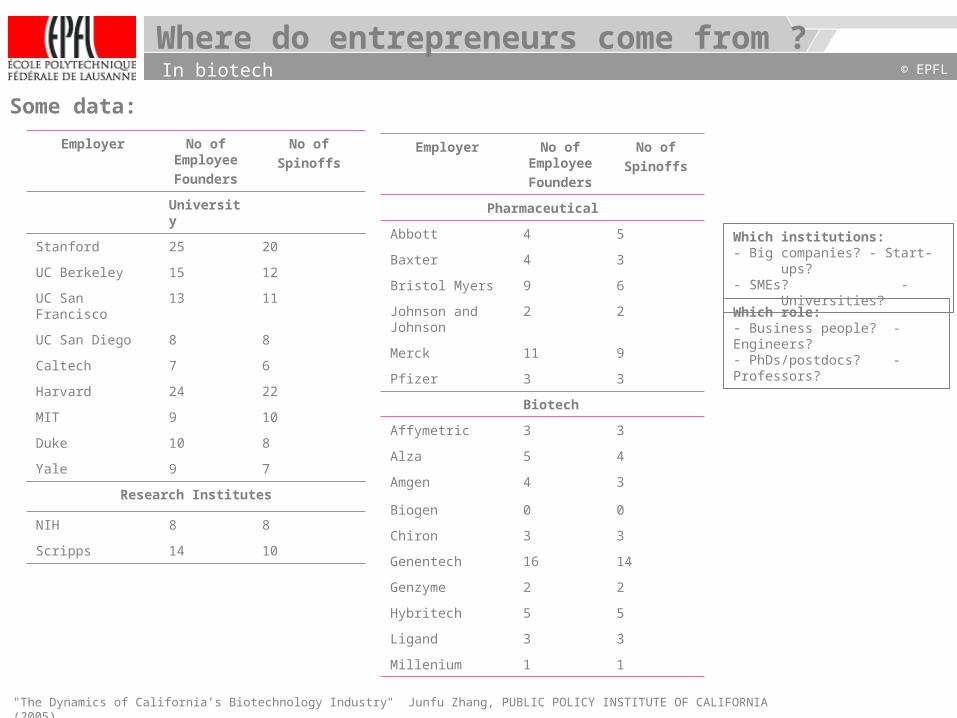

Some data:

"The Dynamics of California’s Biotechnology Industry" Junfu Zhang, PUBLIC POLICY INSTITUTE OF CALIFORNIA (2005)

Where do entrepreneurs come from ?

Employer No of Employee

Founders

No of

Spinoffs

University

Stanford 25 20

UC Berkeley 15 12

UC San Francisco 13 11

UC San Diego 8 8

Caltech 7 6

Harvard 24 22

MIT 9 10

Duke 10 8

Yale 9 7

Research Institutes

NIH 8 8

Scripps 14 10

Employer No of Employee

Founders

No of

Spinoffs

Pharmaceutical

Abbott 4 5

Baxter 4 3

Bristol Myers 9 6

Johnson and Johnson

2 2

Merck 11 9

Pfizer 3 3

Biotech

Affymetric 3 3

Alza 5 4

Amgen 4 3

Biogen 0 0

Chiron 3 3

Genentech 16 14

Genzyme 2 2

Hybritech 5 5

Ligand 3 3

Millenium 1 1

In biotech

Which institutions:- Big companies? - Start-ups?- SMEs? -

Universities?

Which role:- Business people? - Engineers?- PhDs/postdocs? - Professors?

© Service des relations industrielles (SRI)© EPFL

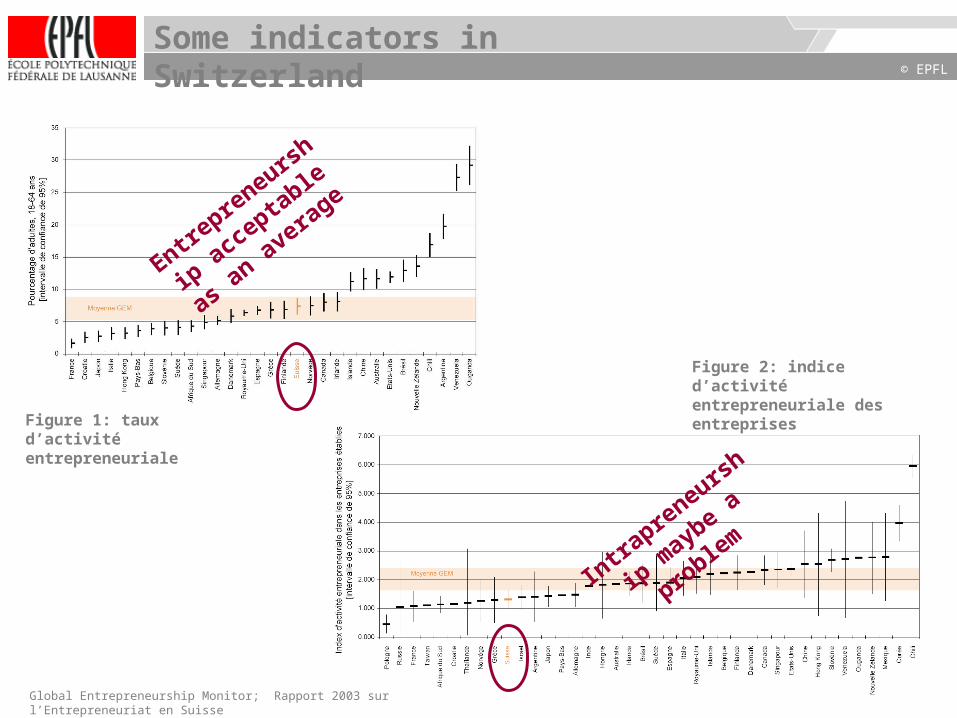

Some indicators in Switzerland

Global Entrepreneurship Monitor; Rapport 2003 sur l’Entrepreneuriat en Suisse

Figure 1: taux d’activité entrepreneuriale

Figure 2: indice d’activité entrepreneuriale des entreprises

Entrepre

neursh

ip a

ccepta

ble

as an a

vera

ge

Intr

apreneurs

hi

p mayb

e a

proble

m

© Service des relations industrielles (SRI)© EPFL

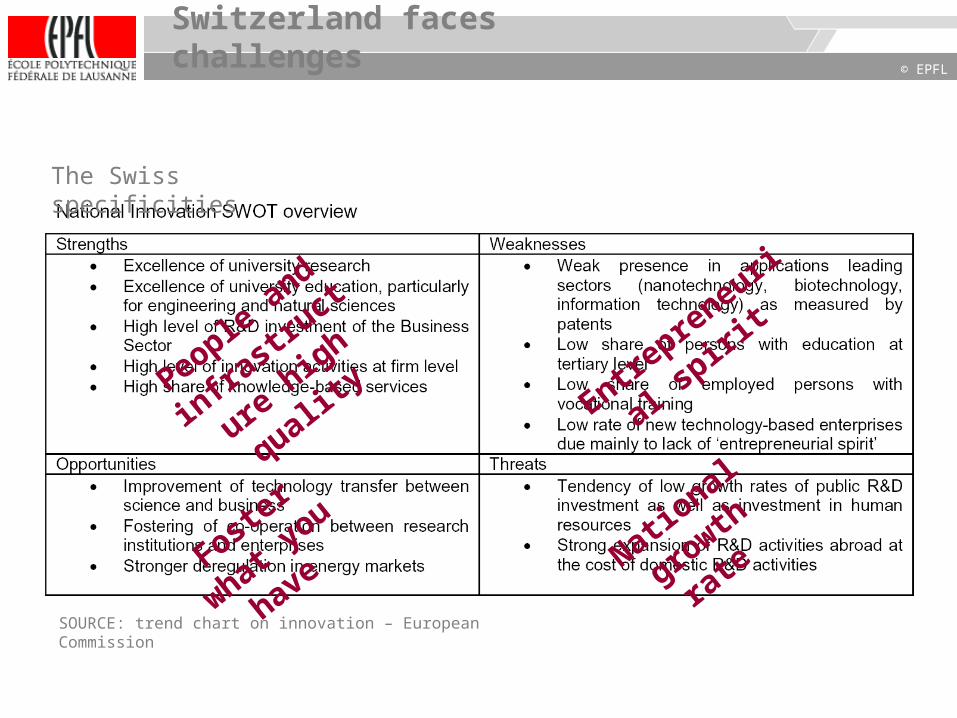

Switzerland faces challenges

SOURCE: trend chart on innovation – European Commission

People a

nd

infr

astru

ctu

re h

igh

quality

Foster

what you

have

Entrepre

neur

ial s

pirit

National

grow

th

rate

The Swiss specificities

© Service des relations industrielles (SRI)© EPFL

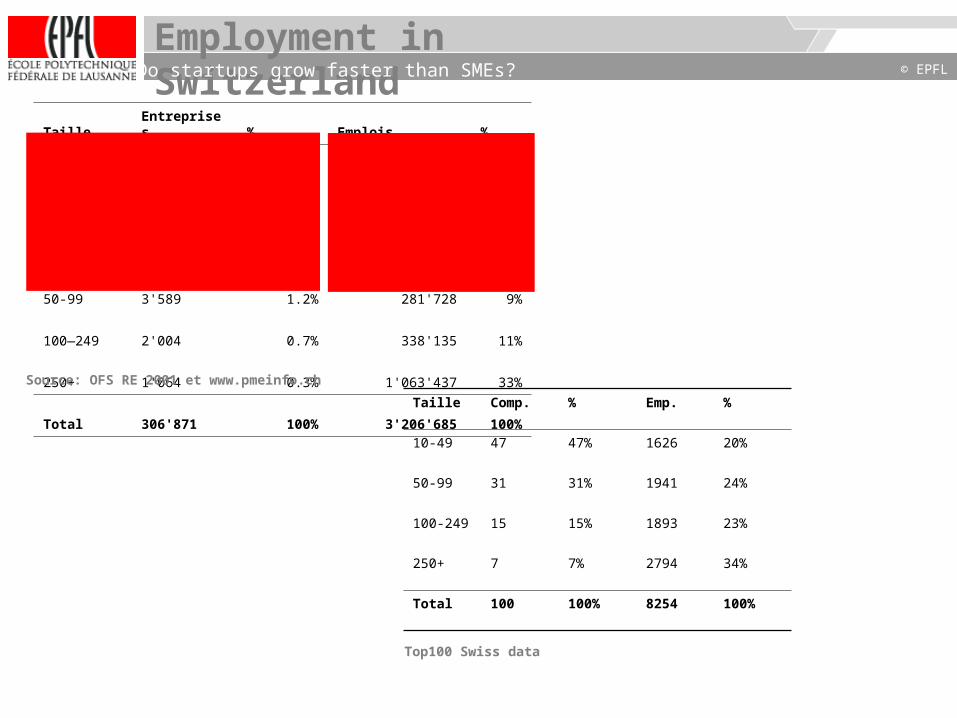

Employment in Switzerland

Taille Entreprises % Emplois %

0--4 229'735 75% 526'640 16%

5--9 40'007 13% 316'017 10%

10--49 30'472 10% 680'728 21%

50-99 3'589 1.2% 281'728 9%

100—249 2'004 0.7% 338'135 11%

250+ 1'064 0.3% 1'063'437 33%

Total 306'871 100% 3'206'685 100%66% of jobsSource: OFS RE 2001 et www.pmeinfo.ch

99% of companies

it is well known SMEs are an important component

© Service des relations industrielles (SRI)© EPFL

Jobs in “top100 Swiss” startups

0

5

10

15

20

25

1995 1996 1997 1998 1999 2000 2001 2002 2003

Foundation

# Co

mpa

nies

Source: http://www.inno-swiss.com/fr/rangliste.asp

0

200

400

600

800

1000

1200

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Foundation

Em

plo

ym

en

t

0

20

40

60

80

100

120

140

160

180

200

1994 1996 1998 2000 2002 2004

Foundation

Em

plo

ym

en

t

About 10-15 companies per year, creating in average 80 jobs each

© Service des relations industrielles (SRI)© EPFL

Employment in Switzerland

Taille Entreprises % Emplois %

0--4 229'735 75% 526'640 16%

5--9 40'007 13% 316'017 10%

10--49 30'472 10% 680'728 21%

50-99 3'589 1.2% 281'728 9%

100—249 2'004 0.7% 338'135 11%

250+ 1'064 0.3% 1'063'437 33%

Total 306'871 100% 3'206'685 100%

Source: OFS RE 2001 et www.pmeinfo.ch

Taille Comp. % Emp. %

10-49 47 47% 1626 20%

50-99 31 31% 1941 24%

100-249 15 15% 1893 23%

250+ 7 7% 2794 34%

Total 100 100% 8254 100%

Top100 Swiss data

Do startups grow faster than SMEs?

© Service des relations industrielles (SRI)© EPFL

Company IPO Market Cap. Employees

Microsoft 1986 266 61 000

Intel 1971 163 85 000

Cisco 1990 120 38 000

Dell 1988 95 55 000

Google 2004 80 3 000

Oracle 1986 68 50 000

Yahoo 1996 47 7 600

eBay 1998 45 8 100

Apple 1984 30 15 000

Amazon 1997 13 9 000

Sun Microsystems 1982 12 31 000

Company IPO Cap. Employees

SAP 1988 52 32 000

Dassault Systèmes 1994 5.4 4 400

Business Objects 1993 2.5 3 800

ARM 1998 2.2 1 200

Logitech 1990 1.4 6 900

Gemplus 2000 1.3 5 500

ASM Lithography 1994 0.8 8 200

USA vs. Europe - Hi-tech It’s also about jobs

Source: Personal Compilation from Yahoo data, sept05

© Service des relations industrielles (SRI)© EPFL

USA vs. Europe - Biotech

Company Foundation IPO Market Cap. Employees

Amgen-Immunex 1980 1984 99.1 14 300

Genentech 1976 1986 94.4 7 600

Gilead 1987 1993 19.4 1 600

Genzyme 1981 1986 18.4 7 100

Biogen 1978 1983 14.3 4 300

Chiron 1981 1990 8.0 5 400

Medimmune 1987 1991 7.3 1 800

Invitrogen 1987 1999 4.4 3 800

Applied Biosystems 1981 1983 4.2 4 900

Affymetrix 1991 1996 3.3 900

Protein DesignLabs 1986 1992 2.9 600

Cephalon 1987 1991 2.4 2 200

Human Genome 1992 1993 1.6 800

Vertex 1989 1991 1.3 700

Medarex 1987 1991 1.0 400

Zymogenetics 1981 2002 1.0 400

Celera 1998 1998 0.9 500

Company Foundation IPO Market Cap. Employees

Shire Pharmaceuticals 1986 1996 6.4 1 800

Elan 1969 1992 3.6 1 900

Actelion 1997 2000 2.5 1 000

Qiagen 1996 1996 1.9 1 300

Crucell 1993 2000 0.9 250

Genmab 1999 2000 0.6 200

It’s also about jobs

Source: Personal Compilation from Yahoo data, sept05

© Service des relations industrielles (SRI)© EPFL

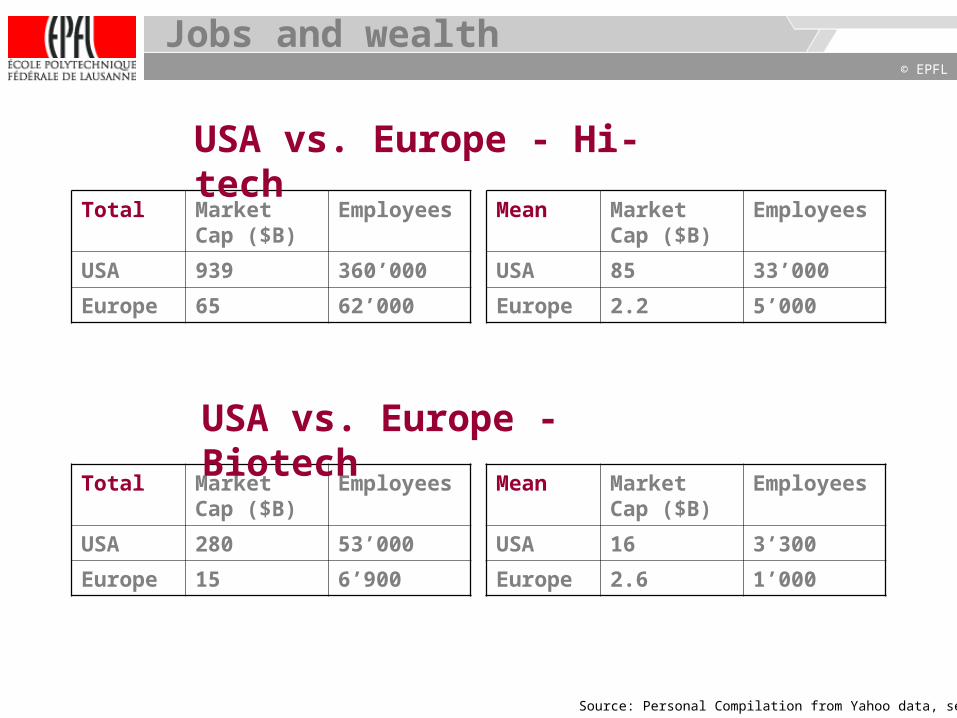

Total Market Cap ($B)

Employees

USA 939 360’000

Europe 65 62’000

Mean Market Cap ($B)

Employees

USA 85 33’000

Europe 2.2 5’000

Total Market Cap ($B)

Employees

USA 280 53’000

Europe 15 6’900

Mean Market Cap ($B)

Employees

USA 16 3’300

Europe 2.6 1’000

USA vs. Europe - Biotech

USA vs. Europe - Hi-tech

Jobs and wealth

Source: Personal Compilation from Yahoo data, sept05

© Service des relations industrielles (SRI)© EPFL

Jobs in California biotech

98% of companies"The Dynamics of California’s Biotechnology Industry" Junfu Zhang, PUBLIC POLICY INSTITUTE OF CALIFORNIA (2005)

45% of jobs

44% of companies

2.5% of jobs

© Service des relations industrielles (SRI)© EPFL

Switzerland vs. US biotech

Size Enterprises % Jobs %

0--4 229'735 75% 526'640 16%

5--9 40'007 13% 316'017 10%

10--49 30'472 10% 680'728 21%

50-99 3'589 1.2% 281'728 9%

100--249 2'004 0.7% 338'135 11%

250+ 1'064 0.3% 1'063'437 33%

Total 306'871 100% 3'206'685 100%

Many Swiss companies remain extremely small

© Service des relations industrielles (SRI)© EPFL

Jobs in tech clusters

"High-Tech Start-Ups and Industry Dynamics in Silicon Valley" Junfu Zhang, PUBLIC POLICY INSTITUTE OF CALIFORNIA (2003)

“5 or more employees” might be an interesting measure

© Service des relations industrielles (SRI)© EPFL

US VC Fund Size ($M) Date

Mayfield XII 375 2005

Battery VII 450 2004

USVP IX 600 2004

Kleiner Perkins XI 400 2004

Sequoia XI 400 2003

Eur. VC Fund Size (€M) Date

Index III 300 2005

Soffinova V 380 2004

TVM VI 240 2004

Atlas VI 600 2001

Amadeus III 345 2000

Top US and European VCs

Source: Personal data

US VCs are bigger but there is money in Europe

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Year

$B

US Top 10 Eur Top 40

Some VCs among the biggest

© Service des relations industrielles (SRI)© EPFL

US and European VCs

Source: Amadeus Capital Partners (thanks P. Dutheil)

US VCs are bigger but there is money in Europe

from 2000 to Q3 - 2004

© Service des relations industrielles (SRI)© EPFL

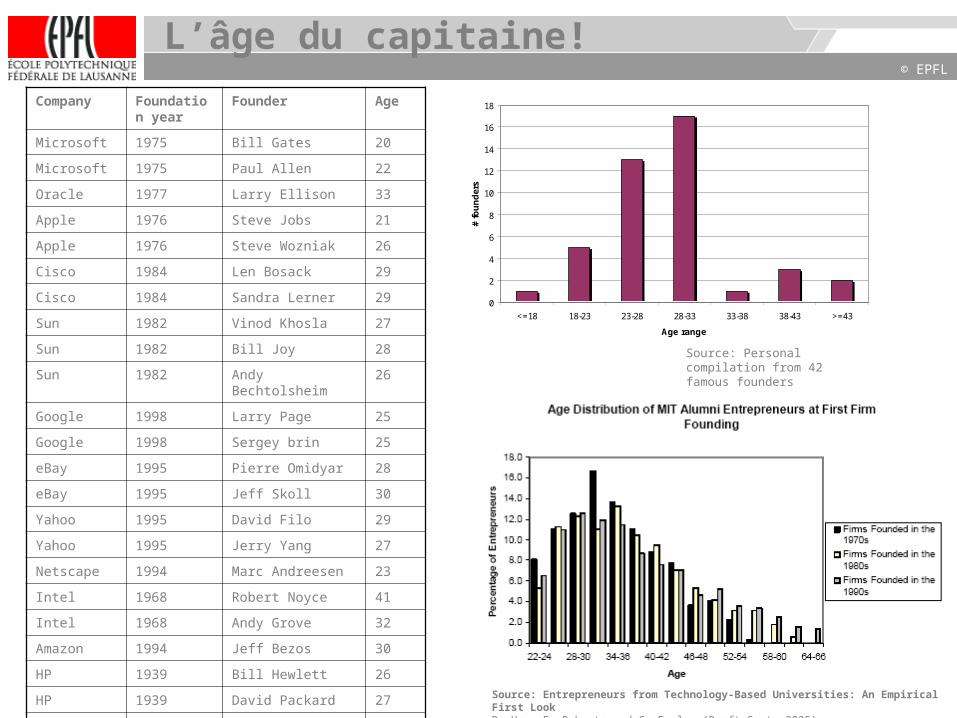

L’âge du capitaine!

Company Foundation year

Founder Age

Microsoft 1975 Bill Gates 20

Microsoft 1975 Paul Allen 22

Oracle 1977 Larry Ellison 33

Apple 1976 Steve Jobs 21

Apple 1976 Steve Wozniak 26

Cisco 1984 Len Bosack 29

Cisco 1984 Sandra Lerner 29

Sun 1982 Vinod Khosla 27

Sun 1982 Bill Joy 28

Sun 1982 Andy Bechtolsheim 26

Google 1998 Larry Page 25

Google 1998 Sergey brin 25

eBay 1995 Pierre Omidyar 28

eBay 1995 Jeff Skoll 30

Yahoo 1995 David Filo 29

Yahoo 1995 Jerry Yang 27

Netscape 1994 Marc Andreesen 23

Intel 1968 Robert Noyce 41

Intel 1968 Andy Grove 32

Amazon 1994 Jeff Bezos 30

HP 1939 Bill Hewlett 26

HP 1939 David Packard 27

Dell 1984 Michael Dell 19

Source: Personal compilation from 42 famous founders

0

2

4

6

8

10

12

14

16

18

<=18 18-23 23-28 28-33 33-38 38-43 >=43

Age range

# fo

un

der

s

Source: Entrepreneurs from Technology-Based Universities: An Empirical First LookD. Hsu, E. Roberts and C. Eesley (Draft Sept, 2005)

© Service des relations industrielles (SRI)© EPFL

Research and Innovation

There has been an going debate on the contradiction indoing quality research and spin-off activity. However:

- many studies show a correlation between number of publications and patenting, between quality research and innovation (e.g. Agrawal 2002, Shane 2000)

- in biotech, many very successful startups are linked to “Star” scientists, e.g. Genentech, Biogen, Amgen have Nobel Prize founders

- who knows Einstein had patents on refrigerators ? (and made money with them!)

- clearly Stanford, Berkeley, MIT, Harvard are among- the best for spin-offs- the best in research ranking

- “a university’ s national academy membership is the most important variable in explaining its number of academic entrepreneurs” Zhang (2005)

© Service des relations industrielles (SRI)© EPFL

A few personal thoughts

It seems there may be an advantage for founders who are- ambitious, i.e. focused on growth- young- living in the USA? (at least know how it works)

It is more difficult but possible to succeed in Europe

Wealth and job creation are the two faces of the same coin

I am not sure the lack of resources is a good explanationfor the low success rate and number in Europe

The world is global, I am not sure what a local leader is

© Service des relations industrielles (SRI)© EPFL

So what?

A few other lessons from the USA, at least from the Silicon Valley…

- Public funding is huge (e.g. $3B for Stem Cell research in California)

- Innovation should be opened (e.g. Saxenian’s work)

- Ambitious projects/people more visible and likely to succeed?

- People keep trying and risk taking is a value

- It may be easier when you are young

© Service des relations industrielles (SRI)© EPFL

“Success is going from one failure to another, without losing your enthusiasm”

Winston Churchill

“Ever tried, ever failed? keep trying! fail better!” Samuel Beckett

“If I am in total control, I am not going fast enough”

Mario Andretti

About failure and risk