© edupristine – © edupristine...

TRANSCRIPT

© EduPristine PGCFR© EduPristine – www.edupristine.com

Corporate Finance

© EduPristine PGCFR 1

Agenda

� Reading 1: Capital Budgeting

� Reading 2: Cost of Capital

� Reading 3: Measures of Leverage

� Reading 4: Dividend and Share Repurchases

� Reading 5: Working Capital Management

� Reading 6: Corporate Governance

© EduPristine PGCFR

Capital Budgeting

2

© EduPristine PGCFR

Coverage of the topic – Capital Budgeting

1. Meaning and process of capital budgeting

2. Types of Projects

3. Basic Principles

4. Techniques of capital budgeting

5. Other Concepts

a) Projects with unequal life

b) Capital Rationing

c) NPV & stock price

3

© EduPristine PGCFR

Meaning of Capital Projects

Capital project

� Project involving huge sum of money outflow to purchase a capital asset (Long-term asset for use)

� Typical cash flow pattern – Outflow at To followed by a stream of Cash Inflows

Different e.g. of Capital Projects

1. Replacement projects: replacing old equipment with new one (cash flows can be predicted with more

certainty)

2. Expansion projects: expanding current production capacity (comparatively requires more analysis to

determine the cash flows)

3. New Product or services: introducing new product or service (more rigorous analysis is required to

find out cash flows, carries more risks)

4. Regulatory, safety and environmental: Required by government or some external party. May generate

no revenue.

5. Other projects: Risky projects difficult to analyze by usual method (R&D) or pet projects of someone in

the company (CEO buying a private jet)

4

© EduPristine PGCFR

Meaning and process of capital budgeting

Capital Budgeting

� Refers to planning for proposed capital outlays and financing of these outlays

� Evaluating Projects for which cash flows will be received over a period longer than a year

� Decision should be consistent with the goal of maximizing shareholder value

Has following 4 administrative stages:

� Idea generation: which all are the projects where a company can invest money (Most important)

� Analyzing project proposals: finding cash flows, risks etc. of the project (Most time consuming)

� Creating firm wide capital budgets: analyze whether to take the projects now or at later stage etc.

� Monitoring and Post-Audit: again reviewing the cash flows, risks etc. of the shortlisted projects

5

© EduPristine PGCFR

Basic principles of capital budgeting

1. Evaluation of decisions is based on cash flows, not accounting income

2. Cash flows are analyzed on an after-tax basis because shareholders get benefit from profit after tax only

Cash flows After Tax is NOT EQUAL to Net Income. (PAT from Income Statement)

3. Evaluation is based on Incremental Cash Flows

� Difference between the cash flows with project & cash flows without the project under consideration. This cash flows should be taken for analysis & not the total cash flows

4. Timing of cash flows affects decisions because of time value of money

� Earlier cash flows are more valuable than future cash flows

5. A project must earn equal to or more than its opportunity Cost to be accepted (like a benchmark)

� Opportunity Costs is the profit that would have earned through the next best project)

� E.g. :Investment in Stocks Vs. Interest income in an FD

6

© EduPristine PGCFR

Basic principles of capital budgeting (Contd.)

6. Sunk Costs do not play any role in Capital Budgeting

� It is the cost which cannot be recovered (whether the project is selected or not)

� E.g.: money paid to market research firm for determining demand for a new product

� Purchase price of the old machinery which is now contemplated to be replaced.

7. Externalities MUST be considered while evaluating a project

� It is the effect of the investment on other aspects besides the investment itself:

� It can be a negative impact or a Positive Impact

� Cannibalization: One product of a company eating over the share of another product of the same company

� Maruti Suzuki’s Alto model’s sale being impacted due to the launch of A-Star model

8. Financing costs (like interest rate) are not considered as a part of the cash flows because they are already considered in project's hurdle rate (required rate of return)

9. Pattern of Cash Flows

a) Conventional Cash flow – One initial outflow followed by a series of inflows

b) Nonconventional Cash Flows – Cash flows can flip from positive to negative after the initial outflow

7

© EduPristine PGCFR

Basic principles of capital budgeting (Contd.)

10. Role of Depreciation

� Depreciation is a non-cash expense hence does not play any active role in determining CF

� However, since it’s a tax deductible expense, it leads to tax saving

� Reduced tax outflow is deemed to a cash inflow

� Two approaches to calculate CFAT

1. CFAT = PBDT *(1 - T) + Dep x T

2. CFAT = PAT + Dep

11. Gain or Loss on Capital Asset

� Whenever a capital asset is sold, gain / loss is calculated

� Gain (or Loss) = Scrap or Sale value - Book Value (on the date of Sale)

� This capital gain (or loss) is taxable thus results into additional taxes (or tax savings)

� Net Cash Flow in case of:

1. Gain = Sale Value – additional taxes

2. Loss = Sale value + Tax Savings (deemed inflow)

8

© EduPristine PGCFR

Basic principles of capital budgeting (Contd.)

12. Working Capital Adjustment

� In case a new capital asset is purchased, there is a change warranted in the operational or working

capital requirement also.

� E.g. A bigger machinery will

• Need more stock of Raw material – Additional Raw Material

• Will have more WIP at any point in time - Additional WIP

• Will produce more finished output - Additional finished goods

• Overall, more investments will have to be made in the Working capital

� Adjustments required are:

1. Treat the ADDITIONAL working capital as cash out flow at To (as part of the initial cash flow)

2. Treat the same amount as cash inflow at the end of the project (as part of the terminal value)

9

© EduPristine PGCFR

Different Types of Project

1. Mutually Exclusive Projects

� Projects out of which only one can be selected

� Acceptance of one would imply rejection of the other

� Compete directly with each other

a) Either old machinery can be repaired or can be replaced by a new machinery

b) Purchase of a laptop – Either Dell or HP

2. Independent Projects

� Projects which can be selected irrespective of the other project

� Acceptance of one DOES NOT mean rejection of the other

� DO NOT Compete directly with each other

a) Entering a new market – South Africa and Egypt – BOTH can be done at the same time

b) Purchase of CDs – Moser Baer and Sony – BOTH can be done at the same time

10

© EduPristine PGCFR

Techniques of Capital Budgeting

� The methods which are used to evaluate the project based on its cash flows are known as techniques of

capital budgeting

� There are five main techniques of capital budgeting

1. Average Accounting Rate of Return (ARR)

2. Payback Period (PBP)

3. Net Present value (NPV)

4. Profitability Index (PI)

5. Internal Rate of Return (IRR)

� Each technique has a different mathematical construct to evaluate the project, each will have its own

limitations and advantages vis-à-vis other techniques

� Due to difference in basic construct, the evaluation result may be DIFFERENT

11

© EduPristine PGCFR

valuebookAverage

incomenetAverageAAR =

Tech 1 - Average Accounting Rate of Return (ARR)

� ARR is average (accrual) return earned from the project during its life

� Return is expressed as % of the average investment during the project life

� Decision Criteria: Accept the project if the ARR

is more than the benchmark rate

� Limitations

• Cash flows are not considered

• Time Value of money ignored

12

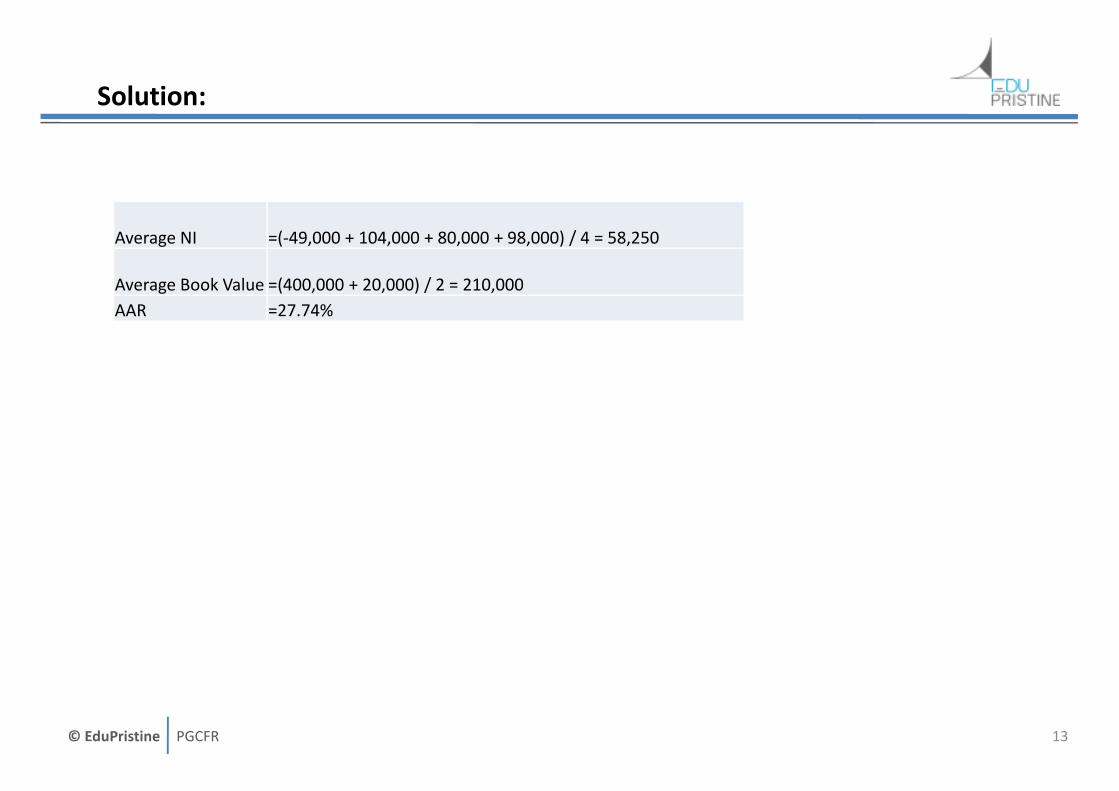

ABC Limited

Year Net Accounting Income

1 (49,000)

2 104,000

3 80,000

4 98,000

Initial Investment 4,00,000

Salvage Value after 4 years is 20,000

Example

© EduPristine PGCFR

Solution:

13

Average NI =(-49,000 + 104,000 + 80,000 + 98,000) / 4 = 58,250

Average Book Value =(400,000 + 20,000) / 2 = 210,000

AAR =27.74%

© EduPristine PGCFR

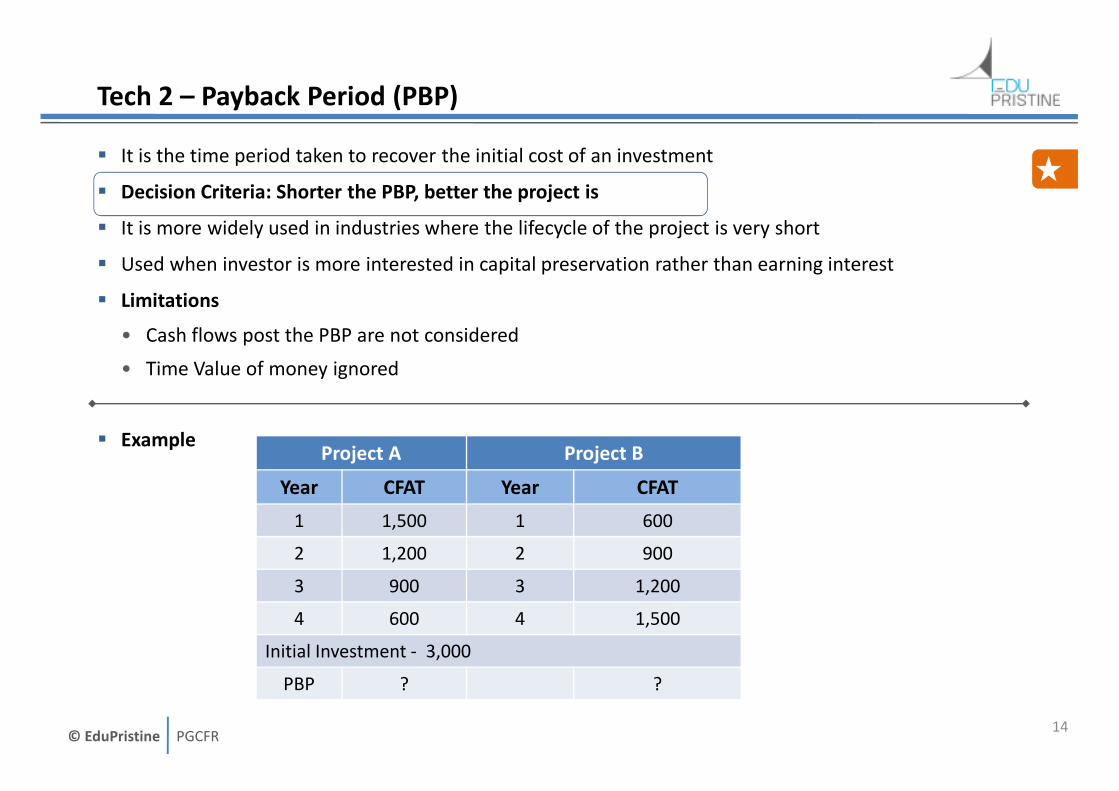

Tech 2 – Payback Period (PBP)

� It is the time period taken to recover the initial cost of an investment

� Decision Criteria: Shorter the PBP, better the project is

� It is more widely used in industries where the lifecycle of the project is very short

� Used when investor is more interested in capital preservation rather than earning interest

� Limitations

• Cash flows post the PBP are not considered

• Time Value of money ignored

� Example

14

Project A Project B

Year CFAT Year CFAT

1 1,500 1 600

2 1,200 2 900

3 900 3 1,200

4 600 4 1,500

Initial Investment - 3,000

PBP ? ?

© EduPristine PGCFR

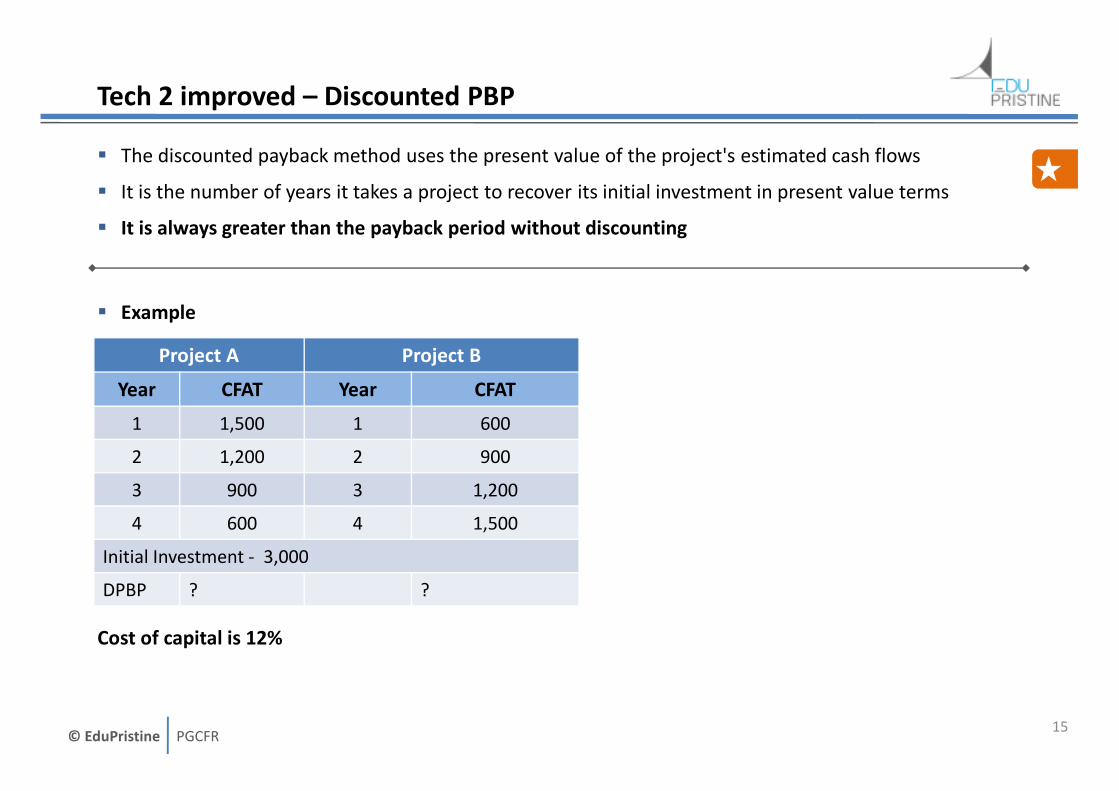

Tech 2 improved – Discounted PBP

� The discounted payback method uses the present value of the project's estimated cash flows

� It is the number of years it takes a project to recover its initial investment in present value terms

� It is always greater than the payback period without discounting

� Example

Cost of capital is 12%

15

Project A Project B

Year CFAT Year CFAT

1 1,500 1 600

2 1,200 2 900

3 900 3 1,200

4 600 4 1,500

Initial Investment - 3,000

DPBP ? ?

© EduPristine PGCFR

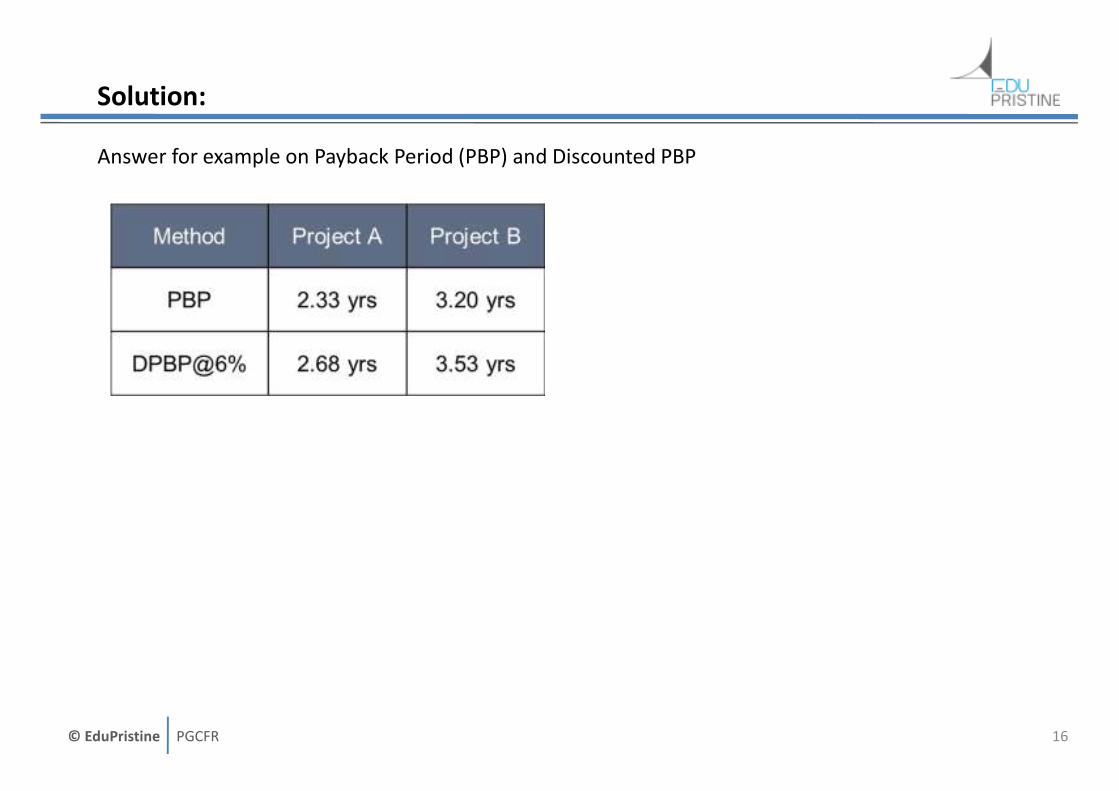

Solution:

Answer for example on Payback Period (PBP) and Discounted PBP

16

© EduPristine PGCFR

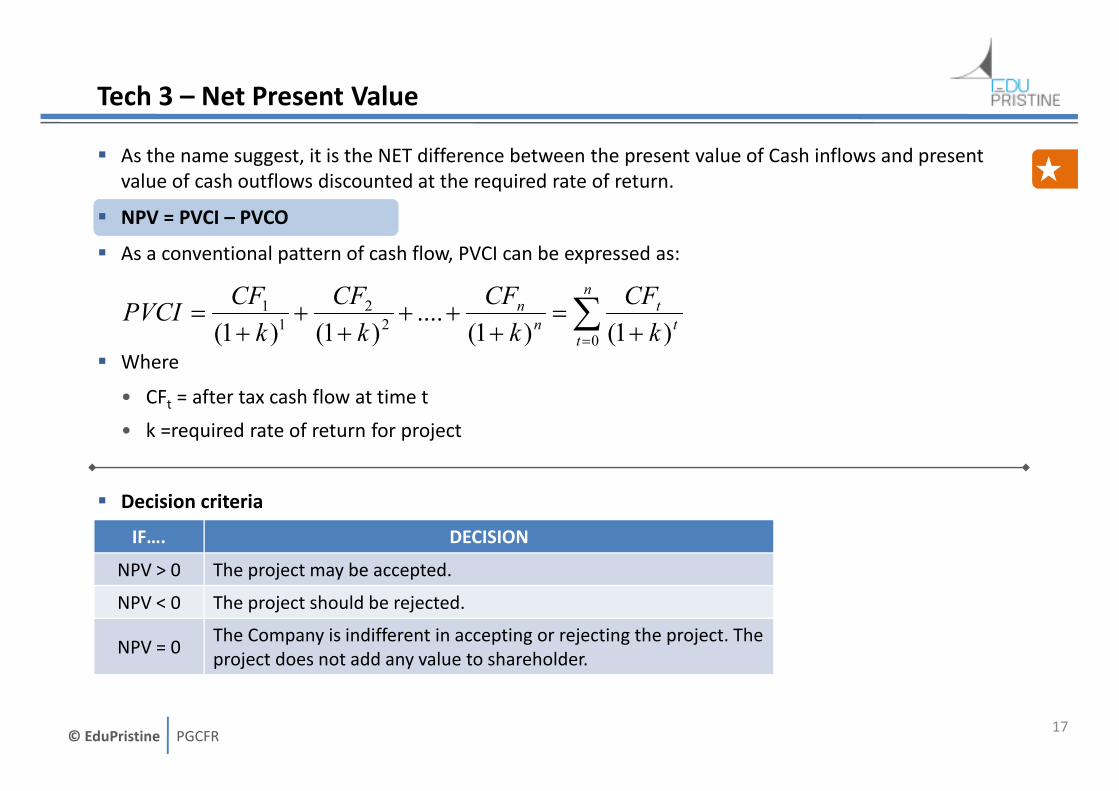

Tech 3 – Net Present Value

� As the name suggest, it is the NET difference between the present value of Cash inflows and present

value of cash outflows discounted at the required rate of return.

� NPV = PVCI – PVCO

� As a conventional pattern of cash flow, PVCI can be expressed as:

� Where

• CFt = after tax cash flow at time t

• k =required rate of return for project

� Decision criteria

17

∑= +

=+

+++

++

=n

tt

t

n

n

k

CF

k

CF

k

CF

k

CFPVCI

02

2

1

1

)1()1(....

)1()1(

IF…. DECISION

NPV > 0 The project may be accepted.

NPV < 0 The project should be rejected.

NPV = 0The Company is indifferent in accepting or rejecting the project. The

project does not add any value to shareholder.

© EduPristine PGCFR

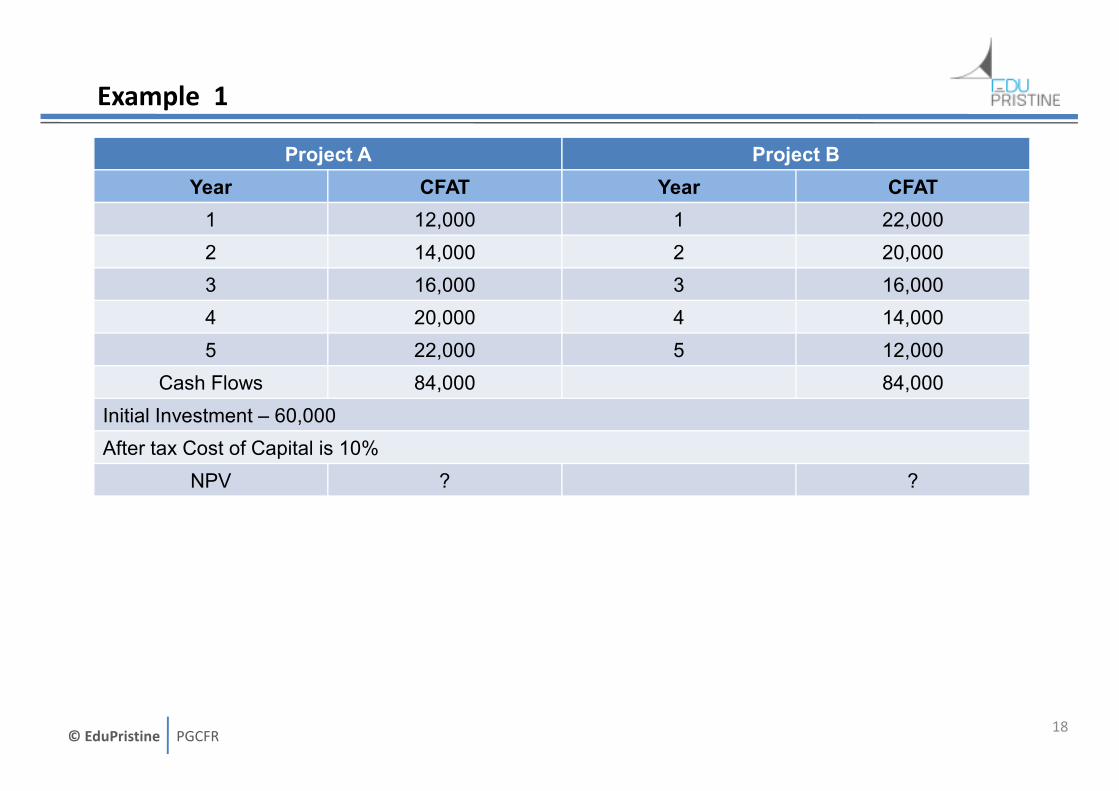

Project A Project B

Year CFAT Year CFAT

1 12,000 1 22,000

2 14,000 2 20,000

3 16,000 3 16,000

4 20,000 4 14,000

5 22,000 5 12,000

Cash Flows 84,000 84,000

Initial Investment – 60,000

After tax Cost of Capital is 10%

NPV ? ?

Example 1

18

© EduPristine PGCFR

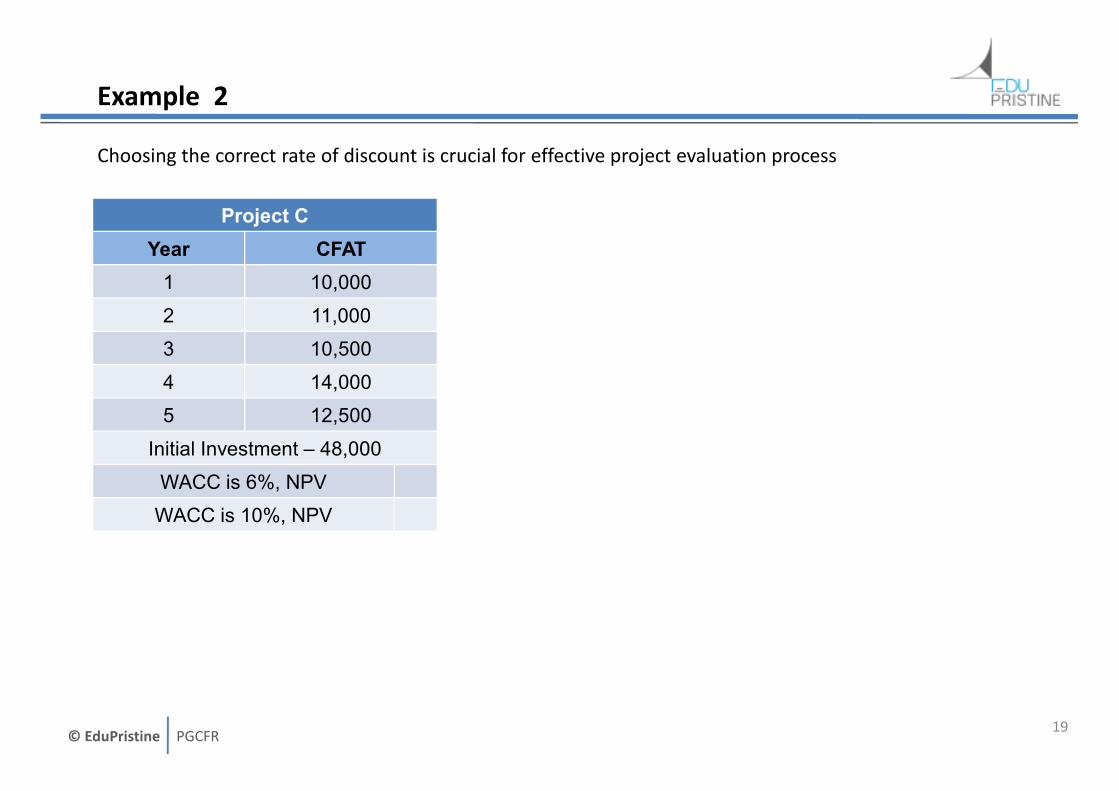

Example 2

Choosing the correct rate of discount is crucial for effective project evaluation process

19

Project C

Year CFAT

1 10,000

2 11,000

3 10,500

4 14,000

5 12,500

Initial Investment – 48,000

WACC is 6%, NPV

WACC is 10%, NPV

© EduPristine PGCFR

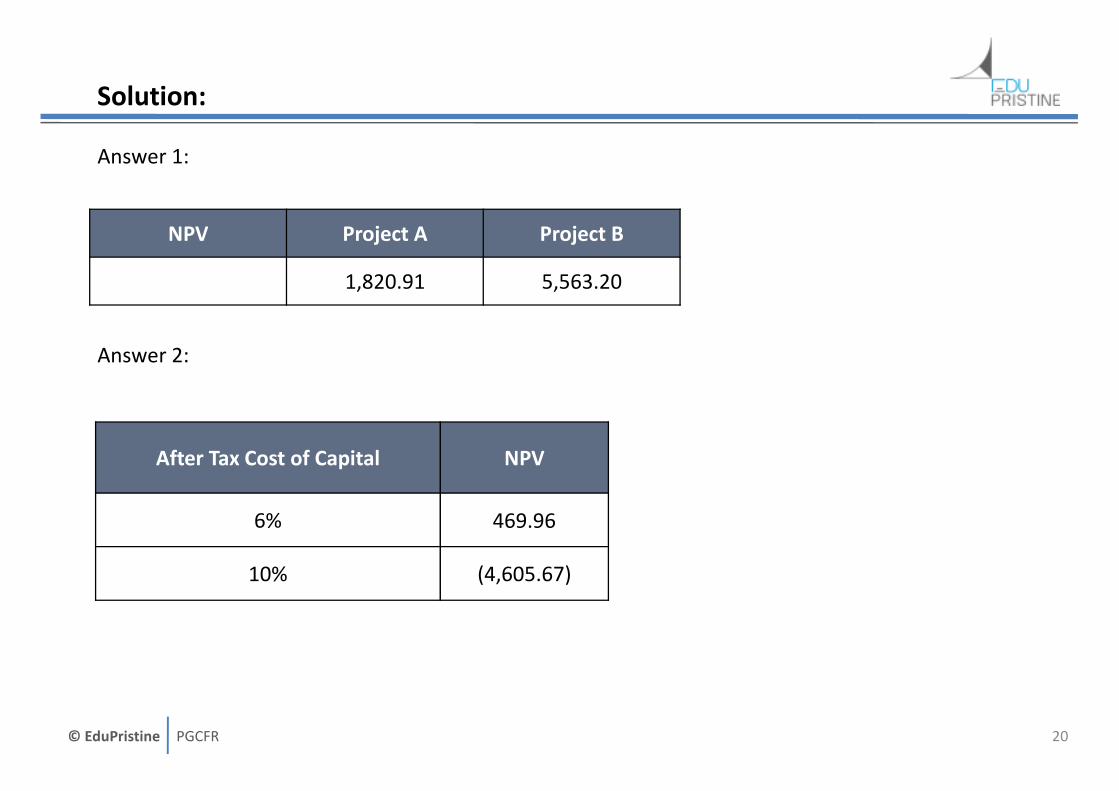

Solution:

Answer 1:

Answer 2:

20

NPV Project A Project B

1,820.91 5,563.20

After Tax Cost of Capital NPV

6% 469.96

10% (4,605.67)

© EduPristine PGCFR

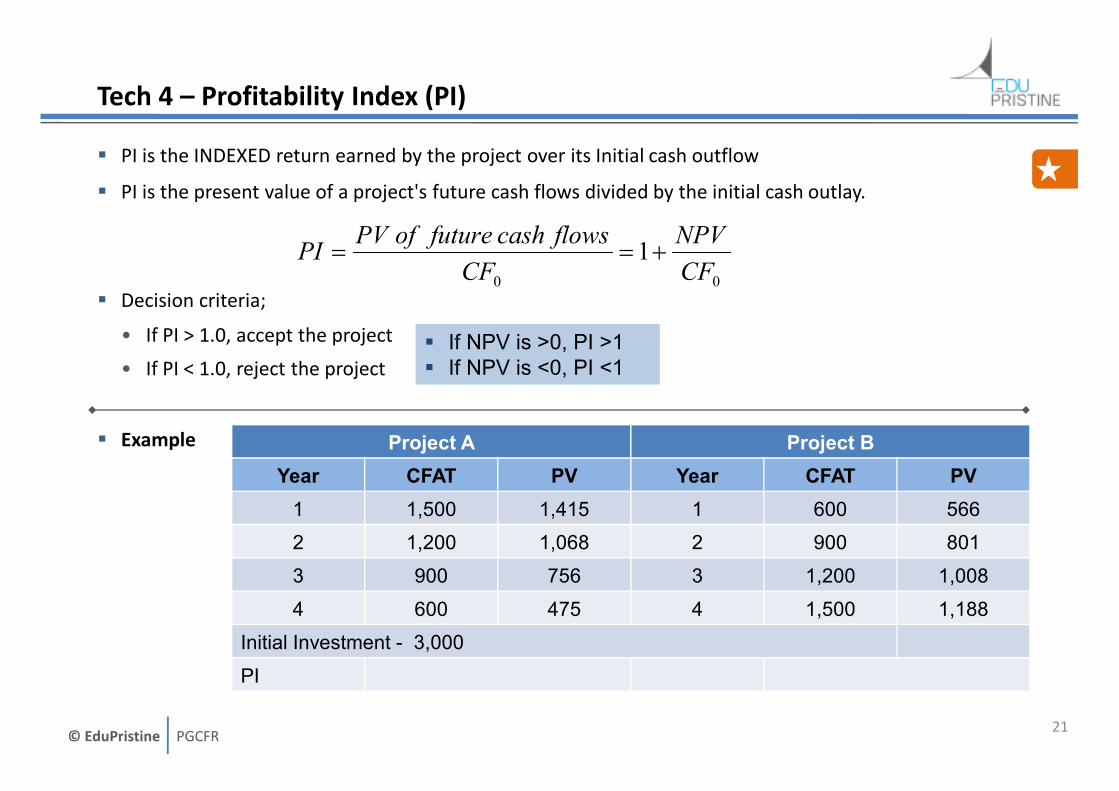

Tech 4 – Profitability Index (PI)

� PI is the INDEXED return earned by the project over its Initial cash outflow

� PI is the present value of a project's future cash flows divided by the initial cash outlay.

� Decision criteria;

• If PI > 1.0, accept the project

• If PI < 1.0, reject the project

� Example

21

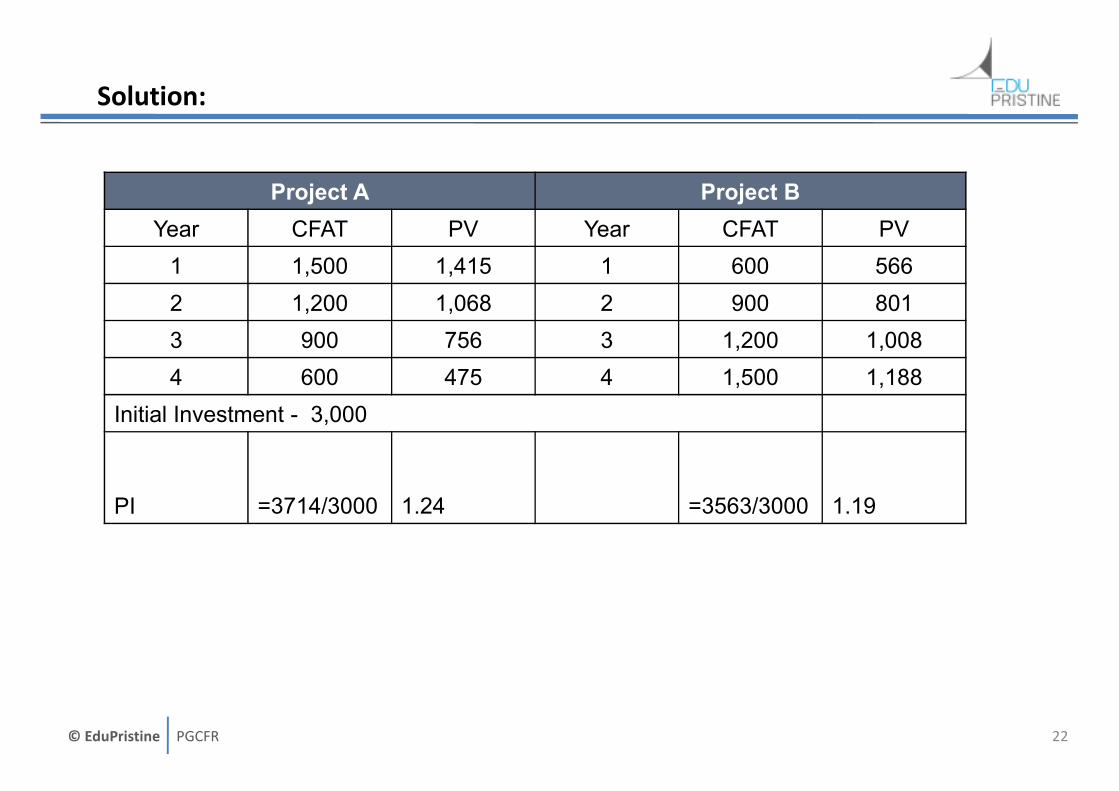

Project A Project B

Year CFAT PV Year CFAT PV

1 1,500 1,415 1 600 566

2 1,200 1,068 2 900 801

3 900 756 3 1,200 1,008

4 600 475 4 1,500 1,188

Initial Investment - 3,000

PI

00

1CF

NPV

CF

flowscashfutureofPVPI +==

� If NPV is >0, PI >1

� If NPV is <0, PI <1

© EduPristine PGCFR

Solution:

22

Project A Project B

Year CFAT PV Year CFAT PV

1 1,500 1,415 1 600 566

2 1,200 1,068 2 900 801

3 900 756 3 1,200 1,008

4 600 475 4 1,500 1,188

Initial Investment - 3,000

PI =3714/3000 1.24 =3563/3000 1.19

© EduPristine PGCFR

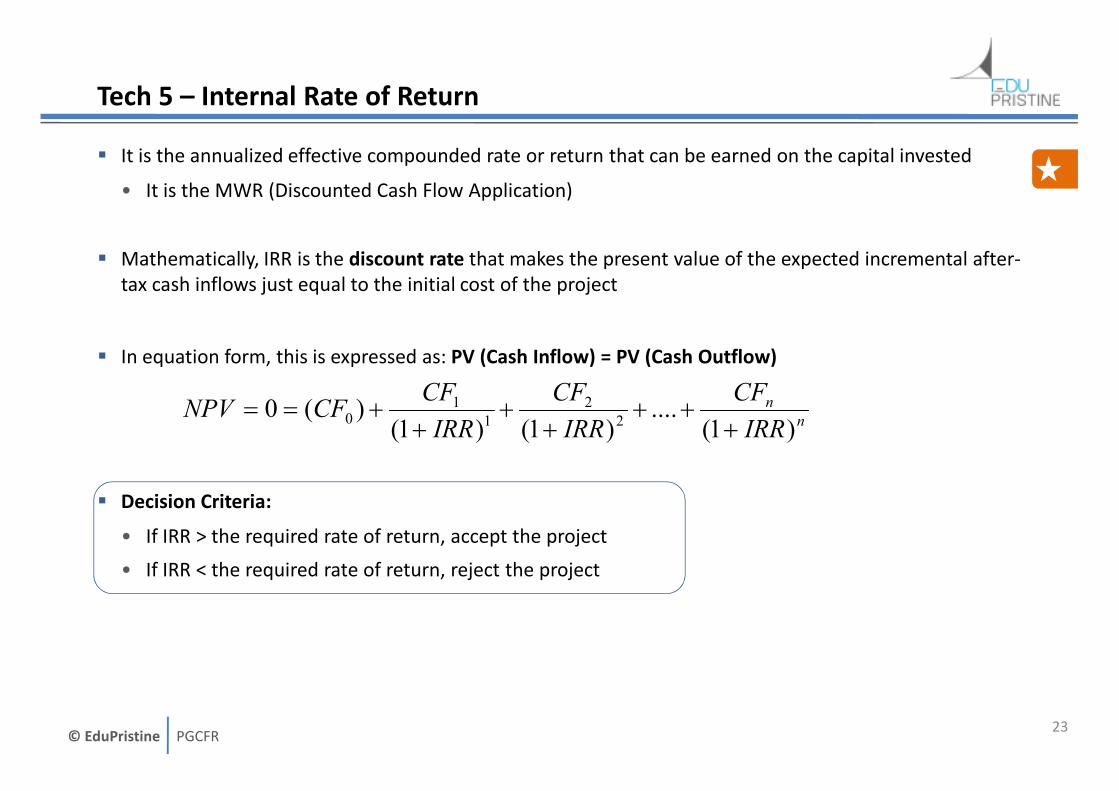

Tech 5 – Internal Rate of Return

� It is the annualized effective compounded rate or return that can be earned on the capital invested

• It is the MWR (Discounted Cash Flow Application)

� Mathematically, IRR is the discount rate that makes the present value of the expected incremental after-

tax cash inflows just equal to the initial cost of the project

� In equation form, this is expressed as: PV (Cash Inflow) = PV (Cash Outflow)

� Decision Criteria:

• If IRR > the required rate of return, accept the project

• If IRR < the required rate of return, reject the project

23

n

n

IRR

CF

IRR

CF

IRR

CFCFNPV

)1(....

)1()1()(0

2

2

1

10 +

+++

++

+==

© EduPristine PGCFR

Example 3

24

Project A Project B

Year CFAT Year CFAT

1 12,000 1 22,000

2 14,000 2 20,000

3 16,000 3 16,000

4 20,000 4 14,000

5 22,000 5 12,000

Cash Flows 84,000 84,000

Initial Investment – 60,000

NPV ? ?

IRR ? ?

© EduPristine PGCFR

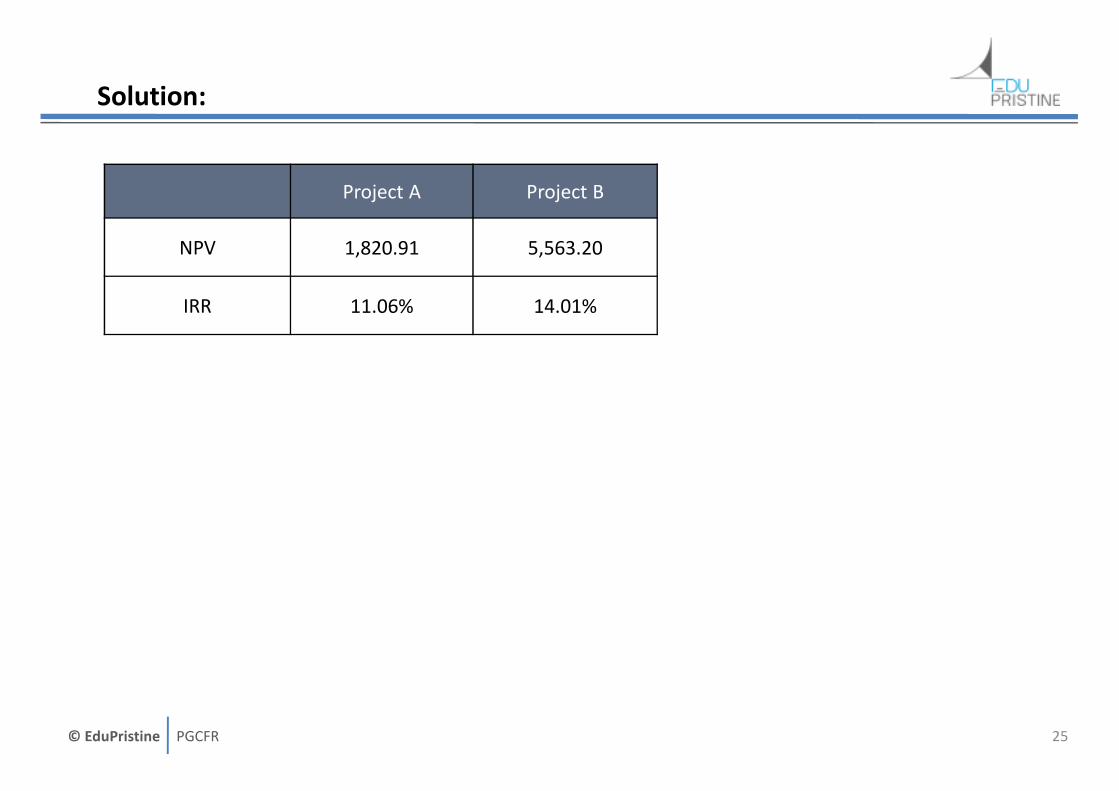

Solution:

25

Project A Project B

NPV 1,820.91 5,563.20

IRR 11.06% 14.01%

© EduPristine PGCFR

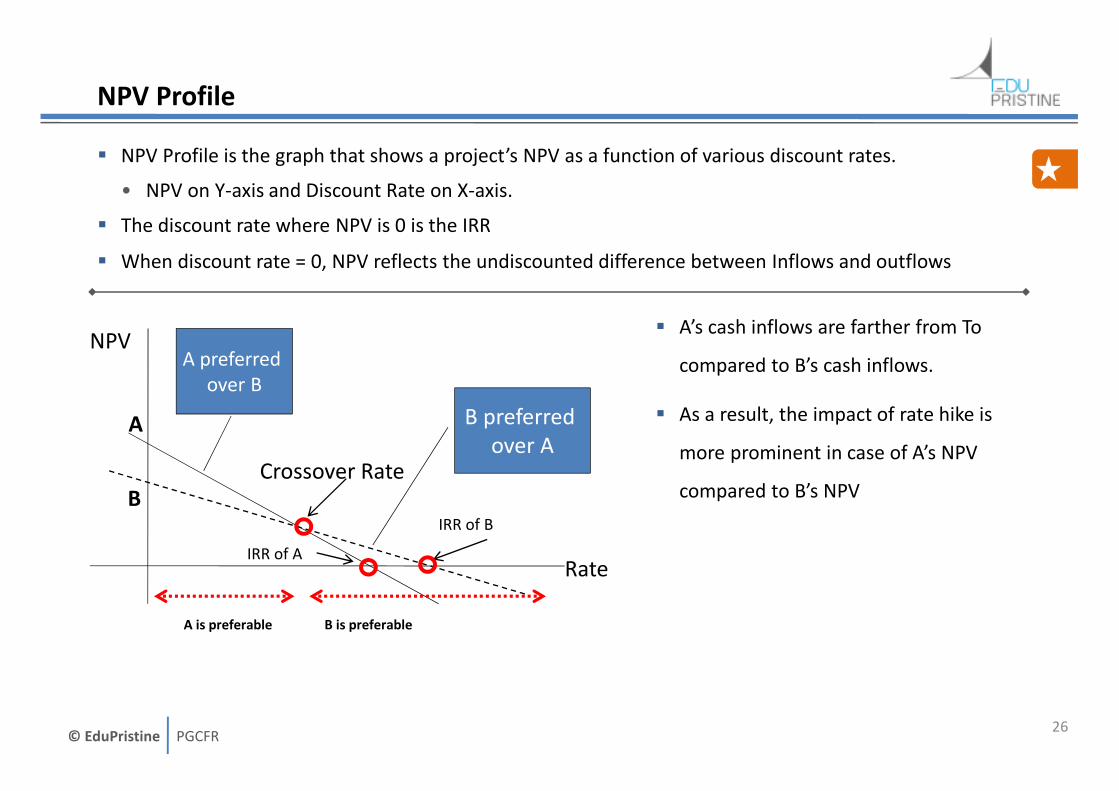

NPV Profile

� NPV Profile is the graph that shows a project’s NPV as a function of various discount rates.

• NPV on Y-axis and Discount Rate on X-axis.

� The discount rate where NPV is 0 is the IRR

� When discount rate = 0, NPV reflects the undiscounted difference between Inflows and outflows

26

A

BCrossover Rate

IRR of A

IRR of B

NPVA preferred

over B

B preferred

over A

Rate

A is preferable B is preferable

� A’s cash inflows are farther from To

compared to B’s cash inflows.

� As a result, the impact of rate hike is

more prominent in case of A’s NPV

compared to B’s NPV

© EduPristine PGCFR

IRR vs NPV

� For conventional projects, the NPV and IRR will agree on whether to invest or not to invest.

� NPV and IRR may give conflicting results for different project sizes: Choose NPV

� Limitations of IRR

• Size effect ignored by IRR

• Multiple IRR or No IRR problem

• IRR assumes yearly returns are invested at the IRR which may not be possible most of the times

27

© EduPristine PGCFR

Preference of Capital Budgeting Methods

1. Financial textbooks preach the superiority of the NPV and IRR methods.

2. In Europe, Pay Back Period is used more often than IRR and NPV.

3. Larger companies prefer to use the NPV, IRR methods

4. Private corporations used the payback period more frequently than public corporations

5. Companies managed by MBA’s had stronger preferences for discounted cash flow techniques (NPV and

IRR methods)

28

© EduPristine PGCFR

Other Concepts - Projects with Unequal lives

� When the options that are being evaluated are of different tenure (project life), we need to make an

adjustment

� The objective of this adjustment is to make like-to-like comparison between both the projects removing

the impact of unequal lives .

Methods that can be used:

A. Least common multiple of lives approach

Example: Project Eagle of 6 years and Project Bird of 3 years. Since LCM of both the projects complete

duration is 6, calculate NPV/IRR from Project Eagle as usual and for Project Bird assume the project

restarts at the end of 3rd year. So in effect Project Bird will have to be repeated twice for a like to like

comparison with Project Eagle

B. Equivalent Annual Annuity Approach – Simpler approach

Step 1: It basically calculates the sequence of annual payments (annuities) that is equal to the project’s

NPV.

Step 2: The project which has higher annuity is selected

29

© EduPristine PGCFR

Other Concepts – NPV and Share Price

� NPV is the addition to shareholders wealth (at To) by taking an action and discounting its CFs using

WACC

� Wealth of the shareholders is measured by the share price

� Therefore by Fundamental Analysis, NPV is addition in the Market capitalization at To

� The value of the company is the value of existing investments plus the NPV of all future investments.

� If a project has an NPV of $250 Mn and the current value of the company is $5,000 Mn (100 Mn

outstanding shares), the total market cap will increase by $250 Mn.

• Share price should increase by $2.5 ($250 Mn divided by 100Mn)

• New share price will be $50 + $2.5 = $52.5

3030

Because of speculations and other forces prevailing in the capital market,

the above relation might not hold true at all time

© EduPristine PGCFR

Other Concepts – Capital rationing

� Firms/Companies have fixed amount of capital to allocate amongst capital projects

� Capital rationing is the allocation of this fixed amount of capital among the set of available projects such

that the selection will maximize shareholder’s wealth

� Project’s with negative NPVs are to be discarded irrespective of availability of capital

1. Hard capital rationing – funds allocated to the manager of capital project cannot be increased

2. Soft capital rationing – manager of capital project is allowed to increase allocated capital budget

provided they can justify to senior management of creating shareholder value on that additional

capital

3131

Profitability Index is used to rank projects on the basis of their relative returns

© EduPristine PGCFR

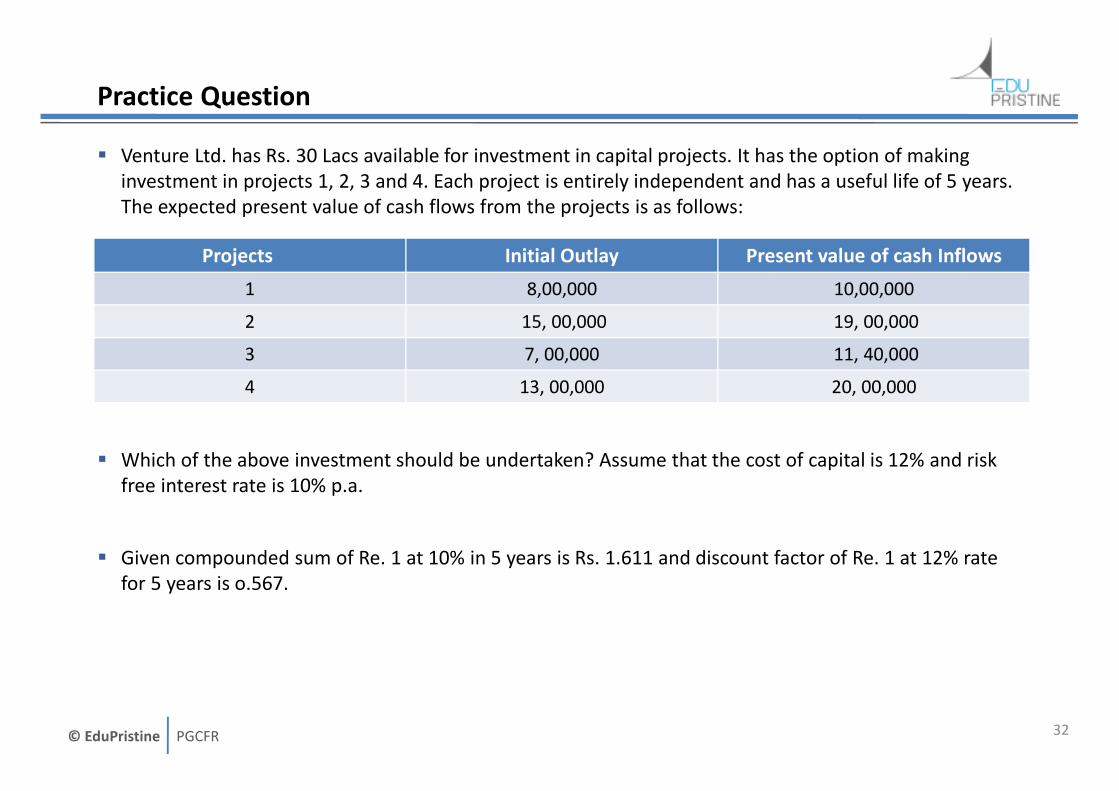

Practice Question

� Venture Ltd. has Rs. 30 Lacs available for investment in capital projects. It has the option of making

investment in projects 1, 2, 3 and 4. Each project is entirely independent and has a useful life of 5 years.

The expected present value of cash flows from the projects is as follows:

� Which of the above investment should be undertaken? Assume that the cost of capital is 12% and risk

free interest rate is 10% p.a.

� Given compounded sum of Re. 1 at 10% in 5 years is Rs. 1.611 and discount factor of Re. 1 at 12% rate

for 5 years is o.567.

32

Projects Initial Outlay Present value of cash Inflows

1 8,00,000 10,00,000

2 15, 00,000 19, 00,000

3 7, 00,000 11, 40,000

4 13, 00,000 20, 00,000

© EduPristine PGCFR

Other Concepts – Project Sequencing

Project Sequencing

� Sequenced through time so that investing in a project creates the option to invest in future projects.

� Example: A chemical company can first select a project of establishing the chemical plant & then to use

the excess heat of chemicals it can establish a chemical power plant

33

© EduPristine PGCFR

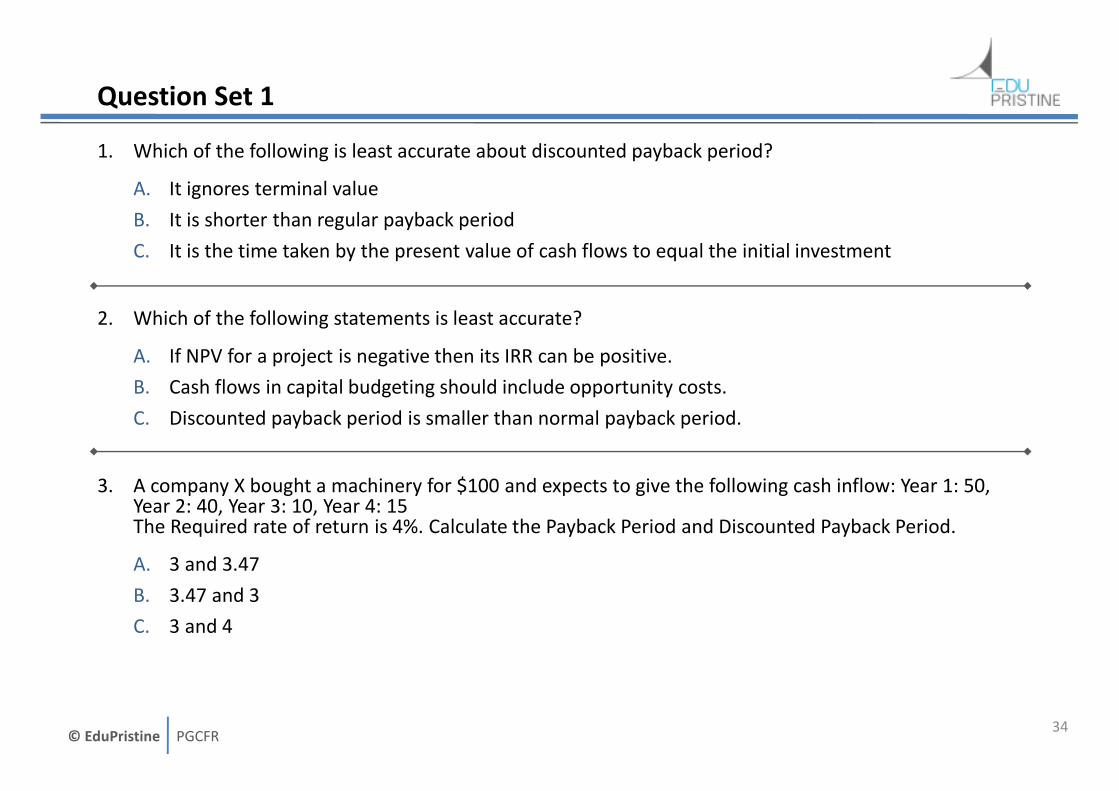

Question Set 1

1. Which of the following is least accurate about discounted payback period?

A. It ignores terminal value

B. It is shorter than regular payback period

C. It is the time taken by the present value of cash flows to equal the initial investment

2. Which of the following statements is least accurate?

A. If NPV for a project is negative then its IRR can be positive.

B. Cash flows in capital budgeting should include opportunity costs.

C. Discounted payback period is smaller than normal payback period.

3. A company X bought a machinery for $100 and expects to give the following cash inflow: Year 1: 50, Year 2: 40, Year 3: 10, Year 4: 15The Required rate of return is 4%. Calculate the Payback Period and Discounted Payback Period.

A. 3 and 3.47

B. 3.47 and 3

C. 3 and 4

34

© EduPristine PGCFR

Question Set 1 (Contd.)

4. If a four-year project having payback period of 2.5 years then

A. IRR will be higher than the cost of capital

B. NPV will be positive

C. None of the above

5. Sigma Tech has a net worth of $4 million and Global Inc has a net worth of $500 million. Which of the

following methods of capital budgeting is most likely to be used by these companies?

A. Sigma should use the NPV method

B. Global should use the discounted payback method

C. Sigma should follow the discounted payback method

35

© EduPristine PGCFR

Solutions (Q.Set1)

1. Solution: BIt is shorter than regular payback period

2. Solution: CIf the cost of capital >IRR then NPV can be negative whatever is the value of IRR.Cash flows should include opportunity costs.Discounted payback period is larger than normal payback period because future cash flows are discounted and their PV is less than undiscounted value.

3. The correct answer is 3 and 3.47.

4. The correct answer is C.

5. Solution: CSigma is a smaller company as compared to Global, hence is more likely to follow the discounted payback method.

36

© EduPristine PGCFR

Question Set 2

1. In the capital budgeting process, three of the major steps are:

A. Analyze the project proposal, create firm wide capital budget and monitor decisions.

B. Analyze the project proposal, raise capital and monitor project performance.

C. Analyze the project proposal, create firm wide capital budget and raise capital

2. Which of the following costs is least likely to be used in capital budgeting analysis?

A. Fees paid to a marketing research firm to estimate the demand for a new product prior to a decision on the project.

B. Cannibalization of its existing product market due to the launch of another product by a firm.

C. The tax saving affect of depreciation cost.

3. Which of the following is true about Cannibalization:

A. It’s a positive externality

B. It’s a negative externality

C. It’s not an externality

37

© EduPristine PGCFR

Question Set 2 (Contd.)

4. With regards to capital budgeting, an appropriate estimate of the incremental cash flows from a

project is least likely to include:

A. Interest Costs

B. Externalities

C. Opportunity Costs

5. The effects that the acceptance of a project may have on firm’s other cash flows is known as:

A. Opportunity Cost

B. Externalities

C. Sunk Cost

38

© EduPristine PGCFR

Solutions (Q.Set2)

1. Solution: A

Capital budgeting has 4 steps. In none of the steps capital is raised in capital budgeting process.

2. Solution: A

Fees paid to a marketing research firm to estimate the demand for a new product prior to a decision

on the project is a sunk cost and should not be included in the capital budgeting analysis.

3. The correct answer is It’s a negative externality.

4. The correct answer is Interest Costs.

5. Solution: B

Opportunity Cost: Cash flows that a firm will lose by undertaking the project

Sunk Cost: Costs that cannot be avoided, even if the project is not undertaken

39

© EduPristine PGCFR

Question Set 3

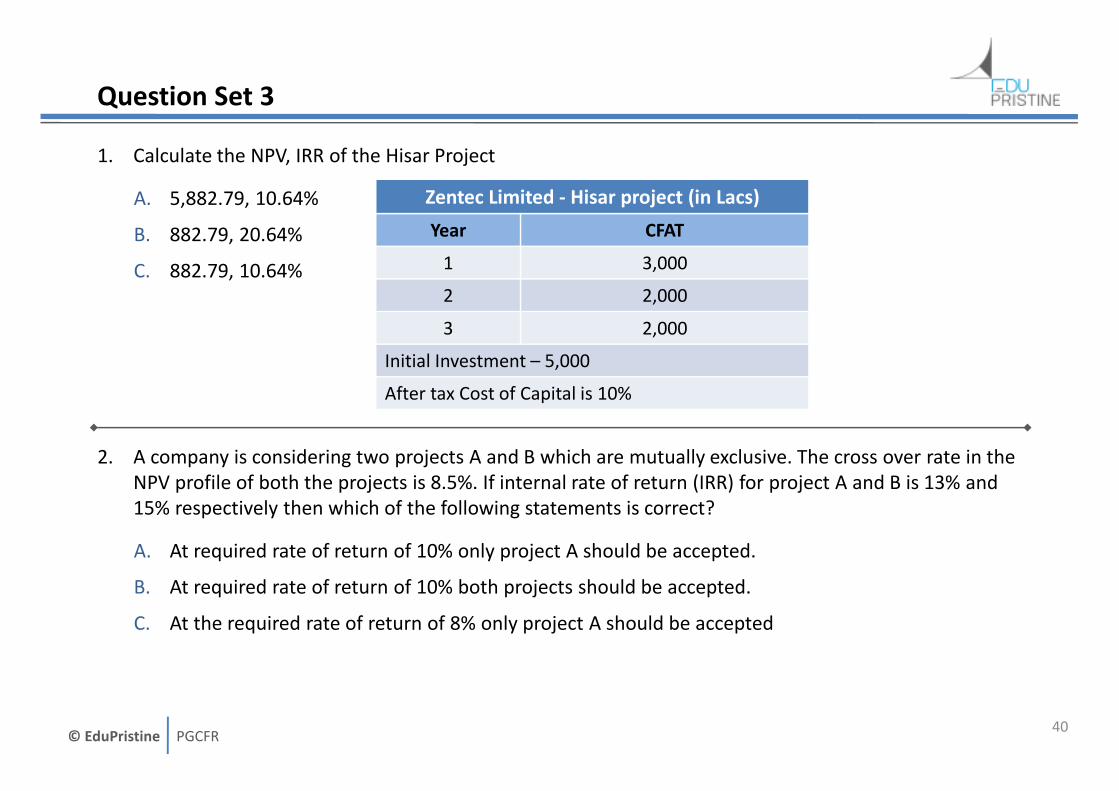

1. Calculate the NPV, IRR of the Hisar Project

A. 5,882.79, 10.64%

B. 882.79, 20.64%

C. 882.79, 10.64%

2. A company is considering two projects A and B which are mutually exclusive. The cross over rate in the

NPV profile of both the projects is 8.5%. If internal rate of return (IRR) for project A and B is 13% and

15% respectively then which of the following statements is correct?

A. At required rate of return of 10% only project A should be accepted.

B. At required rate of return of 10% both projects should be accepted.

C. At the required rate of return of 8% only project A should be accepted

40

Zentec Limited - Hisar project (in Lacs)

Year CFAT

1 3,000

2 2,000

3 2,000

Initial Investment – 5,000

After tax Cost of Capital is 10%

© EduPristine PGCFR

Question Set 3 (Contd.)

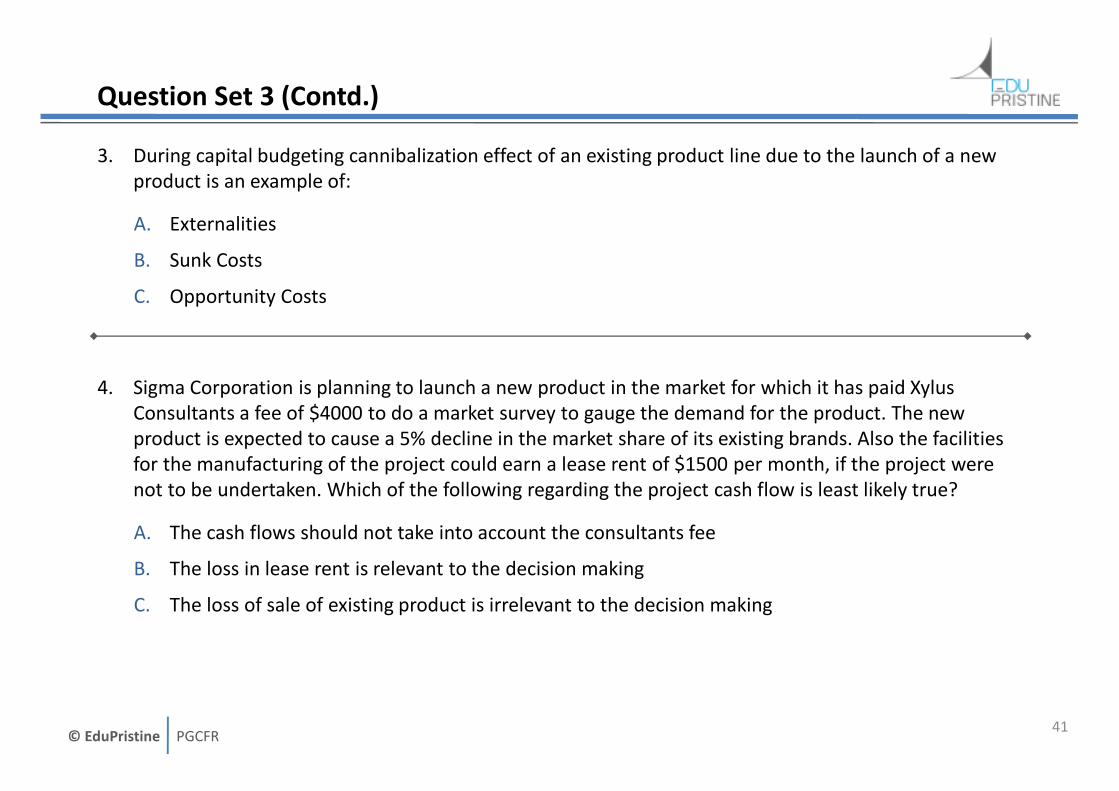

3. During capital budgeting cannibalization effect of an existing product line due to the launch of a new

product is an example of:

A. Externalities

B. Sunk Costs

C. Opportunity Costs

4. Sigma Corporation is planning to launch a new product in the market for which it has paid Xylus

Consultants a fee of $4000 to do a market survey to gauge the demand for the product. The new

product is expected to cause a 5% decline in the market share of its existing brands. Also the facilities

for the manufacturing of the project could earn a lease rent of $1500 per month, if the project were

not to be undertaken. Which of the following regarding the project cash flow is least likely true?

A. The cash flows should not take into account the consultants fee

B. The loss in lease rent is relevant to the decision making

C. The loss of sale of existing product is irrelevant to the decision making

41

© EduPristine PGCFR

Solutions (Q.Set3)

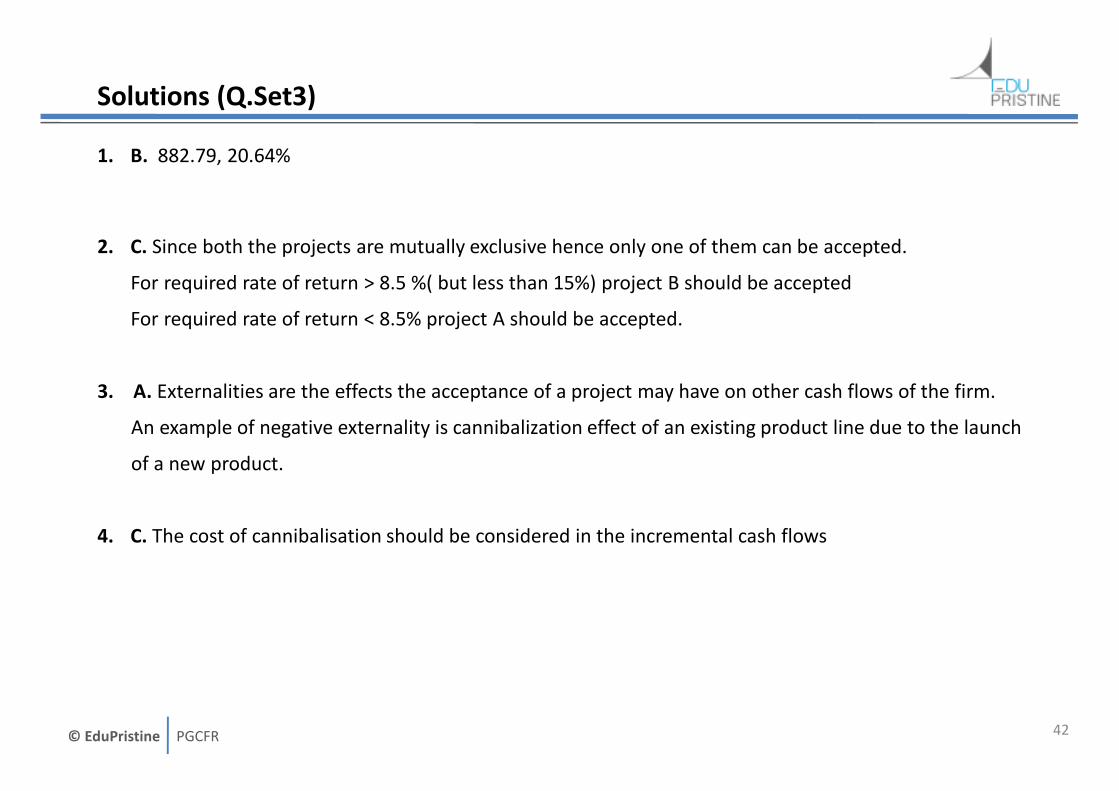

1. B. 882.79, 20.64%

2. C. Since both the projects are mutually exclusive hence only one of them can be accepted.

For required rate of return > 8.5 %( but less than 15%) project B should be accepted

For required rate of return < 8.5% project A should be accepted.

3. A. Externalities are the effects the acceptance of a project may have on other cash flows of the firm.

An example of negative externality is cannibalization effect of an existing product line due to the launch

of a new product.

4. C. The cost of cannibalisation should be considered in the incremental cash flows

42

© EduPristine PGCFR

Cost of Capital

43

© EduPristine PGCFR

Coverage of the topic - Cost of Capital

1. Context for Cost of Capital

2. Different Components of Capital

3. Cost of individual Components of Capital

4. Weighted average cost of capital (WACC)

5. Marginal cost of capital (MCC)

6. Other Topics

A. Calculating βeta for the project

B. Country equity risk premium (CRP)

C. Treatment of floatation costs

44

© EduPristine PGCFR

Context for cost of capital

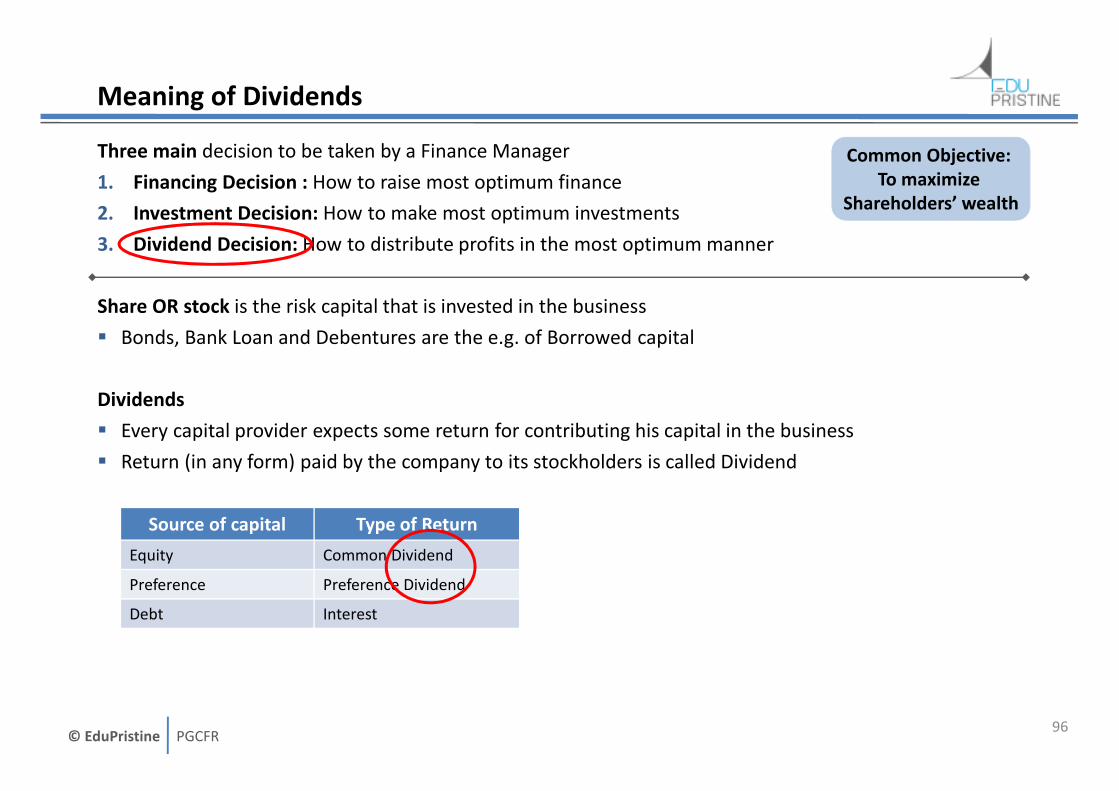

� Three main decision to be taken by a Finance Manager

• Financing Decision: How to raise most optimum finance

• Investment Decision: How to make most optimum investments

• Dividend Decision: How to distribute profits in the most optimum manner

� Financing and Investing decisions are independent: there is no one to one relationship between every

action of both decisions

� In evaluating investing decisions, there is need for an opportunity cost against which the returns from

the project / asset can be compared with

• This opportunity cost is genesis of Cost of Capital

45

Common Objective:

To maximize

Shareholders’ wealth

© EduPristine PGCFR

Cost of Capital - Meaning

Different ways to understand the meaning of cost of capital:

1. The rate of return that the suppliers of capital, bondholders and owners, require as a compensation for

their contribution of capital

2. The cost to finance assets of the firm

3. The minimum rate which the assets of the firm must earn to add to shareholders wealth

4. The opportunity cost which is used as a benchmark to evaluate capital projects

5. WACC reflects the average risk of projects that make up the firm

46

© EduPristine PGCFR

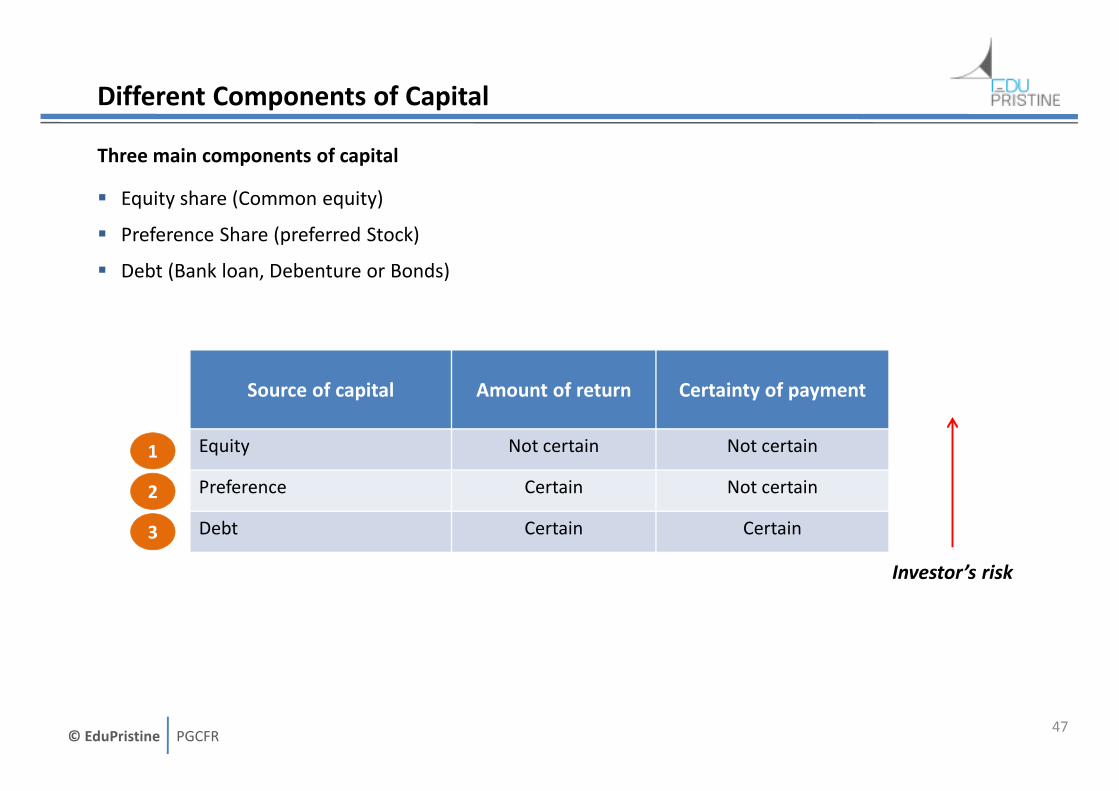

Different Components of Capital

Three main components of capital

� Equity share (Common equity)

� Preference Share (preferred Stock)

� Debt (Bank loan, Debenture or Bonds)

47

Source of capital Amount of return Certainty of payment

Equity Not certain Not certain

Preference Certain Not certain

Debt Certain Certain

1

2

3

Investor’s risk

© EduPristine PGCFR

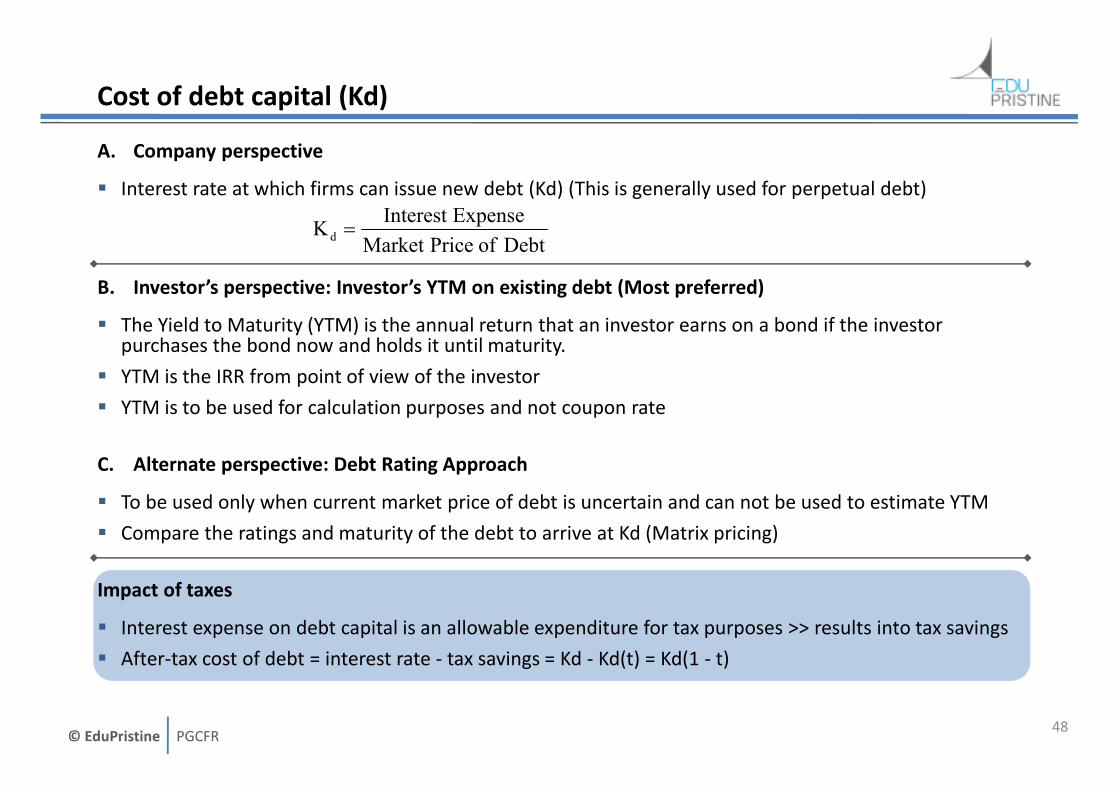

Cost of debt capital (Kd)

A. Company perspective

� Interest rate at which firms can issue new debt (Kd) (This is generally used for perpetual debt)

B. Investor’s perspective: Investor’s YTM on existing debt (Most preferred)

� The Yield to Maturity (YTM) is the annual return that an investor earns on a bond if the investor purchases the bond now and holds it until maturity.

� YTM is the IRR from point of view of the investor

� YTM is to be used for calculation purposes and not coupon rate

C. Alternate perspective: Debt Rating Approach

� To be used only when current market price of debt is uncertain and can not be used to estimate YTM

� Compare the ratings and maturity of the debt to arrive at Kd (Matrix pricing)

Impact of taxes

� Interest expense on debt capital is an allowable expenditure for tax purposes >> results into tax savings

� After-tax cost of debt = interest rate - tax savings = Kd - Kd(t) = Kd(1 - t)

48

Debt of PriceMarket

ExpenseInterest K d =

© EduPristine PGCFR

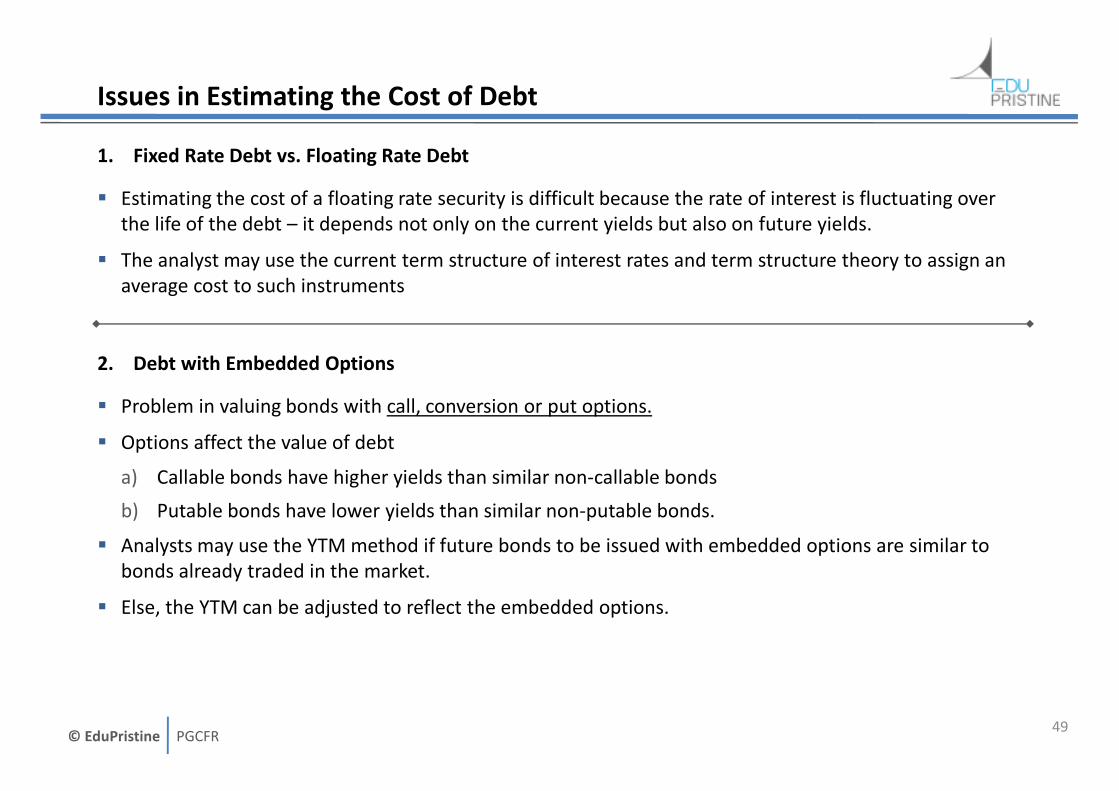

Issues in Estimating the Cost of Debt

1. Fixed Rate Debt vs. Floating Rate Debt

� Estimating the cost of a floating rate security is difficult because the rate of interest is fluctuating over

the life of the debt – it depends not only on the current yields but also on future yields.

� The analyst may use the current term structure of interest rates and term structure theory to assign an

average cost to such instruments

2. Debt with Embedded Options

� Problem in valuing bonds with call, conversion or put options.

� Options affect the value of debt

a) Callable bonds have higher yields than similar non-callable bonds

b) Putable bonds have lower yields than similar non-putable bonds.

� Analysts may use the YTM method if future bonds to be issued with embedded options are similar to

bonds already traded in the market.

� Else, the YTM can be adjusted to reflect the embedded options.

49

© EduPristine PGCFR

Issues in Estimating the Cost of Debt (Contd.)

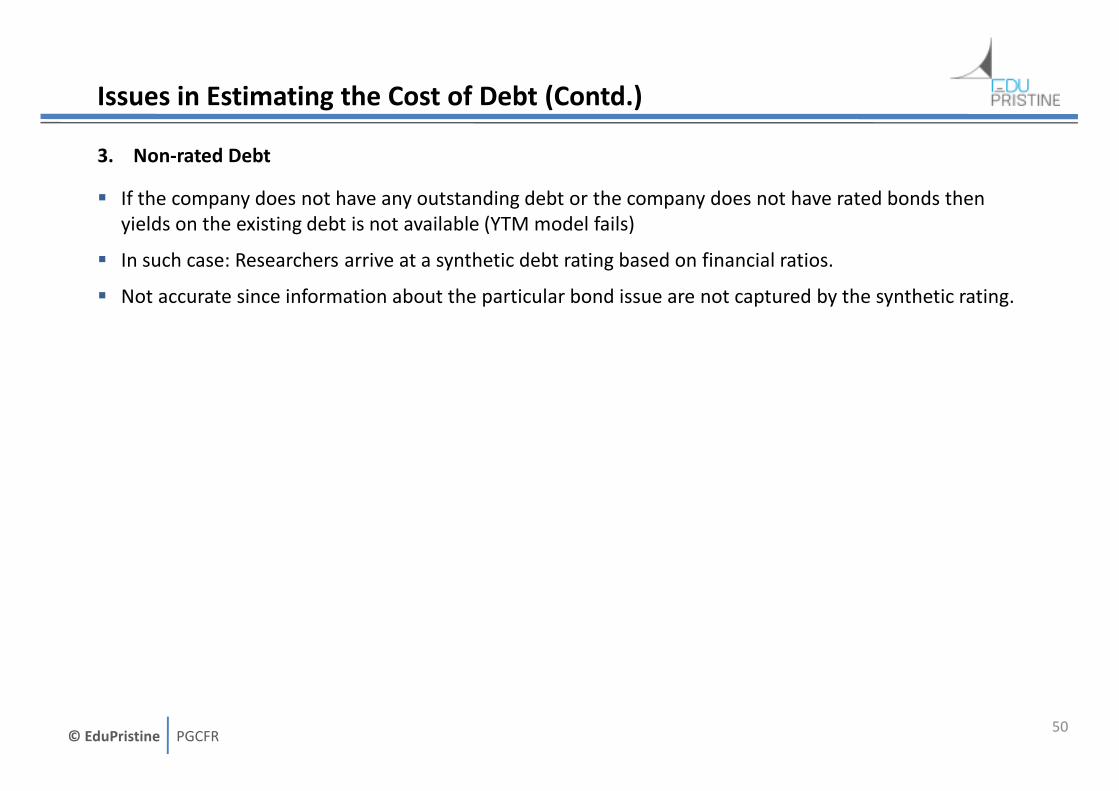

3. Non-rated Debt

� If the company does not have any outstanding debt or the company does not have rated bonds then

yields on the existing debt is not available (YTM model fails)

� In such case: Researchers arrive at a synthetic debt rating based on financial ratios.

� Not accurate since information about the particular bond issue are not captured by the synthetic rating.

50

© EduPristine PGCFR

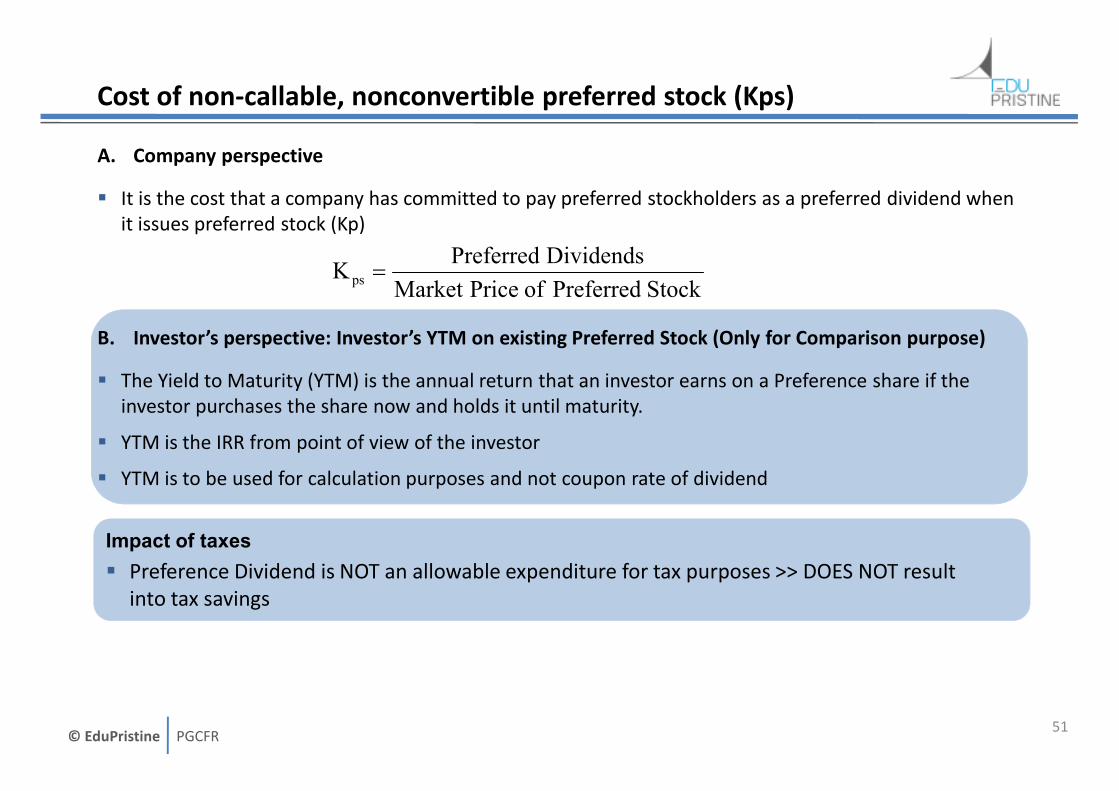

Cost of non-callable, nonconvertible preferred stock (Kps)

A. Company perspective

� It is the cost that a company has committed to pay preferred stockholders as a preferred dividend when

it issues preferred stock (Kp)

B. Investor’s perspective: Investor’s YTM on existing Preferred Stock (Only for Comparison purpose)

� The Yield to Maturity (YTM) is the annual return that an investor earns on a Preference share if the

investor purchases the share now and holds it until maturity.

� YTM is the IRR from point of view of the investor

� YTM is to be used for calculation purposes and not coupon rate of dividend

51

Stock Preferred of PriceMarket

Dividends PreferredK ps =

Impact of taxes

� Preference Dividend is NOT an allowable expenditure for tax purposes >> DOES NOT result

into tax savings

© EduPristine PGCFR

Cost of equity capital (Ke)

Ke can be calculated by three Approaches:

1. Capital asset pricing model (CAPM)

2. Dividend discount model (DDM)

3. Bond yield plus risk premium

52

Answer will be different by all three approaches

Impact of taxes

� Common Dividend is NOT an allowable expenditure for tax purposes >> DOES NOT result

into tax savings

© EduPristine PGCFR

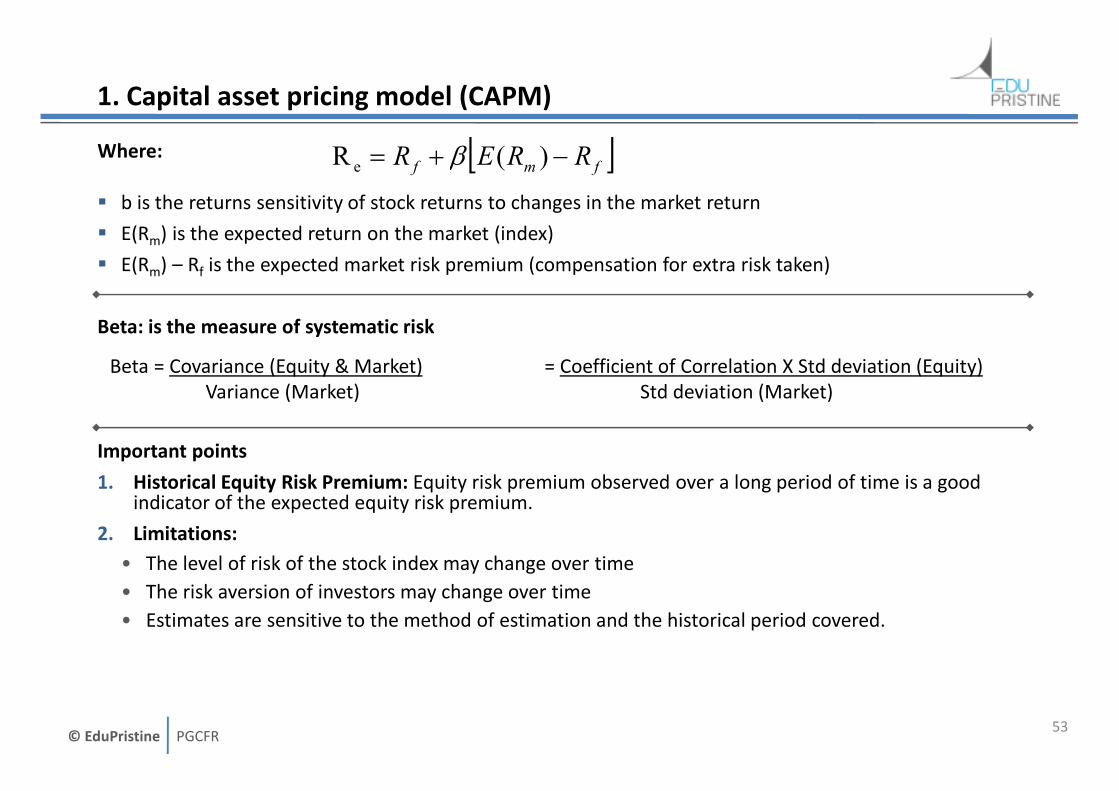

1. Capital asset pricing model (CAPM)

Where:

� b is the returns sensitivity of stock returns to changes in the market return

� E(Rm) is the expected return on the market (index)

� E(Rm) – Rf is the expected market risk premium (compensation for extra risk taken)

Beta: is the measure of systematic risk

Important points

1. Historical Equity Risk Premium: Equity risk premium observed over a long period of time is a good indicator of the expected equity risk premium.

2. Limitations:

• The level of risk of the stock index may change over time

• The risk aversion of investors may change over time

• Estimates are sensitive to the method of estimation and the historical period covered.

53

[ ]fmf RRER −+= )(R e β

Beta = Covariance (Equity & Market)

Variance (Market)

= Coefficient of Correlation X Std deviation (Equity)

Std deviation (Market)

© EduPristine PGCFR

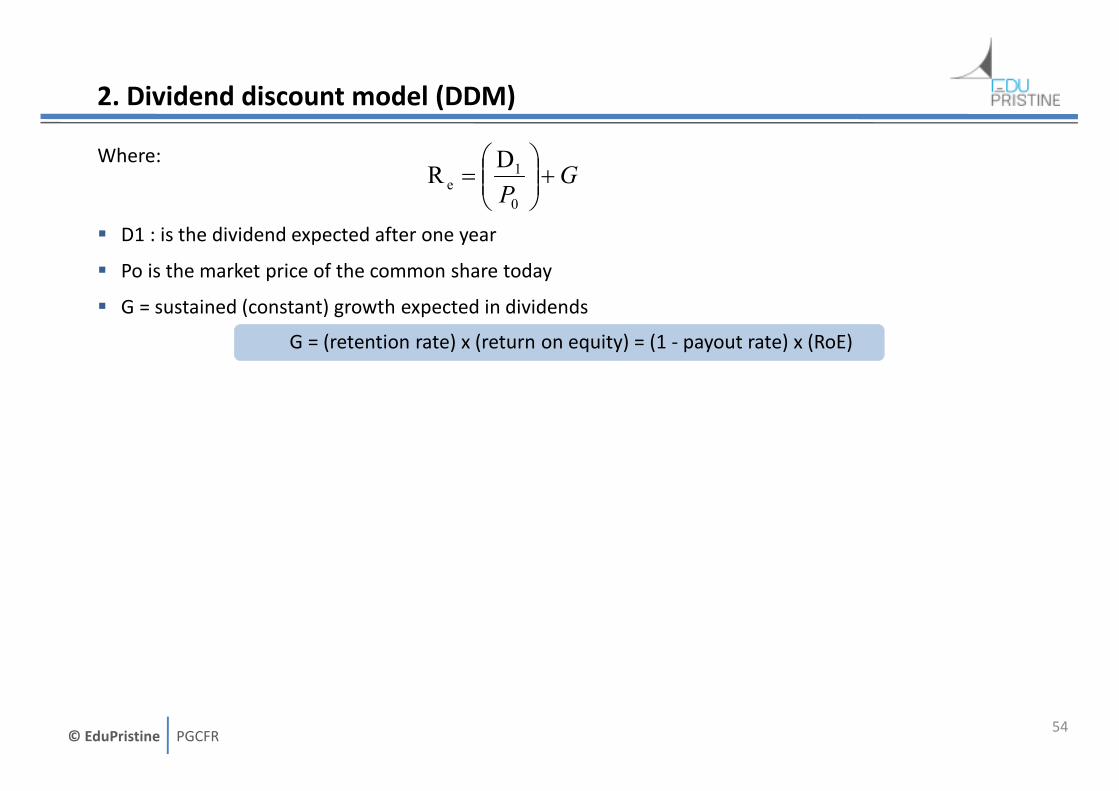

2. Dividend discount model (DDM)

Where:

� D1 : is the dividend expected after one year

� Po is the market price of the common share today

� G = sustained (constant) growth expected in dividends

G = (retention rate) x (return on equity) = (1 - payout rate) x (RoE)

54

GP

+

=

0

1e

DR

© EduPristine PGCFR

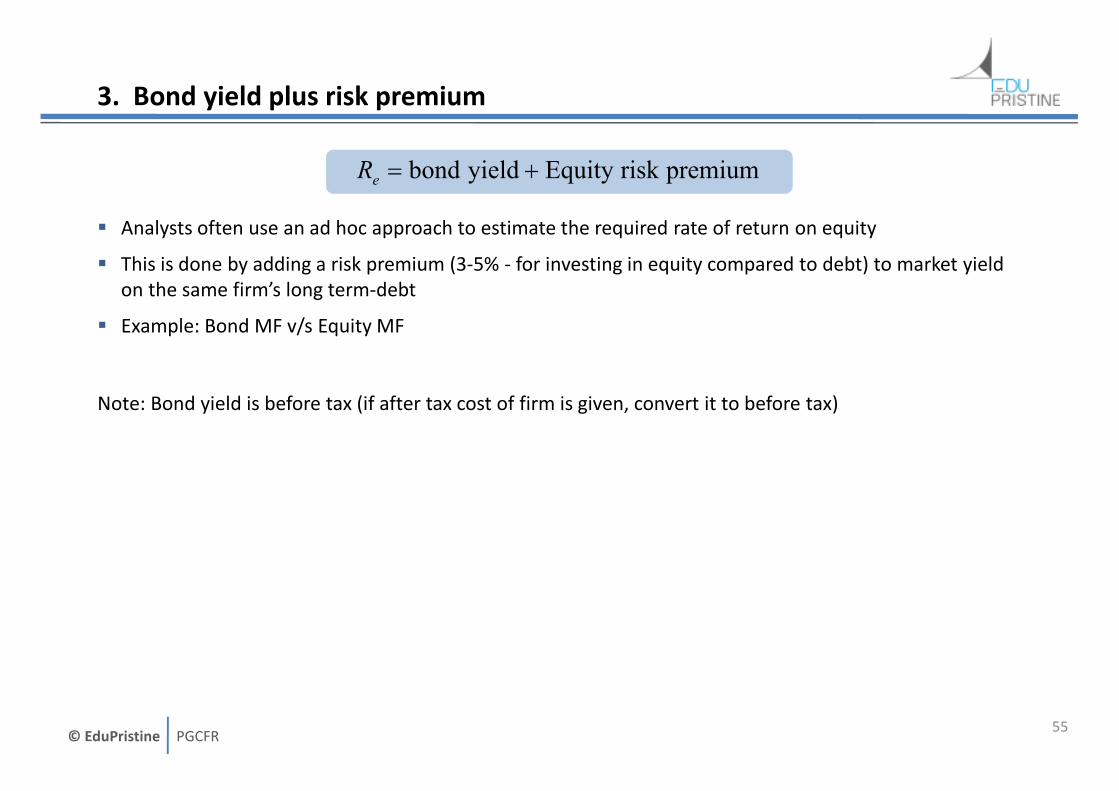

3. Bond yield plus risk premium

� Analysts often use an ad hoc approach to estimate the required rate of return on equity

� This is done by adding a risk premium (3-5% - for investing in equity compared to debt) to market yield

on the same firm’s long term-debt

� Example: Bond MF v/s Equity MF

Note: Bond yield is before tax (if after tax cost of firm is given, convert it to before tax)

55

premiumrisk Equity yield bond +=eR

© EduPristine PGCFR

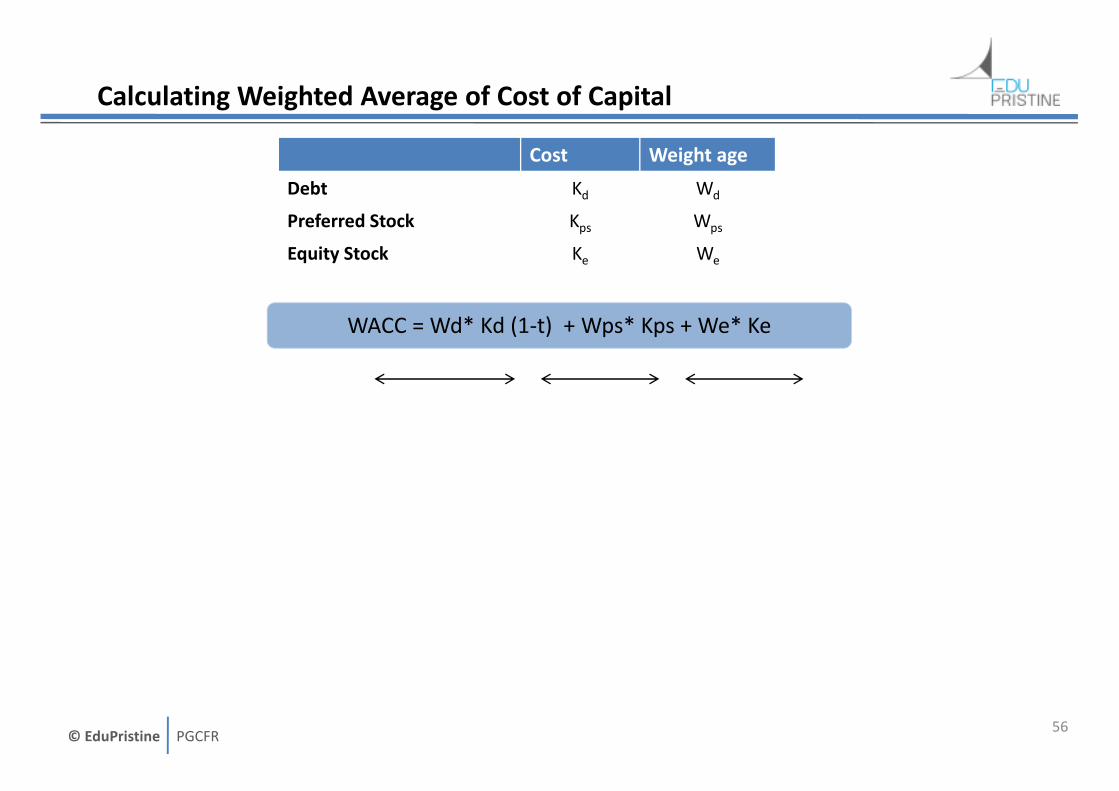

Calculating Weighted Average of Cost of Capital

WACC = Wd* Kd (1-t) + Wps* Kps + We* Ke

56

Cost Weight age

Debt Kd Wd

Preferred Stock Kps Wps

Equity Stock Ke We

© EduPristine PGCFR

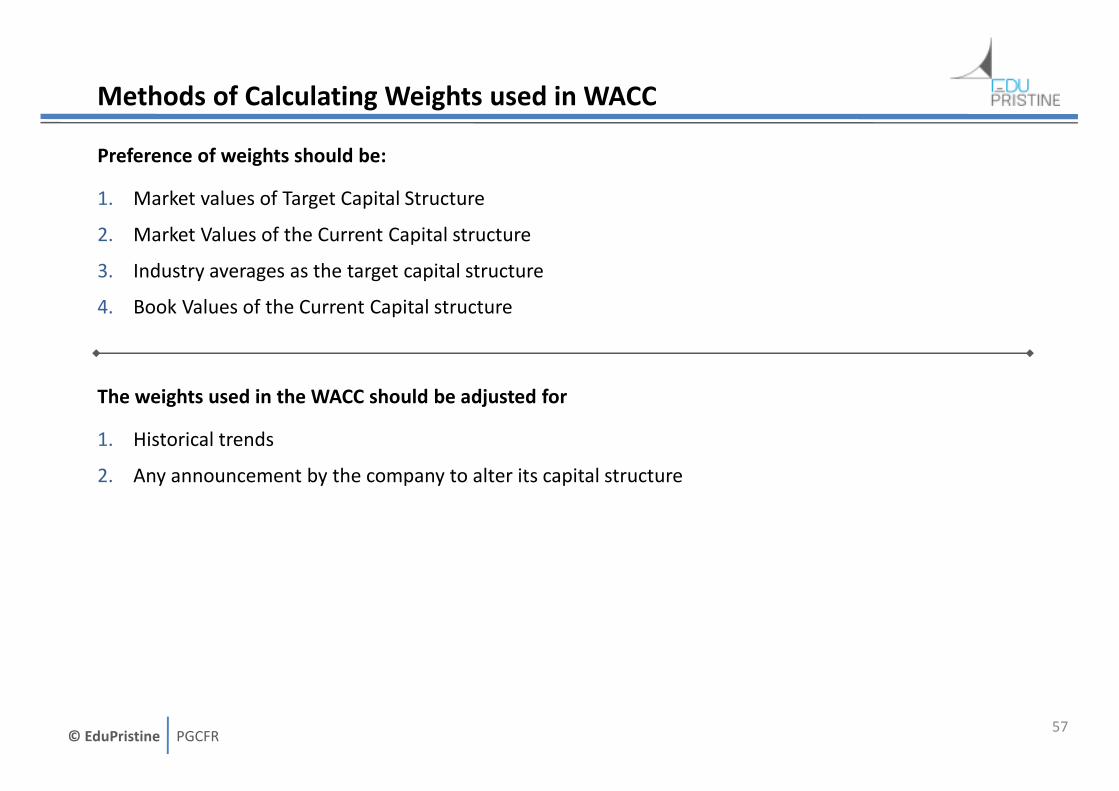

Methods of Calculating Weights used in WACC

Preference of weights should be:

1. Market values of Target Capital Structure

2. Market Values of the Current Capital structure

3. Industry averages as the target capital structure

4. Book Values of the Current Capital structure

The weights used in the WACC should be adjusted for

1. Historical trends

2. Any announcement by the company to alter its capital structure

57

© EduPristine PGCFR

Marginal Cost of Capital - Coverage

1. Basic Explanation

2. Optimal Capital Budget

3. Break points

4. MCC Schedule`

58

© EduPristine PGCFR

Marginal Cost of Capital - Basic Meaning

� MCC is the cost of incremental capital raised by the firm

� In other words, what it would cost to raise additional funds for the potential investment project.

Let us identify the difference between WACC and MCC

� A company wants to raise capital for an expansion plan for setting up new factory.

� Although the existing debt is at 12%, any additional debt can be raised at 14%.

� New shares will involve an issue cost of Rs. 2.5 per share.

Calculate Average and Marginal Marks of the studentss

59

Particulars S 1 S 2 S 3 S 4 S 5

Marks obtained 80 75 100 50 80

© EduPristine PGCFR

Optimal Capital Budget

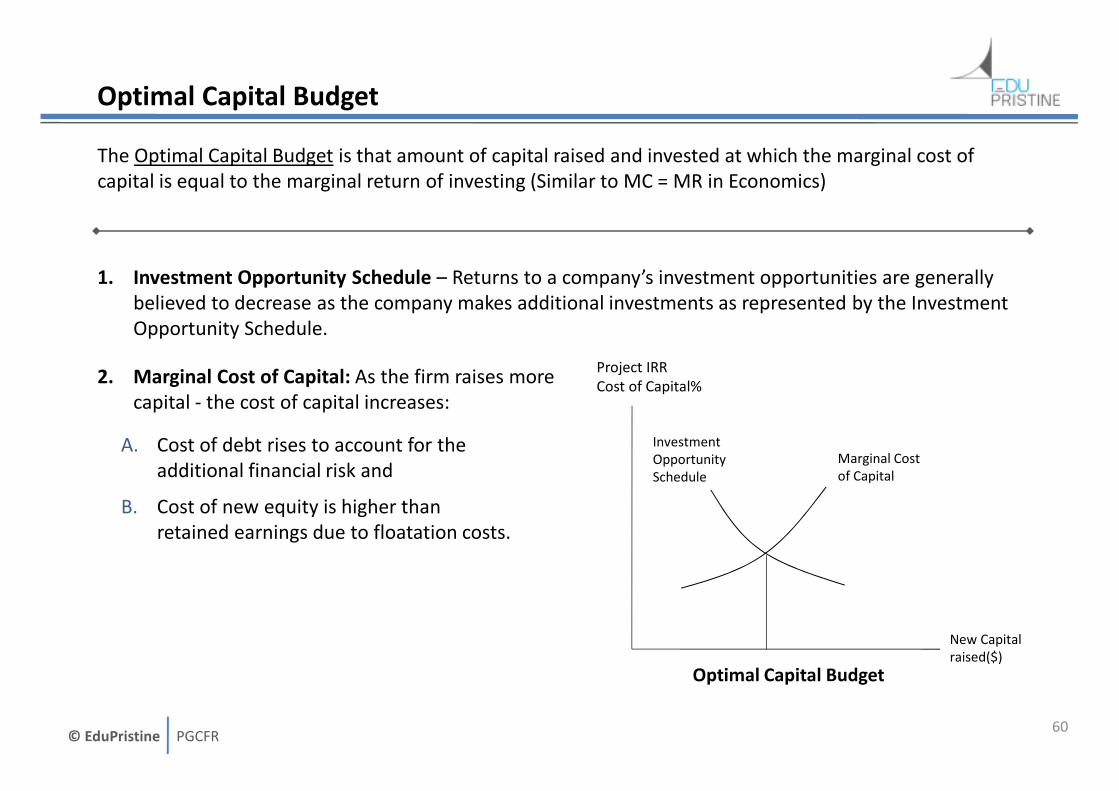

The Optimal Capital Budget is that amount of capital raised and invested at which the marginal cost of

capital is equal to the marginal return of investing (Similar to MC = MR in Economics)

1. Investment Opportunity Schedule – Returns to a company’s investment opportunities are generally

believed to decrease as the company makes additional investments as represented by the Investment

Opportunity Schedule.

2. Marginal Cost of Capital: As the firm raises more

capital - the cost of capital increases:

A. Cost of debt rises to account for the

additional financial risk and

B. Cost of new equity is higher than

retained earnings due to floatation costs.

60

Marginal Cost

of Capital

Investment

Opportunity

Schedule

Project IRR

Cost of Capital%

New Capital

raised($)

Optimal Capital Budget

© EduPristine PGCFR

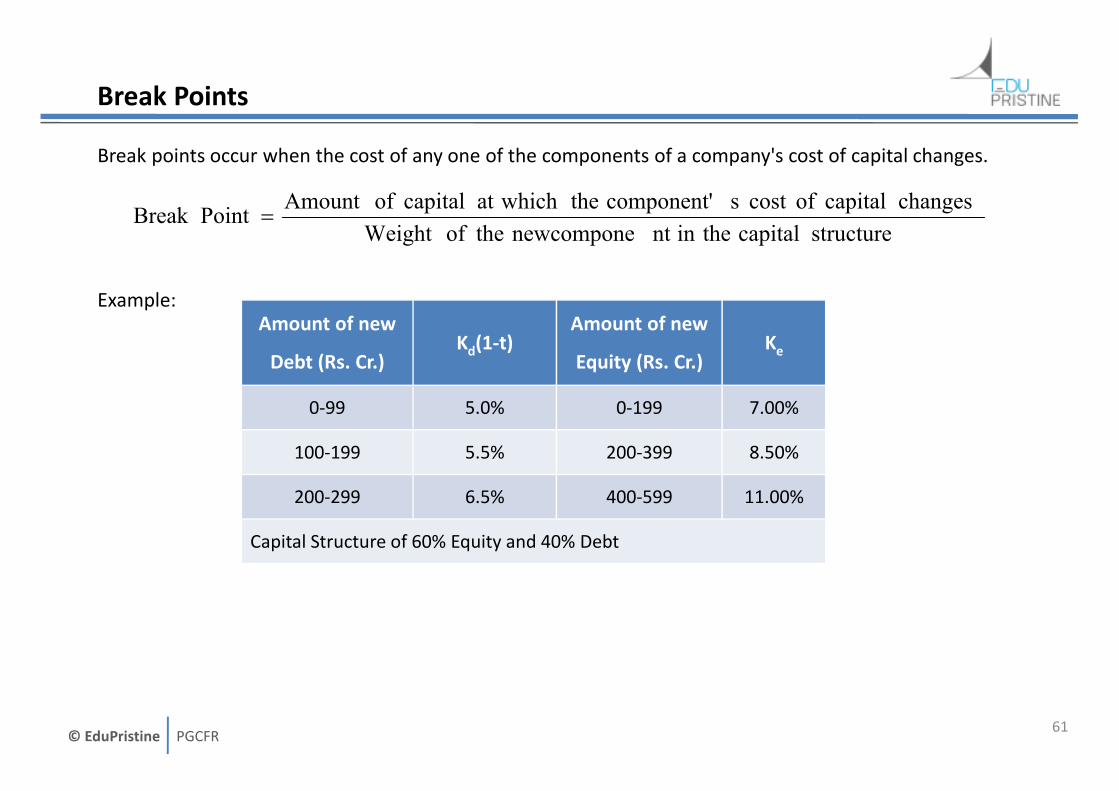

Break Points

Break points occur when the cost of any one of the components of a company's cost of capital changes.

Example:

61

Amount of new

Debt (Rs. Cr.)Kd(1-t)

Amount of new

Equity (Rs. Cr.)Ke

0-99 5.0% 0-199 7.00%

100-199 5.5% 200-399 8.50%

200-299 6.5% 400-599 11.00%

Capital Structure of 60% Equity and 40% Debt

structurecapitaltheinntnewcomponetheofWeight

changescapitalofcostscomponent'thewhichatcapitalofAmountPointBreak =

© EduPristine PGCFR

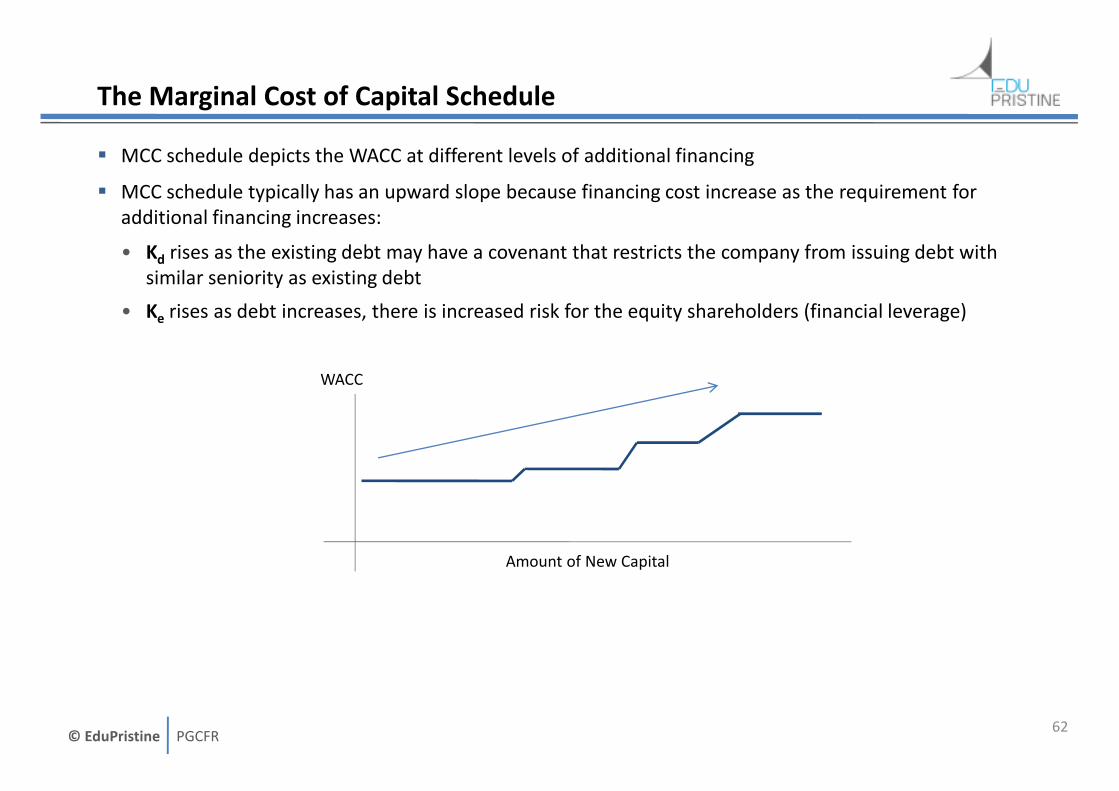

The Marginal Cost of Capital Schedule

� MCC schedule depicts the WACC at different levels of additional financing

� MCC schedule typically has an upward slope because financing cost increase as the requirement for

additional financing increases:

• Kd rises as the existing debt may have a covenant that restricts the company from issuing debt with

similar seniority as existing debt

• Ke rises as debt increases, there is increased risk for the equity shareholders (financial leverage)

62

Amount of New Capital

WACC

© EduPristine PGCFR

Using WACC (or MCC) in Capital Budgeting

� If we chose to use the company’s WACC as discount rate in the calculation of the NPV of a project, we

assume the following:

a) The project has the same risk as the average-risk project of the company

b) The project will have a constant target capital structure throughout its useful life.

� Companies may use an ad-hoc or a systematic approach for adjusting the WACC to evaluate new

projects with risks different than risk of companies existing projects.

63

© EduPristine PGCFR

Other Topics – 1. Beta and Cost of Capital for a Project

� Project: A new venture by an existing company which is in addition to its other businesses

� Beta (total systematic risk) is a combination of:

1. Operating risk AND

2. Financial risk

� Risk (and Beta) of a new project can be very different than overall Risk (and Beta) of the firm

� There is a need to evaluate risks (Beta) specific to the particular project in order to estimate the

discount rate (WACC) to evaluate that particular project

� Since each project is not represented by a publicly traded security, it is difficult to calculate the Project

Beta

� In order to estimate Beta for the Project - Pure Play Method is USED

64

© EduPristine PGCFR

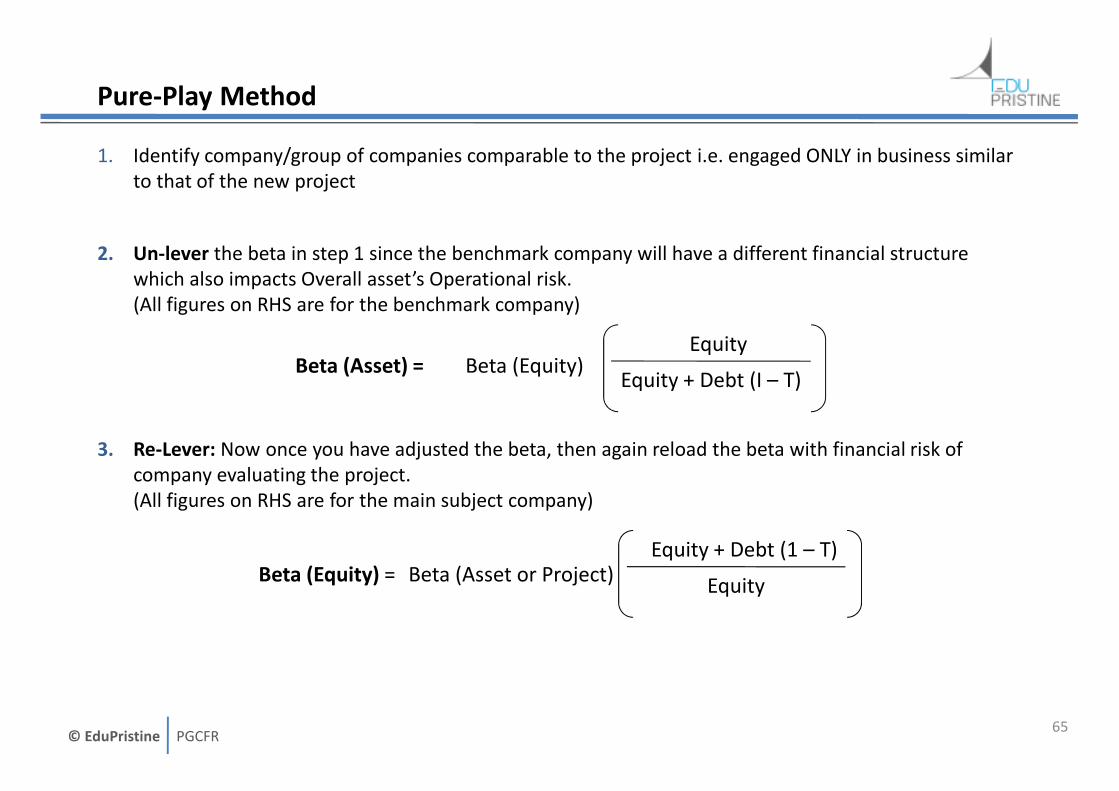

Pure-Play Method

1. Identify company/group of companies comparable to the project i.e. engaged ONLY in business similar

to that of the new project

2. Un-lever the beta in step 1 since the benchmark company will have a different financial structure

which also impacts Overall asset’s Operational risk.

(All figures on RHS are for the benchmark company)

3. Re-Lever: Now once you have adjusted the beta, then again reload the beta with financial risk of

company evaluating the project.

(All figures on RHS are for the main subject company)

65

Beta (Asset) = Beta (Equity)Equity

Equity + Debt (I – T)

Beta (Equity) = Beta (Asset or Project)Equity + Debt (1 – T)

Equity

© EduPristine PGCFR

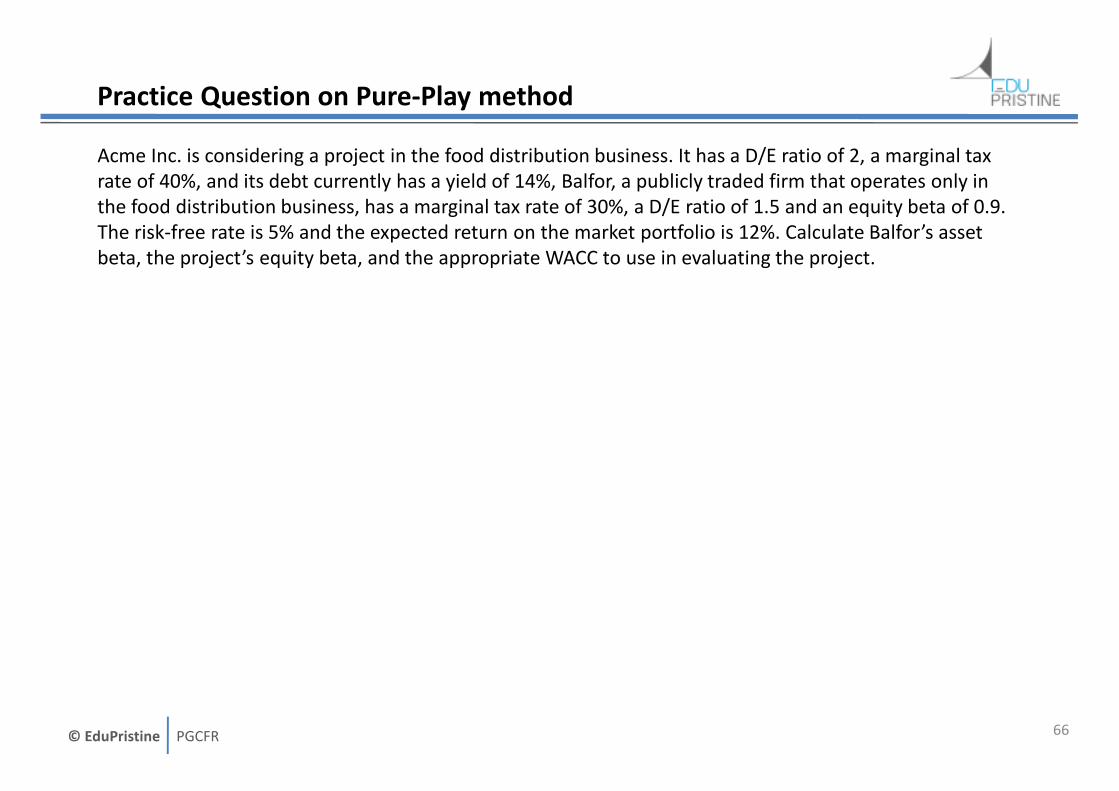

Practice Question on Pure-Play method

Acme Inc. is considering a project in the food distribution business. It has a D/E ratio of 2, a marginal tax

rate of 40%, and its debt currently has a yield of 14%, Balfor, a publicly traded firm that operates only in

the food distribution business, has a marginal tax rate of 30%, a D/E ratio of 1.5 and an equity beta of 0.9.

The risk-free rate is 5% and the expected return on the market portfolio is 12%. Calculate Balfor’s asset

beta, the project’s equity beta, and the appropriate WACC to use in evaluating the project.

66

© EduPristine PGCFR

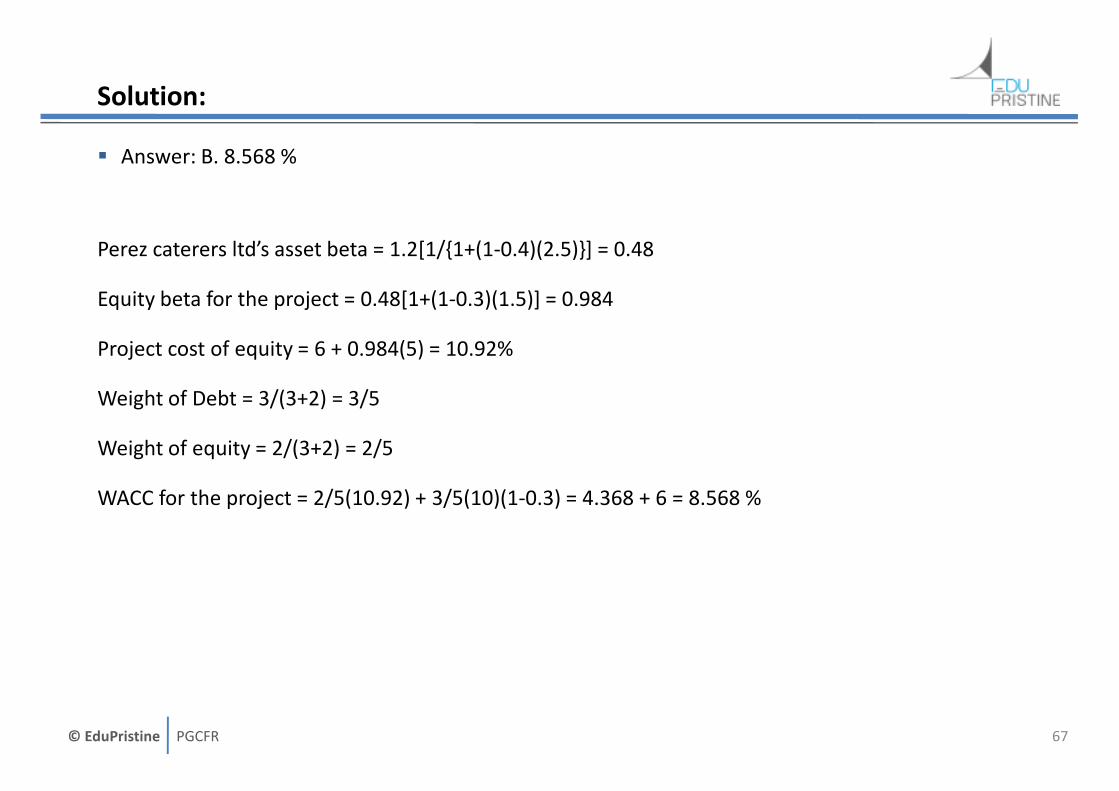

Solution:

� Answer: B. 8.568 %

Perez caterers ltd’s asset beta = 1.2[1/{1+(1-0.4)(2.5)}] = 0.48

Equity beta for the project = 0.48[1+(1-0.3)(1.5)] = 0.984

Project cost of equity = 6 + 0.984(5) = 10.92%

Weight of Debt = 3/(3+2) = 3/5

Weight of equity = 2/(3+2) = 2/5

WACC for the project = 2/5(10.92) + 3/5(10)(1-0.3) = 4.368 + 6 = 8.568 %

67

© EduPristine PGCFR

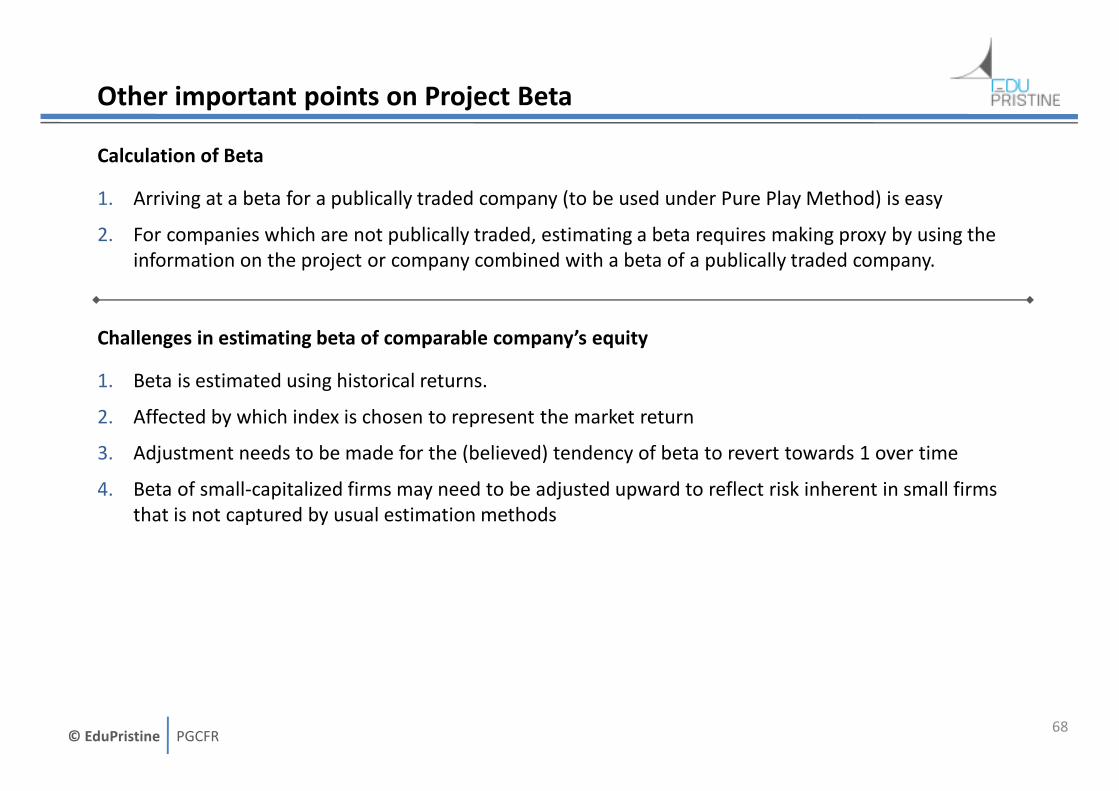

Other important points on Project Beta

Calculation of Beta

1. Arriving at a beta for a publically traded company (to be used under Pure Play Method) is easy

2. For companies which are not publically traded, estimating a beta requires making proxy by using the

information on the project or company combined with a beta of a publically traded company.

Challenges in estimating beta of comparable company’s equity

1. Beta is estimated using historical returns.

2. Affected by which index is chosen to represent the market return

3. Adjustment needs to be made for the (believed) tendency of beta to revert towards 1 over time

4. Beta of small-capitalized firms may need to be adjusted upward to reflect risk inherent in small firms

that is not captured by usual estimation methods

68

© EduPristine PGCFR

Other Topics – 2. Country equity risk premium (CRP)

Context:‘β’ does not adequately capture the country risk of an emerging / developing market

� We need to add a country risk premium (CRP) to the market risk premium

� Risk of investing in a developing country is measured by the sovereign yield spread i.e. the difference in

yields between the developing country’s government bonds (denominated in local currency) and

Treasury bonds of similar maturity

� The above compensates only the bond risk. This is adjusted for the equity market risk by adjusting it for

the relative risk of equity markets to the bond markets

69

Consider Sovereign = Government

What is developing is a relative term

=

currency developedIn marketbond

sovereignofDeviationStandardAnnualized

currency DevelopingIn Country developingofindex

equityofDeviationStandardAnnualized

spreadyieldSovereignCRP

Ke = Rf + ß [E(Rm) – Rf + CRP]

© EduPristine PGCFR

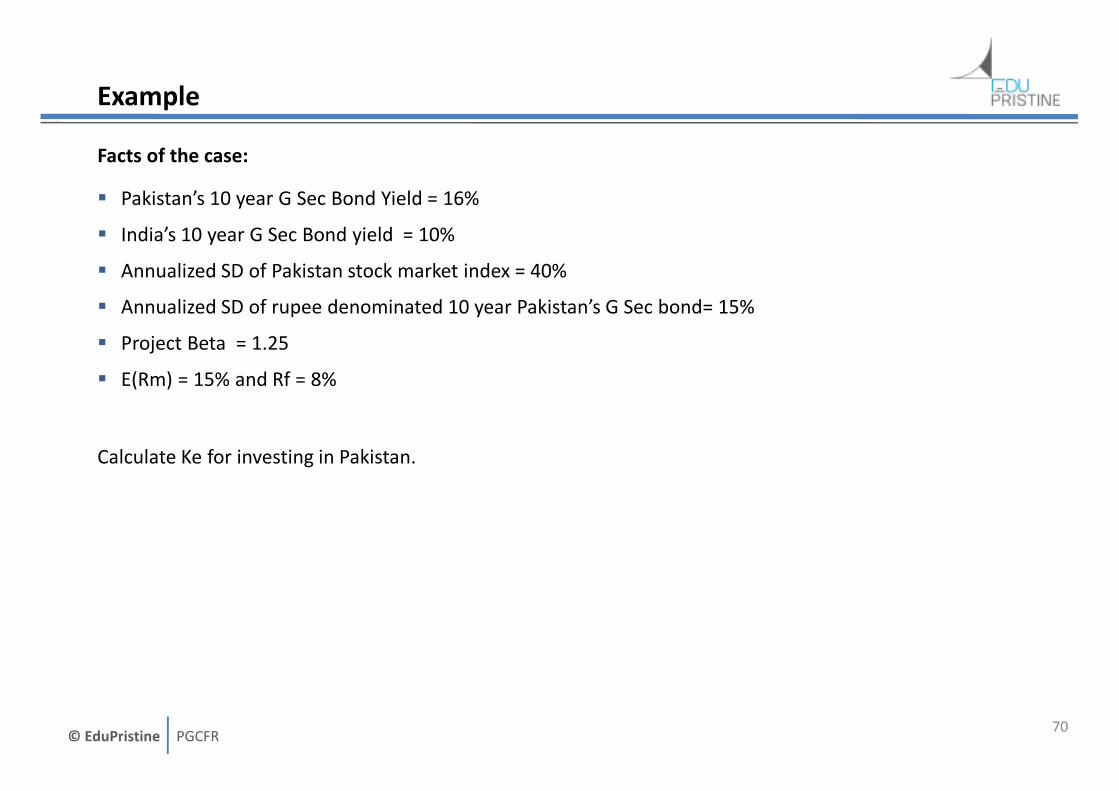

Example

Facts of the case:

� Pakistan’s 10 year G Sec Bond Yield = 16%

� India’s 10 year G Sec Bond yield = 10%

� Annualized SD of Pakistan stock market index = 40%

� Annualized SD of rupee denominated 10 year Pakistan’s G Sec bond= 15%

� Project Beta = 1.25

� E(Rm) = 15% and Rf = 8%

Calculate Ke for investing in Pakistan.

70

© EduPristine PGCFR

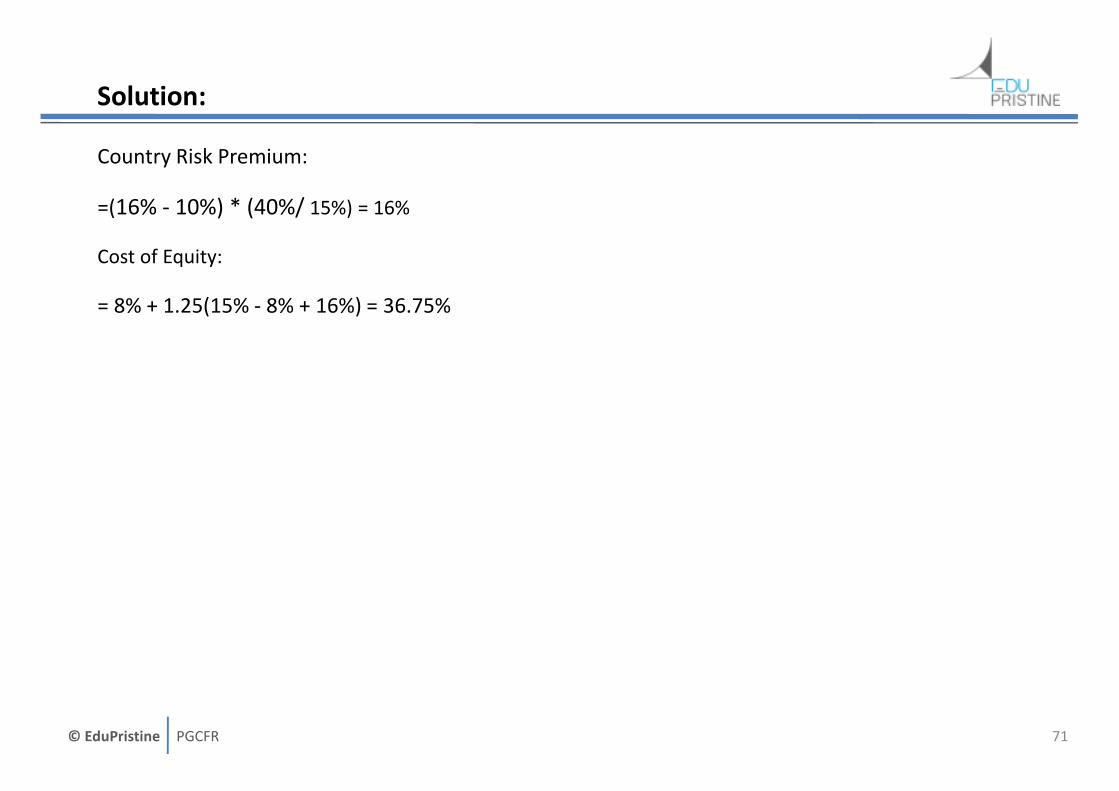

Solution:

Country Risk Premium:

=(16% - 10%) * (40%/ 15%) = 16%

Cost of Equity:

= 8% + 1.25(15% - 8% + 16%) = 36.75%

71

© EduPristine PGCFR

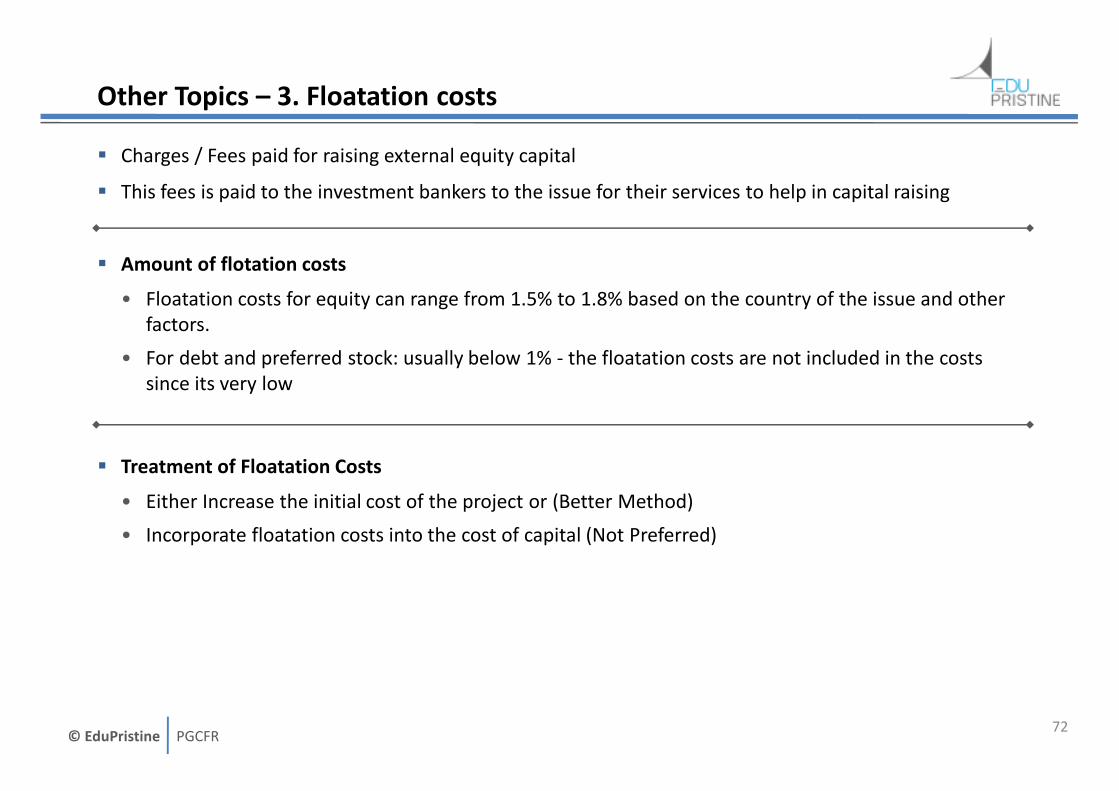

Other Topics – 3. Floatation costs

� Charges / Fees paid for raising external equity capital

� This fees is paid to the investment bankers to the issue for their services to help in capital raising

� Amount of flotation costs

• Floatation costs for equity can range from 1.5% to 1.8% based on the country of the issue and other

factors.

• For debt and preferred stock: usually below 1% - the floatation costs are not included in the costs

since its very low

� Treatment of Floatation Costs

• Either Increase the initial cost of the project or (Better Method)

• Incorporate floatation costs into the cost of capital (Not Preferred)

72

© EduPristine PGCFR

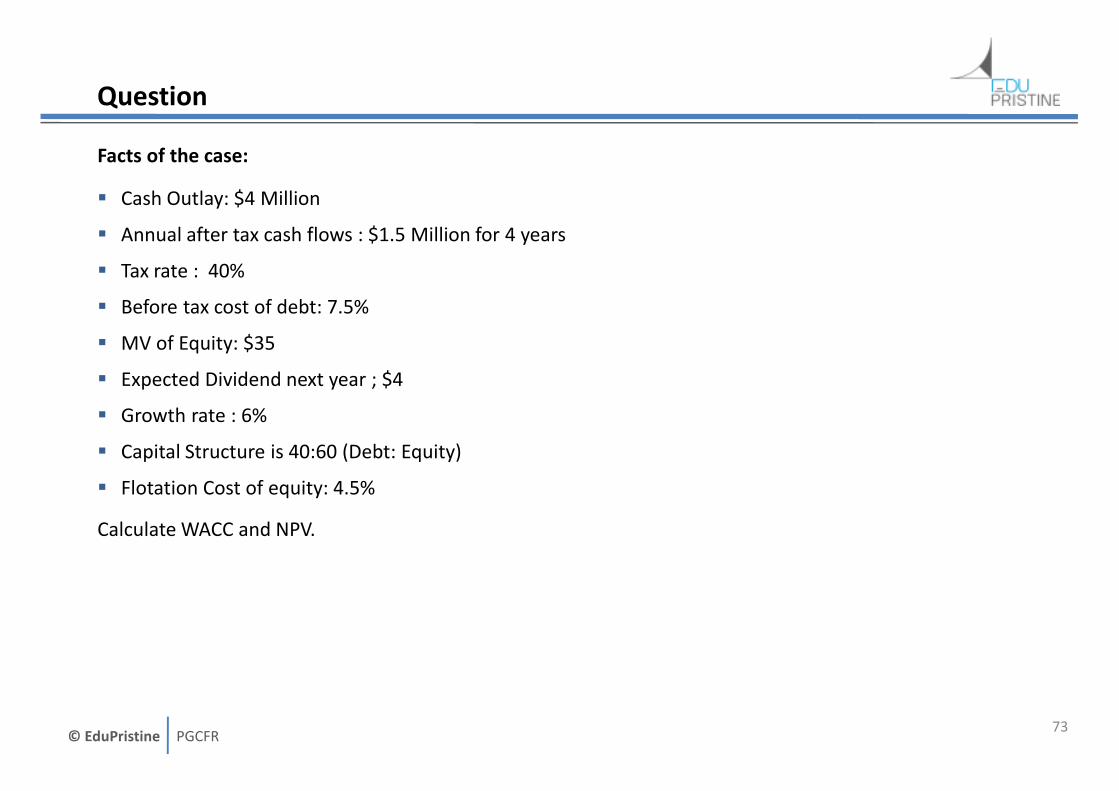

Question

Facts of the case:

� Cash Outlay: $4 Million

� Annual after tax cash flows : $1.5 Million for 4 years

� Tax rate : 40%

� Before tax cost of debt: 7.5%

� MV of Equity: $35

� Expected Dividend next year ; $4

� Growth rate : 6%

� Capital Structure is 40:60 (Debt: Equity)

� Flotation Cost of equity: 4.5%

Calculate WACC and NPV.

73

© EduPristine PGCFR

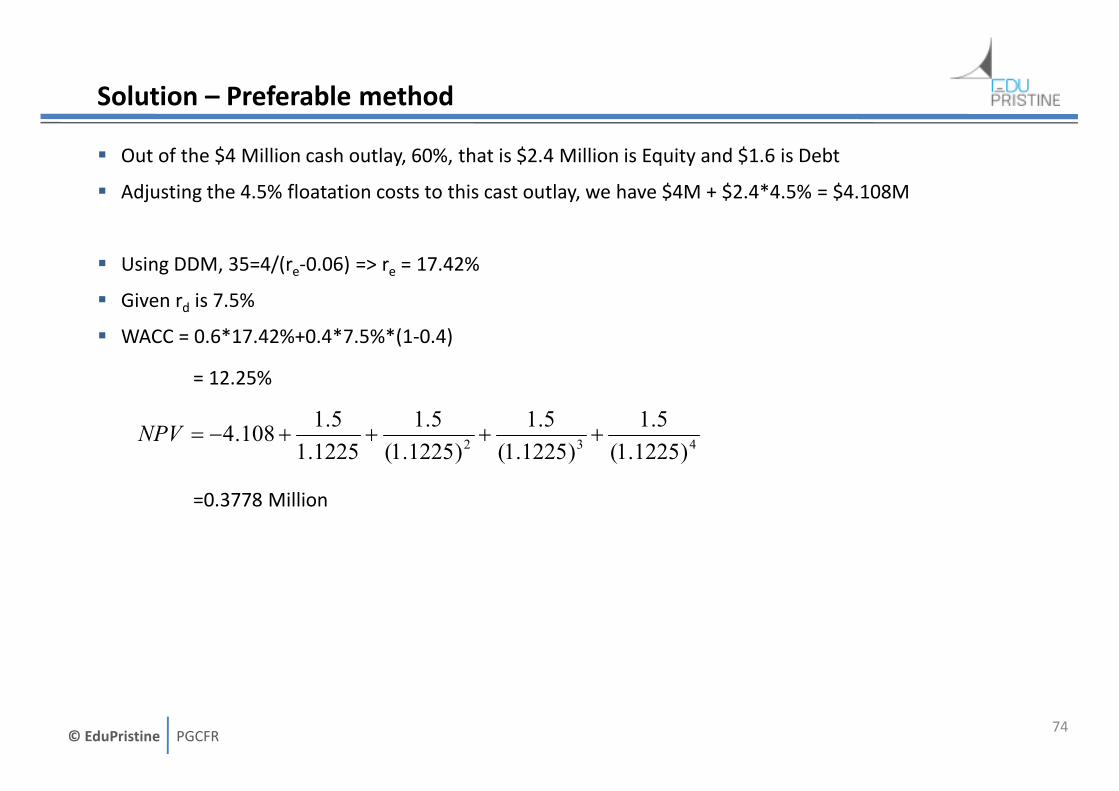

Solution – Preferable method

� Out of the $4 Million cash outlay, 60%, that is $2.4 Million is Equity and $1.6 is Debt

� Adjusting the 4.5% floatation costs to this cast outlay, we have $4M + $2.4*4.5% = $4.108M

� Using DDM, 35=4/(re-0.06) => re = 17.42%

� Given rd is 7.5%

� WACC = 0.6*17.42%+0.4*7.5%*(1-0.4)

= 12.25%

=0.3778 Million

74

432 )1225.1(

5.1

)1225.1(

5.1

)1225.1(

5.1

1225.1

5.1108.4 ++++−=NPV

© EduPristine PGCFR

Questions

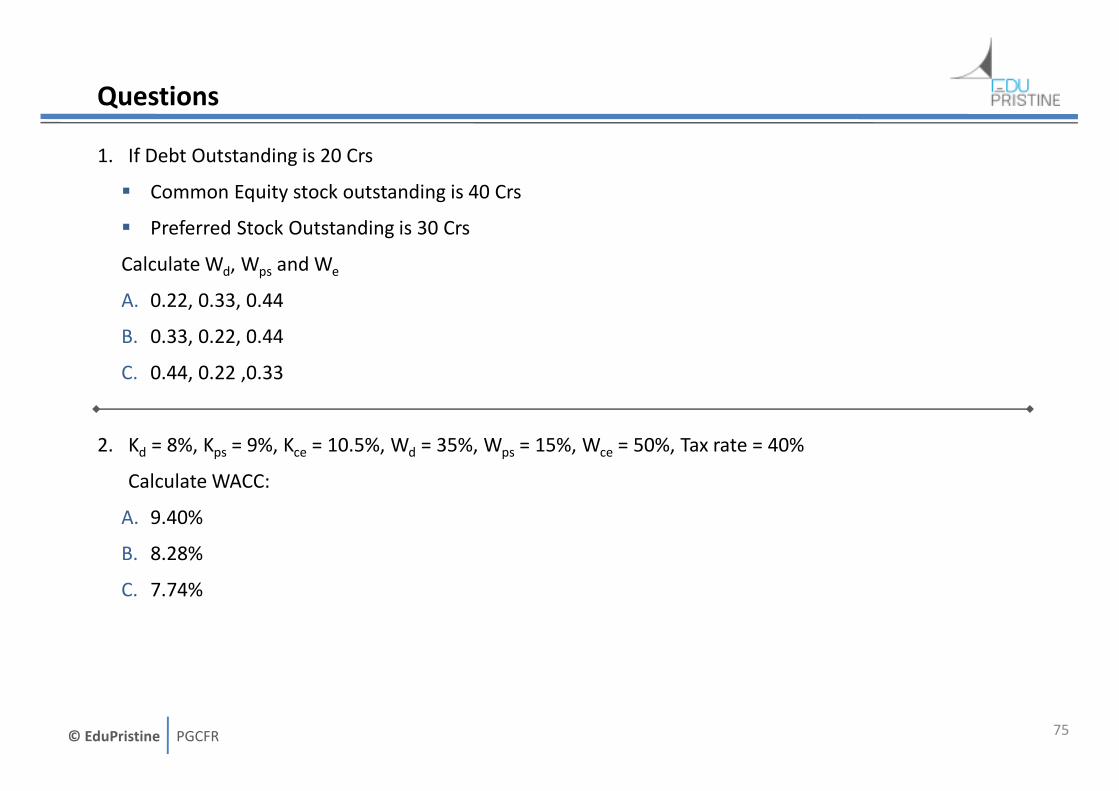

1. If Debt Outstanding is 20 Crs

� Common Equity stock outstanding is 40 Crs

� Preferred Stock Outstanding is 30 Crs

Calculate Wd, Wps and We

A. 0.22, 0.33, 0.44

B. 0.33, 0.22, 0.44

C. 0.44, 0.22 ,0.33

2. Kd = 8%, Kps = 9%, Kce = 10.5%, Wd = 35%, Wps = 15%, Wce = 50%, Tax rate = 40%

Calculate WACC:

A. 9.40%

B. 8.28%

C. 7.74%

75

© EduPristine PGCFR

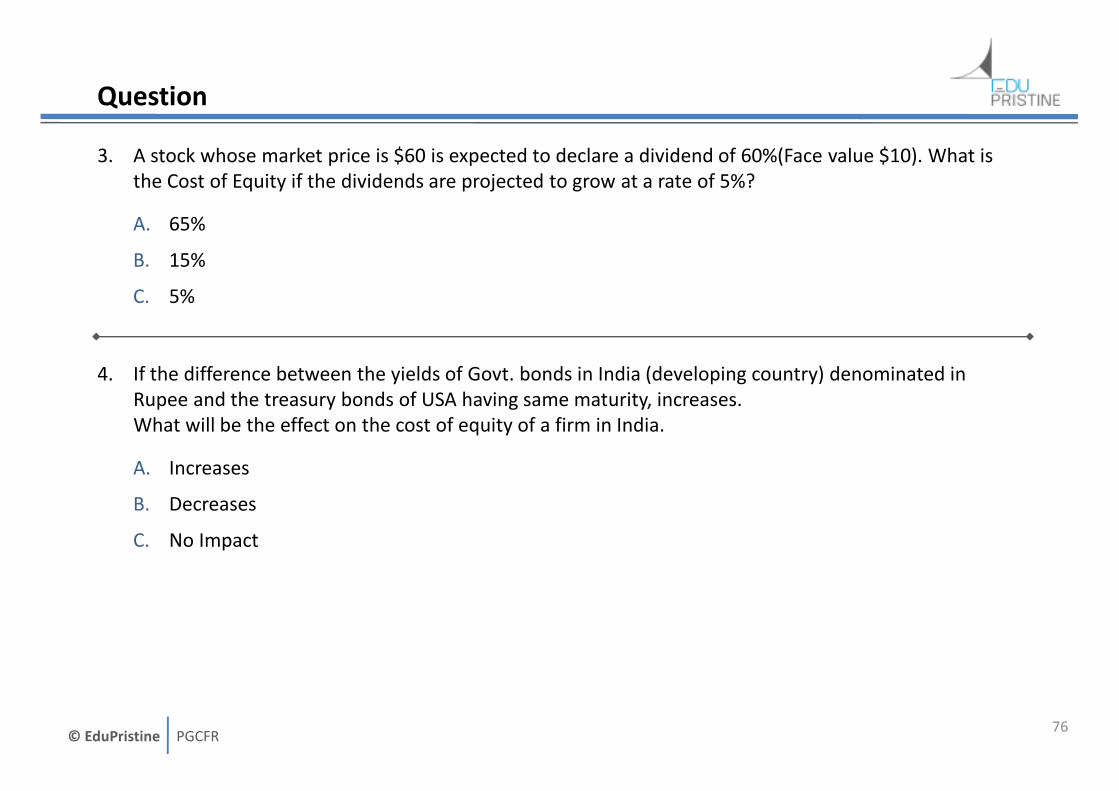

Question

3. A stock whose market price is $60 is expected to declare a dividend of 60%(Face value $10). What is

the Cost of Equity if the dividends are projected to grow at a rate of 5%?

A. 65%

B. 15%

C. 5%

4. If the difference between the yields of Govt. bonds in India (developing country) denominated in

Rupee and the treasury bonds of USA having same maturity, increases.

What will be the effect on the cost of equity of a firm in India.

A. Increases

B. Decreases

C. No Impact

76

© EduPristine PGCFR

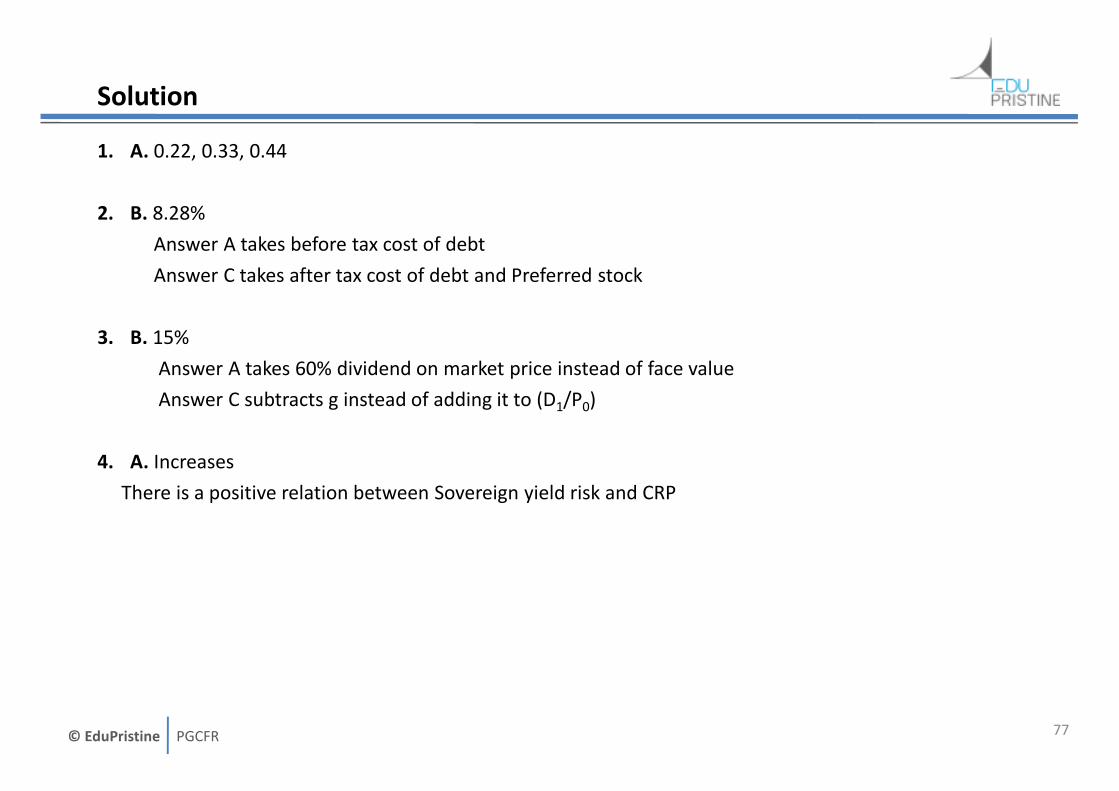

Solution

1. A. 0.22, 0.33, 0.44

2. B. 8.28%

Answer A takes before tax cost of debt

Answer C takes after tax cost of debt and Preferred stock

3. B. 15%

Answer A takes 60% dividend on market price instead of face value

Answer C subtracts g instead of adding it to (D1/P0)

4. A. Increases

There is a positive relation between Sovereign yield risk and CRP

77

© EduPristine PGCFR

Measures of Leverage

78

© EduPristine PGCFR

Coverage of the topic – Measures of Leverage

1. Key terms used in Leverage Analysis

2. Meaning and Need for Leverage

3. Types of Leverage

A. Operating Leverage

B. Financial Leverage

C. Combined Leverage

4. Break even Analysis

A. Break even points

B. Operating Break even points

79

© EduPristine PGCFR

Key terms used in Leverage Analysis

Cost Structure of a company is the mix of two types of cost: (in terms of variability)

� Variable Costs fluctuate in DIRECT PROPORTION with the level of production and sales.

• Example: Raw materials cost, delivery charges

� Fixed Costs are expenses which DO NOT FLUCTUATE at all regardless of level of production

• Example: Rent, wages for salaried employees, interest on debt

Fixed costs may further be divided into:

� Operating Fixed Cost: Related to operational aspects / business model of the company.

• These are the cost related to the main / incidental activity of the business

� Financial Fixed Cost: Related to capital structure of the company

• Among Debt, Equity and Preference share, only DEBT has a fixed cost – Interest that needs to be paid

irrespective of the profits.

80

© EduPristine PGCFR

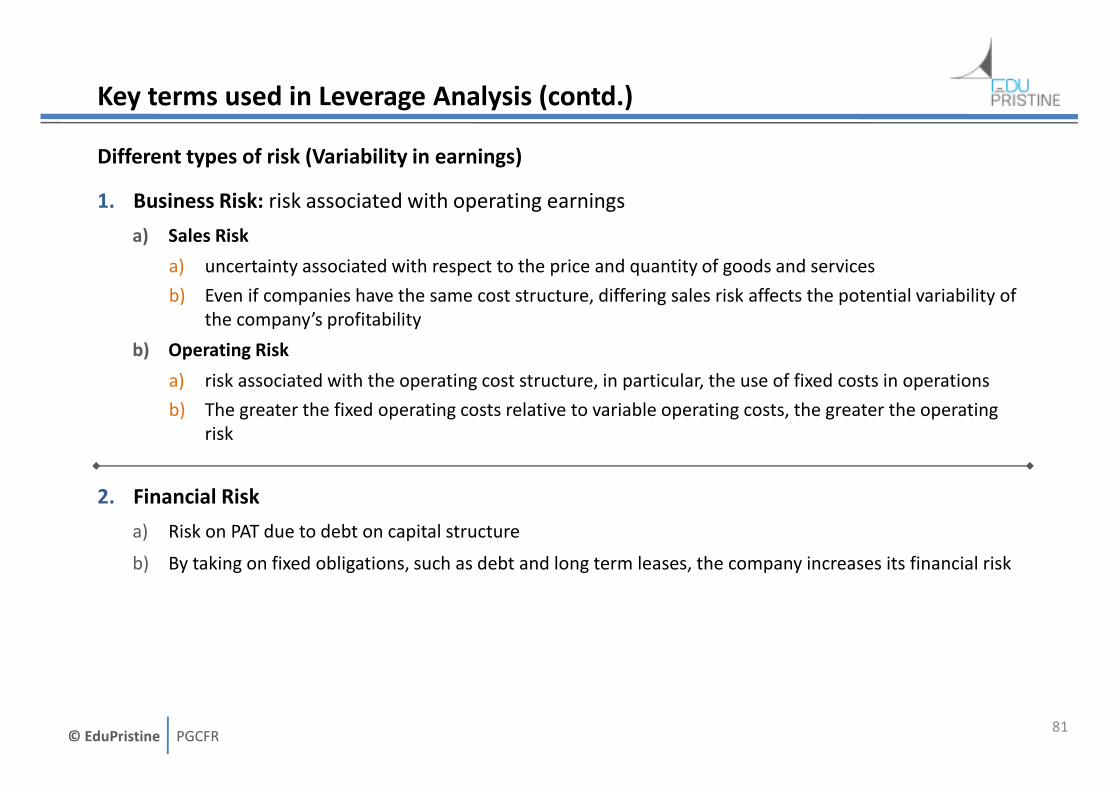

Key terms used in Leverage Analysis (contd.)

Different types of risk (Variability in earnings)

1. Business Risk: risk associated with operating earnings

a) Sales Risk

a) uncertainty associated with respect to the price and quantity of goods and services

b) Even if companies have the same cost structure, differing sales risk affects the potential variability of

the company’s profitability

b) Operating Risk

a) risk associated with the operating cost structure, in particular, the use of fixed costs in operations

b) The greater the fixed operating costs relative to variable operating costs, the greater the operating

risk

2. Financial Risk

a) Risk on PAT due to debt on capital structure

b) By taking on fixed obligations, such as debt and long term leases, the company increases its financial risk

81

© EduPristine PGCFR

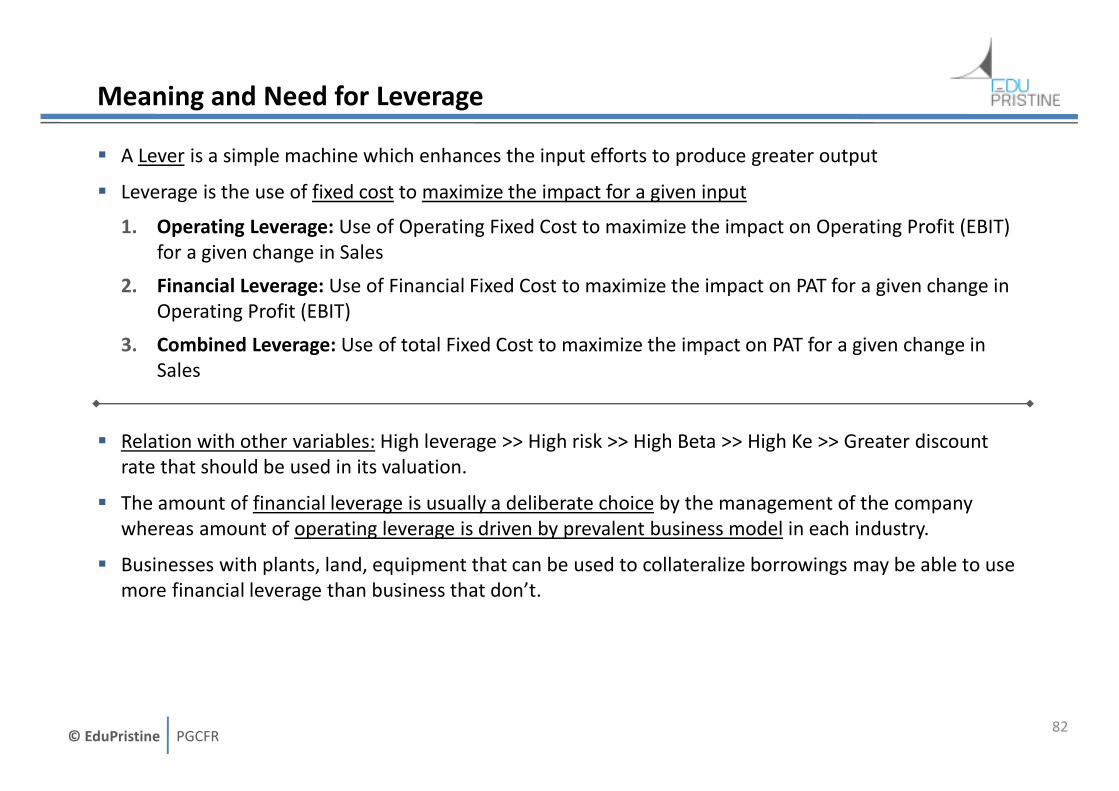

Meaning and Need for Leverage

� A Lever is a simple machine which enhances the input efforts to produce greater output

� Leverage is the use of fixed cost to maximize the impact for a given input

1. Operating Leverage: Use of Operating Fixed Cost to maximize the impact on Operating Profit (EBIT)

for a given change in Sales

2. Financial Leverage: Use of Financial Fixed Cost to maximize the impact on PAT for a given change in

Operating Profit (EBIT)

3. Combined Leverage: Use of total Fixed Cost to maximize the impact on PAT for a given change in

Sales

� Relation with other variables: High leverage >> High risk >> High Beta >> High Ke >> Greater discount

rate that should be used in its valuation.

� The amount of financial leverage is usually a deliberate choice by the management of the company

whereas amount of operating leverage is driven by prevalent business model in each industry.

� Businesses with plants, land, equipment that can be used to collateralize borrowings may be able to use

more financial leverage than business that don’t.

82

© EduPristine PGCFR

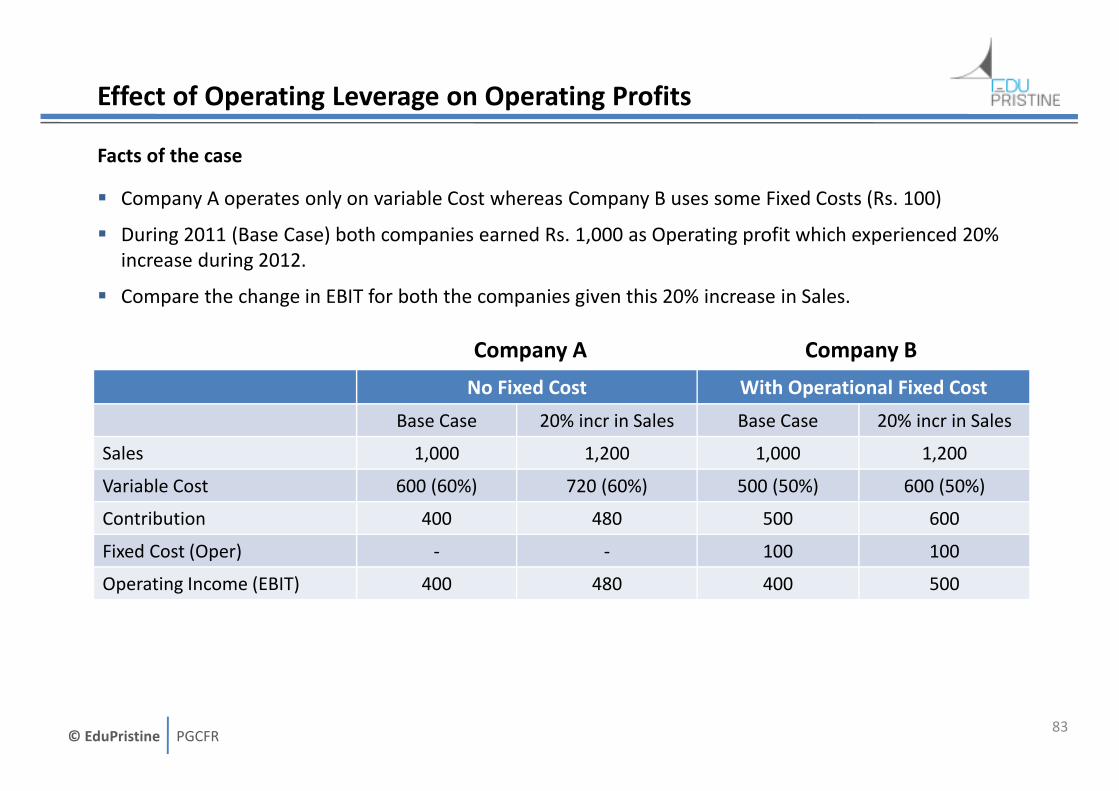

Effect of Operating Leverage on Operating Profits

Facts of the case

� Company A operates only on variable Cost whereas Company B uses some Fixed Costs (Rs. 100)

� During 2011 (Base Case) both companies earned Rs. 1,000 as Operating profit which experienced 20%

increase during 2012.

� Compare the change in EBIT for both the companies given this 20% increase in Sales.

83

No Fixed Cost With Operational Fixed Cost

Base Case 20% incr in Sales Base Case 20% incr in Sales

Sales 1,000 1,200 1,000 1,200

Variable Cost 600 (60%) 720 (60%) 500 (50%) 600 (50%)

Contribution 400 480 500 600

Fixed Cost (Oper) - - 100 100

Operating Income (EBIT) 400 480 400 500

Company A Company B

© EduPristine PGCFR

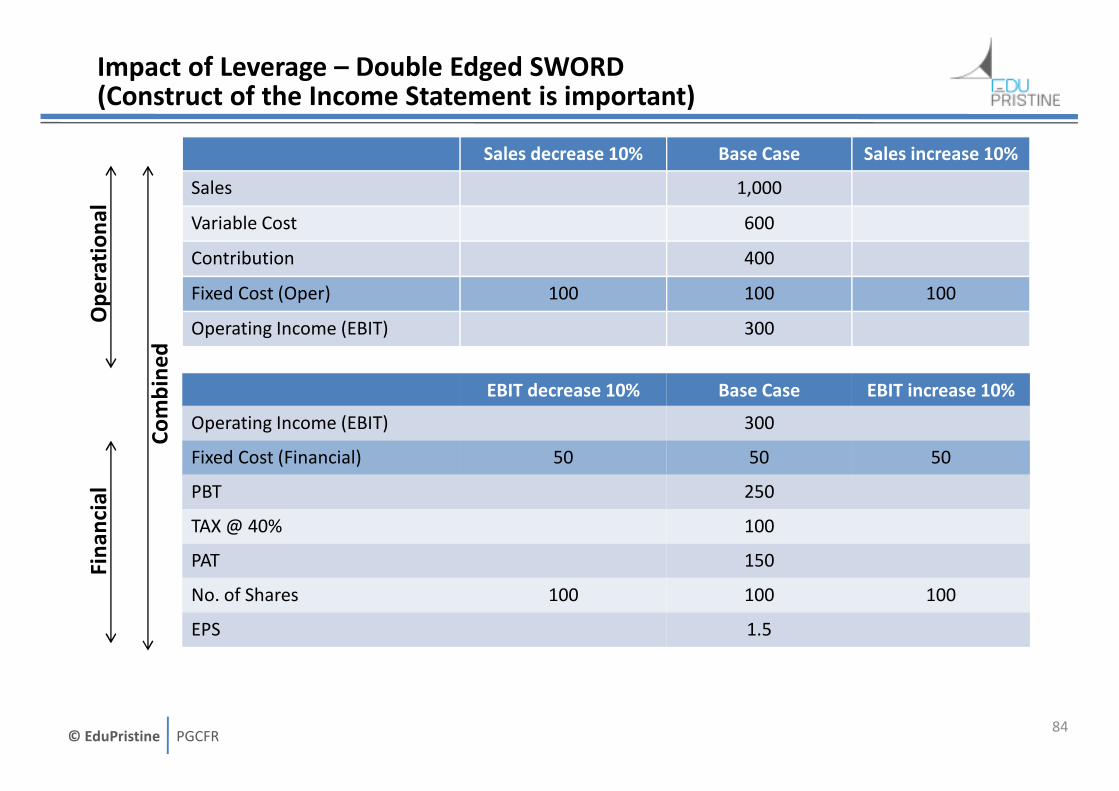

Impact of Leverage – Double Edged SWORD(Construct of the Income Statement is important)

84

Sales decrease 10% Base Case Sales increase 10%

Sales 1,000

Variable Cost 600

Contribution 400

Fixed Cost (Oper) 100 100 100

Operating Income (EBIT) 300

EBIT decrease 10% Base Case EBIT increase 10%

Operating Income (EBIT) 300

Fixed Cost (Financial) 50 50 50

PBT 250

TAX @ 40% 100

PAT 150

No. of Shares 100 100 100

EPS 1.5

Op

era

tio

na

lFi

na

nci

al

Co

mb

ine

d

© EduPristine PGCFR

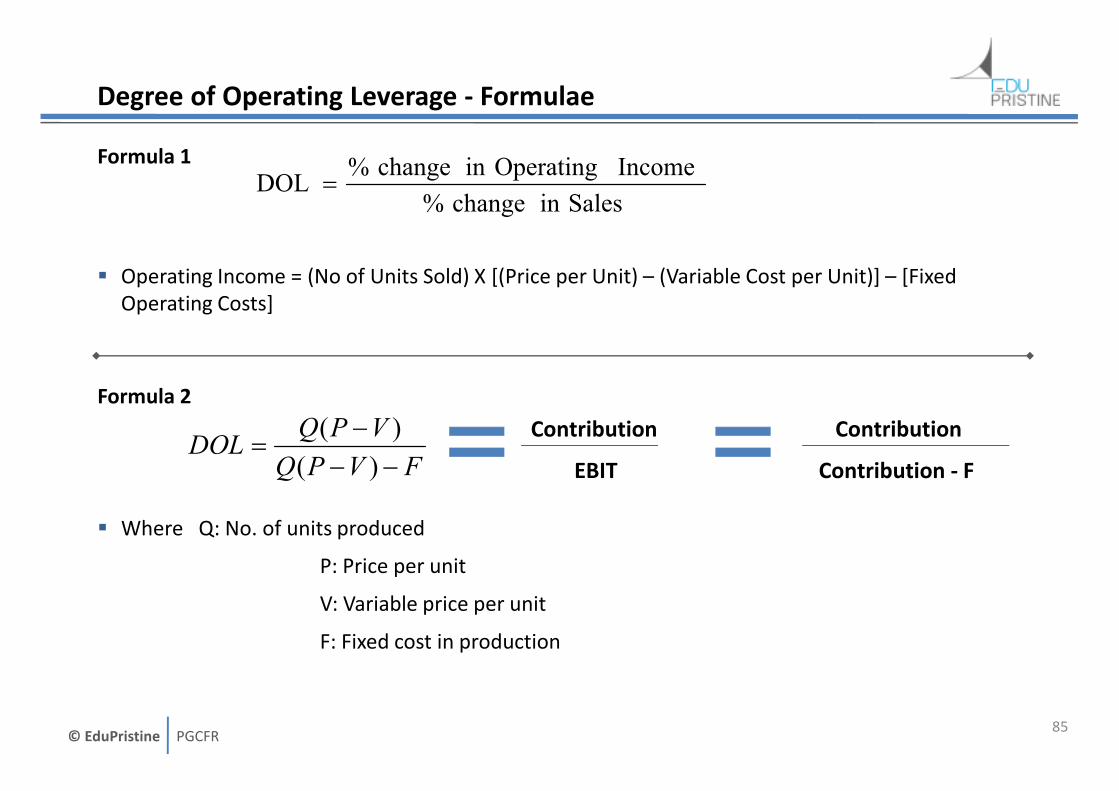

Degree of Operating Leverage - Formulae

Formula 1

� Operating Income = (No of Units Sold) X [(Price per Unit) – (Variable Cost per Unit)] – [Fixed

Operating Costs]

Formula 2

� Where Q: No. of units produced

P: Price per unit

V: Variable price per unit

F: Fixed cost in production

85

FVPQ

VPQDOL

−−−

=)(

)(

Salesin change %

Income Operatingin change %DOL =

Contribution

EBIT

Contribution

Contribution - F

© EduPristine PGCFR

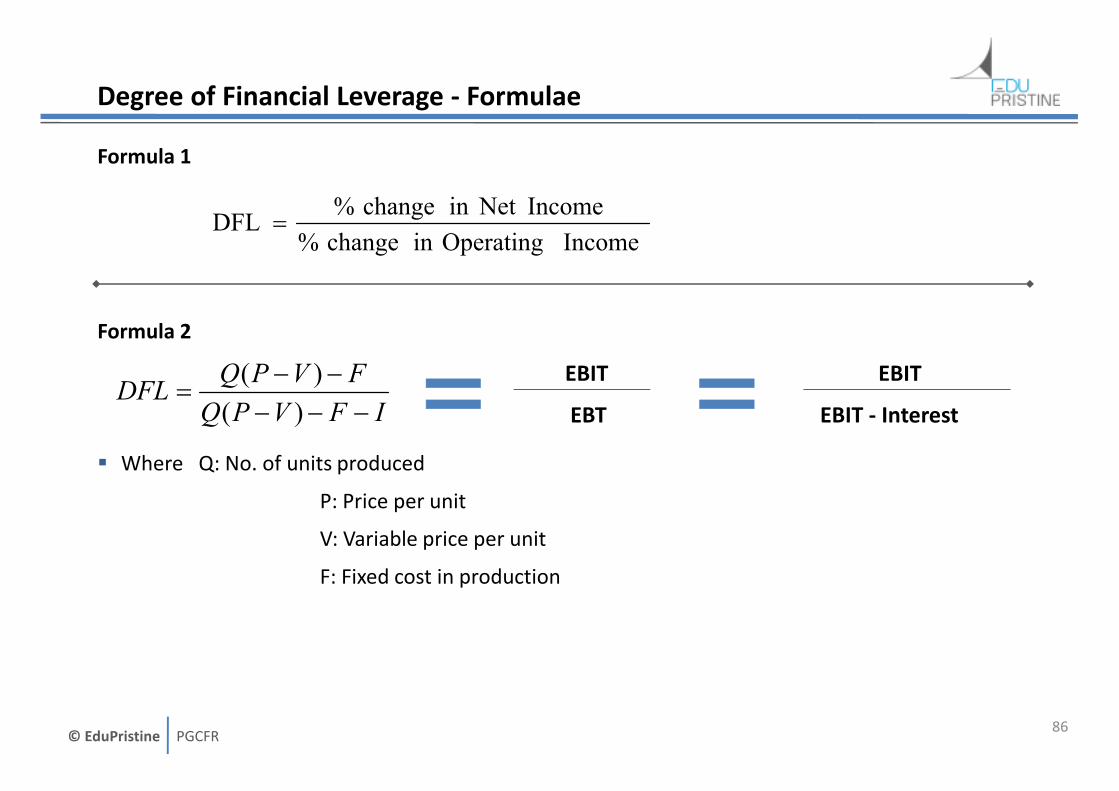

Degree of Financial Leverage - Formulae

Formula 1

Formula 2

� Where Q: No. of units produced

P: Price per unit

V: Variable price per unit

F: Fixed cost in production

86

EBIT

EBT

EBIT

EBIT - Interest

Income Operatingin change %

IncomeNet in change %DFL =

IFVPQ

FVPQDFL

−−−−−

=)(

)(

© EduPristine PGCFR

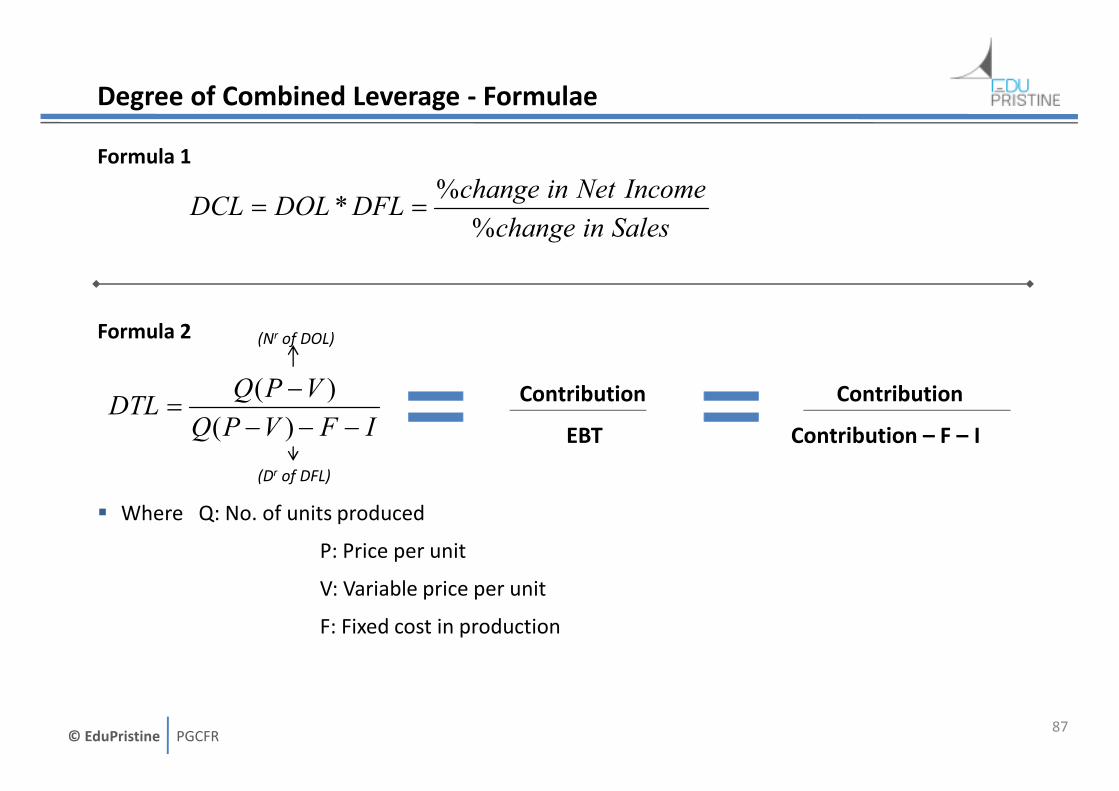

Degree of Combined Leverage - Formulae

Formula 1

Formula 2

� Where Q: No. of units produced

P: Price per unit

V: Variable price per unit

F: Fixed cost in production

87

Contribution

EBT

Salesinchange

IncomeNetinchangeDFLDOLDCL

%

%* ==

IFVPQ

VPQDTL

−−−−

=)(

)(

(Nr of DOL)

(Dr of DFL)

Contribution

Contribution – F – I

© EduPristine PGCFR

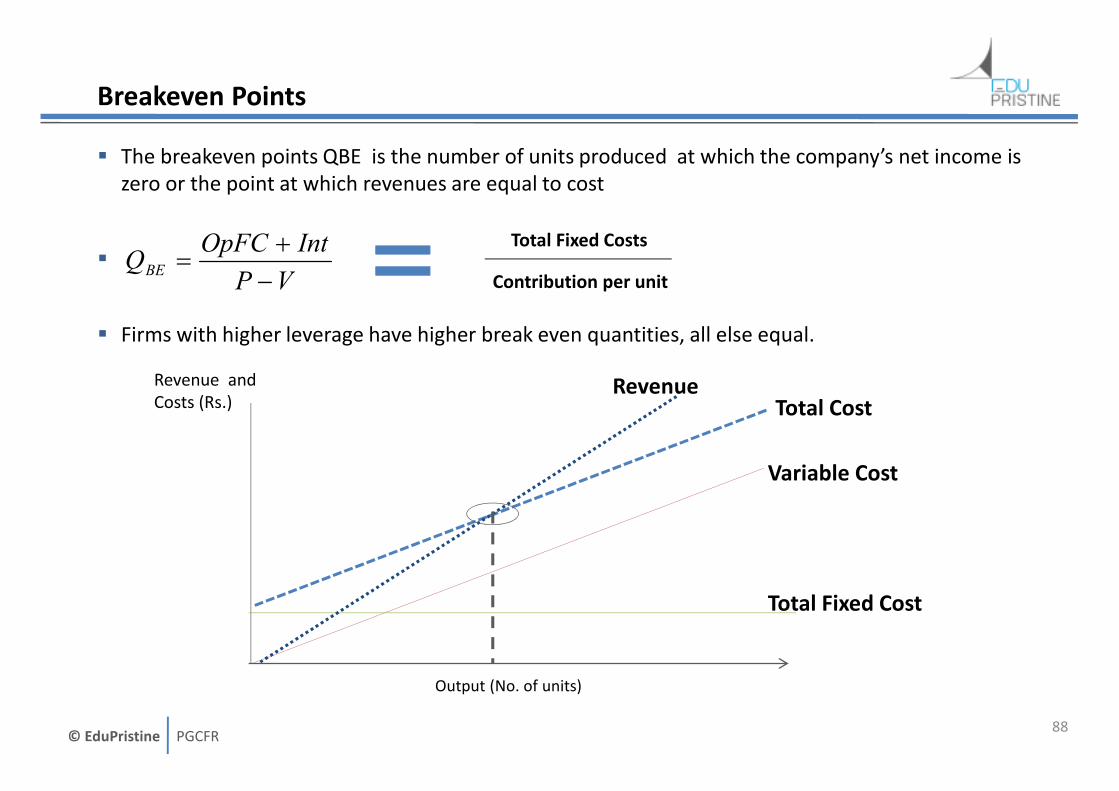

Breakeven Points

� The breakeven points QBE is the number of units produced at which the company’s net income is

zero or the point at which revenues are equal to cost

�

� Firms with higher leverage have higher break even quantities, all else equal.

88

VP

IntOpFCQBE −

+=

Total Fixed Costs

Contribution per unit

Total Fixed Cost

Variable Cost

Total CostRevenue

Output (No. of units)

Revenue and

Costs (Rs.)

© EduPristine PGCFR

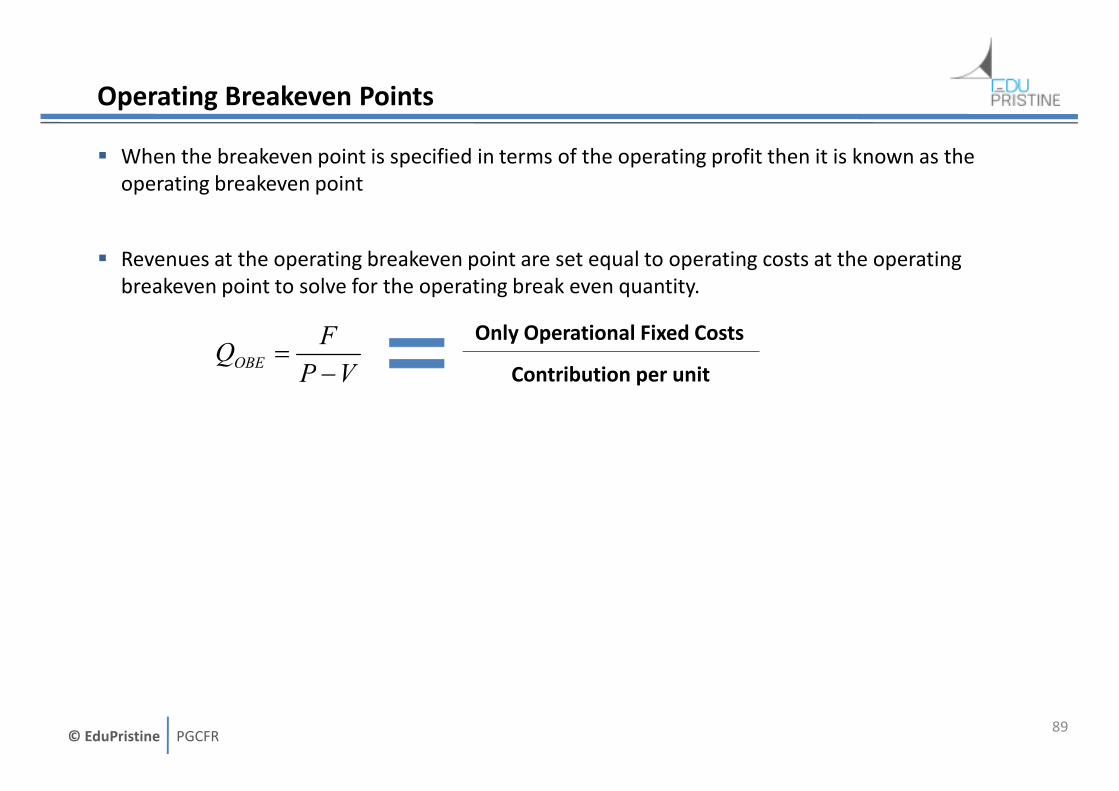

Operating Breakeven Points

� When the breakeven point is specified in terms of the operating profit then it is known as the

operating breakeven point

� Revenues at the operating breakeven point are set equal to operating costs at the operating

breakeven point to solve for the operating break even quantity.

89

VP

FQOBE −

=Only Operational Fixed Costs

Contribution per unit

© EduPristine PGCFR

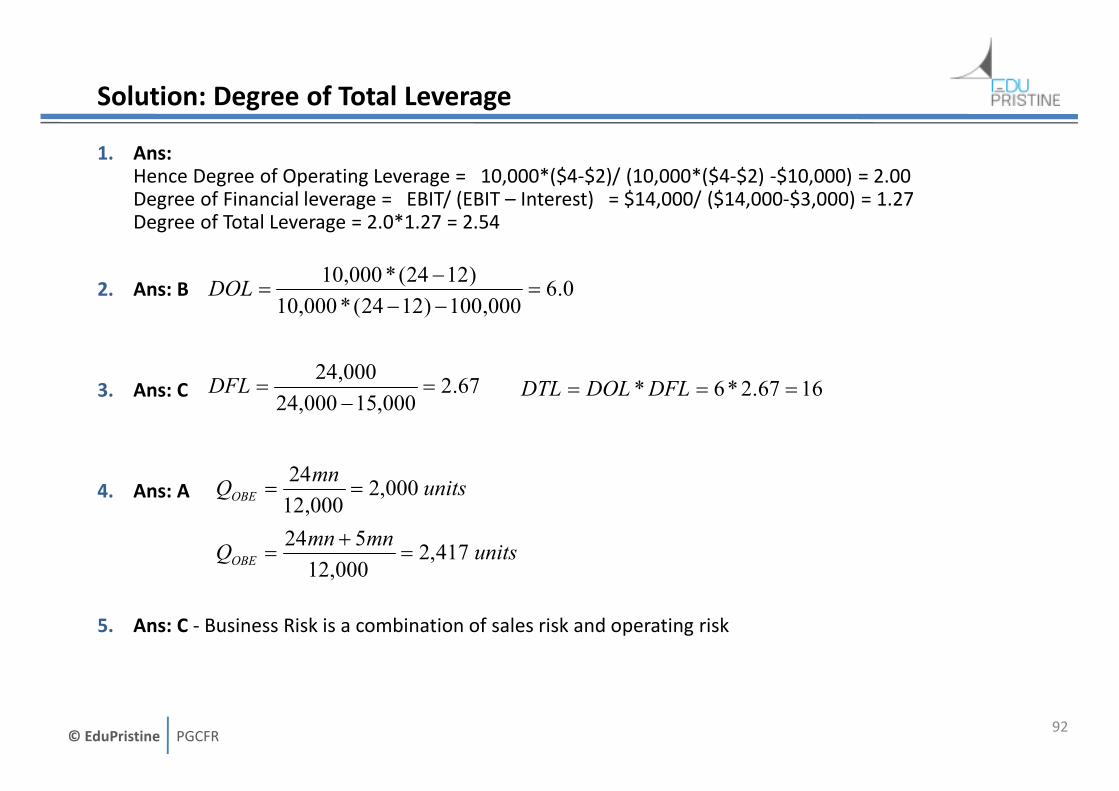

Question: Degree of Total Leverage

1. A company XYZ Ltd sells 10,000 units of water bottles at a price of $4 per unit. ABC’s fixed costs are

$10,000 and it pays an annual interest of $ 3,000.The variable cost of production is $ 2 per unit and the

operating profit (EBIT) is $ 14,000. Which of the following statements is true?

A. Degree of Total Leverage = 2.54

B. Degree of Total Leverage = 1.91

C. Degree of Total Leverage = 3.00

2. Ques 2: Given that a company XYZ manufactures 10,000 widgets each can be sold in the market for

$24. The variable cost per widget is $12. While the fixed costs are $100,000. What is the operating

leverage:

A. 7.2 B. 6.0 C.8.5

3. Ques 3: Assuming that the operating income for XYZ on sale of 10,000 widgets is $24,000 and interest

cost is $15,000. Calculate the degree of financial leverage and the degree of total leverage

90

DFL DTL

A 3.45 10

B 1.45 14

C 2.67 16

© EduPristine PGCFR

Questions(cont..)

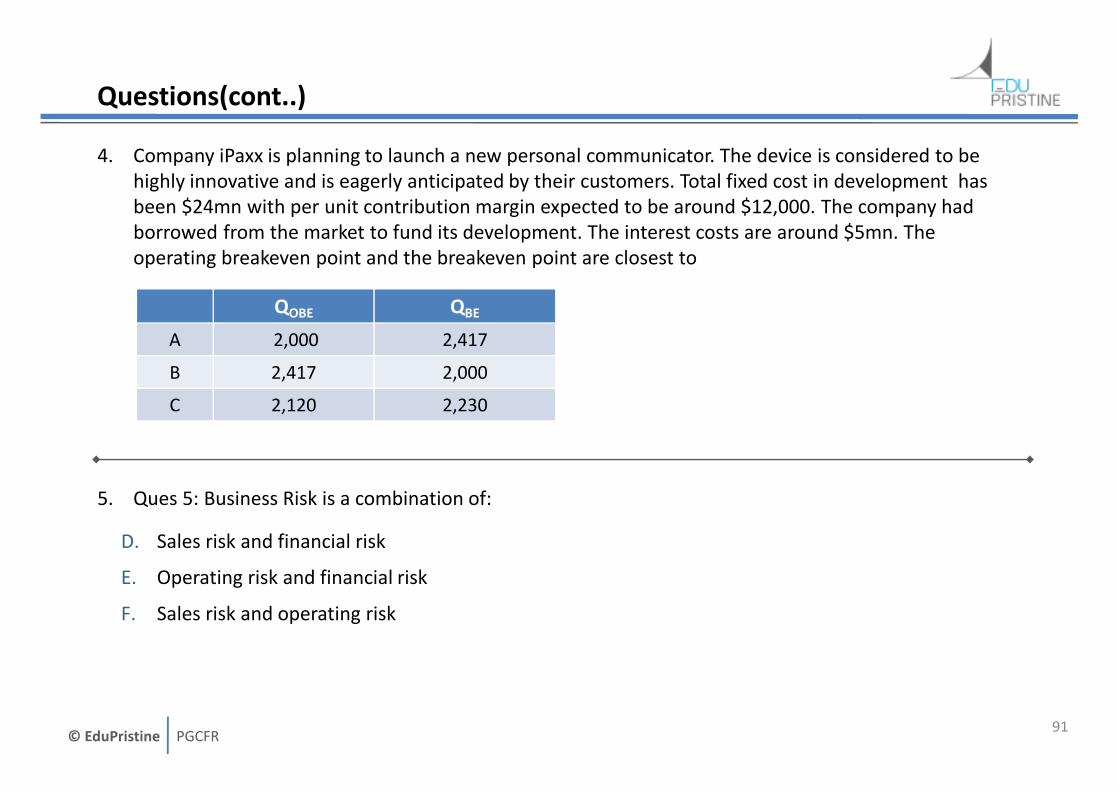

4. Company iPaxx is planning to launch a new personal communicator. The device is considered to be

highly innovative and is eagerly anticipated by their customers. Total fixed cost in development has

been $24mn with per unit contribution margin expected to be around $12,000. The company had

borrowed from the market to fund its development. The interest costs are around $5mn. The

operating breakeven point and the breakeven point are closest to

5. Ques 5: Business Risk is a combination of:

D. Sales risk and financial risk

E. Operating risk and financial risk

F. Sales risk and operating risk

91

QOBE QBE

A 2,000 2,417

B 2,417 2,000

C 2,120 2,230

© EduPristine PGCFR

Solution: Degree of Total Leverage

1. Ans:Hence Degree of Operating Leverage = 10,000*($4-$2)/ (10,000*($4-$2) -$10,000) = 2.00Degree of Financial leverage = EBIT/ (EBIT – Interest) = $14,000/ ($14,000-$3,000) = 1.27Degree of Total Leverage = 2.0*1.27 = 2.54

2. Ans: B

3. Ans: C

4. Ans: A

5. Ans: C - Business Risk is a combination of sales risk and operating risk

92

0.6000,100)1224(*000,10

)1224(*000,10=

−−−

=DOL

67.2000,15000,24

000,24=

−=DFL 1667.2*6* === DFLDOLDTL

unitsmn

QOBE 000,2000,12

24==

unitsmnmn

QOBE 417,2000,12

524=

+=

© EduPristine PGCFR

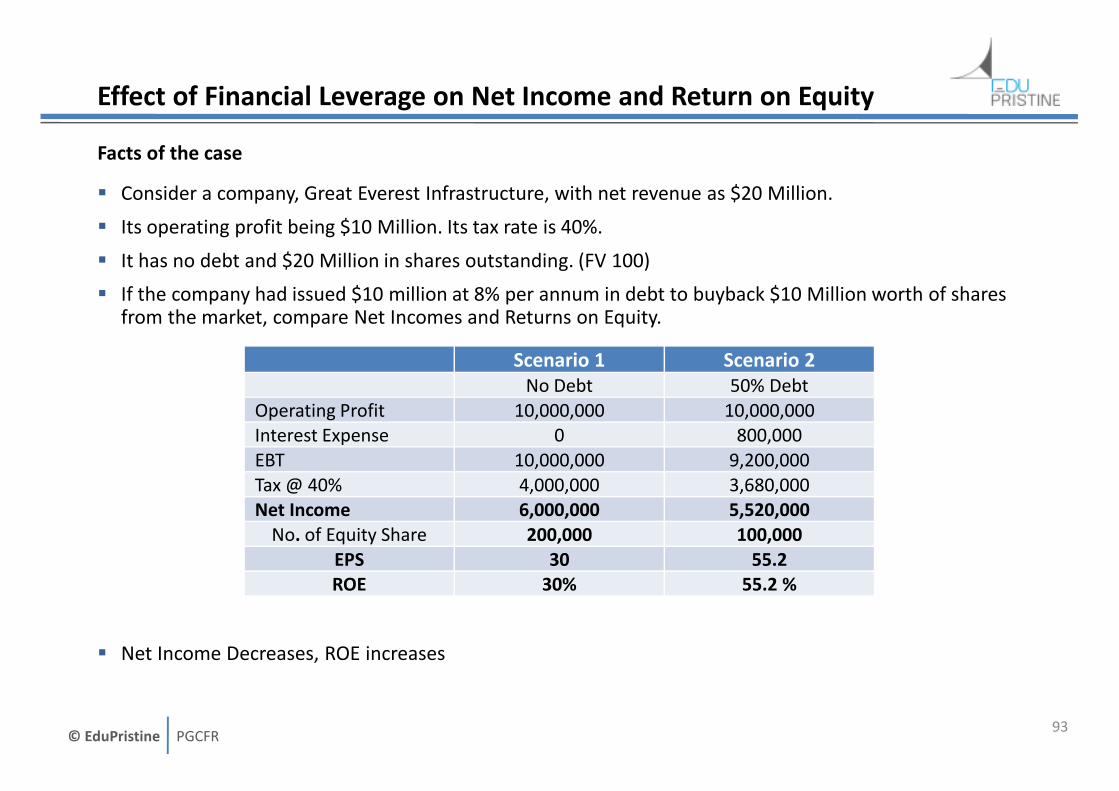

Effect of Financial Leverage on Net Income and Return on Equity

Facts of the case

� Consider a company, Great Everest Infrastructure, with net revenue as $20 Million.

� Its operating profit being $10 Million. Its tax rate is 40%.

� It has no debt and $20 Million in shares outstanding. (FV 100)

� If the company had issued $10 million at 8% per annum in debt to buyback $10 Million worth of shares from the market, compare Net Incomes and Returns on Equity.

� Net Income Decreases, ROE increases

93

Scenario 1 Scenario 2

No Debt 50% Debt

Operating Profit 10,000,000 10,000,000

Interest Expense 0 800,000

EBT 10,000,000 9,200,000

Tax @ 40% 4,000,000 3,680,000

Net Income 6,000,000 5,520,000

No. of Equity Share 200,000 100,000

EPS 30 55.2

ROE 30% 55.2 %

© EduPristine PGCFR

Dividend and Share Repurchases

94

© EduPristine PGCFR

Coverage of the topic – Capital Budgeting

1. Dividends

a) Meaning

b) Chronology

c) Types

d) Forms

2. Important terms in relation to Shares

3. Share Repurchase and its methods

4. Effect of Share Repurchase on

a) Earning Per Share

b) Book value Per share

5. Similarity between Cash Dividends and Share Repurchase

95

© EduPristine PGCFR

Meaning of Dividends

Three main decision to be taken by a Finance Manager

1. Financing Decision : How to raise most optimum finance

2. Investment Decision: How to make most optimum investments

3. Dividend Decision: How to distribute profits in the most optimum manner

Share OR stock is the risk capital that is invested in the business

� Bonds, Bank Loan and Debentures are the e.g. of Borrowed capital

Dividends

� Every capital provider expects some return for contributing his capital in the business

� Return (in any form) paid by the company to its stockholders is called Dividend

96

Source of capital Type of Return

Equity Common Dividend

Preference Preference Dividend

Debt Interest

Common Objective:

To maximize

Shareholders’ wealth

© EduPristine PGCFR

Order of distribution of returns to different capital providers

97

Particulars

Sales

(Less) COGS

(Less) Selling Exp

(Less) Administrative Exp

(Less) General Exp

EBITDA

(Less) Depreciation

EBIT

(Less) Interest on Debt

EBT

(Less) Income Tax Expense

PAT

(Less) Preference Dividend

Earning Attributable to

Common stockholders

(Less) Common Dividends

Retained Earnings

1

2

3

Profit and Loss Account

Profit and Loss

Appropriation Account

© EduPristine PGCFR

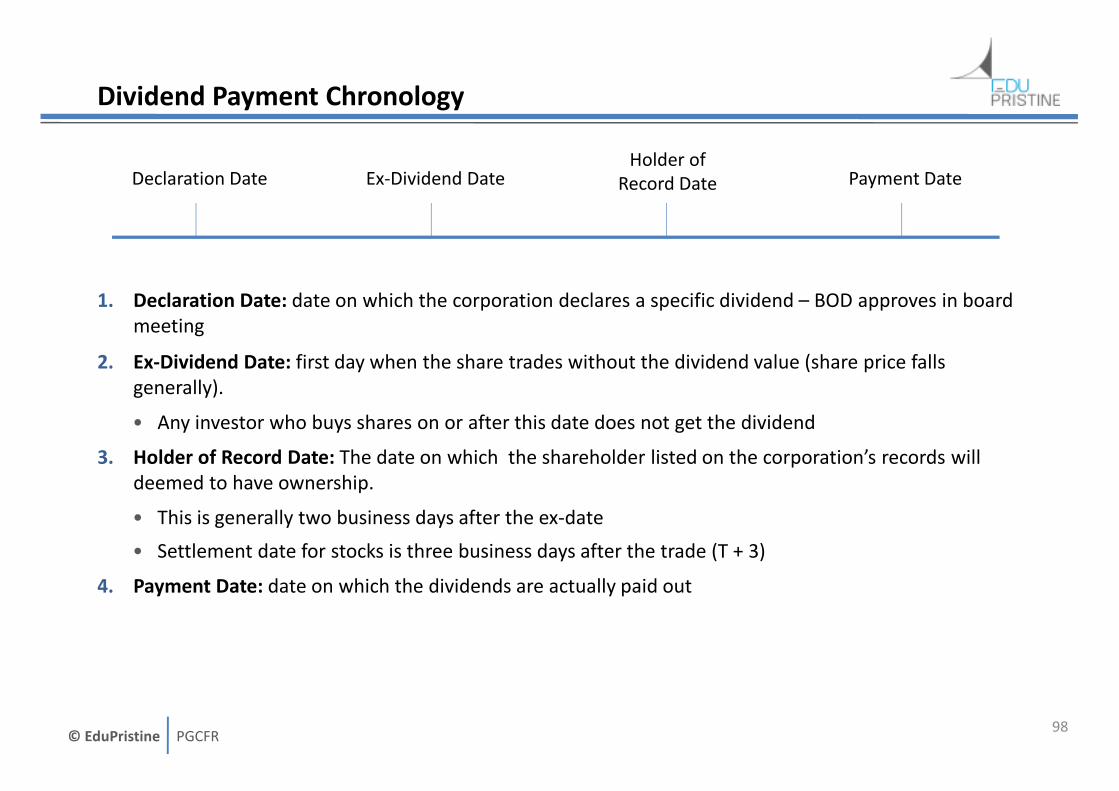

Dividend Payment Chronology

1. Declaration Date: date on which the corporation declares a specific dividend – BOD approves in board

meeting

2. Ex-Dividend Date: first day when the share trades without the dividend value (share price falls

generally).

• Any investor who buys shares on or after this date does not get the dividend

3. Holder of Record Date: The date on which the shareholder listed on the corporation’s records will

deemed to have ownership.

• This is generally two business days after the ex-date

• Settlement date for stocks is three business days after the trade (T + 3)

4. Payment Date: date on which the dividends are actually paid out

98

Declaration Date Ex-Dividend DateHolder of

Record Date Payment Date

© EduPristine PGCFR

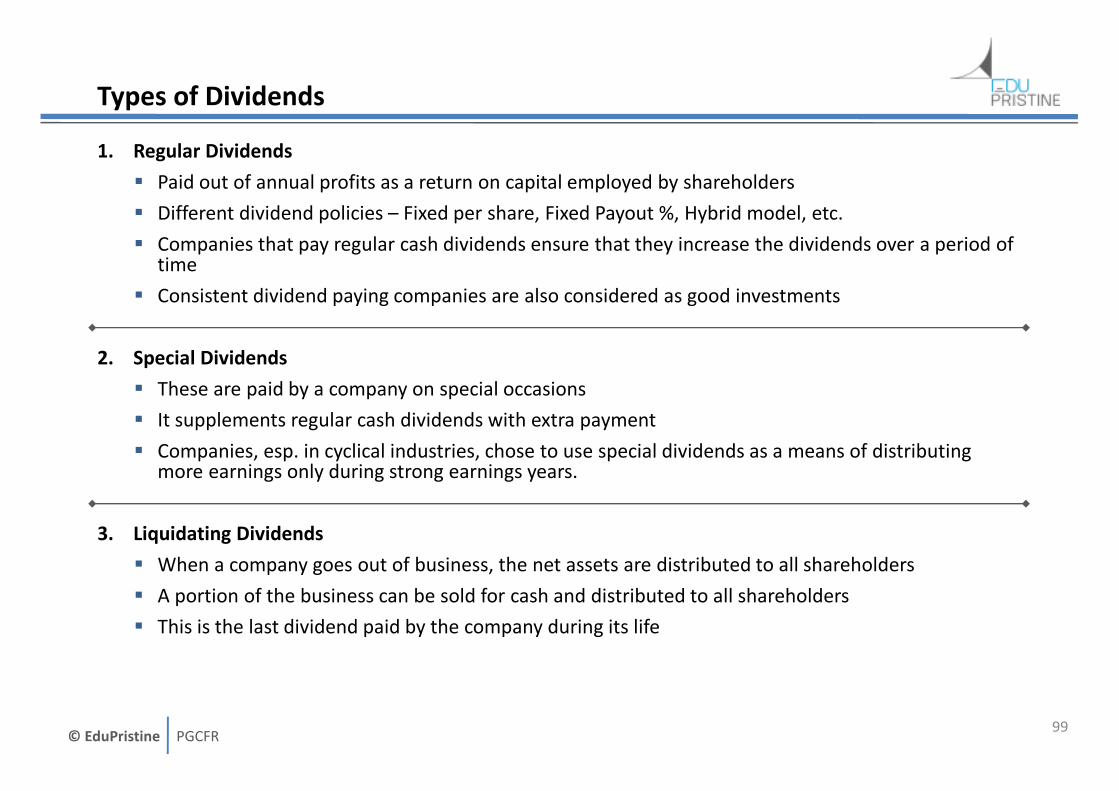

Types of Dividends

1. Regular Dividends

� Paid out of annual profits as a return on capital employed by shareholders

� Different dividend policies – Fixed per share, Fixed Payout %, Hybrid model, etc.

� Companies that pay regular cash dividends ensure that they increase the dividends over a period of time

� Consistent dividend paying companies are also considered as good investments

2. Special Dividends

� These are paid by a company on special occasions

� It supplements regular cash dividends with extra payment

� Companies, esp. in cyclical industries, chose to use special dividends as a means of distributing more earnings only during strong earnings years.

3. Liquidating Dividends

� When a company goes out of business, the net assets are distributed to all shareholders

� A portion of the business can be sold for cash and distributed to all shareholders

� This is the last dividend paid by the company during its life

99

© EduPristine PGCFR

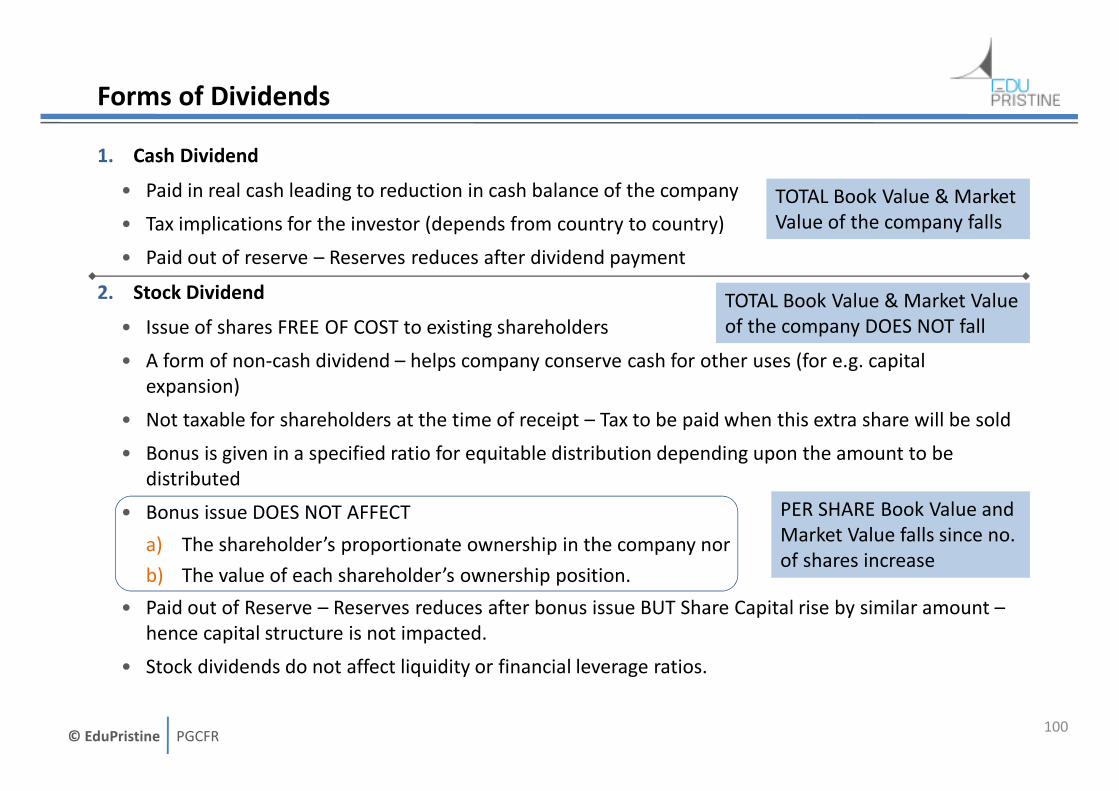

Forms of Dividends

1. Cash Dividend

• Paid in real cash leading to reduction in cash balance of the company

• Tax implications for the investor (depends from country to country)

• Paid out of reserve – Reserves reduces after dividend payment

2. Stock Dividend

• Issue of shares FREE OF COST to existing shareholders

• A form of non-cash dividend – helps company conserve cash for other uses (for e.g. capital

expansion)

• Not taxable for shareholders at the time of receipt – Tax to be paid when this extra share will be sold

• Bonus is given in a specified ratio for equitable distribution depending upon the amount to be

distributed

• Bonus issue DOES NOT AFFECT

a) The shareholder’s proportionate ownership in the company nor

b) The value of each shareholder’s ownership position.

• Paid out of Reserve – Reserves reduces after bonus issue BUT Share Capital rise by similar amount –

hence capital structure is not impacted.

• Stock dividends do not affect liquidity or financial leverage ratios.

100

TOTAL Book Value & Market

Value of the company falls

TOTAL Book Value & Market Value

of the company DOES NOT fall

PER SHARE Book Value and

Market Value falls since no.

of shares increase

© EduPristine PGCFR

Important terms in relation to shares

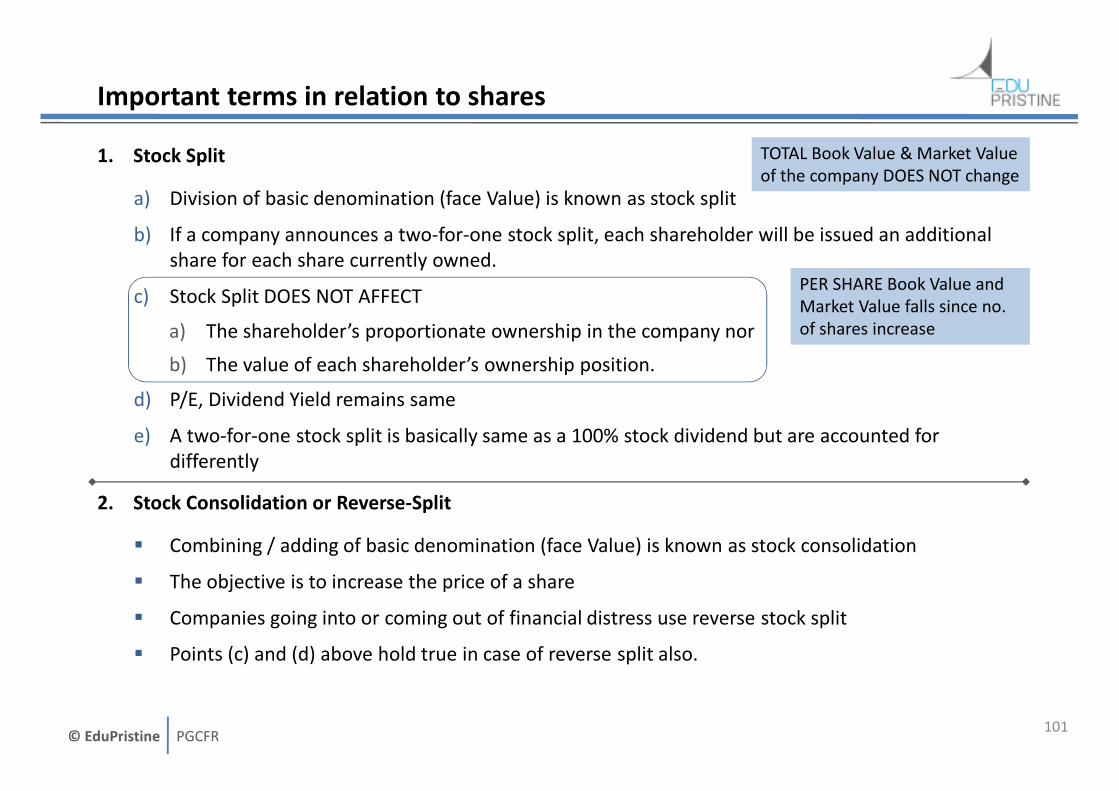

1. Stock Split

a) Division of basic denomination (face Value) is known as stock split

b) If a company announces a two-for-one stock split, each shareholder will be issued an additional

share for each share currently owned.

c) Stock Split DOES NOT AFFECT

a) The shareholder’s proportionate ownership in the company nor

b) The value of each shareholder’s ownership position.

d) P/E, Dividend Yield remains same

e) A two-for-one stock split is basically same as a 100% stock dividend but are accounted for

differently

2. Stock Consolidation or Reverse-Split

� Combining / adding of basic denomination (face Value) is known as stock consolidation

� The objective is to increase the price of a share

� Companies going into or coming out of financial distress use reverse stock split

� Points (c) and (d) above hold true in case of reverse split also.

101

TOTAL Book Value & Market Value

of the company DOES NOT change

PER SHARE Book Value and

Market Value falls since no.

of shares increase

© EduPristine PGCFR

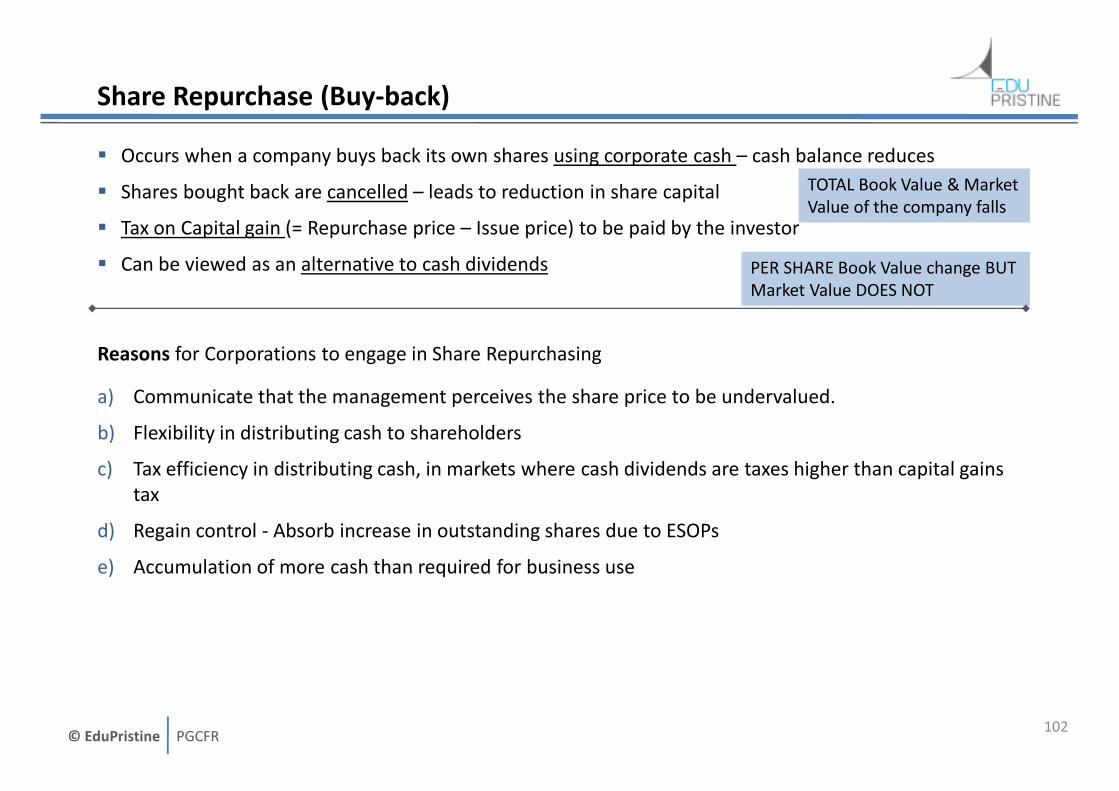

Share Repurchase (Buy-back)

� Occurs when a company buys back its own shares using corporate cash – cash balance reduces

� Shares bought back are cancelled – leads to reduction in share capital

� Tax on Capital gain (= Repurchase price – Issue price) to be paid by the investor

� Can be viewed as an alternative to cash dividends

Reasons for Corporations to engage in Share Repurchasing

a) Communicate that the management perceives the share price to be undervalued.

b) Flexibility in distributing cash to shareholders

c) Tax efficiency in distributing cash, in markets where cash dividends are taxes higher than capital gains

tax

d) Regain control - Absorb increase in outstanding shares due to ESOPs

e) Accumulation of more cash than required for business use

102

TOTAL Book Value & Market

Value of the company falls

PER SHARE Book Value change BUT

Market Value DOES NOT

© EduPristine PGCFR

Methods of Share Repurchase

Following are four common methods in which shares are repurchased:

1. Buy in the open market

• This approach is very flexible for the company

• Allows the company to purchase shares from the open market at current market price

• The company can time its purchases to exploit any perceived under evaluation in the market

2. Buy fixed number of shares at fixed price

• The company makes a fixed price tender offer to existing shareholders to repurchase a specific

number of shares at a fixed price

• The company may offer to buy shares at some premium to the market prices prevailing

3. Dutch Auction

• Similar to a fixed price buy except company announces a band of prices instead of the fixed price

• Provides the company with the minimum cost at which it can repurchase the shares

4. Repurchase by Direct Negotiation

• If any shareholder has a large stake then the company can negotiate directly with that shareholder

103

© EduPristine PGCFR

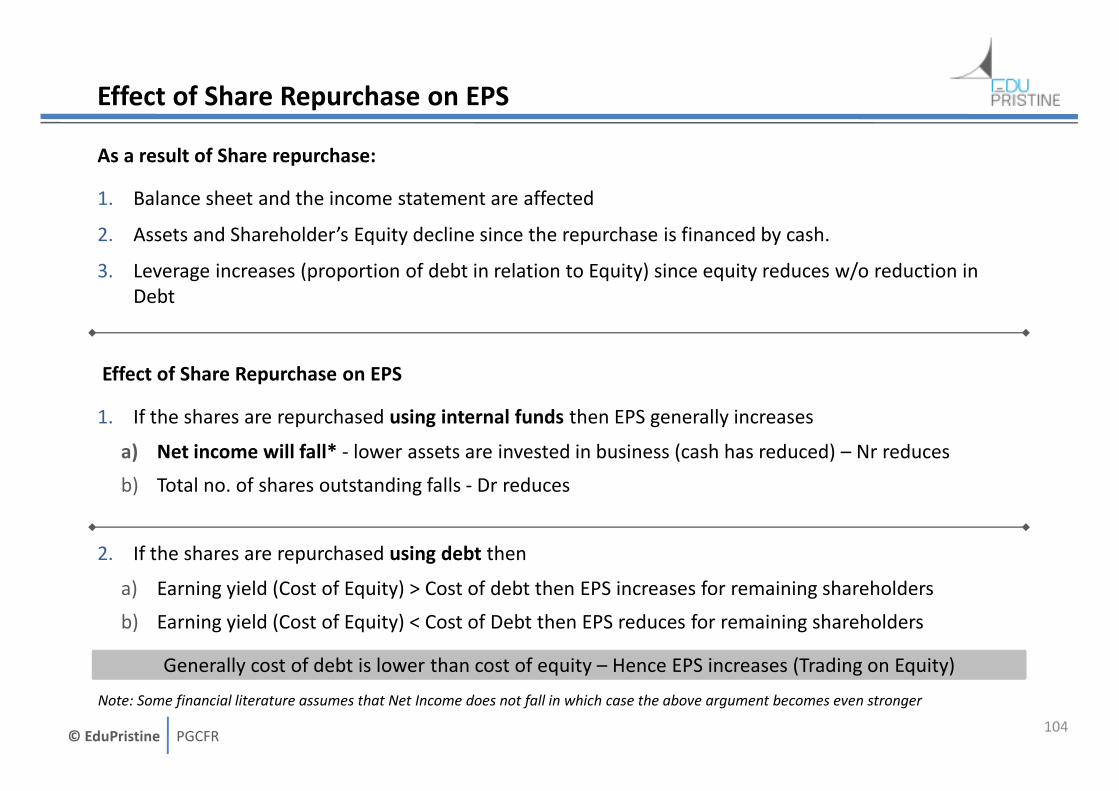

Effect of Share Repurchase on EPS

As a result of Share repurchase:

1. Balance sheet and the income statement are affected

2. Assets and Shareholder’s Equity decline since the repurchase is financed by cash.

3. Leverage increases (proportion of debt in relation to Equity) since equity reduces w/o reduction in

Debt

Effect of Share Repurchase on EPS

1. If the shares are repurchased using internal funds then EPS generally increases

a) Net income will fall* - lower assets are invested in business (cash has reduced) – Nr reduces

b) Total no. of shares outstanding falls - Dr reduces

2. If the shares are repurchased using debt then

a) Earning yield (Cost of Equity) > Cost of debt then EPS increases for remaining shareholders

b) Earning yield (Cost of Equity) < Cost of Debt then EPS reduces for remaining shareholders

104

Note: Some financial literature assumes that Net Income does not fall in which case the above argument becomes even stronger

Generally cost of debt is lower than cost of equity – Hence EPS increases (Trading on Equity)

© EduPristine PGCFR

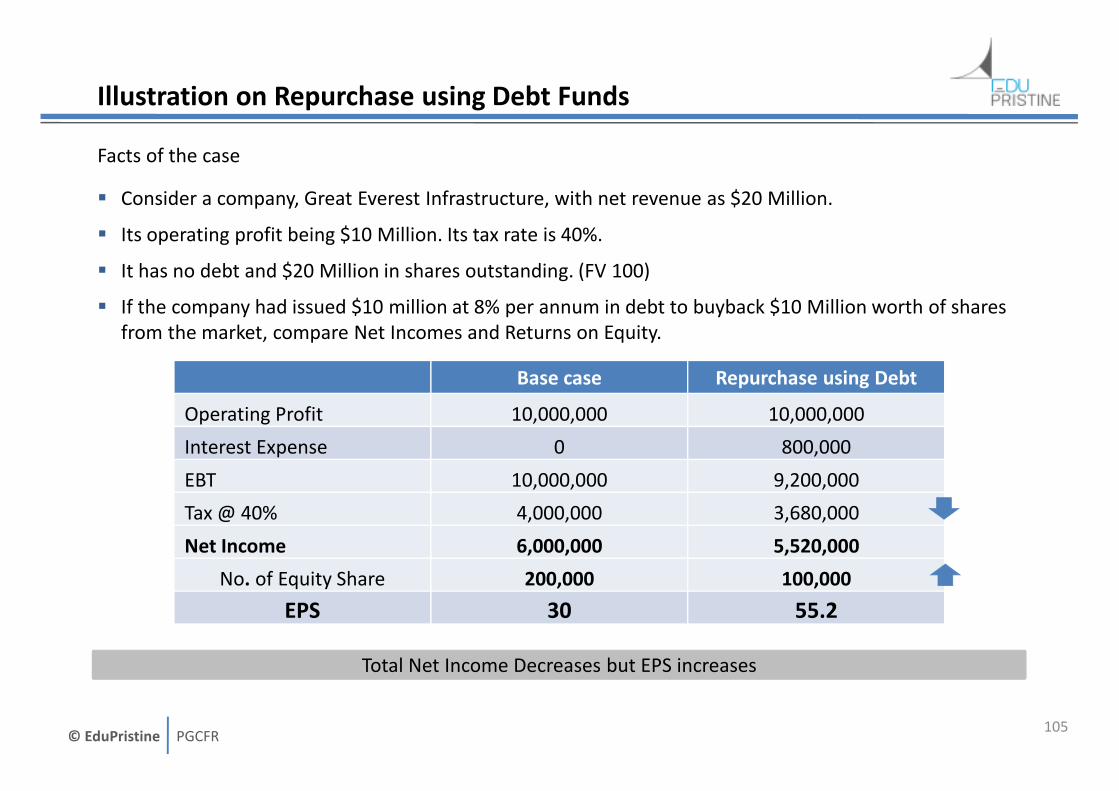

Illustration on Repurchase using Debt Funds

Facts of the case

� Consider a company, Great Everest Infrastructure, with net revenue as $20 Million.

� Its operating profit being $10 Million. Its tax rate is 40%.

� It has no debt and $20 Million in shares outstanding. (FV 100)

� If the company had issued $10 million at 8% per annum in debt to buyback $10 Million worth of shares

from the market, compare Net Incomes and Returns on Equity.

105

Base case Repurchase using Debt

Operating Profit 10,000,000 10,000,000

Interest Expense 0 800,000

EBT 10,000,000 9,200,000

Tax @ 40% 4,000,000 3,680,000

Net Income 6,000,000 5,520,000

No. of Equity Share 200,000 100,000

EPS 30 55.2

Total Net Income Decreases but EPS increases

© EduPristine PGCFR

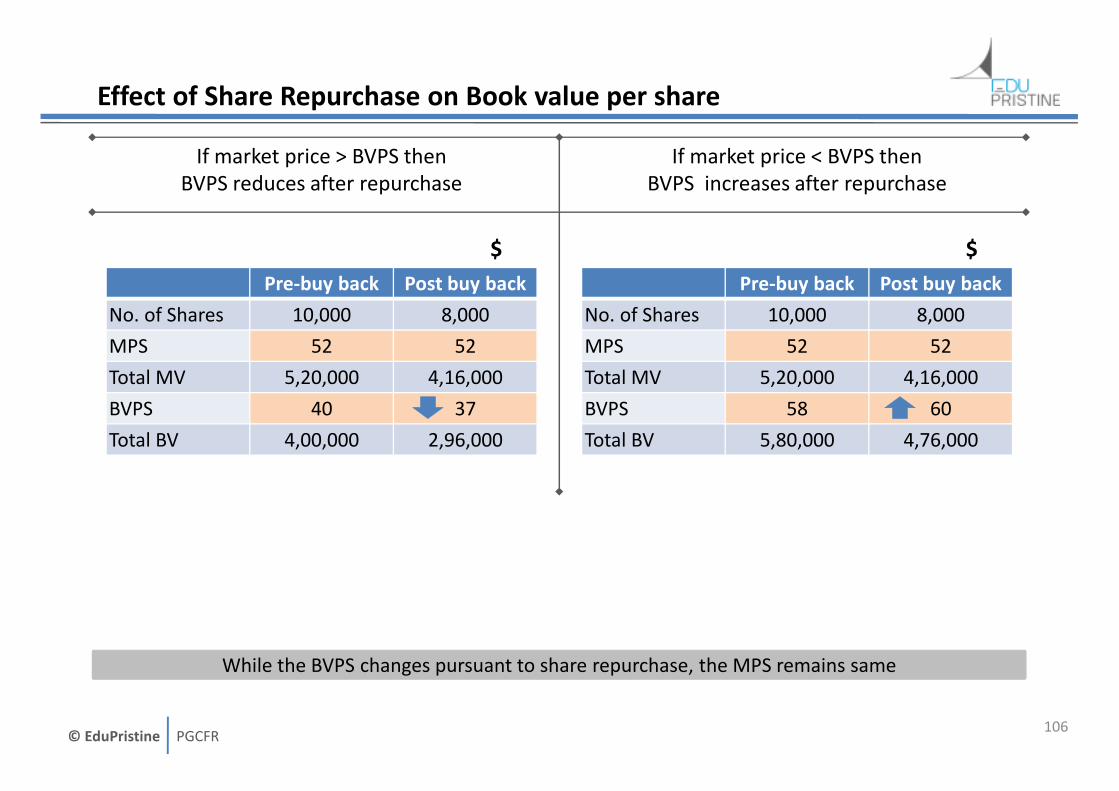

Effect of Share Repurchase on Book value per share

If market price > BVPS then

BVPS reduces after repurchase

If market price < BVPS then

BVPS increases after repurchase

106

Pre-buy back Post buy back

No. of Shares 10,000 8,000

MPS 52 52

Total MV 5,20,000 4,16,000

BVPS 40 37

Total BV 4,00,000 2,96,000

Pre-buy back Post buy back

No. of Shares 10,000 8,000

MPS 52 52

Total MV 5,20,000 4,16,000

BVPS 58 60

Total BV 5,80,000 4,76,000

$$

While the BVPS changes pursuant to share repurchase, the MPS remains same

© EduPristine PGCFR

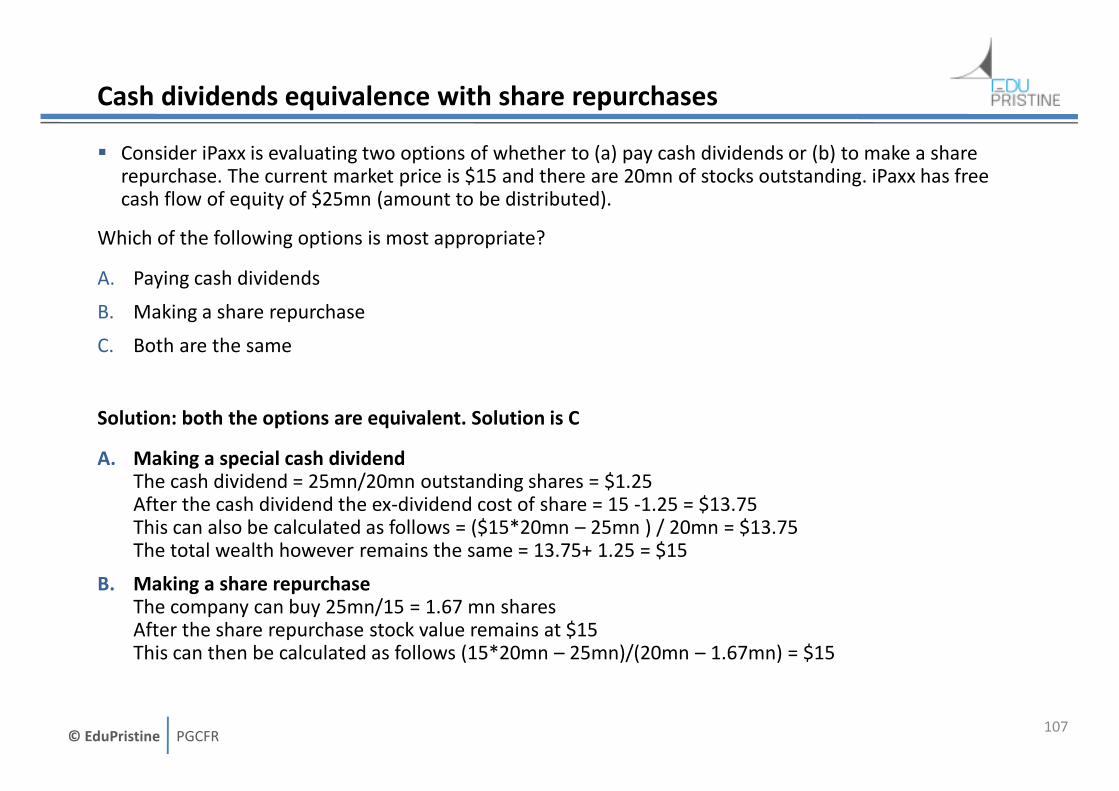

Cash dividends equivalence with share repurchases

� Consider iPaxx is evaluating two options of whether to (a) pay cash dividends or (b) to make a share repurchase. The current market price is $15 and there are 20mn of stocks outstanding. iPaxx has free cash flow of equity of $25mn (amount to be distributed).

Which of the following options is most appropriate?

A. Paying cash dividends

B. Making a share repurchase

C. Both are the same

Solution: both the options are equivalent. Solution is C

A. Making a special cash dividendThe cash dividend = 25mn/20mn outstanding shares = $1.25After the cash dividend the ex-dividend cost of share = 15 -1.25 = $13.75This can also be calculated as follows = ($15*20mn – 25mn ) / 20mn = $13.75The total wealth however remains the same = 13.75+ 1.25 = $15

B. Making a share repurchaseThe company can buy 25mn/15 = 1.67 mn sharesAfter the share repurchase stock value remains at $15This can then be calculated as follows (15*20mn – 25mn)/(20mn – 1.67mn) = $15

107

© EduPristine PGCFR

Questions

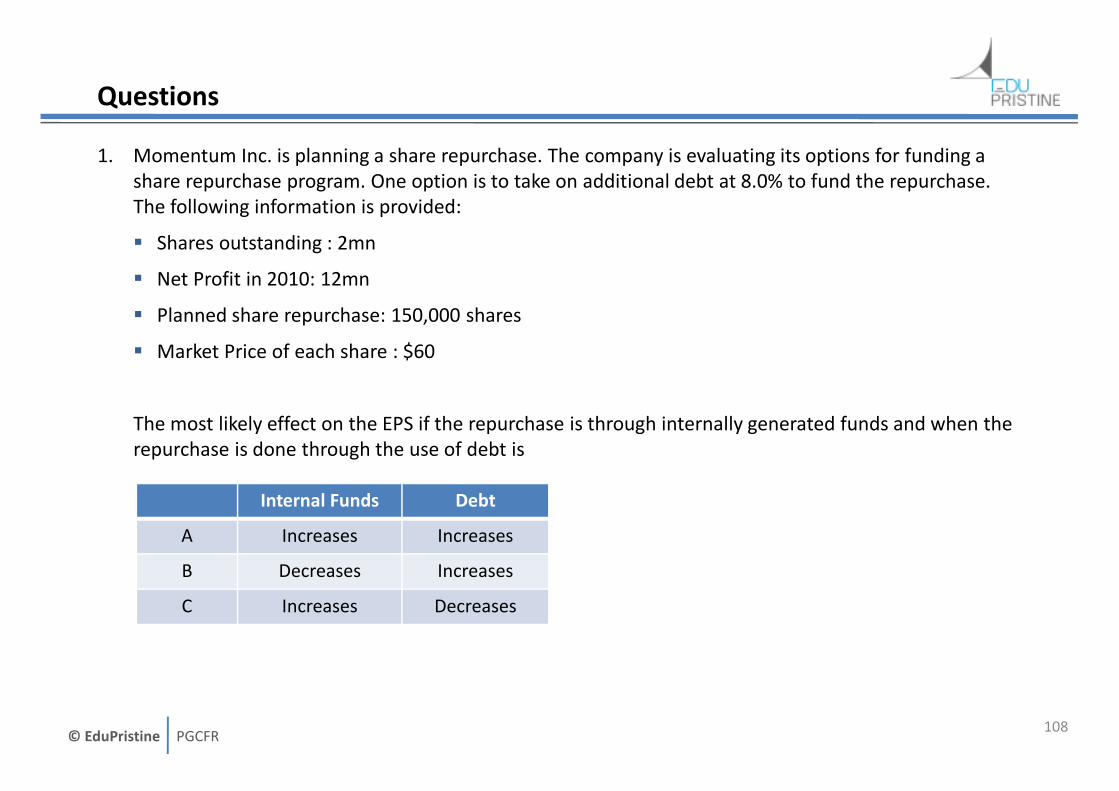

1. Momentum Inc. is planning a share repurchase. The company is evaluating its options for funding a

share repurchase program. One option is to take on additional debt at 8.0% to fund the repurchase.

The following information is provided:

� Shares outstanding : 2mn

� Net Profit in 2010: 12mn

� Planned share repurchase: 150,000 shares

� Market Price of each share : $60

The most likely effect on the EPS if the repurchase is through internally generated funds and when the

repurchase is done through the use of debt is

108

Internal Funds Debt

A Increases Increases

B Decreases Increases

C Increases Decreases

© EduPristine PGCFR

Questions (cont…)

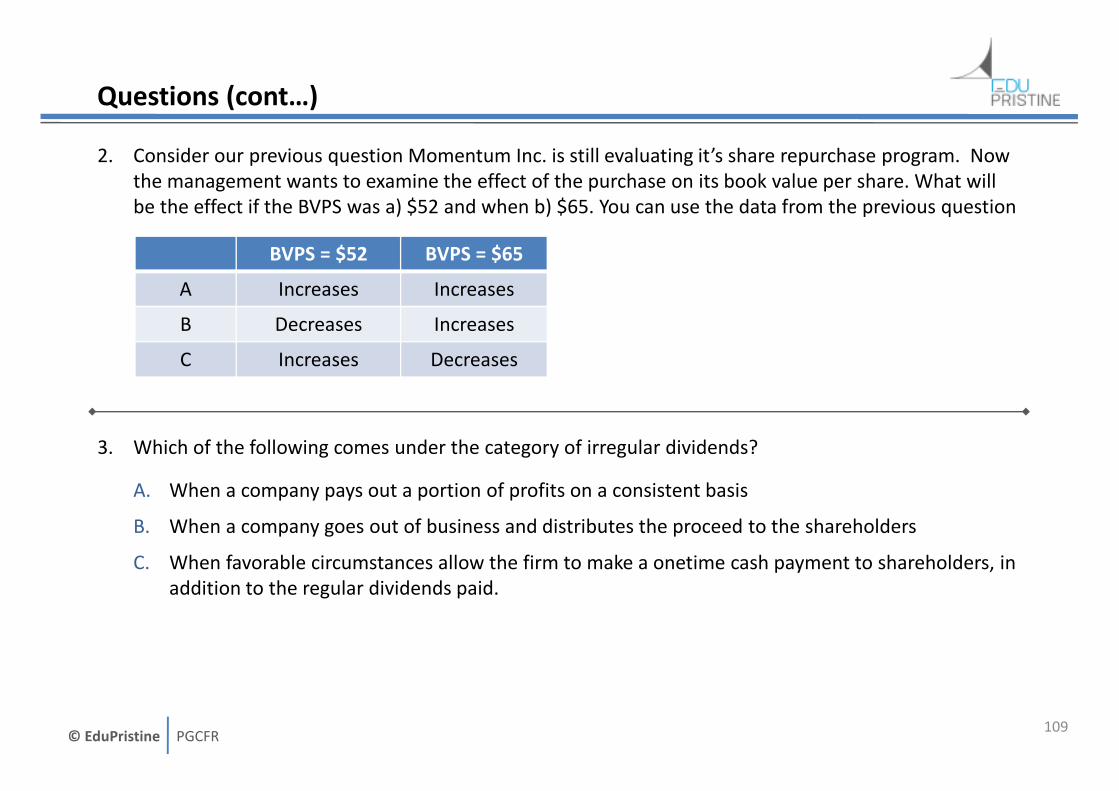

2. Consider our previous question Momentum Inc. is still evaluating it’s share repurchase program. Now

the management wants to examine the effect of the purchase on its book value per share. What will

be the effect if the BVPS was a) $52 and when b) $65. You can use the data from the previous question

3. Which of the following comes under the category of irregular dividends?

A. When a company pays out a portion of profits on a consistent basis

B. When a company goes out of business and distributes the proceed to the shareholders

C. When favorable circumstances allow the firm to make a onetime cash payment to shareholders, in

addition to the regular dividends paid.

109

BVPS = $52 BVPS = $65

A Increases Increases

B Decreases Increases

C Increases Decreases

© EduPristine PGCFR

Answers

1. AThe EPS in FY 2010 = 12mn / 2mn = $6When the repurchase is funded through internal funds then the EPS increases as the shares outstanding decreases while the net profit remains the same or reduces by a lower amount: (12mn)/(2mn – 150,000) = $6.48The earnings yield is E/P : 6/60 = 10%Cost of Repurchase = 150,000*60 = 9mnEPS after repurchase = ( 12mn – 9mn*8%)/(2mn – 150,000) = 6.09OrSince the Cost of Funding < Earning yield the EPS will increase after the buyback

2. BNo calculations are required as when Market Price > BVPS then the book value will decrease after repurchase. If MP < BVPS then the book value will increase after repurchase.

3. CSpecial dividends are paid when favorable circumstances allow the firm to make a onetime cash payment to shareholders, in addition to the regular dividends paid. Special dividends are also called extra dividends and irregular dividends.

110

© EduPristine PGCFR

Working Capital Management

111

© EduPristine PGCFR

Coverage of the topic – Working Capital Management

1. Meaning and Need of Working Capital Management

2. Important terms used in WCM

3. Elements of Working Capital

1. Current Assets – Cash, Inventory, Account Receivable

2. Current Liabilities – Accounts Payable

4. Sources of short term funding

1. Banking channel

2. Non-Banking channel

112

© EduPristine PGCFR

Meaning of Working Capital

� There are two types of capital which is required by any firm:

1. Fixed or Permanent Capital

– Capital which is invested in long term assets of the firm

– E.g. buying of machinery for production will need funds to finance it

– Once invested, it is blocked for a longer term

2. Working Capital

• Capital which is required to utilize or operate the long term assets

• E.g. amount blocked / utilised in

– Purchase of Raw material

– Payment of wages to workers

– Production of Finished goods

– Financing of A/Rs,

• Once invested, it gets released after short term after which again it is required to be invested (keeps

rotating)

113

© EduPristine PGCFR

Meaning of Working Capital (Contd.)

Investment in working capital means investment into the current assets of the firm like:

� Raw Material

� WIP

� Finished Products

� Account receivable

� Prepaid expenses

Current Assets

� Assets which are likely to be converted into cash within 1 year OR 1 operating cycle whichever is longer

This need for investment into current assets of the firm is contributed by:

� Externally by Current Liabilities

� Internally by WC financing

Current Liabilities

� Liabilities which are likely to be paid within 1 year OR 1 operating cycle whichever is longer

114

Working capital = Current Assets - Current liability

© EduPristine PGCFR

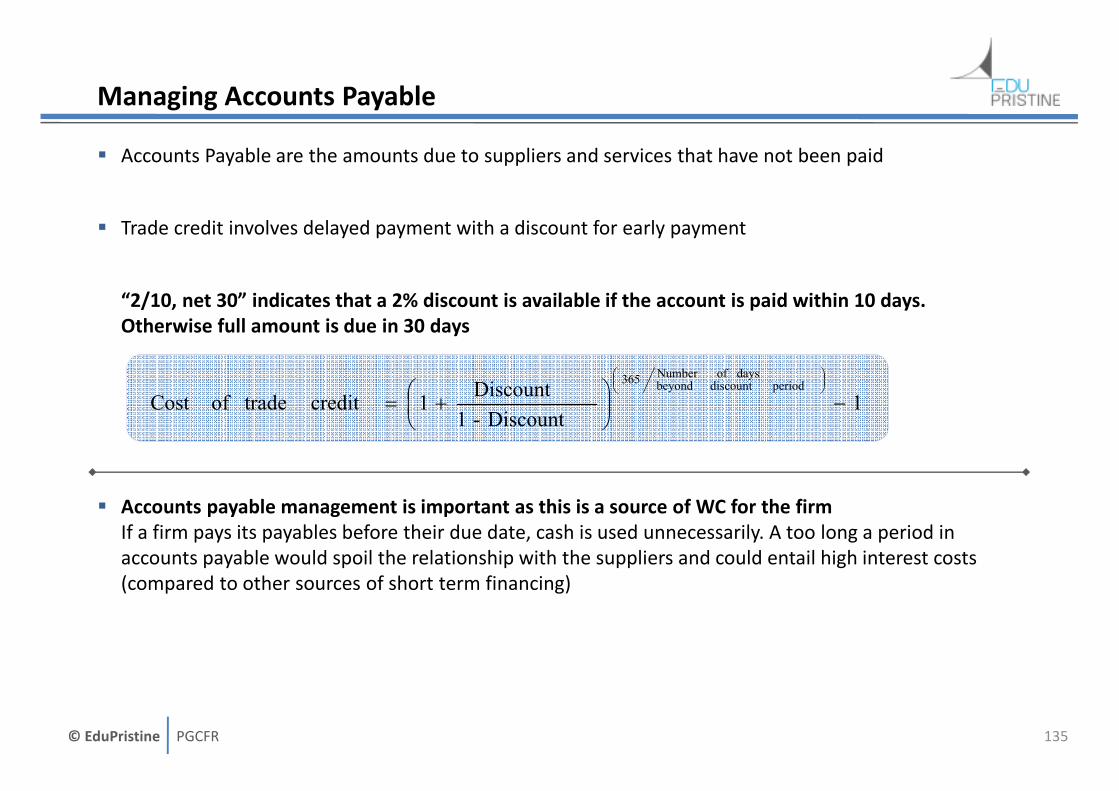

Trade-off in working capital management

� There is a trade-off between stricter credit terms and the ability to make sales. Too strict

receivables terms would hamper sales and lenient terms would tie up too much capital

� Inventory management is also a trade-off: High inventory levels (as might be reflected by low

inventory turnover or longer days of inventory) will cause high costs of carry and low inventory

levels may result in lost sales due to stock outs

� Accounts payable management is important as this is a source of working capital for the firm

If a firm pays its payables before their due date, cash is used unnecessarily. A too long a period in

accounts payable would spoil the relationship with the suppliers and could entail high interest

costs (compared to other sources of short term financing)

115

© EduPristine PGCFR

Meaning of Liquidity (availability of cash)

� Liquidity is very closely related to Working capital. In fact, it is the mirror image of Working

capital

� Liquidity : the extent to which a company is able to meet its short-term obligations using assets

that can be readily converted to cash

• In other words, it is the ability of the firm to repay (or cover) its short term liabilities (current liabilities)

• This is a cash concept (not a accrual concept)

• Lack of liquidity can lead to bankruptcy

� Liquidity Management – The ability of an organization to generate cash when and where it is

needed

� It is the abundance of current assets over and above the current liabilities (which is equal to WC)

• Greater the current assets to meet current liabilities, lower the risk and thus better it is for the firm

116

© EduPristine PGCFR

Two Sources of Liquidity

1. Primary Sources of Liquidity

� These are 1st resorts which are available to a firm to raise short term finance

� These include selling operational assets or increasing operational liabilities

a) Bank Accounts

b) Collections from ARs

c) Liquidation of short term maturity securities

d) Trade Credit

e) Bank lines of credit

2. Secondary Sources of Liquidity

� These are sources that are used in case of emergency

a) From long term liability : Negotiating Debt Contracts

b) Liquidating assets : short term/long term assets

c) Filing for bankruptcy protection and reorganization

117

Primary Sources of Liquidity would most likely not disturb the normal operations of the company

Use of secondary resources may signal a company’s deteriorating financial health

and provide liquidity at a high price

© EduPristine PGCFR

Factors that reduce liquidity position

1. Drags: When collection reduces (lags) creating pressure from the decreased availability of funds

1. Uncollected receivables

2. Obsolete Inventory

3. Tight Credit (difficult to raise finance>> lower inflows)

2. Pulls: when payments are made faster than scheduled

� Making payments to Accounts Payable early

� Reduced credit limits that require prepayment of existing outstanding balance

118

© EduPristine PGCFR

Comparison of a firm’s liquidity with its peers

There are different ratios using which are used together

Liquidity ratios

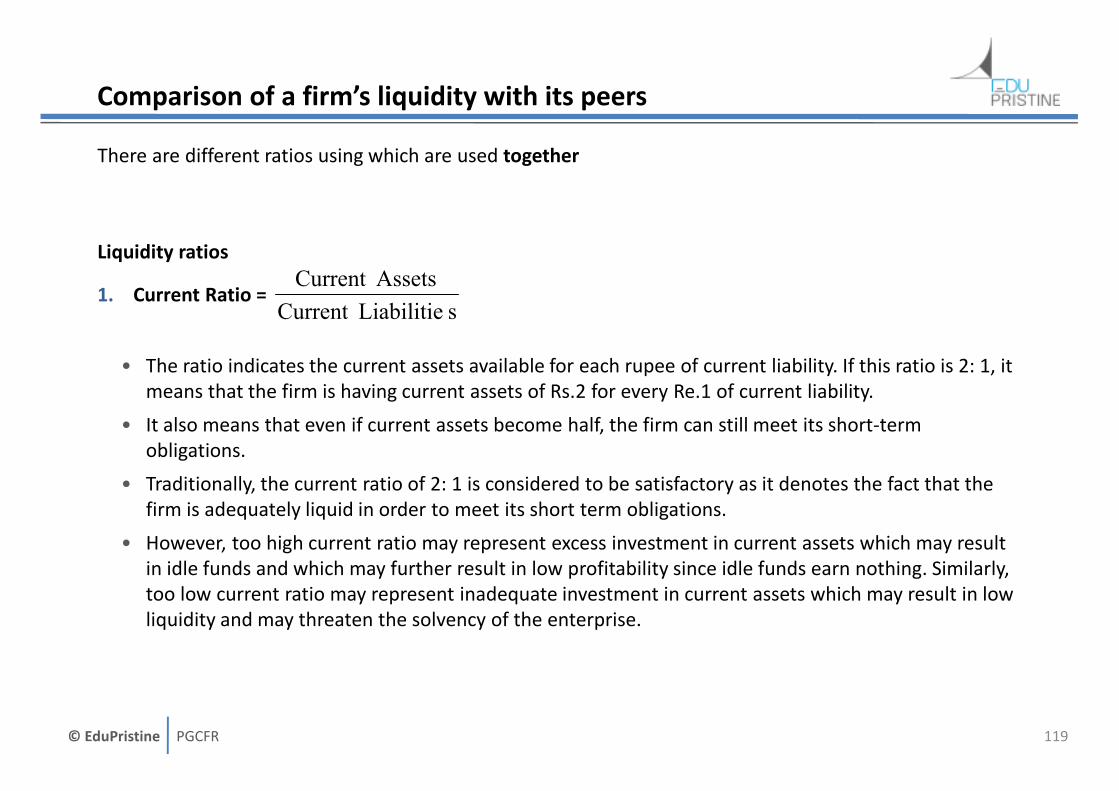

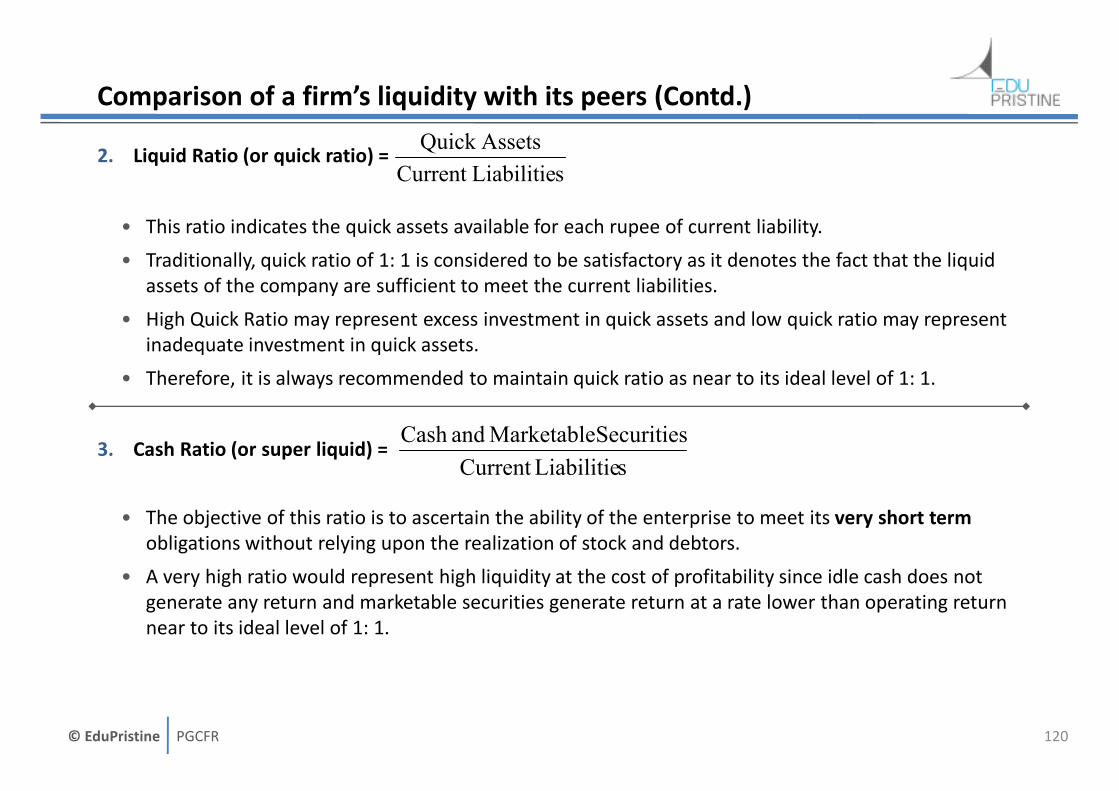

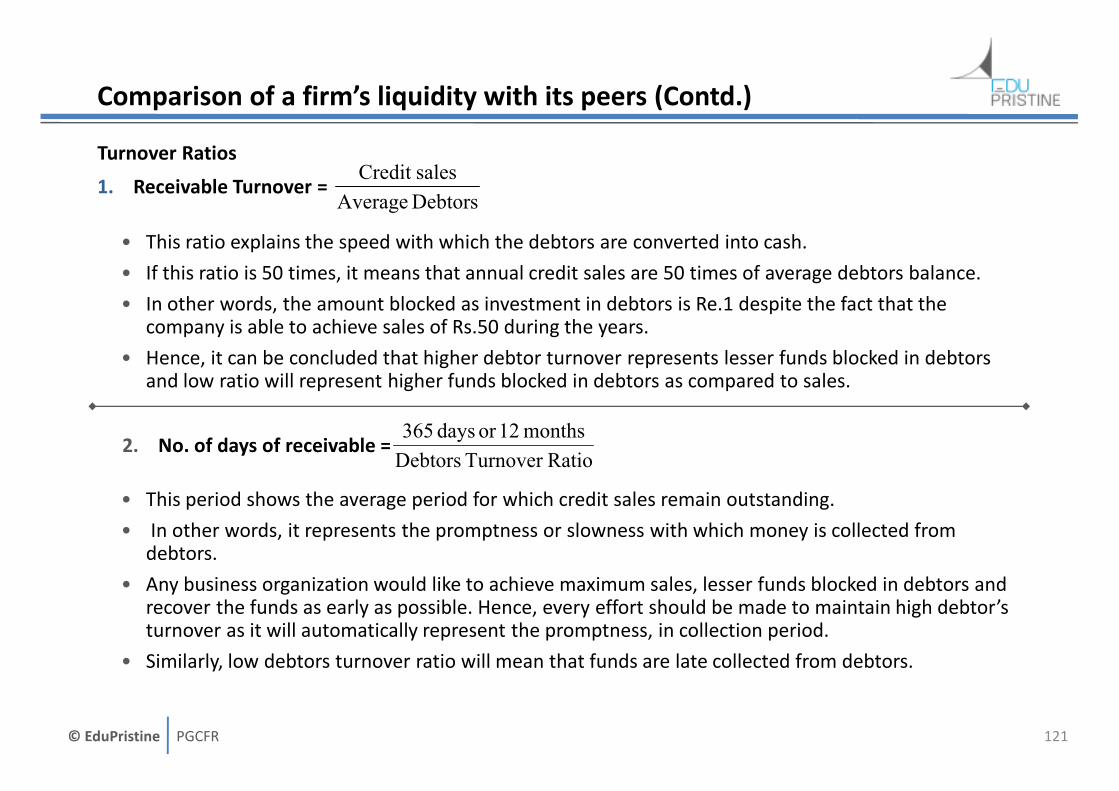

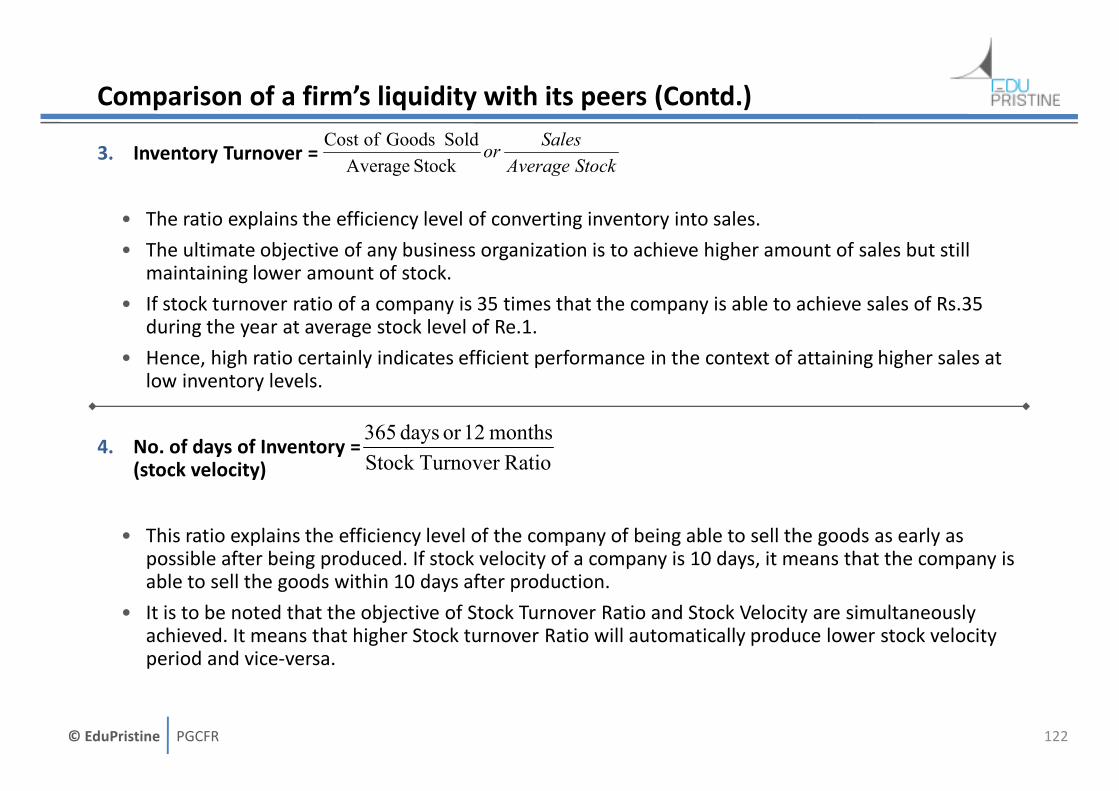

1. Current Ratio =

• The ratio indicates the current assets available for each rupee of current liability. If this ratio is 2: 1, it

means that the firm is having current assets of Rs.2 for every Re.1 of current liability.

• It also means that even if current assets become half, the firm can still meet its short-term

obligations.