課程 5: real estate financing. flow of real estate financial capital the issues: real estate is...

TRANSCRIPT

課程 5: Real Estate Financing

Flow of Real Estate Financial Capital

• The issues:• Real estate is capital intensive

• Typical capital structure is dominated by debt

• That is a major portion of the funds to purchase a home or construct an office building, etc must be borrowed

• The segment of the capital markets where these funds come from are called mortgage markets

• This sector of the debt market is by far the largest in the US and in some respect the world

Flow of Real Estate Financial Capital

• Potential developers, homeowners etc. must obtain financing in order to build, own and operate properties

• Funds are supplied by a variety of individuals, firms, institutions and government as shown in the figure

• Between the users and the sources of funds are a number of service organizations that make the raising of capital easier and more efficient

• Financial capital flows from suppliers to users in the form of debt (mortgage) and equity

• Providers of debt have priority claim on the revenue from operation• Equity holders have residual claim on cash flow

The Flow of Real Estate Financial Capital

ThriftsCommercial BanksInsurance companiesPension FundsREITsCredit UnionsGovernmentsNonfinancial businessHouseholdsForeign Investors

Mortgage BankersMortgage BrokersReal Estate BrokersInvestment BankersGovernment agenciesSyndicators

DevelopersOwners of HomesOwners of income PropertiesLand Owners

SUPPLIESOF CAPITAL

SERVICE GROUPS USERS OF CAPITAL

Equity

Debt

E

D

7.70%

8.11%6.09%

8.67%

9.34%

23.96% 36.12%

Mortgages

U.S. Government

Corporate Bonds

Consumer Credit

Bank Loans andCommercial Paper

Tax ExemptObligations

All Others3Q 1994

total: $12,309 Billion

Total Credit Outstanding in U.STotal Credit Outstanding in U.S

The Supply of Mortgage Debt • Types of lenders

– Portfolio lenders

– Non-portfolio lenders

– Depository institutions

– Contractual or non-depository institutions

– Specialized mortgage market intermediaries

• mortgage companies

• federally related agencies or GSEs

• real estate investment trusts

• Types of loans– Construction Loans

– Permanent loans

Total Mortgage Outstanding

1-4 family

Multifamily

Comm.

Farm

75.2%

16.1%

1.6%6.8%

Total $4,279 (billions, 3rd Q 1994)

Total Mortgage Debt Outstanding

• The total mortgage outstanding is around $4.3 trillion– single family mortgage debt accounts for the biggest share 75.2

% or $3.2 trillion ($3,217.5 billion)

– Commercial and multifamily accounts for roughly 23% or $1 trillion

• Residential Mortgages– Commercial banks and S&Ls are the major portfolio lenders of whole loans

– Roughly 49% or $1.6 trillion of the mortgages are securitized mainly by GNMA, FNMA FHLMC or GSEs

– GSEs hold 7.6% or $246.1 billion of whole loans

– GSEs account for roughly 57% or $1.75 trillion of 1-4 family residential mortgages

Mortgage Market Participants

Originations Servicing Holdings0

200

400

600

800

1000

Originations Servicing Holdingsthriftsmortgage CompaniesFederally Chartered CompaniesInsurance CompaniesCommercial BanksPension and Retirement FundsAll Others

In Billions of Dollars

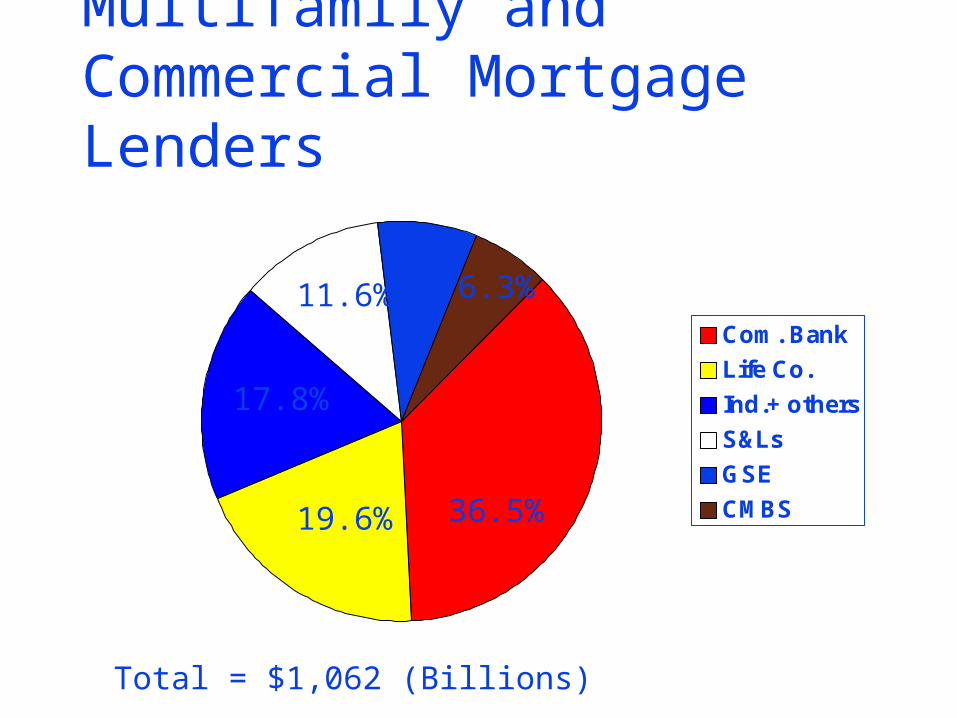

Multifamily and Commercial Mortgage Lenders

Com. Bank

Life Co.

Ind.+ others

S&Ls

GSE

CMBS36.5%19.6%

17.8%

11.6%8.1%

6.3%

Total = $1,062 (Billions)

Commercial Mortgage Markets• Commercial mortgage market is smaller than residential market

• $1.1 trillion versus $3.2 trillion

• This market is far less securitized than the residential market

• 6.3% or $66.8 billion versus 49% or $1.6 trillion

• Federal agencies are far less involved in commercial mortgages

• The market is dominated by private sector institutions including life insurance companies, S&Ls and commercial banks

• life insurance companies are largest providers of commercial mortgages

• S&Ls expanded their lending activities aggressively into commercial mortgages during the 1980s

Commercial Mortgage Market• During 1996 approximately $20 billion of whole loans were originated by life

insurance companies as reported by ACLI

• Throughout the year traditional commercial lenders enjoyed attractive spreads, solid underwriting and good real estate market fundamentals

• Traditional lenders dominated the market for $10 M to 50 M mortgages on institutional quality offices, warehouses, apartments and retail

• The Market still remains the domain of familiar names: Principal Financial, TIAA, Northwestern Mutual, Metropolitan Life and Minnesota Mutual to name a few

• No shows: Equitable, Life, Travelers, Aetna and Prudential

• Problem loans remained at record low: 2.51 % (3 Q 1996) vr. 2.35 (4Q 1995)

• Wall Street dominates two extremes of the market: filled the void left by S&Ls for low-quality loans and jumbo-sized high-quality loans amenable to “single asset” securitization

Lender Requirements 4Q/95 4Q/96

Insurance Companies/Pension ( “A” quality RE) Rates 6.75 - 7.50% 7.50 - 8.15% Spreads (UST) 125-175 bp 125- 175 bp Max. Loan-to-value 75% 75% Min. Debt Service Coverage 1.20x 1.20x Term 7-10 yrs 7-10 yrs

Commercial Banks (“A” Quality Real Estate) Rates --- Fixed 6.65 - 7.50% 7.25 - 8.15% Rates --- Floating 6.75- 8.00% 6.60 - 7.60% Spreads -- Fixed (UST) 135 - 200 bp 125 - 175 bp Spread -- Floating (LIBOR) 125 - 250 bp 100 - 200 bp Max. loan-to-value 75% 75% Min. Debt Service Coverage 1.20x 1.20x Term 7 - 10 yrs 7 - 10 yrs

Conduits (“B” & “C”) Quality Real Estate) Rates 7.50 - 8.25% 8.20 - 9.15% Spreads (UST) 200 - 275 bp 200 - 275 bp Max. Loan-to-Value 75% 75% Min. Debt Service Coverage 1.20x 1.20x Term 5 - 10 yrs 5 -10 yrs

*Represents typical transaction, not full range; Source: Equitable Real Estate Investment Management

COMMERCIAL MORTGAGE CAPITAL SOURCE

Delinquency Rates by Property Type

Sector 3Q/1995 2Q/1996 3Q/1996 12-mo-change

Apartment 1.80% 0.99% 1.02% -0.78%

Retail 1.95% 1.82% 1.75% -0.20%

Office 4.32% 4.27% 4.14% -0.18%

Industrial 3.96% 1.77% 1.47% -2.49%

Hotel 5.20% 2.67% 2.80% -2.40%

Source: American Council of Life Insurance (ACLI); 1996 Mean = 2.51%, 1995 Mean = 2.35%

Why Study Mortgage Market ?

• Shed light on how traditional method of financing assets by financial intermediaries is rapidly changing

• securitization is the new BIG BROTHER

• Demonstrates how financial engineering can redirect cash flows to create securities that more closely satisfy the asset/liability needs of investors

• Government agencies provide Credit guarantees for mortgage backed securities

• should government agencies continue to provide guarantee

Supply of loanable funds

• The amount of funds borrowed and lent depends on interest rates.– As rates rise many spending units save more and spend less

– Simultaneously when interest rates rise many spending units demand less credit

– The figure following illustrates the operation of supply and demand for loanable funds

– The demand schedule is downward sloping, reflecting greater willingness to borrow at lower rates.

– The supply schedule, s1, rise to the right, because people have more to lend at higher rates

– The intersection of the of the two schedules determines the amount of funds lent, f1, and the prevailing interest rate, i1

Supply and demand for loanable funds

d1

s2

s1

f1 f2

i1

i2

Amount of loanable funds

Interestrate

Real Estate Financial Instrument

• When ever real estate is financed, the property is pledged as collateral or security creating a financial instrument known either as MORTGAGE or DEED OF TRUST Power of secured debt: attempting to buy a $300 suit on credit versus obtaining $200,000 loan to build a house

– Mortgage : Two Parties– Deed of Trust : Three Parties– Promissory Note– Title Pledge

Note + Pledge

Funds

Pledge and lien are extinguished with performance of mortgage contract

MORTGAGE

Borrower(Mortgagor)

Lender(Mortgagee)

A bilateral financial contract

Note

Funds

pledgeof title

Titlegoesto borrowif nodefault

if defaultpropertyis soldand proceedsgoes tolender

DEED OF TRUST

Borrower(Trustor)

Lender(Beneficiary)

Trustee

A three-party financial contract

Important Contractual Provisions in Real Estate Financial Instruments

• Parties to the contract

• Loan amount

• Term of loan

• Interest rate

• Amortization period

• Property description

• Priority of loan

• Acceleration clause

• Escalation clause

• Prepayment clause

• callable mortgage

• non-callable mortgage

Important Contractual Provisions in real estate financial instrument

• Due-on-Sale Clause

• Default Clause (put option)

• Personal Liability Clause

• Deficiency Judgment

• Foreclosure

• Redemption Rights

– Equitable right

– Statutory right

• Escrow Provisions

Loan Termination• Termination by satisfying contract

• ending lien against pledged property• trustee provides deed of release• defeasance clause

• Termination by mutual agreement• Refinance• Recasting

• Deed in lieu of foreclosure• Termination by foreclosure

Theories of Mortgage Law• Legal steps after default to apply property to payment of the

debt

• What is default

• Theories of mortgage law

• lien theory

• title theory

• intermediate theory

• Types of foreclosure

• foreclosure by court action and judicial sale

• foreclosure by power of sale contained in document

Redemption Rights

date ofdefault

Foreclosuresuite filed

Foreclosuresale

End ofStatutory period

Equitable Right of Redemption Period

Statutory Right of Redemption Period

FORECLOSURE PROCESS